Any guesses as to which country currently has the highest number of coronavirus cases per capita? I’d have got this one wrong, until I happened to spot a table yesterday with some numbers for San Marino.

Anyway, here are the top ten for total cases per million people (data updated to 1pm).

Leave out the tiny countries/territories and the next few are Switzerland, Norway, Singapore, Sweden, and France.

On these standard lists of countries and territories – no matter how tiny – there are about 230 countries/territories. At present, New Zealand is about 60th (ie lower end of the worst quartile – probably not the impression you’ve had from the Ministry of Health or ministers). Here is a chart of which countries are, right now, just a bit better/worse than New Zealand.

Australia, with which we have a pretty open border and lots of movement across it, has about three times the cases per capita.

I’m not sure that the per capita numbers mean a great deal, especially when very small absolute numbers are involved. One infected family or small cluster here and we’d quickly go shooting up past Taiwan, and despite the confidence the Ministry of Health (and their Minister) keep expressing in public, neither they nor we know what they don’t know. They presumably know most of the contacts of the people with confirmed cases, but none of the contacts of the cases they don’t yet know, let alone the contacts of those contacts. It is striking how much open alarm there now is in the United States – active cancellation of events, top universities moving to online only etc – even though in the per capita ranking the US isn’t much different than New Zealand (in fact, as recently as Saturday morning was a bit further down this unwelcome league table than us). Perhaps it is a reminder that three weeks ago, Italy had no confirmed cases and now (eg) million people and the heartland of the Italian economy are in quarantine. Two weeks ago, Italy had the same number of confirmed cases the US has now.

Of course, the other aspect of some relevance is the trajectory of cases numbers over time. Singapore, Hong Kong, and Taiwan all have had more cases per million than New Zealand. A few weeks ago there was a real fear of an exponential increase in those places, perhaps especially Hong Kong, where the travel restrictions from the PRC had been imposed only fairly sluggishly and the numbers moving were large. And yet in all three places, the exponental increase hasn’t happened. In fact, in Singapore and Hong Kong more than half of all the people with confirmed cases have now recovered. Presumably the virus isn’t any different, so we should look to behaviour, policies and practices.

Our government and Ministry of Health like to talk up the travel ban, but (eg) Hong Kong never really had one (and places like Australia and the United States did). What seems much more striking about Singapore and Hong Kong was the extent of social distancing that has been practised for some weeks now. In Hong Kong’s case, schools and universities were closed. In Singapore, they weren’t but reports suggest huge numbers of people working from home etc. That also seems to have been the lesson in how the PRC got on top of the virus, notably outside Hubei province. I like to reason by reference to cross-country comparisons, and so it surprises me how little of the debate or media coverage here is looking through the range of other advanced country experiences. Instead, we seem to get endless backward-looking upbeat comments from the Prime Minister, Minister of Health, and the Ministry of Health, who seem only interested in encouraging anything much more than hand-washing when it is confirmed that things really are much worse in New Zealand. They seem reluctant to (a) acknowledge what they don’t know, (b) the nature of incubation periods (if/when things are confirmed to be much worse, we’ll wish policies and practices at least a couple of weeks earlier had been different. There is a line I read recently that suggested that whatever a country does before a pandemic really breaks out will seem too much, and whatever it does afterwards will seem too little. With other country’s experiences to go by, it isn’t obvious why our authorities are encouraging such a relaxed attitude. Surely none of us wants to end up a Lombardy?

