If one had simply been handed the Governor’s speech this morning, with no other knowledge of the New Zealand data, or of the Governor’s stewardship of monetary policy in his four years in office, it might have seemed quite reasonable. And a person who had a good track record in making sense of inflation pressures and adjusting the OCR to keep inflation fluctuating around the target would have built a store of reputation and credibility. Backed by all the analytical resources at his command, one might be inclined to be influenced by such a person’s analysis and storytelling.

But Graeme Wheeler is not that sort of person. Instead, he – and his advisers – badly misread inflation pressures, and after champing at the bit to raise interest rates, he launched an ill-judged, unnecessary, and ill-fated tightening cycle. He set out on his quest talking up a coming 200 basis points of OCR increases, before finally bowing to reality after 100 basis points, and has only, and mostly very grudgingly, lowered the OCR since then. In real terms, the OCR today is no lower than it was before that tightening cycle began. And so core inflation lingers well below the midpoint of the target – a focus he and the Minister had explicitly added to the PTA in 2012 – and the unemployment rate is now into an eighth year materially above anyone’s estimates of the NAIRU.

Of course, forecasting and policy mistakes are, to an extent, inevitable. No one is granted the gift of perfect foresight – and if anyone had, they’d be better employed somewhere other than a central bank. But what has compounded the problem – the reasons not to take too seriously what the Governor says – is his continued failure to even acknowledge mistakes, let alone express any contrition. It is hard to have any confidence that someone has learned from their mistakes if they won’t even own up to having made obvious ones. And while no individual speech can cover everything, it is striking how totally absent any treatment of the Bank’s conduct of monetary policy over the last four years was from this one.

Since my wife will be ticking me off for overdoing it and not resting if I write too much, I wanted to pick up on just two points in the speech.

The first was the Governor’s apparent model of inflation.

low inflation in some countries is linked to demographic change, especially in countries with a declining workforce and rapidly ageing population. Low inflation is also due to technological change around information flows and energy production, and to the global over-supply of commodities and manufactured goods;

Which sounded depressingly like the excuses and alternative explanations that were touted, in reverse, in the 1960s and 1970s. At that stage people talked about the role of union power, occasionally even about demographics, about oil prices and resource scarcity and so on. Each of those phenomena were real – as those in the Governor’s list are – but to cite them as explanations for persistently high, or persistently low, inflation is some mix of cop-out and analytical failure.

Persistent inflation – or the absence of persistent inflation – is always and everywhere a monetary phenomenon. By that, I don’t mean printing banknotes, and I don’t mean particular levels or growth rates for things central banks call “monetary aggregates”. I mean simply that monetary policy can, if it chooses (or is permitted to) counter the impact of the sorts of factors the Governor listed and deliver an inflation rate that averages around target. If they no longer believe that, the Reserve Bank should hand back its remit.

Sometimes, the job of monetary policy is harder than normal, and sometimes easier. In the 1960s and 70s, with overfull employment in many countries, lots of union power, and lots of demand pressure associated with a rapidly growing workforce, it took a lot of effort to get and keep inflation under control. Some countries did pretty well. Others – and New Zealand and the UK were two prime examples – did poorly. In the current climate, there seem to be a variety of ill-understood factors dampening inflation pressures globally. Some countries have done well in countering them – Norway is an example, and on Stan Fischer’s reckoning the US might be too. Others less so. But last year, on IMF numbers, around 90 countries had inflation in excess of 2 per cent, and almost 70 had inflation in excess of 4 per cent

Of course, the current effective lower bound on nominal interest rates, a bit below zero, does constrain many countries’ freedom of action. But it doesn’t change the fact that inflation is a monetary phenomenon – it is just that regulatory and administrative practices hamstring the ability to use monetary policy to the full in those countries. Low inflation in other countries doesn’t make the Reserve Bank of New Zealand’s job harder. although common global factors – affecting us as much as other countries – may do.

