I was exchanging notes last week with someone who is doing research on New Zealand economic policy, and the development of economic institutions, in the 1980s and 1990s. In the course of that conversation he sent me a copy of interesting short paper – presumably obtained from the national archives – from the period when the thinking and debates that led to the Reserve Bank of New Zealand Act 1989 were underway.

Reform of the Reserve Bank had been in the wind for some time. Loosely, the Reserve Bank tended to be keen on an independent central bank, and recognised that some accountability procedures would be part of the price of that. On the other side of the street, the Treasury was keen on an accountable and efficient central bank. Neither institution – nor the key ministers at the time – wanted the Minister of Finance to be determining day-to-day monetary policy. (Ministers determining policy adjustment had been the standard practice, by law, for decades – and it was the practice at the time in most western countries, the exceptions being Switzerland and West Germany and (more or less) the United States.) Everyone involved wanted a much lower average inflation rate than New Zealand had had in the 1970s and 1980s.

The Treasury was heavily involved in work on reshaping the institutional form of much of what central government did. Of particular relevance was the new state-owned enterprises (SOE) model, adopted for many/most government trading enterprises (NZ Post, for example, is still with us today). The Reserve Bank, then as now, was a somewhat anomalous organisation and part of the – at times – acrimonious debate between the Reserve Bank and the Treasury over several years reflected the idiosyncratic nature of the institution, and differing views over what parallels or comparators were relevant. For example, were banknotes or the retail government banking operations, or the sale of government bonds really just commercial activities really just commercial activities. And might the (apparent) policy goals be achieved better in an organisation given more commercial incentives.

At one end of the spectrum was a proposal out of The Treasury in late 1986 to turn the Reserve Bank into an SOE (it was never quite a final Treasury proposal, but was written by a senior Treasury adviser and taken seriously as the highest levels of The Treasury. For anyone interested, you can read more about it in Innovation and Independence, the 2006 history of the Bank (bearing in mind that that history was very much written from a Reserve Bank perspective, one of the authors not only having been an active protagonist in the late 1980s debates but at the time of writing serving as chair of the board of the Reserve Bank).

The proposals were stimulating, far-reaching (including allowing for the Reserve Bank to be declared bankrupt and statutory managers appointed) and – in the views of probably all Reserve Bankers involved at the time (and in my view now) – quite unrealistic, and failing to really grapple with the reasons for having a central bank at all. I am one of those who believes that the economy and financial system could function adequately without a central bank – although on balance I think a central bank can improve our ability to cope with severe shocks – and in many respects the logic of the Treasury position might have been better developed into a proposal to explore whether we could do without a central bank altogether. But they didn’t. (Had the Bank been abolished, my position – then and now – is that New Zealand would fairly quickly have become a de facto part of the Australian dollar area, with monetary conditions influenced by the RBA with Australian perspectives in mind. That is probably clearer now than it was then – in 1986/87 only Westpac and ANZ of the larger banks were Australian owned.)

But the point of this post isn’t to rehearse all the old debates. I was overseas on secondment at the time, and only got involved in the debates (which lingered in various forms for several years, even after the Reserve Bank Act was passed) a bit later. But I was intrigued by this one particular paper I was sent last week.

The Reserve Bank has received the “Reserve Bank as SOE” proposal in November 1986. At the time, the Reserve Bank Board was the decisionmaking body for the Bank itself (although not on monetary policy, which was in law set by the Minister). The Board asked management to obtain independent expert analysis and advice on the Treasury ideas and for their March 1987 meeting the Board had in front of it a six page commentary from Professor Charles Goodhart.

Goodhart is one of the more significant figures in the last 50 years or so in thinking and writing about central banking. At the time, he was Professor of Money and Banking at the London School of Economics and had previously served as Adviser to the Governor of the Bank of England. He had relatively recently published an influential book The Evolution of Central Banks: A Natural Development? (and had been the star guest, and guest lecturer, at the Reserve Bank’s somewhat-extravagant 50th anniversary celebrations in 1984). Goodhart was very smart and thoughtful, but well-disposed to a traditional (British) view of central banks.

