Yesterday afternoon we had the latest round of official comment from the Prime Minister and the Minister of Finance, at the post-Cabinet press conference (transcript here). It was really just more of the same. The Prime Minister, in particular, tends to play down the risks to New Zealand, and offers little effective leadership. Then again, the journalistic questioning didn’t seem very searching – no one, for example, asked about the rate at which Australian case numbers were growing and whether, with an open border and lots of travel (30000 arrivals a week from Australia) we aren’t really just in a Common Virus Area with Australia. “Wash your hands and carry on” seems to be the gist of her message – as, no doubt, it was for many of her overseas peers….until it wasn’t. There is still no pro-active discussion with the public about how the government is thinking of handling things just a little way ahead (do or don’t school closures play a part in their thinking, as just one example).

Much the same criticism can be mounted of their approach to the economic costs and dislocations, which will already be mounting by the day. There are signs – including in an RNZ interview this morning – of some greater degree of realism from the Minister of Finance, but he must be constrained in his public comments by the apparent political imperative to play things down, and focus on the China-related disruption rather than on the widening and deepening global situation, and the implications of that for New Zealand.

The Prime Minister and Minister of Finance announced the gist of the package of measures they will actually announce next week (the Minister’s statement is here). Even setting aside the lack of specifics, what they did announce still seems almost entirely backward-looking.

The Business Continuity Package includes:

- a targeted wage subsidy scheme for workers in the most adversely affected sectors.

- training and re-deployment options for affected employees; and

- working with banks on the potential for future working capital support for companies that face temporary credit constraints;

As if the biggest disruptions and dislocations are not still yet to be, and when they unfold their effects will be pervasive – almost every firm in the country will be hit to a greater or lesser extent.

Now, the Minister has said that he has officials working on longer-term options (and he is somewhat stymied by having a central bank – his Monetary Policy Committee – that isn’t doing its job). And that leaves me thinking that this “package” to date is as much about politics and being seen to be doing stuff – especially six months out from an election – as about a serious response to a worsening situation. Perhaps that is too cynical, but between Ministers and officials surely there is a recognition of what is near-certain to be, not far down the track?

It isn’t at all clear what sort of sensible dividing line the government has in mind for who is and isn’t going to be eligible (even now, won’t every business in Queenstown and Rotorua being feeling the effect?). “Training options” must have seemed like a good idea to someone, but if far-reaching social distancing is coming soon – as Siouxsie Wiles put it yesterday – it is hard to see polytechs etc effectively doing much of such training.

And, on the other hand, there seems to be no urgency around measures that might ensure adequate income support if/when we get to point where large numbers of people – across a whole range of sectors – simply can’t work (quaratined, self-isolated, or whatever) and their employers’ can’t afford, or won’t pay them.

Then, of course, there is what they won’t do

Media: ANZ’s chief economist says scrapping next month’s minimum wage increase in response to coronavirus is a no-brainer. Are you considering that?

Robertson: No.

PM: No.

Media: Will you consider it at all?

Robertson: No.

PM: I think, in fact, one of the benefits that we have—perhaps relative to other economies—is not only are we well placed in terms of low debt; our position around surpluses, the upgrade package, so that stimulus already going into the economy. Also we have to keep in mind what we need people to keep doing, of course, is continue to spend and consume. And so also the adjustments we’ve already had to benefits, and I would say, of course, what people are anticipating in their wages, is all part of continuing to keep the economy ticking over.

So they might a good talk about maintaining labour market attachment, but they won’t even consider postponing the next minimum wage increase. Minimum wage increases tend to have their most visible effects in downturns, amplifying the difficulty marginal new entrants and less-able workers have in getting (back) into a job. As I say, so far the economic policy response looks more like politics.

The one bit of the ‘indicative package’ that was new was this

- working with banks on the potential for future working capital support for companies that face temporary credit constraints;

That seems to be all we know for now.

But there is likely to be a significant issue there, one which is likely to get much bigger quite soon.

Hamish Rutherford has a piece in the Herald about this, drawing in part on a chat we had late yesterday. I suggested that one option officials might have in mind could be some sort of guarantee scheme. As far as we know, banks themselves don’t currently face funding constraints, so there shouldn’t be any need for direct government lending. But banks will become increasingly uneasy about continuing to extend new credit – increased overdrafts etc – to firms that already have a lot of debt, and where it isn’t clear when (or even if) normality in business conditions and cash-flows will resume.

One other reason why we really don’t want direct government lending is that government (Treasury, Reserve Bank or whoever) has few or no credit evaluation capability, and even less so in extremely uncertain unsettled times. If something is going to be done along the lines the Minister suggests, it needs to harness the interests and expertise of the banks themselves, who actually know about the businesses – and key individuals – they’ve been lending to.