Before turning to the second main aspect of the speech I wanted to comment on, I would note that there was plenty in the speech that I agreed with. My differences with the Bank have never been about how the inflation target is specified and I agree that the government should not be considering lowering the target when the next PTA is signed next year. There might be a case for considering raising the target – to minimize the risk that the near-zero bound becomes a problem – but that is a topic for another day. As the Governor notes, no other governments in other countries have changed the inflation targets their central banks work to, or abandoned inflation targeting.

The second area I wanted to focus on was the section devoted to explaining why the Governor disagrees with people like me, who think that interest rates should be cut further now. Here is what the Governor has to say.

This view advocates bringing inflation quickly back to the mid-point of the inflation band by rapidly cutting the OCR. Driving interest rates down quickly would lower the exchange rate, contributing to increased traded goods inflation and stronger traded goods sector activity. The ensuing increase in house price inflation is not seen as a consideration for monetary policy, even though there would be an increased risk of a large correction in the housing market and associated deterioration in economic growth.

There would be considerable risks in this strategy. An aggressive monetary policy that is seen as exacerbating imbalances in the economy would not be regarded as sustainable and would not generate the exchange rate relief being sought.

With the economy currently growing at around 2½ – 3 percent and with annual growth projected to increase to around 3½ percent, rapid and ongoing decreases in interest rates would likely result in an unsustainable surge in growth, capacity bottlenecks, and further inflame an already seriously overheating property market. It would use up much of the Bank’s capacity to respond to the likely boom/bust situation that would follow and would place the Reserve Bank in a situation similar to many other central banks of having limited room to respond to future economic or financial shocks.

Such consequences suggest that a strategy of rapid policy easing to extremely low rates would be counter to the provisions in the PTA that require the Bank to “seek to avoid unnecessary instability in output, interest rates and the exchange rate” and to “have regard to the soundness of the financial system”.

Do note the rather loaded language throughout this section.

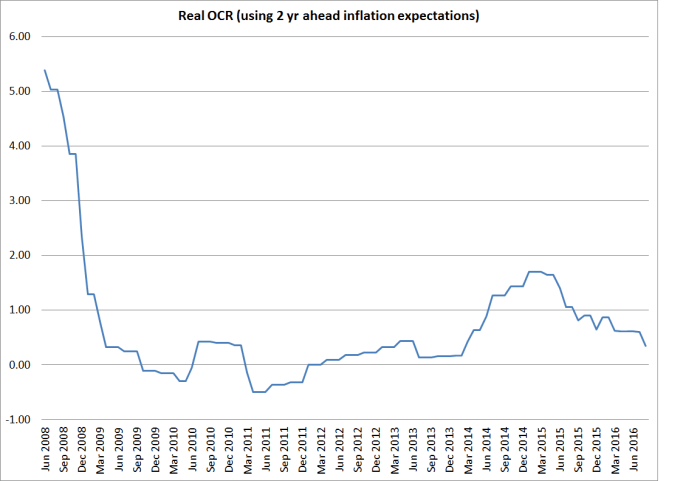

Note too, as context, the chart of the real OCR

To this point, far from having seen “rapid” OCR cuts, the OCR in real terms hasn’t yet got back down to where it was before the ill-judged tightening cycle began. Context matters: if the Governor were making these sorts of arguments when the real OCR was already 100 bps below previous record lows, with the labour market overheating and inflation rapidly heading back to 2 per cent, they might sound more plausible

As it is, I’m not quite sure what to make of the comments. On the one hand, in the first paragraph he accepts that such a strategy would work by lowering the exchange rate. But then in the next paragraph he appears to suggested that unexpectedly rapid OCR cuts would not in fact lower the exchange rate. We all know that foreign exchange markets can be fickle things, but I’m pretty confident that if he’d come out this morning and said “you know, on reflection it does look as though interest rates will need to be quite a bit lower than we had thought. We’ll do whatever it takes to get inflation fluctuating back around 2 per cent, and at present it looks as though that might mean the OCR has to head towards 1 per cent” that the exchange rate would be quite a lot lower.

