There was a new announcement from the Reserve Bank this morning. The two key elements, as summarised by Westpac are

A Term Auction Facility. The RBNZ will lend to banks for up to 12 months, taking Government bonds, residential mortgage-backed securities, and other bonds as collateral. This basically ensures banks will be well-funded for the foreseeable future. This will prevent an increase in the cost of bank funding, which in turn will help ensure that short-term interest rates for businesses and households remain low.

– FX swap market funding. Banks sometimes borrow money from offshore and swap the debt back to New Zealand dollars. In recent days the cost of performing this swap has exploded. Left unchecked, this could have caused an increase in the cost of funding New Zealand banks, which in turn could have led to higher interest rates in New Zealand. The RBNZ has essentially offered to facilitate some of those swap arrangements, which will keep the cost of overseas funding contained.

Both initiatives seem sensible, as (for that matter) does the rest of the statement (although the new Fed USD swap line is surely of symbolic significance only, recognition that we are a real advanced economy, since New Zealand banks tend not to have an underlying need for USD.

I’m guess the fx swap market activity will make a useful difference. But I wonder how much difference the Term Auction Facility will make though. I recall conversation with bankers at the height of the 2008/09 crisis who observed that their boards simply would not look at Reserve Bank funding – however reasonable the term – as a particular secure foundation on which to maintain, let alone expand (as it hoped for this time), their credit. Time will tell, but the Reserve Bank of Australia announced a much more aggressive package yesterday afternoon, including provisions explicitly allowing banks to borrow more – at very low fixed rates – to the extent they increase business credit this year.

There were also indications in the statement that the Bank has been dabbling in the government bond market

Supporting liquidity in the New Zealand government bond market

The Reserve Bank has been providing liquidity to the New Zealand government bond market to support market functioning.

But, as Westpac notes,

However, the amount of liquidity provided seems tiny so far, and has had little effect on longer-term Government bond rates.

Funding rates through the fx swaps market aren’t transparent to you and me. But bank bill yields are readily observable. As I noted in yesterday’s post they had moved much further above the OCR than one we normally expect (especially when the Bank has committed not to change the OCR itself). On this morning’s data, that gap is still 42 basis points (a more normal level might be around 20 basis points. When the goal is supposed to be abundant liquidity and interest rates as low as possible (consistent with MPC’s self-imposed floor on the OCR), there is simply no need or excuse for these pressures. Surely they aren’t worried about some spontaneous outbreak of inflation?

Similarly, here is the chart for the 10 year bond

il

In other words, barely below the levels at the start of the year, before any of us had heard of the novel coronavirus, let alone had our economies shredded by it. The 10 year rate appears to have dropped a little further this afternoon, but it is still well above where it probably should be.

The Reserve Bank of Australia yesterday announced a significant bond purchase programme designed to cap three year government bond yields at 25 basis points (with flow through effects on the rest of the curve. Our Reserve Bank has still done nothing of substance on that front – and our shorter-term government bonds yields are well above 25 basis points. Why not? Well, there is no obvious reason for the lethargy – inflation isn’t about to be a problem – other perhaps than that Orr and Hawkesby went so strongly out on a limb with their complacency about the situation, as recently as last week and this, and Orr has never been one to be willing to concede he might have got things wrong (despite being in a game where such errors are, from time to time, inevitable).

Ah, but perhaps inflation and inflation expectations are just where we want them. But no. These are the New Zealand inflation breakevens (difference between nominal and indexed 10 year government bonds.

Recall that the target is 2 per cent, and these are 10 year average implied expectations. Things were not that great anyway – not averaging much above 1 per cent in the last couple of years – but now we are down to 0.65 per cent. (It isn’t quite as precipitate as the fall seen in the US, but hardly comforting even if the data are harder to interpret than usual.) This risk – inflation expectations falling away, raising real interest rates all else equal – used to worry the Governor. Nothing has been heard of the line from him or his offsiders since it became a real and immediate threat.

There isn’t really much excuse for the MPC’s sluggishness and inaction. After all, they talked about bond purchases being next cab off the rank, and then markets went haywire, their peers in Australia acted, and they did nothing. Of course, it doesn’t help that it seems the Reserve Bank was seriously unprepared. You’ll recall that as recently as Tuesday last week, we had 19 pages of high level stuff on alternative instruments from the Governor, with the clear message he thought we were well away from needing them. We were promised a series of technical working papers “in the next few weeks” but despite the crisis breaking upon them almost two weeks later we’ve seen nothing. All those years they had to prepare, and it seems all too little serious preparation was actually done (as we now know – because they told us so – despite all the talk of negative interest rates as an option, it now turns out they’d taken now steps to ensure banks’ system could cope).

But none of that need stop the Reserve Bank launching a large scale bond purchase offer (or auction programme). It isn’t operationally complex. The Bank transacts these securities in the normal course of its business, and each year buys back bonds approaching maturity. There won’t be any systems implications.

I wonder if one other reason they are reluctant to act is a sense that then people would see how little the alternative instruments they favour actually offer. While they don’t act, there is a pretence that there is a big bazooka. But only while they don’t act.

