Six months or so ago I was getting a little frustrated by talk suggesting that low inflation was just one of those things. No one else, it was implied, was succeeding in meeting their inflation targets, and so we shouldn’t really be expecting the Reserve Bank of New Zealand to meet the target the Minister of Finance had set for them.

And so I wrote a short post about Norway. It was a small advanced economy, which has had substantial issues around rising house prices and high household debt, and which had been hit by an even nastier terms of trade shock (falling oil prices) than New Zealand had faced. Oh, and Norway has typically had lower policy interest rates than New Zealand (so perhaps less room for manoeuvre), and has a higher inflation target (2.5 per cent rather than 2 per cent). Like New Zealand, they started raising policy rates again quite soon after the 2008/09 recession (and crisis conditions) ended, but they realized that wasn’t necessary and reversed themselves. Unlike our Reserve Bank, they didn’t make same mistake twice.

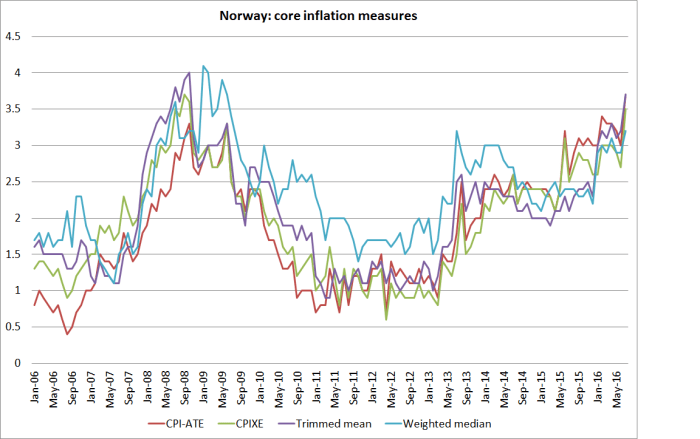

Norway also saw its inflation rate fall away quite sharply in the aftermath of the recession. Here is the suite of core inflation measures that the Norges Bank itself highlights – recall that the target is 2.5 per cent inflation.

Inflation – even core inflation – seems to be more variable in Norway than in New Zealand. It was very low in 2011 and 2012, but has been trending back upwards for several years now. When I wrote about Norway last in February, these core measures averaged 2.5 per cent. Core inflation has increased further since then, now averaging 3.5 per cent (although the Norges Bank observes that they expect it to settle back nearer 2.5 per cent).

It isn’t as if Norway’s economy has been booming. Indeed, Norway’s unemployment rate – while still below New Zealand’s – has risen quite markedly in the last few years.

No doubt there are lots of other detailed differences between the two countries’ experiences, but it seems to me that the biggest of them has been the New Zealand policy mistake – promising to raise the OCR aggressively, then doing so, and only reluctantly reversing that mistake. Here are two countries’ policy interest rates.

Here are the BIS index measures of the two countries’ exchange rates.

In Norway, the central bank doesn’t anguish about tradables inflation being negative for years and outside their control. Here is the chart from a recent Norges Bank MPS that I reproduced in February.

And here are two-year ahead inflation expectations in the two countries – the Reserve Bank survey for New Zealand, and a survey measure for Norway that I’ve taken from their MPS.

And here are two-year ahead inflation expectations in the two countries – the Reserve Bank survey for New Zealand, and a survey measure for Norway that I’ve taken from their MPS.

It looks a lot like a story in which

(a) the Reserve Bank of New Zealand badly misread (actual and prospective) inflation pressures,

(b) leading them to raise the OCR when they should have been holding or cutting it,

(c) which drove the exchange rate up (the juicy prospects of high and rising NZ yields)

(d) and drove tradables inflation more persistently negative than it should have been

(e) all while the Reserve Bank only very slowly realized its error, never explicitly acknowledged it, and only very reluctant reversed the rate hike cycle,

(f) all of which understandably dampened expectations of future inflation quite a long way, while still suggesting to people looking at NZD assets that if there was ever yield to be found anywhere in the OECD the RB woiuld do its utmost to make sure that place was New Zealand.