A decade later, Goodhart served as one of the first members of the UK Monetary Policy Committee, after the newly-elected Labour government in 1997 gave the Bank of England operational independence in the conduct of monetary policy. But in 1987, the Bank of England was, to a considerable extent, the executing agent for the policy choices of the Chancellor of the Exchequer – the Chancellor being advised by both the Bank and the Treasury, and typically being closer to The Treasury (in the UK ministers have their offices in the department for which they are responsible, not something akin to the Beehive). It is worth noting that by 1987 the UK had successfully lowered its inflation rate very substantially (the UK inflation record in the 1970s had been, if anything, worse than New Zealand’s).

It is perhaps also worth noting that when the Reserve Bank of New Zealand Bill was finally brought to Parliament in 1989, Goodhart played an important role in providing public support (including FEC testimony) for the chosen model. Part of that involved providing an academic counterweight to the New Zealand academic (macro)economics community, most of which, at very least, sceptical of the legislation.

But that was 2.5 years later, long after the notes for the Reserve Bank Board had been written. In those notes, Goodhart’s stance – while useful to the Bank in countering Treasury – was very different to the legislation he later provided public endorsement to.

The first half of the paper (history and theory) is interesting, but not particularly controversial for these purposes. But the second half is about “policy conclusions”, drawing from an analysis that was generally in favour of (a) discretionary monetary policy, and (b) a central bank not influenced by profit-maximising considerations.

Here is his view on who should do what

Get the Minister of Finance further away from the conduct of monetary policy and let the Reserve Bank itself decide what rate of inflation to target. (This was more than year before “inflation targeting” itself became a thing, and was presumably just about setting a broad direction for policy – in New Zealand at the time there was, for example, beginning to be talk about “low single figure inflation”).

I don’t suppose that idea went down overly well with his Treasury readers (including the Secretary to the Treasury who was then a member of the Board).

One of the later mythologies that developed around the Reserve Bank Act (over the years we spent a lot of time rebutting it) was that the Governor’s salary was tied to the inflation target. It never was. But until reading this paper I hadn’t realised where the possibility of making such a link had come from. Here is Goodhart, talking about accountability.

Wow. At this stage, there was still no sense of making the Governor the single decision maker, but a leading academic writer on central banking was seriously proposing not just that the Reserve Bank should be able to set a target rate of inflation for itself, but that a range of key executives should be partly paid in the form of options that would pay off if the target was met. He doesn’t seem to notice, for example, the distinction between a private business (operating in a market it can’t control) and a public agency able to do whatever it takes, at whatever short-run cost, to achieve a target rate of inflation.

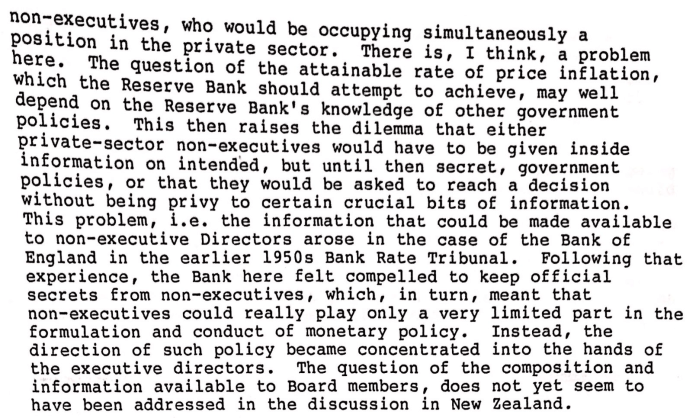

At the time, there was still a presumption that decisionmaking at a reformed Reserve Bank would be made (ultimately) by the Board – as, of course, responsibility in SOEs and many other Crown agencies rested with the respective boards. The Board was largely non-executive (Governor, Deputy Governor, Secretary to the Treasury plus other members appointed by the Minister) and Goodhart moves on to discuss the issue of whether non-executives could be involved in monetary policy decisions.

