Monetary policy matters.

Other things matter more of course. Even in the economic area, the long-term prosperity of a country and its people is affected very little by the quality of the country’s monetary policy. But the short to medium term matters too. And monetary policy can make quite a difference to how the economy performs, and the employment opportunities open to its people over horizons of typically a couple of years, but potentially stretching out to five years.

So it is encouraging to find various people weighing in on how monetary policy should be conducted – partly on the questions of where the OCR should be right now (about which there will always be quite a bit of uncertainty even if everyone agreed on what target monetary policy should be pursuing), but more importantly on what target monetary policy should be aimed at. In this post, I’m going to disagree with several recent contributions to the debate, but differences of view are vital if there is going to be debate at all.

Of course, many of these issues are addressed and dealt with – passively or actively – in the design of the Policy Targets Agreement. Those documents matter, a lot. In the PTA, the Minister of Finance constrains the otherwise unchecked power Parliament gives to a single unelected individual (a person in turn chosen by faceless company directors with no democratic mandate or public accountability) to run monetary policy as s/he chooses. The process behind agreeing the PTA is clothed in secrecy – even years afterwards the Reserve Bank refuses to release the relevant papers. It needn’t (and shouldn’t) be so. This isn’t just a bureaucratic piece of paper, but the design of the policy “rule” that will govern New Zealand’s short-term stabilization policy for the following five years.

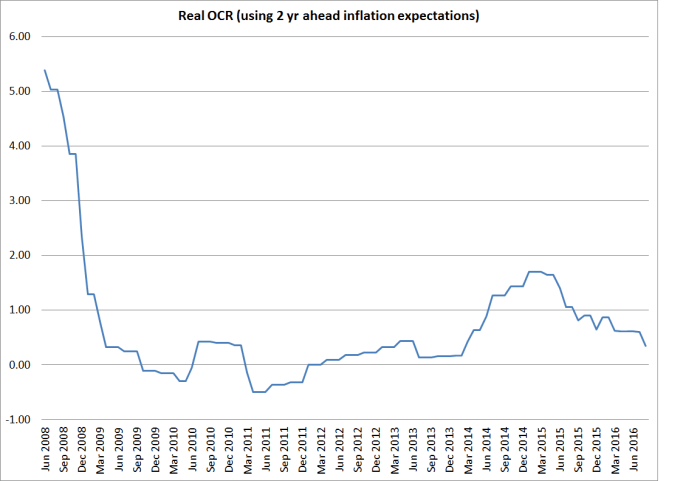

I’ve noted previously the much better approach taken in Canada – where the Bank of Canada had an open process of research and reflection in advance of the next review of its equivalent of the PTA. There is no reason at all why New Zealand shouldn’t do that, and more. Instead of relying on occasional passing comments from the Minister of Finance or the Secretary to the Treasury about their views on the (absence of a) case for substantive change to the PTA, the Treasury and the Reserve Bank, supported by the Minister of Finance, should be promoting an open research programme, inviting outside submissions, and looking to host a conference/workshop early next year where interested parties could engage and offer advice to the Minister and whomever the Board determines will be next Governor. Among the many issues such a work programme might look at is how best to design the policy rule to cope with the risk that New Zealand hits the near-zero lower bound in the next five years (as an illustrative piece – see Fig 1 – by a senior Treasury economist highlights, it is hardly a trivial risk). It might seem uncomfortable for the Bank – once upon a time, as an insider, I’d probably have pushed back too. But it is what open government should actually look like. In practice, we all know that ex post accountability for monetary policy judgements means little in practice (perhaps inevitably so). Getting the “rules” right at the start – and appointing good people, which probably includes shifting towards a committee decision-making model for monetary p0licy – probably matters more. (For avoidance of doubt, I’m not championing any particular changes to the PTA, although there are a few matters that could usefully be tidied up.)

But to come back to the various contributions to the debate that I’ve seen over the last few days.