As a result, the exchange rate (while quite variable) stays high, inflation stays low, and inflation expectations are at constant risk of falling further. All because the Governor (and his advisers) got things wrong, and refuse to convincingly change tack. As I noted yesterday – and as several others have now pointed out – the Governor was given an easy opportunity to affirm that he’d do whatever it takes to get inflation back to target. For whatever reason, he simply passed up the opportunity. People, probably quite rationally, think he will in fact be very reluctant to do what is needed.

Frankly, if Norway can get inflation back to (and even beyond) target, so can we. It is mostly a matter of (a) reading inflation pressures roughly correctly, and (b) really wanting to. The Governor – and his advisers – have failed on both counts.

It isn’t always true, but sadly over the last few years it wouldn’t be wildly wrong to suggest that New Zealand outcomes would have been better over the Wheeler years if the Governor and his senior team had simply taken a holiday, and done nothing at all to the OCR for four years. We’d have avoided the badly misjudged tightening cycle, and although the OCR would still be a bit higher now – it was 2.5 per cent when Wheeler took office – inflation expectations would almost certainly be higher, and so real interest rates would, most likely, be no higher at all. That would have had the incidental benefit of leaving New Zealand more headroom against the risk of hitting the near-zero lower bound at some point.

Perhaps spurred on by criticism in various quarters that the Governor doesn’t make himself available for searching interviews, he seems to have established a pattern of talking to the Herald after the release of the MPS. The latest sets of questions and answers is here. It is all pretty soft-soap stuff, with no follow-ups or challenges, allowing the Governor to get away without even answering the question (as here, where he – in customary style – injects a variety of interesting but not very relevant detail, while not dealing with central issue.)

Rate cuts are supposed to bring the currency down, this didn’t. What’s happened?

Since the June statement we’ve seen the Bank of Japan ease, Bank of England ease, we’ve seen the Reserve Bank of Australia ease. If you combine that with quantitative easing that is larger than at any other time – and it was pretty large in 2009 – and with negative interest rates in countries that account for a quarter of world output, you’re just in a phenomenal situation.

There is no doubt the world is in a puzzling situation, but the Bank – and the Governor – are paid to do a competent job, not to end up sounding as if it is all too hard and is someone else’s fault. I’m sure his markets staff had advised him that the probability of the exchange rate rising yesterday was quite high – if they didn’t, they certainly weren’t doing their job. The Governor simply made a choice – he is a reluctant cutter, and that became clear once again yesterday.

It is a shame that the Herald, given the privileged access, didn’t ask a few more questions such as:

- Why didn’t you cut by 50 basis points, given that your own forecasts suggests further OCR cuts will be needed, and that on those forecasts it is still another two years until inflation gets back to target?

- Why are you so apparently indifferent to an unemployment rate that has now been above any NAIRU estimate for seven years?

- What plans and preparations are you putting in place to cope with the possibility that New Zealand finds itself exhausting the limits of conventional monetary policy?

- Inflation was below 2 per cent when you took office, has not been near 2 per cent since then, and on your own forecasts won’t be back to 2 per cent until a year after your term ends. You and the Minister put the 2 per cent midpoint explicitly in the PTA. How would you assess your performance in respect of the Bank’s primary responsibility, monetary policy?

I’m really glad to see someone kicking against the prevailing notion that just because CBs haven’t done enough, that there’s nothing they can do. I know at least some journalists read this blog.

My belief is that if the RBNZ actually got ahead of the curve for once, house prices would fall not rise.

LikeLike

With the advent of internet buying prices and the current worldwide production overcapacity, cheap oil prices and fast freight, interest rates have only a minimal effect on the inflation effect on prices. Competition is rife. In order to get prices into the inflation band you would have to effectively create a blockage on free flowing goods and services from overseas ie a tax or a import duty on incoming goods and services.

LikeLike

you mean, do something quite different than Norway did?

When inflation was really low and the terms of trade were falling they cut real interest rates to new lows, and the exchange rate fell.