And what of GDP growth? Recall, that the Bank has persistently overestimated how rapidly spare capacity has been used up. Their forecasts currently have GDP growth accelerating to 3.5 per cent. But the expectations survey they run – and apparently now want to gut – suggests informed observers don’t agree: latest expectations among that group were for growth of 2.5 per cent and 2.4 per cent in each of the next two years. On that basis, those observers don’t expect the substantial excess capacity in the labour market to be absorbed any time soon. And as a reminder to the Bank, to absorb an overhang of unemployed people the economy has to have a period of faster-than-sustainable growth. To get core inflation back to target typically involves much the same sort of pressures.

In fact, most of this is – as always with this Governor – about house prices. In his description of the “further cuts” view, the Governor notes that for those running this view

The ensuing increase in house price inflation is not seen as a consideration for monetary policy

That is because it is not, under the current Act and PTA, a relevant consideration for monetary policy. The target is medium-term CPI inflation. House prices don’t figure in that index and – unless they have had a major recent change of view – the Bank doesn’t think they should. Monetary policy has one instrument and can really only successfully pursue one target. The Minister of Finance and the Governor agreed that target would be medium-term CPI inflation.

But perhaps my biggest concern is that the Governor is now falling back, quite openly and formally, on the spurious argument that if he cut more now, he would only increase the chances of running into the near-zero lower bound at some future date. His logic here is totally wrong, and his approach is only increasing the risk of lower-bound problems becoming an issue for the Reserve Bank of New Zealand.

With hindsight that is pretty clear. Remember that I’ve pointed out that we’d have been better off if the Governor had done nothing at all on monetary policy in his four years in office. Actual inflation would be a bit higher – since average interest rates would have been lower, and no doubt the average exchange rate – and, on the Bank’s own reckoning (they point out that expectations appear to have become more backward looking) inflation expectations would have been higher. Higher inflation expectation would, in turn, have supported higher nominal interest rates now (for the same real interest rates). But the same analysis applies looking ahead. If the OCR were cut further and faster than the Bank currently plans then, on their forecasts, inflation and inflation expectations would rise, helping to underpin higher nominal interest rates in future. The risk of the current strategy – especially given the Bank’s asymmetric track record – is that actual inflation continues to undershoot, excess capacity lingers, and in response inflation expectations drift ever further downwards. If that happens, the nominal OCR will have to be lowered just to stop real interest rates rising.

The lesson from a wide variety of advanced countries over the last decade is surely that, with hindsight, they didn’t cut their official interest rates hard enough and far enough early enough. I stress the “with hindsight” – there was little good basis for knowing that in 2009, but there is much less excuse for central banks, like the RBNZ and RBA, that still have conventional policy capacity.

On which point, two other observations:

- there was still no reference in the speech to New Zealand doing anything about making the near-zero lower bound less binding. There is simply no excuse for the New Zealand authorities to have done nothing pre-emptive to ensure that the ability to use monetary policy aggressively in the next downturn is not constrained by artificial constraints around the price of physical banknotes.

- in his alarmist rhetoric about “further inflaming” the housing market, the Governor appears to have forgotten completely the line the Bank used when LVR restrictions were first imposed. Asked then why not use monetary policy instead, the (correct) response was that our modelling suggesting that it would take 200 basis points of OCR increases to have the same impact on the housing market as the (quite limited) estimated impact of LVR controls. No one – not even me – is suggesting that the OCR should be cut by 200 basis points now. And if the Bank is concerned about banking system risks from high house prices, it has capital requirements that it could adjust.