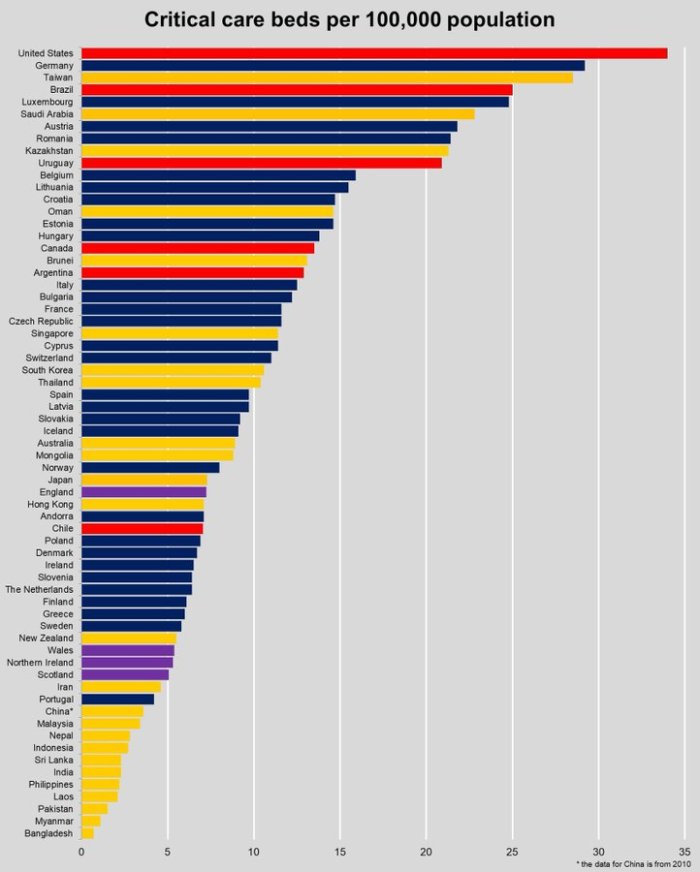

Where, of course, ICU beds are a real constraint, so much so that over the weekend there was mention of an Italian technical discussion document mooting the possibility of denying ICU care the very old. I also happened see this chart over the weekend. (Assuming these numbers are roughly comparable, you have to look a long way down this chart to find New Zealand.)

All of which is a bit of a distraction from the main – economics and economic policy – focus of this blog. I’m running late today because The Spinoff asked me to write a short piece this morning elaborating some points I’d made earlier in a radio interview. Here is what I wrote there, with some elaborations and additional points I didn’t have space for.

The economic implications of the Covid-19 public health emergency are formidable, and are growing by the day.

Most of what we’ve seen in New Zealand so far relates to the epidemic stemming from China and the steps taken to get things under control. Much of the policy discussion, including recent comments from the minister of finance, seems to have focused on attempts to assist firms and individuals in sectors which directly affected.

But that approach risks being a big mistake. It might have been fine if the only material outbreaks of the virus had been in China, and once they got things under control it was only a matter of time – albeit perhaps months – until those specific sectors and firms can get back to normal. But that simply isn’t what we face. Only yesterday the Italian government quarantined one of the major industrial regions of Europe.

Realistically, we have to suppose northern Italy won’t be the last place where life and production will be severely disrupted. The trajectories of case numbers in various other European countries seem, to date, disconcertingly similar. And then there is the United States.

Public health experts tell us the virus can be checked, but only with expensive and disruptive restrictions – voluntary or imposed, here or abroad. In her latest column here, Siouxsie Wiles notes:

Another thing we are all going to need to start doing soon is minimising or avoiding contact with other people. This is called social distancing. If you are greeting people, don’t hug, shake hands, hongi, or kiss. Bump elbows or feet instead. Work from home if you can. Much as it pains me to say it, social distancing also means avoiding public transport (get on your bicycle!). Similarly, it means avoiding gyms, churches, cinemas, concerts, and other events and places where people congregate.

Already, airlines report that forward bookings have dropped away sharply, and foreign tourism is heading towards zero for a time. It won’t be the only severely adversely affected industry, and the effects will be felt widely.

I found it very interesting that Wiles – who seems to know whereof she speaks on the viral things, and seems to be no panic-monger – was prepared to use, of New Zealand, the words “we are all going to need to start doing soon”. That isn’t at all the message our happy-talking political and official leaders are giving.

Economic policy needs to be focused not primarily on the limited and concentrated economic disruption we’ve already seen. Instead, ministers and officials need to focus on the much, much larger, but scale-uncertain, losses and disruption that will soon break on us, and on vulnerable individuals rather than firms. As importantly, we need to be positioning ourselves to ensure that when the epidemic passes – and that could be some time – we are positioned to get overall demand and economic activity back towards normal as soon as possible.

Much of the economic loss and disruption we are near-certain to face over the next few months is now all but unavoidable. Nothing we do will put tourists back on plane, or open up supply lines from Milan, or whereever the next place to clamp down severely is. When people choose to stay home and maintain those distances, spending and economic activity will drop. It is the price we will pay as governments here and in other countries seek to spread out and reduce the incidence of the virus itself, and as individuals seek to limit our personal risks.