In their weekly commentary, the ANZ economics team says they will offer some more detailed opinions on the framework “down the track”, but for now they offer two suggestions:

It’s arguable whether CPI inflation is the right target. It might be better to include a basket of various price indices. Some back-casting to see whether policy and economic outcomes would have been improved under different targets or a basket would also be useful

We need a better framework for driving more co-ordination between fiscal and monetary policy. …there are limits to what monetary policy can do. It is now widely appreciated that fiscal policy and structural reform need to do more heavy lifting to generate better growth outcomes globally. But that is easy for many to say when there are no mandates or requirements to follow through. Monetary policy needs mates

On fiscal policy, I offered some skeptical responses to the ANZ’s thoughts in this area last year. I remain skeptical. If they are arguing for a more expansionary fiscal policy at present (as they were last year) it is a recipe for a higher exchange rate, and no higher growth (other than around the near-zero lower bound, monetary policy offsets the demand effects of fiscal policy). I’m not opposed in principle to greater coordination of fiscal and monetary policy – and as we near the lower bound on interest rates it may become more important – but now hardly seems the time for more spending. Our debt isn’t that low, and that borrowing capacity could yet be very important. If “monetary policy needs mates” in the current context, some mix of more extensive land use deregulation and reduced medium-term immigration targets look more appropriate. But both would make sense on their own terms, whether or not monetary policy faced particular challenges.

But perhaps the more interesting question is whether the CPI itself is the “right” target. There is no compelling theoretical reason to prefer CPI inflation over any other of the range of possible nominal targets (individually or in combination). One could think of using various wage indices, the private consumption deflator, nominal GDP, a differently constructed CPI, or perhaps even the exchange rate itself. One could target levels instead of rates of change. One could, to be deliberately absurd, consider anchoring to the price of tomatoes, or the prices of houses or – oh, we’ve been there before – the price of gold. Plausible arguments could be mounted for most of those options. We ended up, 25 years ago, settling on the CPI (more or less) because it was prominent measure, somewhat understood by the public. There wasn’t a huge amount of analysis behind the choice at the time – and we knew the CPI had its pitfalls, more so then than now – but it has stood the test of time. Almost all the countries that have adopted inflation targeting, use CPI-centred targets. The important exception, the US, uses the private consumption deflator.

Having said that, it is also important to recognize that monetary policy has never just been driven off the CPI inflation rate. First, there are all manner of exclusions and adjustments to get to a sense of where some “core” or “underlying” measure of CPI inflation is right now. Few people, for example, are particularly bothered by the fact that annual headline CPI inflation is currently 0.4 per cent. What bothers them more is the interpretation of that data – hence the range of estimates suggesting “core” CPI inflation is probably somewhere in a range of 1 to 1.5 per cent. And, as importantly, policy has never targeted current inflation. No matter what the Reserve Bank did it couldn’t make any material difference to inflation for the September quarter of 2016. So policy looks ahead to forecasts of (CPI) inflation. But when it looks ahead a couple of years, the precise index the Bank is using doesn’t matter very much. Their forecasting models embed assumed relatively stable relationships among the various elements of the economy – and if they think the economy is going to evolve in a way that will lift pressure on resources over the next few years, that will show through typically in whatever variable they are forecasting – whether it is the CPI, private consumption deflator, wages or whatever. Some of those series might be more volatile than others, and so if one did shift to using them as the basis for the PTA target, one could have to take that into account in the design of the PTA. One can’t simply assume that all the rest of the parameters of the PTA could sensibly be left unchanged if one replaced CPI with some other price/wage/income index as the centerpiece of policy. The LCI, for example, is much less variable than the CPI – so small movements in it tend to matter more.

I’m not, at all, opposed to further work being done on evaluating alternative rules. But my prior is that most of the alternatives would make little difference (when evaluated using forecast data). The bigger issues – and disputes – have not really been about what index the Reserve Bank might be targeting but about (a) their overall read on the outlook for resource pressures, and (b) which risks they choose to tolerate. Neither seems likely to have been much different if they’d been handed a different index (and a suitable target for that index) some years ago. They – and most of the market economists – thought inflation (however defined) would pick up quite strongly (hence the presumed need for such large interest rates increases). They were wrong, but a different target wouldn’t have changed their model of how they thought the economy was working.

Shamubeel Eaqub’s latest weekly column has thoughts along similar lines to the ANZ’s. but he is a bit more specific, arguing (if I read him rightly) that the Reserve Bank should be charged with targeting an index that includes house prices.

There is nothing sacrosanct about how our CPI treats housing (actual rents, and the cost of constructing a new house, but not the land price). It isn’t an uncommon approach – and is used in Australia for example. One could easily argue for an alternative approach – the one used in the US (and in our private consumption deflator) – in which actual and imputed rents (the latter in respect of owner-occupied houses) were used, but not construction costs. That latter approach was long the preferred option of the Reserve Bank, and I still have a hankering for it. In fact, for a few years in the early days of inflation targeting, for accountability purposes the target was expressed not in terms of the CPI, but of an alternative index that used the imputed rents approach. But for the last 20 years, the Reserve Bank has been content with, and positively endorsed, the current “acquisitions” approach.

