And so the die is cast and the motley crew (of, I’m sure, well-intentioned people) that make up our government have decided on a lockdown Liberties are shredded, but I guess people will still be free to shop at The Warehouse. It seems a curious business.

We must hope the strategy “works”, but the problem seems to be that (a) it isn’t clear there is a strategy (just another tactical choice), and (b) it isn’t really clear what “works” means here. The Prime Minister yesterday referred to those standard worst-case types of death numbers, that have been around pandemic planning for years. And she talked in terms of how the lockdown should probably dampen the local outbreak. But there was no sense of how we get from a four-week lockdown to the end, when the virus is no longer a threat (whether the hope of a vaccine is realised, or because a less-lethal version just becomes part of the normal mild perils of winter). In particular, there is no sense of how many lives any particular set of policy responses are credibly likely to save, in a world population with no underlying immunity. I guess the only honest answer is that no one knows, but it would be good to have sense from the government of the central estimates they are working with, and the confidence bands around those estimates. Without anything like that it is all but impossible for citizens to reach a view on the merits of any planned set of interventions, or a strategy.

There are various efforts around to attempt at least sketch outlines of a cost-benefit analysis (though typically of “policy intervention” defined very generally). Some people simply object to such exercises as somehow immoral in the face of the threat. I disagree. I think they can help frame some of the discussions society has to be having. Even if, say, you or I might give everything (if necessary our very lives) to save our children, that simply isn’t the way public health policy (or any other area of public policy for that matter) actually works. We make choices about costs and tradeoffs, whether it is about speed limits, food safety or (closer to this blog) bank capital.

A few weeks ago, I tried to tease out, in a back of the envelope sense, some of how one might like to think about the issues (towards the end ofthis post). A couple of extracts

According to the Treasury’s CBAx spreadsheet, the value of a statistical life (price community would pay to avoid premature death) this year is just on $5m. 25000 people at $5m each is $125 billion. However, the evidence so far – including the Chinese data – is that the deaths are very concentrated among older people. On the Chinese data – which may have its weaknesses – the median age of those dying looks to have been as high as the late 70s, whereas the median age for all New Zealanders last year was 37.3. Remaining life expectancy at 80 seems to be about a quarter of that at 37, so we can chop down that maximum possible saving (from avoiding premature deaths) to no more than, say, $31 billion.

But, of course, even that is too high, since the implicit assumption is that all those lives could be saved with appropriate policy responses. And from everything I read that seems incredibly unlikely. Often people seem to talk about using policy measures and costly private actions (distancing etc) to spread out peaks and reduce the intense, perhaps overwhelming, peak pressures on the health system, and thereby (a) reduce the number of deaths and (b) make the whole experience less intolerable for those who would die anyway and those who, while sick, live. Obviously I have no idea how many lives might be saved in total, but no one seems to seriously suppose it is anything like all of them. If it was half, it would – all else equal – be worth spending $15 billion or so to avoid those premature deaths.

Of course, there are other potential benefits to be added, including any sustained impairment of health (eg lung functioning) for some of those who recover.

Probably three weeks ago $15 billion seemed a really big number. Sadly, now it is chicken-feed relative to the output losses New Zealand will suffer this year. The loss in the June quarter alone could end up getting on for doubling that, if the lockdown gets extended much.

But in any such discussions, it is also worth bearing in mind that we need to think about marginal effects on both sides of the “equation”. How many lives will be saved over the next couple of years by the planned set of interventions vs the additional economic cost from the New Zealand’s government’s interventions. Both what the rest of the world’s governments do, and what the wider public (here and abroad) do anyway isn’t, in principle, relevant to the calculation. And a great deal of the economic losses we are now facing, and about to undergo, are already baked-in. There would be no tourists anyway, as just one example. There would be massive investment uncertainty. There would be increased physical distancing and postponement of events, and so on.

It is hard to put numbers on any of these items, but the discipline of writing the assumptions down, expressing realistic confidence intervals, articulating the basis for your judgements on each line item, and then disclosing that material to the public should be a part of what is going on now It is also at least partly about accountability, for some staggeringly big choices governments are making now, and look set to continue to make in some form or another for some time to come. I don’t have a strong view myself – interesting question to ask is whether, if there was a referendum today you would support the lockdown – but confidence in judgements being made is only likely to be enhanced if there is good, robust analysis underpinning those judgements.

(And here we should make only little allowance for the mad rush; they’ve had two months to learn from Wuhan and prepare and yet in all too many fields of government it is increasingly clear how little that time was used for serious bad-case planning and preparation. That seems particularly evident – perhaps just because it is my focus – in the economic policy area.)

