Six months or so ago, shortly after a flurry of attention in the US around the 10 year bond rate dropping below the three-month rate (which had been something of a predictor of weaker economic conditions) I wrote a post here on yield curve indicators in New Zealand. Once upon a time, we used to pay quite a bit of attention to the relationship between bond yields and 90-day bank bill rates although, as I explain in that post, it isn’t a great indicator of future New Zealand recessions (and wasn’t really used that way when we did pay attention to it).

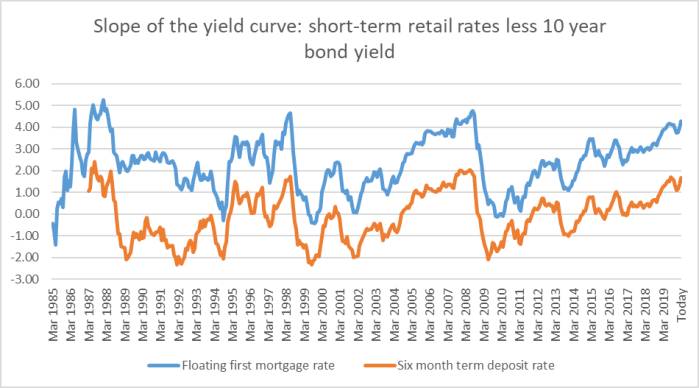

In the post I suggested it might be worth looking at a couple of other yield curve indicators, using the (fairly limited) retail interest rate data the Reserve Bank publishes, comparing short-term retail rates with long-term goverment bond rates. The absolute levels wouldn’t mean much, but the changes over time might. Here is a version of those charts updated to today (using current retail rates from interest.co.nz)

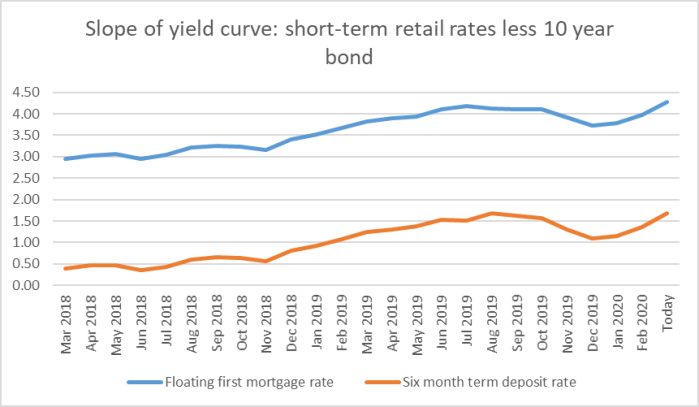

and the same chart for just the last two years.

For what it is worth, the only times these lines have been at or above current levels a New Zealand recession has followed. And although the Reserve Bank interest rates cuts in the middle of last year did reduce the slope of the retail yield curves, we are now sitting right back where we were at the peak last year.

The Reserve Bank is, of course, now strongly expected to cut the OCR this month – as Australia did yesterday and the US this morning, and as they should have done last month. But do that and they’ll only take those retail yield curve slopes back to around where we were late last year – and that on the assumption that long-term bond yields don’t fall materially further. By historical standards that will look like relatively tight monetary policy, at least on this indicator. And all that with credit conditions that tightened last year, look likely to tighten further because of the ill-considered capital requirement increases (they were warned about the risks that the transition period would cover, and exacerbate, the next major downturn) and – despite political rhetoric – are only likely to tighten further under the cloud of extreme uncertainty and actual/potential income losses currently descending.

In this climate, with the evident sharp slowing in economic activity, it would be more normal to envisage hundreds of basis points of cuts. But, through official lassitude and a decade focused more on hoped-for rate increases than on the next severe downturn, cuts of that magnitude simply aren’t an option.

The constant pushback against the idea of OCR cuts now (whether last month, right now, or later in the month) is that they won’t achieve anything much in coping with the immediate disruption and the (probable) rapid increases in job losses over the next month or two. And, of course, that is quite correct.

One also sees pushback using the argument that central banks shouldn’t be responding to share prices, noting that world markets are even now not much off their peaks. Whatever the merits of that argument abroad – and in general I don’t stock prices should (directly) drive monetary policy actions – it is pretty irrelevant here: in all my years of involvement in advising on New Zealand monetary policy, the only time share prices ever really entered deliberations was in October 1987, and even then it was only as a proxy for the serious problems developing just behind the scenes.