I drew some parallels with the guarantee schemes the government put in place – supported by the Bank and Treasury – in 2008/09 for financial institutions. The retail deposit guarantee scheme generated a great deal of controversy, but the wholesale guarantee scheme – designed to help banks tap international markets – was pretty well-designed (in my view, but I was the principal designer): we didn’t guarantee what didn’t need guaranteeing, and we charged a fairly significant price to banks using the guarantee to ensure they had incentives to graduate from it as soon as possible. Broadly speaking, they were sensible interventions. But it is important to remember the context. Officials and ministers were pretty confident of the credit standing of New Zealand banks – finance companies were a different issue – (and, where relevant, Australian parents) – we were providing guarantees into an environment where the credit quality of those we were dealing with wasn’t materially impaired, but rather global funding markets had dried up almost indiscriminately. For what it was worth, we could also cross-check our judgements with market pricing – CDS spreads – and with the views of external ratings agencies.

None of that is on offer if the goverment is serious about taking on business credit risk now. Few New Zealand companies are externally rated, few have quoted CDS spreads. Most just are not that big or (their finances) visible to anyone much other than their banks and owners. And, of course, in many cases it would be the riskiest credits that banks would be looking to the government to support, creating major incentive and monitoring issues. For a firm that has next to no debt and substantial physical assets, support from their own bank isn’t likely to be much of a problem for some considerable time. But for the firms that were straining the tolerance of their bankers anyway, why would it be attractive for the government to take the risk? Most firms will be somewhere in the middle, but remember that those with the higher current debt levels and those now bleeding cash fastest will be the ones eyeing up the possibilities of government support. I really wish officials well trying to devise something workable, sensible – oh, and scalable when things get a lot worse.

(I haven’t really touched on the Reserve Bank’s new capital requirements. They will be accentuating the difficulties borrowers face this year, exactly as the Bank was warned in consultation last year – whack on large new capital requirements with the likelihood of a severe downturn in the next few years and you will materially exacerbate problems, when there are few other effective tools.)

On matters re the Reserve Bank we are to get from the Governor this afternoon some thoughts on how the Bank might approach non-traditional monetary policy when/if the limits of the OCR are reached. No doubt I will write about that material in the next few days, but in meantime as reference here is link to my post about an article the Bank published on the issues and options the Bank published a couple of years ago.

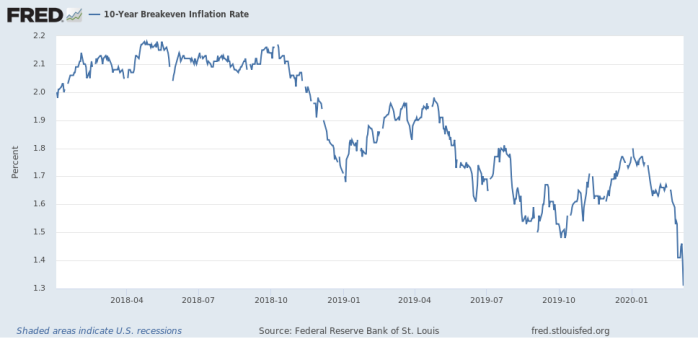

And finally, inflation expectations. I’ve been making the point that there really isn’t a great deal economic policy can do to limit the immediate costs and dislocations over the next few months, and that the focus should really be on getting in place early and decisively policies that will support a recovery as rapid as possible. Part of that – and a theme of mine throughout the life of this blog – has been avoiding any sharp slippage in inflation expectations, which risks “trapping” economies in a very difficult position even after the worst is over, given the current limitations on monetary policy. Real interest rates could be rising, not falling – and in the current environment it is probable that real retail rates should be zero or even negative. I’m sure all that seems quite abstract to many readers, so I wanted to end with a couple of concrete illustrations of the risk.

In this chart I’m sure the breakeven inflation rate for US government 10 year bonds (gap between yields on conventional and indexed bonds) as at the US close this morning.

These aren’t record lows, but the implicit expectations are much lower than they were averaging just a few months ago. Much of last week’s 50 basis point cut, simply stopped real interest rates moving higher. Now, sure, in tense periods these indicators can be thrown around changing (unobservable) risk premia, but this isn’t a time for complacency, when everyone knows there are severe limits to what more central banks can do. Rational agents will be revising downwards their future expectations, and to the extent they do that poses big risks – accentuating the deflationary climate that has been building for more than a decade now, not just in the US but throughout the advanced world.

What about New Zealand? This chart simply shows the gap between the Reserve Bank’s 10 year bond data and the yield on the September 2030 indexed bond. The latest observation is as at yesterday, but New Zealand 10 year bond rates don’t seem much changed this morning.

The recent movement isn’t as dramatic as for the US but (a) the starting level – not much above 1 per cent – was far too low already, and (b) the direction is clear, and concerning.

We need a much more pro-active central bank, doing its core job.

(In closing, it is curious to reflect that the biggest single form of stimulus to demand/activity in New Zealand since coronavirus become prominent is the spat between Mohammed bin Salman and Vladimir Putin and the resulting collapse in world oil prices. Who knows how large the stimulus effect will be – or how significant any countervailing havoc wreaked on, eg, US corporate credits – but whatever the effect it is larger than anything/everything our goverment and central bank have done.)