Reasonable points in some respects (how to manage potential and actual conflicts has been an issue even in the recent appointment of members of the new MPC), although note that in Australia the Reserve Bank of Australia Board – which sets monetary policy – is very similar in composition to the way the RBNZ Board was in the 1980s.

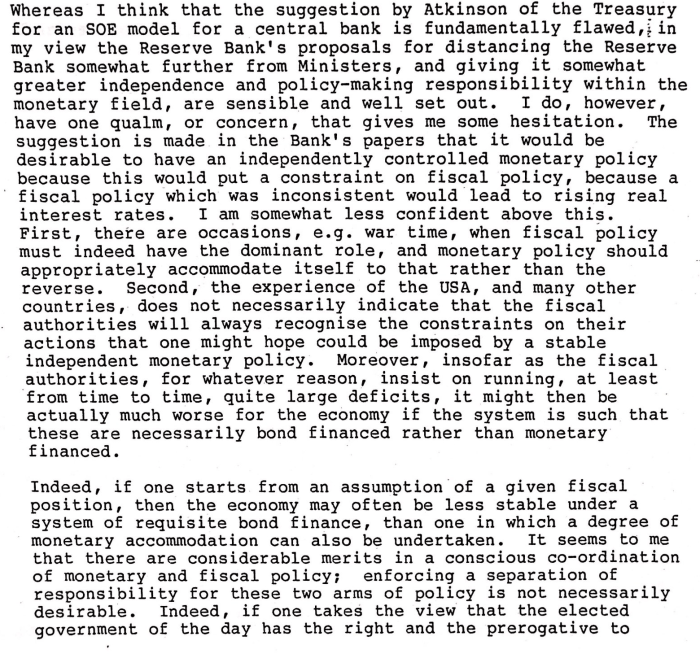

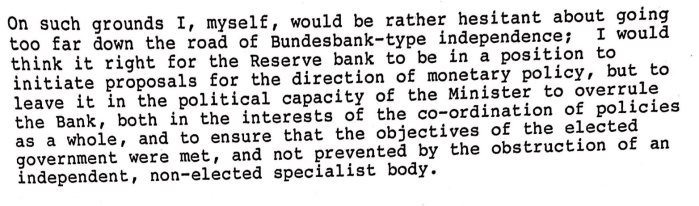

Perhaps more interesting is about the qualms Goodhart has – in early 1987 – about the case for an independent Reserve Bank, in particular around the case for a more active coordination (at least in some circumstances) of fiscal and monetary policy.

Goodhart’s paper ends with this paragraph.

If you were generous, you could interpret the final Reserve Bank of New Zealand model as looking something like that paragraph. Unlike the Bundesbank, the Reserve Bank of New Zealand never had the power to set any specific policy objective for itself, and there was explicit override provisions built into the legislation allowing the government to (temporarily) override the agreed (Governor and Minister) policy targets. But this paragraph sounds a lot more like the Bank of England in the 1980s, than the case made in public for the Reserve Bank of New Zealand Act 1989 (much of which was about having as few residual powers for Minister as was consistent with getting the legislation through the Labour Party caucus).

If you were generous, you could interpret the final Reserve Bank of New Zealand model as looking something like that paragraph. Unlike the Bundesbank, the Reserve Bank of New Zealand never had the power to set any specific policy objective for itself, and there was explicit override provisions built into the legislation allowing the government to (temporarily) override the agreed (Governor and Minister) policy targets. But this paragraph sounds a lot more like the Bank of England in the 1980s, than the case made in public for the Reserve Bank of New Zealand Act 1989 (much of which was about having as few residual powers for Minister as was consistent with getting the legislation through the Labour Party caucus).

In fairness, the Bank asked for these comments from Professor Goodhart at relatively short notice. On the other hand, he was at the time a leading academic writer in the area, and a former senior practitioner. And so I am still struck by the conflicting strands of thought that one finds in this short paper – on the one hand, the idea of options to reward senior central bank staff for meeting a target they might specify themselves, and on the other a real concern about the potential disadvantages in separating fiscal policy too far from monetary policy, and thus some ambivalence about too much operational autonomy for the Reserve Bank at all.