This point cannot be made too often. Between choices here and individual and policy choices abroad much of the economic disruption is simply unavoidable. There will be large losses of production, significant jump losses, material numbers of business failures, and significant permanent losses of wealth. Much of what any spending can do now is really more (re)distributional in nature, than about changing the short-term course of GDP. There is place for such distributional measures – we don’t want sick people at work who can’t afford to take time off – and in my view short-term measures should probably focus on income support, erring on the generous side where necessary.

Trying to directly assist individual firms is a fool’s errand. We just don’t know what we will be dealing with just a few weeks from now. Very soon the number of firms that can plausibly claim adverse effects will be huge. We simply don’t have the capacity to administer complex tailored schemes for huge numbers of firms, and the way would inevitably open up to all sorts of rorts and abuse.

To repeat, facing what is likely to unfold over the next few weeks or months, we need systems that are clean and relatively simple, and don’t rely on either government or the recipient firms being fully resourced to manage them.

That is why we have macroeconomic policy tools, which are designed to operate pretty pervasively when activity across the economy is hard-hit.

Monetary policy is typically the main one. The Reserve Bank is already quite badly behind the game in not having cut interest rates. No doubt they will do so later this month, but they need to cut the OCR hard, and to err on the side of what might look like doing too much. The risks of actually doing too much are slight, and the risks to falling short are substantial. Among them is a risk that expectations about future inflation drop materially further, which would raise real interest rates in the face of this severe and complex shock, greatly complicating the eventual recovery.

But monetary policy is approaching its limits. This is one of those (quite rare) times when monetary policy really needs to be supported by a significant and, when activated, fast-working boost from fiscal policy.

The OCR can probably be cut by up to 175 basis points. Whether the last few cuts make any real difference, even to the exchange rate, is a contested point, but we won’t know if – faced with big drops in activity in demand – the limits aren’t pushed.

Big infrastructure projects are largely beside the point here – they simply take too long to get under way. One-off cash payments to households probably also aren’t the right thing, at least now. In the next few months people will be hunkering down anyway, and as I’ve already noted, a key consideration is providing support and confidence as and when the worst of the virus – and attendant direct economic disruption – has begun to pass. One possible tool, as part of a package, would be a significant, explicitly temporary, cut in the rate of GST.

Such a cut could be implemented quickly, would put more cash directly in the pockets of households, would operate in a somewhat progressive way (poor households spend a larger share of this year’s income than upper-income households) and explicitly encourages people to buy early rather than later (because you know prices will be rising again in, say, 18 months hence when the GST rate goes back up again).

This instrument was used in the UK in 2008/09. The key point I’d add here is that in thinking about stabilisation and supporting recovery in the next 12-18 months we – including political parties from all sides of politics – shouldn’t be focusing on our longer-term preferrred policy changes, but on things that are likely to do the stabilisation job (and can then probably be unwound – as monetary policy). That is also the way towards keeping a reasonable degree of cross-party consensus if the crisis is being welll-handled, rather than a sense that one side or the other is using the crisis opportunistically.

The key point now is that the government has to be looking forward, not backwards, and acting in ways that take seriously the sheer scale of the costs and dislocations we are just about to face. Whatever New Zealand does, we can’t avoid many of the short-term costs that are coming, but we can do a little to mitigate the damage (in an environment like this, for example, retail interest rates probably should be near zero, which they aren’t now) and official actions now can help create a climate most supportive of an eventual recovery. We need people to be confident of aggressive action focused on the real issues. In these circumstances, there are few or no returns to half-measures.

All manner of stresses and problems are likely to come to light, here and abroad, if this virus continues to wreak havoc – or require far-reaching restraints (self or government imposed) over the next year or more – to keep it in check. It would be foolhardy to assume that full recovery will be quick and easy, all the more so if macro policy has not done what it could to, for example, keep inflation expectations up.

Where is the RBNZ in all of this?

They don’t want to comment on the current state of the economy on Tuesday and they just released a trite comment about the banking system.

I just don’t get them. They cut 50bp in August when it was marginal as to whether it was appropriate and now they do nothing as the temple implodes.

Where’s the leadership ?

LikeLiked by 2 people

Fundamentally unfit for the roles they hold – esp Adrian of course, but formally he is still only one vote on the MPC.

LikeLiked by 1 person

Agreed. Now is the time for action.

If I were Governor, I’d have called a MPC conference call. I would have suggested we cut 50bp right now and that we stand ready to do OMO’s and widen collateral – and broaden that to non-bank FI’s if needed – and I would release a very short Statement.