Eaqub argues that if land prices had been included in the CPI – I’m not sure what weight he envisages – inflation on that measure would have been “2.5 per cent or more for the last three years”. Perhaps so, but we’d also have switched to using an index that was much more variable than the CPI, and that greater variability would need to be taken into account in writing the PTA. Moreover, given that the combination of land regulation and immigration policy (or tax policy problems, as Eaqub might argue) have imparted a very strong upward bias to real land prices over several decades, that would also need to taken into account in setting the appropriate target range. It seems to be an argument that would have led to higher real interest rates over history. But, if so, it is worth reflecting that we’ve already had the highest interest rates in the advanced world for the last 25 years, and a mostly overvalued real exchange rate to match. I’m not sure how exacerbating those imbalances looks preferable to what we’ve had. Add to the mix of challenges that monetary policy runs off forecasts, and no one has good forecasting models for urban land price fluctuations. and at best I think such a suggestion would require a lot more in-depth evaluation. Or we could just fix up the structural distortions that mess up our urban land market – but not, say, those of Houston, Atlanta, or Nashville.

The final contribution to the monetary policy debate that I wanted to touch on today was a thoughtful column by my former Reserve Bank colleague (now apparently the chief investment officer for a funds manager) Aaron Drew. Aaron believes that interest rate cuts are doing more harm than good (globally and in New Zealand). In taking that view, he isn’t alone. The BIS in particular has at times argued that the world would be better off if only central banks got on and lifted policy rates back to some more-normal level. I’ve thought there was a germ of an insight there in that monetary policy can’t make much difference to the long-term structural prospects of the economy – and the biggest challenges many countries face are the widespread decline in productivity growth.

Beyond that, I think the argument is just wrong. After all, we’ve already twice tried the experiment of raising interest rates in the years since the 2008/09 recession. Both prove rather short-lived experiments. Aaron cites two arguments in support:

Two key arguments are made as to why cutting rates may be making things worse rather than better. The first is essentially a confidence argument. Cutting rates to very low levels, and in the extreme case to negative levels, signals that things are very wrong with the economy. Households and firms react to this by pulling-back spending.

The second key argument is that cutting interest rates to very low depresses, rather than boosts, household spending because the negative impact it can have on savers and the retired outweighs positive impacts elsewhere.

On the first of these arguments, I’d question just where the evidence anywhere is to support it. It is certainly true that whatever forces have led central banks to adopt such low (or negative interest rates) are extraordinary – out of our range of historical experience. And the associated weakening of income growth prospects should have led people to become quite a bit more cautious – prospects now just aren’t as good as they seemed 10 years ago. But if central banks simply pretended those pressures weren’t there, it doesn’t suddenly make them go away. But whatever the arguments about negative interest rates, that isn’t an issue New Zealand currently faces – our OCR is still higher than the US’s policy rate has been at any time in the last seven years or more.

The second is an empirical matter. Aaron argues that, in contrast to the usual experience, in the current climate lower interest rates are dampening demand and inflation, not contributing to raising them. It could be so, but it isn’t obvious why it should be. He emphasizes the adverse impact of low interest rates on those – the retired – consuming from the earnings of fixed income assets, as well as on those saving for retirement. But the flipside of that approach is the lower servicing costs of debt – especially for the people who already had debt outstanding before the latest surge up in house prices. And real interest rates have been falling for 25 years now.

But even if the income effects in New Zealand did work in Aaron’s direction, the substitution effects don’t. All else equal, lower interest rates make it more worthwhile to do a project today than it would have been without that interest rate cut. And, perhaps more importantly, for all the fuss around exchange rate movements on the day of MPS announcements, I don’t know anyone who thinks that if New Zealand had kept interest rates much higher – and Drew is quite open that he was arguing against cuts (and still thinks he was right to do so) even a year ago – we would not have a higher real exchange rate today. That was the certainly the view the Governor took last week, and I agree with him.

There are some nasty distributional implications of what has gone in the last decade. Many of the old are unexpectedly much worse off (but most aren’t because most are largely reliant on NZS). The implications for other age groups are much less clear. But distributional consequences are an almost inevitable part of unexpected real economic changes. If there aren’t the high-returning projects to generate lots of new investment, the value of (returns to) savings will fall. Central banks can’t alter that, and any slight difference they can make will be marginal at best. As I noted yesterday, it is not as if central banks are holding policy rates down while long-term bond rates linger high. Rising house prices are , of course, a big burden on the young – but, at least technically, that effect is easily mitigated, by reforms to land use regulation and/or changes to immigration policy. And recall that in real terms, nationwide house prices today are little different than they were in 2007 – when interest rates were much much higher.

