In their weekly commentary yesterday, the ANZ economics team offered some thoughts on monetary policy and inflation targeting as conducted in New Zealand. Among their comments was a reaction to my post the other day about Norway’s success in keeping inflation (and inflation expectations) up.

We noted some comparing the inflation performance of New Zealand and Norway last week, with the latter managing to achieve its inflation target. The argument was that other central banks had achieved it through looser monetary policy so the RBNZ could too. It certainly may be possible to get inflation up by throwing the kitchen sink at it. But household debt in Norway has risen to nearly 230% of disposable income (and is one of the highest in the OECD); that’s an accident waiting to happen. Is the economic cost of CPI inflation being 0.4% versus an arbitrary magical 2% that dire an outcome when one considers the possible side effects of this ‘kitchen sink’ style approach?

As a reminder, here are the policy rates for Norway and New Zealand.

I don’t want to put too much weight on Norway, but:

Norway’s approach doesn’t look like ‘the kitchen sink” to me. It looks like what many/most other central banks have done. As inflation pressures around the world proved much weaker than most had expected, Norway had more leeway than most (their policy interest rate still hasn’t got to zero, let alone the extreme lows of Switzerland (-0.75 per cent) or Sweden (-0.5 per cent). They used that leeway, and it seems to have delivered results (inflation fluctuating around target). By contrast, our Reserve Bank has been constantly reluctant to cut – having only realized quite late in the piece that they really shouldn’t have been tightening. As I noted the other day, had the Reserve Bank done nothing more than hold the OCR at 2.5 per cent for the whole time since Graeme Wheeler took office, it is likely that today New Zealand’s inflation rate would be nearer target, and there would be less reason to worry about inflation expectations. Had they set the OCR at its current level – 2 per cent – even a year ago, things would look less problematic on the inflation front than they are now. I don’t accept the characterization that even cutting the OCR to 1 per cent now would be an over the top reaction. After all, even at that level our nominal policy interest rate would still be materially higher than those in most of the rest of the advanced world (with the important exception of Australia, but then Australia has a higher inflation target than most countries do and so – all else equal – should really have slightly higher nominal interest rates). And many of the advanced economies would have been grateful to have had any additional policy leeway they could have found. They didn’t have it. We do.

Am I wholly comfortable with the idea of policy rates at 1 per cent or less, here or in other countries? No, I’m not. There is a variety of factors that help explain why policy rates, and long bond rates, are so low – notably changing demographics and deteriorating productivity growth, both of which weaken the demand for investment – but I don’t think anyone fully has the answer. And if you ask whether, over the next 30 years I expect real interest rates to be higher than they are now, I’d answer yes to that. But that just isn’t (or shouldn’t be) the basis for setting policy rates now – apart from anything else, we just don’t know much of this stuff with any confidence/certainty.

When central banks set policy rates they should be, more or less, responding to market forces (savings supply, investment demand) – attempting to mimic what the market would do if governments had not given central banks the right to issue our money. In the immediate wake of the 2008/09 recession, it was plausible to argue that central banks were holding short-term interest rates down. Implied future long-term interest rates (freely traded in the market) didn’t come down much at all. These days that argument no longer holds. In fact, yesterday 10 year government bond rates in New Zealand were actually below 90 day bank bill rates.

If anything, on this measure, monetary policy has been tightening not loosening (not inconsistent with my earlier chart showing that the real OCR remains above where it was for most of the post-recession period, even as inflation continues to undershoot). The last time this measure got above zero was in early 2015, just before the succession of OCR cuts began.

But ANZ appears to believe that the best argument against following Norway in doing what it takes to get inflation back to around target is that Norway’s household debt is among the very highest in the OECD. In both my posts on Norway, I have pointed out that Norway has had very large house price increases and high household debt. The Norwegian government has responded to any associated financial stability concerns, by accepting the central bank’s recommendation to impose a “countercyclical capital buffer” on banks – a relatively non-distortionary measure that requires banks to temporarily hold a larger margin of capital, just in case.

But the Norwegian story is much less alarming than ANZ makes out. First, while house prices in Norway are very high, here is house price inflation in Norway for the last decade or so.

Not great, but much lower than what we’ve been experiencing recently in New Zealand.

And what about household debt? I presume the ANZ economics team have read Chris Hunt’s Reserve Bank Bulletin article explaining some of the many pitfalls in comparing household debt to disposable income ratios (this piece looking across Nordic countries is also useful)?

That partly reflects challenges in comparing the level of debt across countries. There are several types of issues. For example, many countries include the debt associated with unincorporated business activities (small business owners, owner operated farms and some lending associated with rental property) in household sector accounts, since getting good breakdowns can be difficult. In New Zealand, farm lending and non–mortgage lending to small businesses is not part of household debt, while mortgage lending that finances small business should also be excluded. However, much of New Zealand’s rental property is held by small investors, and lending that finances (the business) of renting out residential property generally is included in the New Zealand measure of household debt.

The other important difference is the way that institutional differences, such as those in the tax system can affect the gross assets and liabilities on a household’s balance sheet across countries, even if the net wealth is the same for two households. In the Netherlands, for example, interest deductibility for mortgages on owner occupied houses encourages borrowers to have interest only mortgages on the liability side of their balance sheet and, for example, tax-preferred insurance policies on the other side. At some point, the asset is used to extinguish the liability, but for households with the same amount of wealth and income, both financial assets and financial liabilities will be higher in the Dutch system than they would in the New Zealand system.