Of course, the more immediate issues now are around economic policy. The interviews on the morning shows this morning suggest an announcement from the Minister of Finance later today around credit. Unfortunately, there is still no hint in any comments from the Governor or the Prime Minister that they are yet willing to do what is really needed. Simply being willing to extend credit to firms might be helpful, but it isn’t really the issue, because for many firms it simply won’t be worthwhile to borrow, taking on more debt against the totally unknown horizon at which something like normality might resume (hint, it isn’t after four weeks). We need a comprehensive system of income guarantees (80 per cent of last year’s net) for individuals and for firms that stay fully staffed and capable, for the year ahead. Just possibly, the guarantees would not prove to be needed for that long, but that is really beside the point now: what matters now is uncertainty and expectations, and not just for the next few weeks (still what the wage subsidy is doing). (My macro-stabilisation package here.)

This sort of guarantee is the sort of policy (“ACC for the whole economy” as someone put it to me) that will help buy a reasonable amount of time, and give firms some confidence in a willingness to take on debt (while still leaving each firms’ owners to make their decision about likely future viability). Is such a scheme likely to be expensive? Sure, but in a sense we paid the premium already, in that low public debt over the last few decades. We should expect the (unwritten, implicit) policy to be honoured, not obviously as some matter of law, but of charity and good economic sense.

The other thing where there is no progress evident at all is on securing a substantial easing in monetary conditions, and substantial relief of servicing costs (not so much the cash outlay as the legal liability) of borrowers. On RNZ this morning the Governor was talking up all his tools, but it all really amounts to almost nothing. He can do large scale asset swaps, and in doing so ease some pressures in specific markets. But monetary conditions are tightening and they need to be loosening a lot. He talks of the further tools he has at his disposal, but apart from easing specific stresses, they simply don’t amount to much, nothing like the scale of the need (and one of his own MPC, his chief economist) told us that just before the crisis really intensified).

Interest rates need to come a lot further down. Business and household borrowing costs at present probably should be no higher than zero. Even getting towards that would require the OCR to be set significantly negative. That can quite readily be implemented. It really needs to be done, and the indifference – and bluster, bordering on outright misrepresentations – from central bankers, including our own, on the failure to adjust interest rates is frankly quite incredible, ie almost literally unbelievable. OCRs don’t stop being effective at zero, it is just that too many central bankers stopping trying (while doing lots of handwaving).

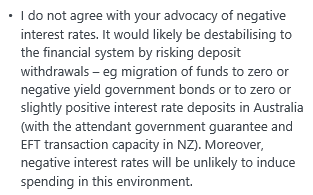

A former colleague, from mostly a banking supervision background, left a comment yesterday disagreeing with my call for negative rates.

I’m sure (well, know) he isn’t the only sceptic, here and abroad, but that isn’t going to stop me championing an idea whose time is long overdue (after all, the near-zero bound only exists because of government regulatory restrictions and monopolies – it isn’t a given of nature).

What to make of Geof’s specific arguments?

First, I don’t accept that it would be destabilising to the financial system at all – if anything, at the margin it would assist financial stability by shifting the burden from borowers (increasingly indebted in most cases) to depositors (time is offering no real return right now).

I also don’t belief that there would be anything like the sort of flight to Australia Geof suggests. After all, exchange rates – even NZD/AUD are volatile enough and transactions costs high enough – to swamp any possible small interest gains. Perhaps more to the point, in a floating exchange rate system, unless there is a run to physical cash – and recall that under my model cash would be more expensive to purchase/withdraw – the total deposits in the banking system do not shrink because someone seeks to withdraw money. For every seller of NZD there has to be a buyer. And, frankly, the more people wanted to sell NZD at present, the better – a materially lower exchange rate is one more helpful part of the stabilisation package.

Finally, Geof also notes that lower interest rates won’t do much to boost spending right now. That is, of course, true and a point I’ve been making throughout. The point of policy right now is not to boost spending (the time for “stimulus” will be later) but, in this case, to ease servicing burdens materially, and to help stabilise and reverse the falls in medium-term inflation expectations that risk materially complicating the recovery phase, by starting us off with higher real interest rates than those we went into the crisis with,

There is always resistance to paradigm shifts, and too many central bankers and the like are operating within a paradigm that simply isn’t open to negative interest rates – even though in New Zealand we went for years with substantially negative real rates a few decades ago. That really now needs to change, and fast. Our Reserve Bank could show the way. Our economic policy position, our stabilisation options, would be improved if they did.

UPDATE: I remembered that I meant to mention an idea a reader passed on this morning. Since many many businesses will fail anyway, and in many cases that may involve personal bankruptcies, in respect of personal guarantees of business borrowings, in this exceptional climate is there a case for considering cutting in half the period in which someone who goes bankrupt is unable to be involved in running a business. Like everything in this crisis, there are risks, but it might be an option worth some officials thinking about.