LikeLiked by 1 person

Norwegian tariffs for industrial goods are low, usually between 3 % and 6 %. Goods imported from an EEA country are free from import duty. Any import of products is subject to Value Added Tax, which is currently levied at 25%. The VAT is deductible if the goods are intended for use in a VAT chargeable business. Before sending a shipment of considerable value, it might be wise to obtain an official ruling on customs treatment from the Norwegian Customs and Excise Authority.

Special duties and other duties and fees are levied on imported alcohol, tobacco, soft drinks, batteries, sugar, candy, foodstuffs, cassettes, cars, boat motors, lubricants, other motor vehicles, oil, gas coal, other petroleum products, plants and parts of plants and radio and TV receivers and accessories. Tariff rates for agricultural products are considerable. The Customs Tariff can be found on the Norwegian Customs and Excise webpage.

https://en.portal.santandertrade.com/international-shipments/norway/customs-procedures

LikeLike

The NZ dollar is not going to fall because there is a booming tourism sector and booming international student sector. These 2 industries alone demand $13 billion NZD per annum which creates an underlying daily and regular support for the NZD.

I believe Wheeler should leave the OCR as it is. 2.25% should have been normal under current conditions. It is important that savers to get a return on their savings. NZ households have $156 billion in savings in bank accounts. There are more savers than there are borrowers. I think 2% is getting aggresively too low. Too low and savers consumption falls which equates to falling demand and its associated falling prices.

LikeLike

Michael,

do you think it is possible that Norway is an outlier

LikeLike

Norway applies a duty on imported goods between 3% to 6%. A lot higher tariff on agricultural produce and a raft of other manufactured products plus they levy a VAT of 25%. It effectively creates a blockade at the border of free flowing product which controls the price of imported products.

LikeLike

It is possible, and I haven’t done enough digging around other countries’ experiences (esp those not at the near-zero floor). But then I look at the US where there does seem to have been some increase in core inflation, and might have been a bit more if they hadn’t raised rates last year. Even in NZ there is some sign of a modest increase in core inflation – across the measures, not just the RB’s favoured measure.

LikeLike

Let’s consider that if you retain a 2.25% interest rate per your suggestion.

Couple of problems that I can forsee:

1. In the global chase for yield and with only Australia having a similar OCR rate of 1.50%, $ will be bid up. You can-not offer a return of 2.25% when US, EU, GB and Japan either have rates set at negative, 0 or 25bp.

2.25% is just to attractive to institutional type investors (Pension funds etc) to be able to sit their cash in a 1st world country gaining a good risk free rate of return vs. obtaining negative returns.

2. If the dollar does continue to rise – what risk to NZ’s export economy – dairy, tourism, international students – at all levels you would be becoming a less attractive country due to higher costs relative to other countries e.g. Australia, Canada, US for Students. Remember one of the more attractive attractions of NZ is that it’s a lower cost destination for inbound students/tourists.

3. Dollar holds at present level/continues to rise – inflation outlook? At a current headline level of 0.4% – what chance that we will go lower e.g. deflation. Then what do you do?

Sadly no perfect answer – but with global rates sitting on zero etc – having rates set at 2.25% creates too large an incentive for foreign traders to execute things like carry trades e.g. I borrow JPY at 0/.25%/purchase Kiwi $ and obtain a risk free return of 2+ % and then lock in FX risk with FX Forward.

LikeLike

The Uridashi Jpy carry trade used to be a $5 billion dollar problem when Allan Bollard went nuts with interest rates hitting 10% but isn’t that sort of somewhere around $1 billion these days so I think the carry trade risk may be somewhat overstated?

LikeLike

Yield is King, so in a world where you can earn 0% for your cash or +2% – what are you going to pick? Australia and NZ both have the same problem that compared to the rest of the world we are an extremely attractive investment destination.

LikeLike

Personally I would pick property for yield. Rents continue to rise each year and interest rates continue to fall. The lack of new hotels mean that the drive for more tourists add more upward pressure on residential property yield plus capital gains due to supply constraints.

LikeLike

Thanks so much for the Norway example Michael, really appreciate it – great post.