But the fact that monetary policy doesn’t have much affect in the very short-term, particular amid really disordered conditions, is really rather beside the point. If what you care primarily about is the employees and firms directly disrupted, there are plenty of direct options the government can, and probably is, considering. But that is simply a different issue, even if one that operates in parallel. Even direct short-term assistance won’t do much to slow the deterioration of economic aggregates – won’t summon up more tourists, won’t fill gaps in supply chains, won’t offset the decline in spending if/when social distancing becomes more imperative. By and large, we are stuck with whatever deterioration in economic activity the next few months bring, most of which will be events almost totally outside our control (overseas economic activity and the spread of the virus abroad and here). We can support individuals to some extent, and perhaps can do something to increase the chances firms will still be there when the pressures pass.

But in many respects, monetary policy is also about the second leg of that. It is about getting in place early – and providing confidence about – conditions that will (a) support the recovery of demand as and when the virus problems pass, or settle down, and (b) helping ensure against that the sort of precipitate fall in inflation expectations (in turn confounding the economic challenges) that I warned about in yesterday’s post does not happen. The importance of early and decisive action is compounded by several things:

- the physical limits to conventional monetary policy (can’t cut very far, so need decisive early action to keep expectations up),

- the probable political limits to fiscal policy (see 2008/09 globally)

- the extreme uncertainty about the course of the virus or the economic consequences (like any city/country, we could face northern Italy or Korean disruption at almost any time),,

- reasons to doubt just how rapid a recovery in demand will be (perhaps especially in tourism) and the likelihood of some – growing by the day – permanent wealth losses

All supported by the fact that, unlike other possible programmes, monetary policy action is readily reversible if the best-case scenario comes to pass.

I find two other thoughts relevant to the discussion. It seems almost certain that the price-stability consistent interest rate is quite a bit lower than it was just a few months ago. In normal circumstances, the job of the central bank is to keep policy rates more or less in line with that short-term neutral rate. It might well be – but no one knows – that the fall is temporary, but the Reserve Bank’s job isn’t to back a particular long-term view (they have taken to talking recently far too much about the long-term, when their prime job is really quite short-term, about stabilisation) but to adjust to pressures evident now.

(In the same vein, we also hear the objection that the virus issues are “short-term” and thus no action is warranted. Quite possibly, perhaps even probably, they are short-term, but so are most of the pressures central banks deal with. Most recessions for that matter, even most crises.)

And finally, it is worth bearing in mind that many commentators are already highlighting debt service burdens for businesses where activity has fallen away sharply, There are no easy answers to what the appropriate policy response, if any, is to those issues. But it is worth pointing out that there are likely to be permanent income/wealth losses, even if in a year’s time the path of GDP is back on the pre-crisis course. Income not earned this year is unlikely to be made up for by more income later. In the extreme, if the economy largely shut downs in certain cities or regions for a short time – or if certain sectors (eg foreign tourism) largely shutdown for longer – those losses will not be made back, and the debt (business and household, bank and non-bank, lease commitments and loans) that was being serviced supported by those actual/expected income flows will still be there. Those losses have to be (will be) distributed somehow and frankly it seems reasonable that part of that would be by adjustments to servicing burdens. People will say – commenters here have – that 25 basis points is really neither here nor there. And, of course, that is true. They will also say that the OCR is “only” 1 per cent – also true – but retail lending rates are over 5 per cent (floating mortgages) or 9 per cent (SME overdrafts), and in a climate like the present. Those rates really should be a great deal lower – at least temporarily – as, of course, should the adjustable rates being earned by savers/depositors.

Pro-active macro policy would be doing all it can, as soon as it can, whatever additional firm-specific measures the government might also try. To repeat, the point isn’t to fix the immediate situation – there is no such fix, absent the magic fairy curing the world of the virus overnight – but to limit the risk of longer-lasting damage and better position ourselves for what could still be a difficult recovery, with permanent wealth losses. The Reserve Bank should be taking the lead – it is conceivable that if they are going to wait until the scheduled review date that even a 100 basis point cut could be under consideration by then – but there is sufficiently little the Bank can do – even about that medium-term horizon, that we should have well-targeted and designed effective and prompt fiscal stimulus as well (again focused on the six to eighteen month horizon). If anyone influential is reading, I commend again – as one part of a response – the case for looking hard at a temporary cut in GST).