As I’ve noted previously, I think there is fair consensus on the last decade’s unconventional policies in other countries: at times there were some real and significant benefits in case of specific market dysfunctions, but beyond that the beneficial effects were relatively limited. Asset purchases, with a policy-set OCR floor, have no mechanisms that would lower interest rates to bank customers. They’ll cap government bond rates, probably with some benefit to interest rate swaps rate, but the biggest effect will simply be to flood bank settlement accounts with a lot more settlement cash. And since that is a rock-solid asset (now) fully remunerated at the OCR itself, it won’t prompt material behavioural changes.

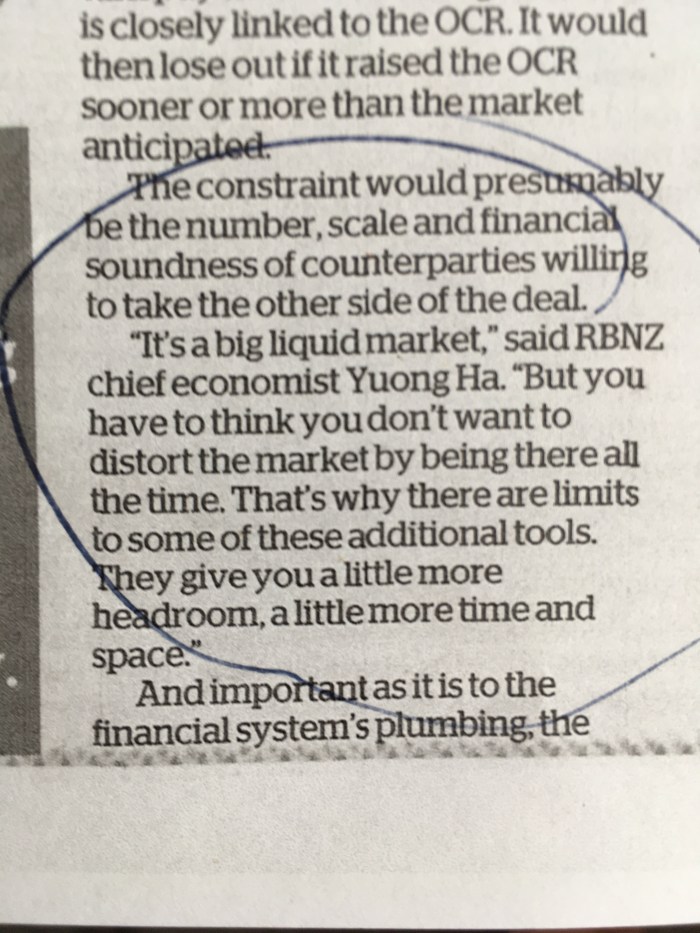

You needn’t just take my word for it. Last Friday in the Herald the Bank’s chief economist (and MPC member) Yuong Ha (who had spent some years monitoring financial markets in his previous role), was talking about alternative instruments (bond purchases, intervention in the interest rate swaps market and so on). He was quoted this way

These tools “give you a little more headroom, a little more time and space”. In some circumstances “a little” might be all the situation demands. In these circumstances it is grossly inadequate and simply no substitute for failing to act on interest rates.

That is part of why I think they should get on now and do the large scale bond buying, or even buying foreign exchange assets. With an interest rate (OCR) floor in place it just won’t make much macro difference, the emperor’s new clothes will be exposed for what they are(n’t), and perhaps we might finally get some focus on the crying need to get retail interest rates lower.

Recall the Bank’s claim that bank systems aren’t ready. For a start, this should be challenged, and some naming and shaming should go on. Apparently some banks aren’t ready, but others are. Name them. Second, at least for wholesale products all the big banks must be finel – lots of financial products abroad have had negative interest rates for several years, and our own inflation-indexed bonds were trading at negative yields at times in recent months. Perhaps as importantly, actual retail rates – and it is probably the retail components of some banks’ system that are the issue – are still well above zero, both term deposit rates and retail lending rates. If the OCR – a wholesale rate – could be set to, say, -2.0 per cent (without triggering conversions to physical cash on a large scale), term deposits might still be only around zero, and retail lending rates higher again. There is a lot of space the Bank could use to drive retail rates down without even having to envisage negative rates for the main retail products. In times like the present every little helps. (As an example of the issue, the Australian banks today announced a scheme to freeze debt repayments for SME borrowers for six months, which is fine, but those borrowers are still paying an interest rate of perhaps 6 per cent, in a climate where time – which is what an interest rate is mostly compensating for – currently has no, or perhaps negative, value.)

Perhaps the Bank, The Treasury and the Minister of Finance are now cooking up some decisive intervention to support the credit system as a whole rather than just extending government loans to the iconic and politically connected Air New Zealand. Such an intervention is sorely needed, and once again the government is behind the game. The credit system is probably the most pressing point right now, but it is no excuse for the MPC, an independent operator, to be not doing its job. The times demand a large easing in monetary conditions, including in real interest rates. The Bank is delivering almost nothing, all while playing smoke and mirrors with the suggestion that its next instrument offers much more potential than is really there.

Once more our key decisionmakers fall short.

There would be nothing to lose now by bold and decisive action. Nothing.