Aaron claims he doesn’t want to abandon inflation targeting, but I’m not sure what his alternative would practically look like. He thought the OCR was already too low last year when it was 3 per cent. Perhaps he is right that raising the OCR back to, say, 3.5 per cent would lift business and household spending and raise inflation. But the evidence to back such a strategy seems slender at best. To adopt such an approach would involve the Reserve Bank going out on such a limb – adopting an approach so different to every other advanced country central bank – that we would have to impose quite a burden of proof on anyone advocating such a strategy.

This post has got longer than I expected. Apologies for that. There are important issues and debates to be had. We should be encouraging the debates, and associated research programmes, not assuming that the answers are already all in.

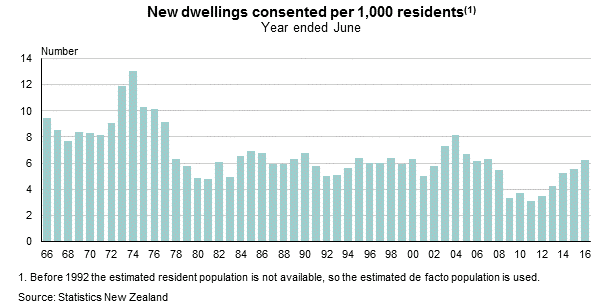

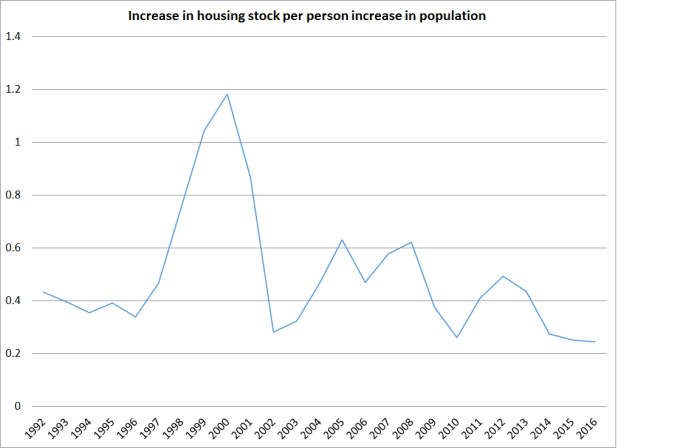

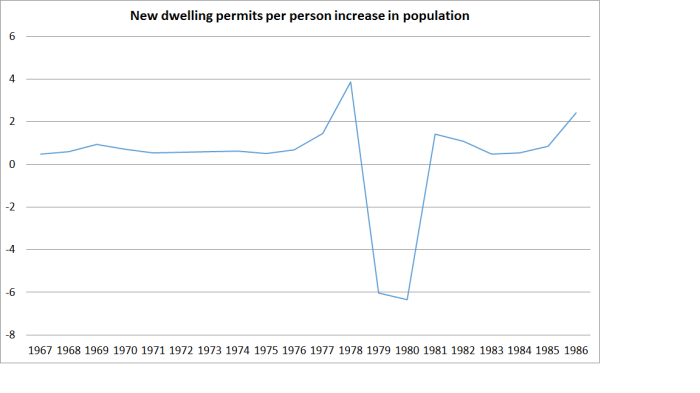

What happened? Well, in the late 1970s the large scale outflow of New Zealanders got underway, and the number of non-citizen immigrants had also been scaled right back. In the years to June 1979 and June 1980, the population is actually estimated to have fallen slightly, and yet 18000 and 15000 new dwelling consents were granted in each of those two years. For the three June years from 1978 to 1980 there was no population growth at all, and yet there were more than 50000 new dwellings consented. No wonder that over the late 1970s and through to around early 1981, New Zealand experienced the largest fall in real house prices (around 40 per cent) in modern history.

What happened? Well, in the late 1970s the large scale outflow of New Zealanders got underway, and the number of non-citizen immigrants had also been scaled right back. In the years to June 1979 and June 1980, the population is actually estimated to have fallen slightly, and yet 18000 and 15000 new dwelling consents were granted in each of those two years. For the three June years from 1978 to 1980 there was no population growth at all, and yet there were more than 50000 new dwellings consented. No wonder that over the late 1970s and through to around early 1981, New Zealand experienced the largest fall in real house prices (around 40 per cent) in modern history.