Today, the Reserve Bank cut the Official Cash Rate 50bp, to 0.50% in response to global economic and financial turmoil. The Reserve Bank stands ready to take further action if and when necessary. We also stand ready to provide short-term liquidity to the New Zealand financial system as required. Ends.

LikeLike

The current shock is not a systemic failure of credit. The banks are not short of liquidity to lend. The problem we currently have is that the RBNZ has placed restrictions on lending with its macroprudential tool restriction on Equity in LVR. They need to relax this restriction.

Also Australian Bank staff now do not have performance targets in lending after the Australian Royal Commission removed bank lending performance targets which has flowed onto their NZ subsidiaries. Previously we could get loans approved within a day.

These days bank staff are just plain lazy with loan applications taking at least 15 days to a month to complete an assessment when bank staff feel like they want to do some work to get a bonus.

LikeLike

Good thoughts. The only issue i can think of with a GST cut is families which live hand to mouth, week to week won’t have any cash to spend if they’ve lost their job. That means the progressivity of GST cuts would be less. That’s what gets me about macro stuff: it avoids the personal micro tragedies. Like CS Lewis argued in The Problem of Pain, giving everyone in the world some paracetamol will cut the net pain (increase wellbeing?) experienced by a large amount, but it (paraphrasing) sucks to be the person who just had surgery to just have para.

LikeLike

As I’ve said, I have no particular problem in erring on the generous side re access to benefits, incl for people who’ve exhausted sick leave. Apart from anything else, there is a wider public interest in sick or self-siolating people staying home.

Bear in mind that even in the worst depression most people don’t lose their jobs.

LikeLike

will be intersting to see what the flow on effect of oil price decreases will be, and raises the opportunity for the tax on petrol to be lowered – rewards people who get out and about and will be of benefit to most homes and business, plus easy to implement

LikeLike

question v soon will be whether we want people “out and about”. Far-reaching social distancing – endorsed by authorities – probably isn’t far away.

LikeLiked by 1 person

Hi Mike

Not really relevant to this post but I am curious why Adrian Orr is giving a talk on unconventional monetary policy options tomorrow but the Minister of Finance has explicitly ruled them out today.

Given the Governor would be breaking new ground with unconventional monetary policy would normal protocol before floating the options have involved a discussion with the Minister first?

If I was the Minister I would have been inclined to suggest the RBNZ test the limits of conventional policy immediately.

LikeLike

I’ll give Adrian some benefit of the doubt here. They have been promising for months – going back at least to the Nov MPS to release something like this early this year. From the advisory last week, they still intend to frame it as “in the unlikely event it is ever needed”. i’d be surprised if they haven’t had discussions with Robertson and Tsy about the hypothetical tools etc, but I guess Robertson still has a political need now (not sure why) to try to minimise what is going on and suggest it is just about a few industries and regions.

Of course (a) in principle, a document like this should have been out, socialised, debated etc several years ago, and (b) it is a bit odd Adrian saying he is going to do a “short speech” tomorrow, when you could presumably have put in out with no more than a foreword from him.

LikeLike

Within Europe, Italy seems a clear outlier (at this stage), what went wrong there? A bit late in moving, bad luck etc. – struggling to find a logical/credible explanation…?? I.e. any lessons for NZ

LikeLike

From what i’ve read it looks as tho Italy’s outbreak got going first, but that the rate at which case numbers are expanding in France, Germany, Belgium, Netherlands etc is following much the same path as for Italy just lagged a couple of weeks. One hopes not, but….

LikeLike

These words from a local blogger have merit. They might be hard nosed, but they go to the fragility of the froth of the NZ economy

Read and digest slowly

“Businesses in the tourism sector already have their hands out. These are businesses that for years have creamed the benefits of endless tourists pillaging New Zealand’s landscapes. Did they not save any money for a rainy day? Did they not see that once China or Chinese tourism went elsewhere they would have a problem?

Of course not, many operators have been creaming the good times, buying up property, boats and fast cars enjoying their new found wealth from the nations prostitution that is tourism. Saving the cash earned? Oh heavens no, we will just use it to borrow even more! Many operators are not truly local and just send their cash offshore anyway.

The restaurant industry, severely overpopulated already, has its hand well out. Many are pure immigration scams anyway and struggle to survive even in boom times. The hoteliers at least in the main centres are going gangbusters if you look at the current hotel prices, try getting a decent hotel room in Auckland over summer for less than $300 a night.”