Once again, this is a speech that reflects a key aspect of the Governor’s underlying “model” – his fear that inflation might be just about to break out, all while taking little or no responsibility for the fact that it repeatedly fails to do so. I’m caricaturing a little bit, but not a lot. Go back and read what he was saying leading into the 2014 tightening cycle, and then read those paragraphs from today’s speech that I included above – written from a point where the real OCR is still slightly higher than it was before the tightening cycle. That mindset clearly shapes how he thinks about policy and his asymmetric view of risks. Past performance might not be a good predictor of future performance in investment management, but in senior managers and key decisionmakers it often is. It is hard to self-correct unrecognized biases – perhaps especially if the decisionmaker thinks those biases are actually strengths. The Governor has form. Unfortunately, it is has mostly been poor form. It is not clear why that bad run is about to break.

In passing, it is just worth noting one of the Governor’s final observations

Central banks do not have special powers of market foresight or a franchise on wisdom. But they do have significant research and analytical capacity that can deliver valuable insights, and this is being applied to challenges associated with the current global economic and financial developments.

And yet, neither in the text of the speech nor in any of the 11 footnotes, is there any reference to any Reserve Bank research at all.

Headline from a Financial Webs-site post his speech:

$NZDUSD spiked by nearly 0.9% after RBNZ Wheeler’s statements in Dunedin.

Maybe the RBNZ should just not say anything – because every time in recent history – either via OCR decisions or RBNZ speeches the Dollar spikes higher based upon their commentary.

Do they even review their speeches and discuss the wording that they are using – because the market just listens to them and then bids up the Kiwi – which all in all is not a good reflection on the RBNZ and how the market views their announcements?

LikeLike

They will have tried to work out how the market will react, and probably told themselves there was nothing in the speech that wasn’t in the MPS a couple of weeks ago, and so no news. I’m not close enough to know what prompted that increase in the TWI, altho the section I dealt with in my post was perhaps more strident on the “why not cut further side” than might have been expected. Even though they have denied it previously, it is a pretty explicit statement of their “reluctant cutter” approach.

LikeLike

some left field thoughts if we were to have a recession the next policy tools after we reach the zero bound for the RBNZ are QE with purchases of gov. and corp bonds then even fiscal QE coordination with treasury will need to get the government to alter the reserve bank act . Then you get inflation.

LikeLike

The comment you picked up on “Driving interest rates down quickly would lower the exchange rate”, I also interpreted as you did. But I think he was attributing those views to the “cutters”.

A thought about exchange rates, I have wondered what would happen to the exchange rate if the RBNZ, government etc. ran a more erratic operation, and made comments about the exchange rate, interest rates etc. that kept the traders nervous. Not what would be described as best practice, but maybe the dollar would drop. Possibly some other consequences.

Re near-zero bounds. If he cuts and it doesn’t work and he runs out of options, then that was always likely to happen. If he thinks the speed of cuts is important (the market needs time to react?) he should make that case (perhaps he did), not say that he doesn’t want to risk getting to a point where he won’t know what I would do.

LikeLike

On reflection – and, actually, reading the press release – I think you are right about the exchange rate para. If so, it is a very bold call on his part – and if he really believes it, makes his repeated calls for a lower exchange rate look emptier than usual. There are plenty of simple exchange rate models around that will tell him that the OCR cuts over the last year or more have had an impact on the exchange rate: narrowing interest differentials have offset the impact of rising risk appetite and some recovery in international commodity prices etc.

Call me an old-fashioned bureaucrat, but I lived thru enough inadvertent messaging problems in my time at the Bank not to wish on anyone the fruit of a central bank actually trying to be inconsistent and all over the place!

LikeLike

Michael – While I tend to agree with the thrust of your arguments from the Bank’s perspective there is an element of consistency in their view if you believe that interest rates are already at very stimulatory levels and that underlying growth is strong and associated returns on assets in NZD are high. If this is right then indeed further “aggressive” cuts might even drive the currency higher and certainly would contribute to unnecessary volatility in the exchange rate.