In Norway, for example, interest on mortgages is tax-deductible, which is not the case (for owner-occupied houses) in New Zealand. A country with a stronger tradition of occupation pension schemes, for example, will – all else equal – tend to see higher outstanding levels of household debt, and higher levels of pension assets on the other side of a household’s balance sheet. And a country in which the government levies high rates of tax on individuals and returns the proceeds in high levels of public services (consumed by households) will, all else equal, have a much higher ratio of household debt to disposable income – for no greater threat to financial stability – than a country with a lower average tax rate and a lower flow of public services to households. Last year, on OECD numbers, Norway’s government receipts were 55 per cent of GDP, while New Zealand’s were 42 per cent. It makes a real difference: if we look instead at the ratio of household debt to GDP, Norway (currently 95 per cent) is actually slightly below New Zealand (currently 99 per cent).

In short, comparisons across time in individual countries are generally meaningful (since the institutional and tax features typically change only slowly), but comparisons across countries at any one period in time are fraught. The Reserve Bank article rightly focuses on the former.

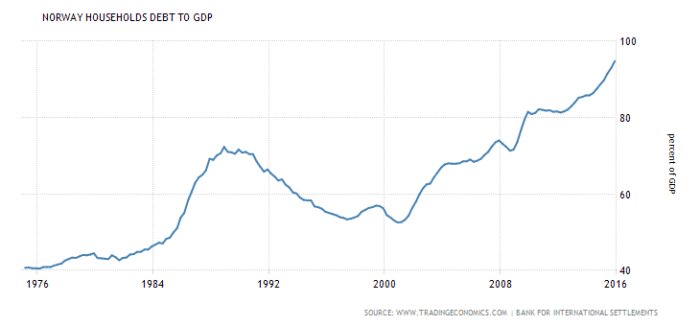

The Reserve Bank publishes household debt data back to 1990. In 1990, household debt in New Zealand was 28 per cent of GDP. That ratio is now 99 per cent of GDP. Here is a long-term time series chart I found for Norway

Household debt to GDP in Norway was already around 70 per cent in 1990, and hasn’t been as low as 28 per cent any time in the 40 year history of this series. If one looks just at, say, the years since 2007, Norway has had more of an increase than New Zealand has, but over a longer-run of time household debt here has increased by (materially) more than what they’ve experienced in Norway.

Of course, perhaps ANZ would like to now reverse the argument and suggest that we need to be even more cautious since we’ve run up much more debt (in change terms) than Norway. But then they’d have to confront the stress tests (in New Zealand) and the judgements of the respective supervisors that both countries’ banking systems are sound. Recall those New Zealand stress test results – and the ANZ is the largest bank in New Zealand – in which a 55 per cent fall in Auckland house prices and an increase in unemployment to 13 per cent wasn’t enough to severely impair the position of New Zealand banks. If ANZ thinks that conclusion misrepresented their risks, a phone call to the Reserve Bank’s supervisors might be in order.

Arguing against doing what it takes to get inflation back to fluctuating around 2 per cent on the basis of household debt numbers just isn’t very compelling. And as I’ve noted before, most of the increase in household debt is in any case a reluctant endogenous response to higher house prices, themselves the outcome of land use restrictions colliding with immigration-driven population pressures.

And that is before considering the other side effects of the current (“reluctant cutter”) policy approach the ANZ seems to be endorsing. We’ll get another read on the unemployment rate tomorrow, but for now the unemployment rate of 5.2 per cent is well above any estimate of the NAIRU (including Treasury’s of around 4 per cent). The unemployment rate has been above the NAIRU for seven years now, and almost by definition that gap is one that monetary policy could have done something about had the Reserve Bank chosen to. There are well-documented long-term adverse implications for the individuals concerned if they are out of employment for long. That is a rather more concrete cost – seven years – than the sort of ill-defined, but quite well protected against, risk around the level of household debt that ANZ worries about. The Swedes ran policy for several years worrying about household debt risks, before they finally realized that Lars Svensson was right after all and began to cut rates aggressively.

There are distributional implications too. The “reluctant cutter” approach has left our (real and nominal) exchange rate higher than it needed to be – consistent with meeting the inflation target. In the longer-term countries get and stay rich by finding products they can sell successfully to the rest of the world – that is, after all, where most of the potential consumers are. As a reminder, here is our export performance.

Another 100 basis points off the OCR wouldn’t transform this picture – the long-term challenges are more about structural policy – but in the last few years the trend has been in the wrong direction, and a misjudged stance of monetary policy has reinforced that.

There are some other things in the ANZ commentary that I agree with. I strongly endorse their call for a monthly CPI (a properly done one), and I was pleased to see their skepticism as to whether the large scale immigration programme is producing per capita income gains for New Zealanders. I might return to some of the questions about the best design of the monetary policy regime another day.

In the meantime, for all of the ANZ’s economics team unease about the risks of housing debt, there is no sign of ANZ having published its submission on the Reserve Bank’s proposed new LVR controls. So we still have no way of knowing whether their CEO was serious is his call for the LVR limits to be set even tighter than what the Reserve Bank is proposing.

The Reserve Bank wants most property investors around the country to have 40 percent deposits in future. We think they should go harder and ask for 60 percent.

I don’t suppose he was, but it would be interesting to see the economic arguments and evidence for such a proposal.