Have you had a look at Sweden’s success or otherwise, am looking to that part of the world to try and think about next steps for RBA/RBNZ…

James McIntyre, CFA | Head of Economic Research, Australia Macquarie Securities Group | Macquarie Group Limited 50 Martin Place Sydney NSW 2000 Australia T 61 2 8232 8930 | M 61 411 849 427 | E james.mcintyre@macquarie.com

[cid:image003.png@01CE877C.7F78F110] This email has been prepared by a member of the Macquarie Research department. For company specific disclaimers and regional specific disclosures, please refer to the link provided below to the Macquarie Group entity disclosures and scroll down to the “Research” section. If you have any questions regarding these please contact me for further clarity.

LikeLike

I haven’t looked at it closely recently – tho of course the Swedes made probably worse misjudgements than the RBNZ in their attempt to raise rates to lean against household debt accumulation. THey didn’t reverse that mistake until core inflation measures had fallen more severely than they have in NZ. BUt since then the Riksbank seem to have been pretty aggressive in pushing mon pol to its limits (negative rates and all) and by the look of it have achieved a material rebound in inflation (eg their CPIF ex energy series), despite pretty much reaching the limits of negative rates. I don’t see NZ rates going to zero or below any time soon, but I worry that people aren’t thinking about 1% or less as being within the normal bounds of where the OCR might reasonably go from here. It looks as though getting much lower will be like pulling teeth – message reinforced in JOhn McDermott’s interview – and the risk is that the unemployed and the export sector just go on paying an unneceesary price (somewhat aided and abetted by our govt, and by some of the local media etc).

LikeLike

Wages are 55% of GDP you cant get inflation unless staff have bargaining power via low unemployment, skills shortages less immigration competing with local labour. Our open borders for trade equal no pricing power for business thus they asorb the weaker nzd.

LikeLike

Agree with fund manager,,,my experience of nz manufacturing businesses are driving down cost through automation’ enabling them to reduce labour costs and manage the high exchange rate.

Low commodity prices also help. Our customers don’t accept price increases from us and we don’t accept them from our suppliers.

LikeLike

This relentless push for higher inflation… I find myself being puzzled about a few things in your narrative.

Why is higher inflation good/desirable in this environment?

Through the first half of the 1990s inflation was the bogeyman, later aptly called “the thief in your pocket” and a 0-2 percent rate was thought to be a reasonable definition of “price stability”, where the distortions resulting from inflation would be minimal. Over subsequent years the target was relaxed I think largely so the Bank wouldn’t necessarily have to lean so hard against economic activity just because inflation was (perhaps briefly) in excess of the target range. There is nothing magical about the 1-3% target range is there? It has been changed a number of times over the last decades, and perhaps in the current low inflation environment where real wages are probably being dampened and where the inflation rates of our trading partners are likewise low, perhaps a 0-2% or 0-3% rate is not so unreasonable in these times?

e.g.

http://www.nzherald.co.nz/opinion/news/article.cfm?c_id=466&objectid=11690383

As a couple of people have I think already suggested, higher inflation isn’t going to help their business, but nor is it likely to help households at large (it could reduce real wages even further). I note that inflation in the form of higher insurance premiums, in ongoing rates rises (4% mooted this year for Wellington), power and so on are ongoing significant expenditure items which seem to consistently increase by more (sometimes much more) than the CPI and so the prospect of yet more inflation, especially on imported goods doesn’t seem too attractive.

Finally, could you please clarify? if I understand correctly (I might not be) you are proposing a lower OCR because incidentally you think that will be inflationary, but primarily if the real exchange rate is weakened in a sustained way through a lower OCR that will ultimately increase our competitiveness? But our exchange rate is floating and is influenced by many things. If a lower OCR doesn’t significantly weaken the exchange rate then isn’t the higher inflation you desire potentially going to make us less competitive than our trading partners? (And is it appropriate for monetary policy to be in effect targeting the exchange rate at all?)

Thanks

LikeLike

Indeed, Aucklanders had a 10% rates rise this year to fund intercity rail from Auckland Harbour to the vibrant heart of Mt Eden when there is nothing there. Not even a decent shopping mall. The most sensible rezoning plan would have Mt Eden zoned for 18 to 50 level buildings so that the $2 billion spend makes sense.

LikeLike