The evidence cited by John in the speech regarding the level of growth does seem compelling even if the quality of the growth is perhaps less than desirable (i.e. low per capita income growth reflecting GDP growth being amped up by immigration).

The mix of monetary conditions is similarly undesirable but I don’t think (and I suspect neither do you) that the Bank has a whole lot of control over the mix. I am not sure how much control they have on the quality of growth either (the mix is largely out of their hands in the medium run).

How much should the Bank be concerned (in PTA terms) with the quality of growth and the mix of monetary conditions? Underlying your views seems to be a much higher weight on these considerations than the Bank has. But the quality of growth doesnt figure in the PTA and the mix is hard to control or predict.

As noted I agree with you that rates should be quite a bit lower (even just signalling that possibility could be enough to help the monetary mix in the short term) but I think the Bank might reasonably disagree as they think that interest rates are much more stimulatory than I (or I think you) think they are. If they are right then isn’t their strategy of not adding more fuel to the fire now sensible?

LikeLike

Hi Kelly

As ever, you raise lots of interesting points.

I agree that the Bank can’t have much impact on the mix of “policy” (or “monetary conditions”). I’ve consistently argued for easier conditions overall – and while I think the real exchange rate is a major structural imbalance, that is really an issue for Beehive/Treasury. I don’t think the Bank should be concerned about the “quality of growth” or even its level (if you pushed me far enough) – real data are mostly, in my view, information to be interpreted in making sense of the inflation picture and judgements about the OCR. So weak per capita growth is probably largely a structural policy issue, but in combination with U greater than NAIRU and weak NT inflation it points in a direction of monetary policy being too tight.

In terms of the Bank’s own take, yes I wouldn’t accuse them of internal inconsistency – if it adds anything much the modelling framework helps largely keep them from that. My criticism is mostly one that they are simply misreading things – interest rates are much less stimulatory than they seem to think (altho John told FEC a few months ago neutral was down to 4%, prob mostly on lower inflation expectations), the unemployment rate is telling us something meaningful about slack and so on.

I was a bit surprised that you found what they had to say on growth “compelling” . I didn’t see anything in the speech or MPS to give me any confidence overall GDP growth would accelerate from here – a central part of their story – and at current levels it is (a) lower than in typical recoveries, even with particularly rapid population growth, and (b) not resulting in any material recovery in non-tradables inflation, or any rapid decline in excess capacity in the labour market.

LikeLike

I wonder what you think of the material in this post by Bernanke? https://www.brookings.edu/blog/ben-bernanke/2016/08/08/the-feds-shifting-perspective-on-the-economy-and-its-implications-for-monetary-policy/

He points out that the FOMC’s estimates of neutral rates and potential growth have declined significantly in recent years – hence the tightening cycle has been delayed and muted compared to historical cycles. There are clear implications for NZ as if this is right then it would seem likely that the neutral rate has fallen in NZ also (its down 1.25 percent since 2012). I think the RBNZ may have trimmed theirs a bit in recent years from maybe 5 percent to 4.5 percent but maybe the fall is much greater hence the low inflation outcomes in terms of non tradeables inflation seen in recent years (I agree with you that non tradeables is the right thing to look at and that its unusually low now).

Another interesting perspective is the line that trend productivity growth might have been adversely affected by the shorter term growth fall out from the GFC hence weaker potential output growth and lower neutral interest rates. He runs the line that there might be benefits to running the economy a bit hotter for a while to try and offset those deleterious effects. Similar arguments might be relevant to NZ and might justify a different risk/reward tradeoff for easier policy in the circumstances than the RBNZ currently assesses.

LikeLike

Very nice piece by Bernanke.