Having said all that, in a way what struck me most about the Goodhart paper is what wasn’t there. The UK’s disinflation experience in the 1980s had a wrenching one. Economic historians will still debate the contribution of monetary policy to the peak of three million people unemployed, but no one seriously doubts it played a part. At the time, there hadn’t been many economywide costs to the degree of disinflation New Zealand had so far managed – the credit boom and stock market excesses were still in full swing- and for a time that was to induce a degree of complacency among New Zealand advisers (I recall a meeting I was in perhaps a year or so later at which the then Deputy Secretary to the Treasury was telling the IMF about how modest he expected the costs of disinflation to be – the head of the IMF mission politely begged to differ).

But in this paper there is no mention of output costs at all – either those associated with getting inflation down to a much lower average level, or the short-term deviations of output from potential that would come to play such a large role in central bank thinking in subsequent decades. Just none. It is quite extraordinary (and thus when Goodhart talked about tying staff pay to the inflation target, no sense of the political impossibility of giving central bankers financial bonuses for actions that would, at least temporarily, raise unemployment – even if one could accurately and formally specify a binding target for the life of the options he proposed).

What of Reserve Bank staff ourselves? From mid-1987 I was Manager of the Monetary Policy (analysis and advice) section at the Bank, and thus quite heavily involved in clarifying what it was we were going to target, how and when. If memory serves, I think many of us were probably too complacent, perhaps a little blind, around the short-run issues, and tended to work on an over-simplified mental model in which once inflation was lowered to target all we really had to worry about were things like oil price shocks or GST adjustments (we didn’t explicitly – and probably not implicitly – think much about significant positive or negative output gaps developing).

On the costs of disinflation itself, we were (on the whole) more realistic, but to some extent that depending on the individuals. There were “battles” between what might loosely be called “the wets” and “the dries”, the former tending to emphasise the transitional costs and the latter the medium-term goal. Some of the wets (I was mostly of the other persuasion) probably doubted that the 0 to 2 per cent inflation target, adopted in 1988, was really worth pursuing. Perhaps what united us was a belief that a lot of other reform – greater fiscal adjustment and more micro reform – would reduce the costs of getting inflation sustainably down.

Some 20 years ago now I wrote a Bulletin article on the origins and early development of the inflation targeting regime. In that article, I tried to capture some of competing models that influenced the legislative framework (a funny mix of independence – not trusting politicians – and accountability – not trusting officials and having ministers hold them to account). I also reported some extracts from some of the papers we wrote (I often holding the pen) as the target came together. From one early and somewhat ambivalent paper (and I can’t recall why shipping got so much attention that month)

Moreover, the Bank noted that “the potential improvements in living standards to be derived from more rapid and complete removal of import protection, and the deregulation of such grossly inefficient sectors as the waterfront (already under

way) and coastal shipping, far outweigh the real economic benefits of slightly faster [emphasis added] reductions in inflation”. In an early echo of what later became a dominant theme in subsequent years, the Bank argued that if price stability was to be pursued over a relatively short time horizon, everything possible needed to be done at least to try to influence expectations and wage and price-setting behaviour.

This post isn’t about having a go at Charles Goodhart, The Treasury, the Bank, or me and my colleagues who were working on some of this stuff at the time. Mostly, it is just about history, and the sober perspective that history often provides – things that seemed clear at the time seem less clear with the perspective of time, and some things – that one later realises are really quite important – that hardly get attention at all. If it is an argument for anything, it is probably for more open and deliberative government and policy development processes, perhaps even for incremental and piecemeal (in Popper’s words) reform. That probably never appeals to reformers – perhaps especially not young ones – and perhaps there are occasions when it can’t be (practically) the chosen path, but blindspots are all too real.

As for the Reserve Bank Act 1989, if there were mistakes and weaknesses in its design (most especially the single decisionmaker model), it did probably serve New Zealand fairly well for several decades. It was, almost certainly, superior to the Atkinson/Treasury scheme. And yet one can also overstate the difference legislation really makes – Australia having made a similar transition to low and stable inflation under legislation still much as it was first passed in 1959.