LikeLike

Do you have a link to the original?

LikeLike

Yes I read that one as well. It’s from Cactus Kate Michael: https://asianinvasion2019.blogspot.com/2020/03/dont-panic-businesses-already-have.html

LikeLike

Thanks

LikeLike

She’s still going? I thought she gave it all up. Oh well.

LikeLike

I really appreciate your views on the economic impacts of covid 19. What are your brief thoughts on the latest Government support and intervention package (although still not finalised)? https://www.interest.co.nz/news/103969/government-develops-business-continuity-package-including-support-coronavirus-affected

LikeLike

Watch for tomorrow’s post. Mostly it seems to fall foul of my critique: looks backwards not forwards. The credit proposal is interesting – and there is a real issue there – but problematic in practice.

LikeLike

About 250 ICU beds in NZ and about 5% of infected need a couple of weeks in ICU. When we hit 5000 infected. (0.1% of NZ population) and hospitals are overwhelmed people will start to die as if there was no hospital system. With 2 weeks in ICU our hospitals can only handle about 2.5% of population getting infected each year. Most everyone over and above that rate of infection will be denied ICU treatment:

the peak number of infected is likely to be more than 10x that 5000ish limit.

So my view is

1/ There will necessarily be brutal triage – older patients will likely be denied treatment in preference to younger, faster recovering patients. Eg we might have enough ICU beds for parents with school age children. Everyone else will likely have to fend for themselves, and death rates will be much higher than the 1-2% possible with good treatment. Wuhan was 7-8%.

2/ There is little to no point in drawing out length of epidemic ‘stretching the curve’ as all but a tiny fraction are going to be denied access to life saving ICU’s anyway. Unless we could miraculously manage to hold it down for a year or two until a vaccine is available, or dramatically increase number of ICU beds in coming months.

3/ Immediate massive country wide quarantine now is the only move that the govt can make if they want to stop this – otherwise they will be passengers in this ride just like us.

LikeLike

Your conclusions – stark as they may be – are the hard facts as far as they can be ascertained from what has played out over the last few months. Yet hardly anyone I meet seems remotely aware that this is the case. Toilet paper hording notwithstanding, they underestimate the severity of this virus.

LikeLike

Well written and informative.

It is a lot to absorb with the conflicting reports.

One question is why hasnt Russia shown up in any of the stats?

In fact she has gone very quiet.

Makes me wonder.

Are there no cases there??

LikeLike

Russia seems to have had about 20 cases so far.

LikeLike

David Chaston at interest.co.nz sums it up nicely

“The economic clean out has begun. The world is having the correction it needed, the one put off relentlessly by fiscal and monetary authorities. Events are overrunning them and their depleted ammunition”.

Now the clean-up begins

LikeLike

Economic activity in NZ will recover quickly when China can get their factories up and running again. Our food exports have been held up in Chinas ports and will pick up once China gets up and running again.

Big correction in the stock exchanges but house prices remain quite bouyant. The RBNZ has yet to unleash its macroprudential tool ie Equity restrictions on LVR. From a property perspective, the old are still getting older and even if we lose 5,000 we still have massive firepower with our immigration net gains of 60,000 a year. Losing an extra 5,000 old folks does provide a gain to Universal Super and other Superannuation funds.

Not too sure what economic clean out David Chaston is referring to because this shock slowdown feels more like the starting gates of the Ellerslie Race Course?

LikeLike

Micheal

As far as Singapore goes, my firm like many is working split shifts, one team from home and one in the office, then swap and the two shall never meet. Twice daily temperature checks whether at home or the office, uploaded to MoH by the company or building management. Of course MoH has draconian powers in the event of any sign of infection. Although it’s noticeably quieter out, it’s not as if social life has ended. I still go to the mall for groceries.

I’ve been traveling the last couple of weeks, on return to Singapore there’s the temperature screening. Arriving in Delhi there is screening and a declaration to be completed, though unlike Singapore screening was not automated. There was literally one guy with a thermoscan checking each passenger from a (half empty) A380. Bangkok screening is automated and Jakarta at least has multiple manual screeners and a health form to be completed.

Restaurants in Singapore are offering all sorts of deals to get customers in but the home delivery folks are making a killing!

LikeLike

Thanks for that

LikeLike