On the neutral interest rate, I presume you saw the recent piece by John Williams

http://www.frbsf.org/economic-research/publications/economic-letter/2016/august/monetary-policy-and-low-r-star-natural-rate-of-interest/?utm_source=mailchimp&utm_medium=email&utm_campaign=economic-letter-2016-08-15

If anything that model would have an even larger fall in the neutral rate than in those FOMC central tendencies. I’m skeptical of anyone’s ability to know what the neutral rate is at present, but given the complete absence of productivity growth in recent years, and very weak inflation, it seems quite conceivable that it is well below the 4% the Bank is still using for NZ (even though, if you asked me to put money on it, my very long term estimate for NZ might still be getting up towards 4 per cent). In the current climate, one probably can’t improve much on just looking out the window at incoming data. While inflation is below target, and U > NAIRU (itself probably trending down) I think there is a good case for cutting, and keeping on cutting, even allowing for the fact that the lags mean one will inevitably end up going a little far. If inflation picks up and core ends up near 2.5% for a year or two it won’t be the worst thing in the world, either in getting inflation expectations back to around 2% and in reducing ZLB risks.

I’m still skeptical of the line that weak demand is itself dampening potential growth. the best counter-example to me remains the Great Depression, a clear case of aggregate demand shortfalls, and yet a period of very strong TFP growth.

https://croakingcassandra.com/2016/02/23/some-great-depression-comparisons/

It would suit me to believe that easier mon pol, boosting demand, would in turn lift potential growth but…..I can’t see the evidence. To me, it still looks a lot more like weak investment demand globally is a response to deteriorating demographics and deteriorating productivity (and hence in combination fewer investment opportunities)

LikeLike

Tend to think people consider interest rates in the shop window rather than the real OCR when making saving / investment decisions. And given these rates are at historic lows, seems monetary conditions are at the ‘easy’ end of the spectrum. To that end, if one deducts recent house price inflation and/or surveyed expectations from current mortgage rates, money looks cheap.

LikeLike

Yes, but isn’t the question what people are making of those shop window rates. A 5% mortgage rate in 2008 would have felt incredibly cheap, now it probably seems not super-attractive at all. Some of that is about the fall in inflation expectations.

There isn’t any doubt that all nominal interest rates are very low in absolute terms, but most of that fall – at least at the short end – happened over 08/09. There hasn’t been much further fall since then – especially in wholesale rates as they face people making tactical asset allocation choices – and if anything the fall in inflation expectations suggests real interest rates have risen a bit.

Is money “cheap”. Yes. Is it cheap enough, given all else that has gone on – demographics, deterioriating productivity etc? That seems much less clear, against a backdrop of low inflation (including non-tradables inflation) and ongoing excess capacitiy (unemployment).

LikeLike

….as I understand it, the lower the rate of interest (or the medium-long term rate of interest), the greater the incentive to invest: business people survey the real economy, nut out a profitability activity, draw up a formal business plan, obtain a contribution toward funding from the local bank, invest in required assets, employ needed skills and start selling product on the market to those who find it less attractive to save given the lower opportunity cost of holding money. Would another 50bp cut in the OCR kick start this process? Maybe but tend to think identifying the profitably activity and acting on it is the required catalyst and that seems dependent on so many variables it fogs the mind (well at least mine!)

LikeLike

Floating rates are what business relies on for working capital. These rates still hover around 5.1%. Hardly any of the recent OCR falls have translated to equivalent falls on the floating rates.

LikeLike

yes, sure there is a wide range of factors in any investment decision. 50bps is hardly ever decisive to anything, but it works in the right direction: encouraging consumption, encouraging investment, and making NZD assets less attractive relative to assets in other currencies, so boosting domestic export-oriented activity. All, no doubt, by small amounts, but the aim here is to get inflation (core) up from 1 to 1.5 to fluctuating around 2 and – with it- unemployment down from just over 5 to say around 4. It probably doesn’t need several hundred points of impetus. If asked where I thought, point estimate, the OCR should be now, I’d probably say 1.25%, but recognize that even as things stand now there is probably a margin of +/- 50 bps around that.

LikeLike