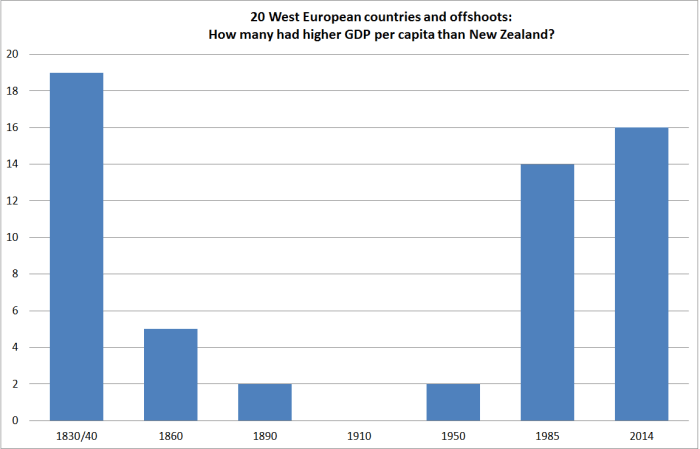

The IMF released its latest Article IV report on New Zealand yesterday. There are also some background research papers released with the report, and I might come back to look at them later.

There aren’t material surprises in the IMF’s views in the full report, which builds on the Concluding Statement released at the end of the staff mission here last November. My comments about that statement (here) were fairly critical, noting both the marked change in the messages from one review to the next, and the fairly limited evidence base for many of the policies the Fund was recommended – quite a few of which were a considerable distance removed from the core business, or expertise (macroeconomic policy and financial stability) of the International Monetary Fund.

Today I wanted to focus just on the Fund’s claim that there is a major policy problem as it affects savings in New Zealand, a proposition on which much of the rest of the report rests. The Fund talks of a “chronically low national saving” rate, and worries about the vulnerability that allegedly results from a net international investment position (NIIP) of around -65 per cent of GDP. In the Fund’s Board discussion, we read that “Directors agreed that raising national, and in particular private, saving is critical to reducing external vulnerabilities from the still heavy reliance of offshore funding”. Note the strong words: action is “critical”.

I’ve shown a version of the following chart before. It is common to present charts of net national savings as a per cent of GDP, but to do so involves two errors: first, the numerator is net but the denominator is gross (the difference is depreciation), and second, the numerator refers to savings of New Zealanders and the denominator refers to economic activity occurring within New Zealand, whether owned by foreigners or New Zealanders. A more conceptually meaningful approach is to do as I do here: compare the net savings of New Zealanders with the net national income of New Zealanders. Here it is shown all the way back to 1970.

Savings of New Zealanders (public and private combined) as a share of income have been consistently lower than the median of the whole group of OECD countries. But there is a very diverse range of experiences, and cultures, within the OECD group. I’ve also shown the comparison with the median of the five other, probably more culturally similar, Anglo countries (US, UK, Canada, Australia, and Ireland). Over the 45 year period, mostly we don’t look much different from the Anglo median – we did worse in the years of very large fiscal deficits in the late 70s and early 80s, but other than the experiences are pretty similar on average. Where is the evidence of a chronic savings problem? And it is no defence simply to focus on private, or (worse) household savings: first, the boundaries between household and business savings are blurred, and second, the private sector takes account (typically implicitly) the savings behavior of governments over time. New Zealand governments have done less badly than most for some decades.

The IMF makes no systematic effort to identify reasons why national savings rates might have been as they are. Instead, they mostly repeat old lines that don’t have much basis to them. For example, they assert that an overwhelming proportion of household assets are in the form of housing, even though new Reserve Bank estimates – published almost a year ago – make clear that that claim was never justified. After all, relative to population, there is now a consensus that we have too few houses not too many. The Fund also asserts that there is something wrong with the tax treatment of housing, but appears to make no effort to illustrate, whether in a cross-country or time series context, how that has contributed to national savings behavior. They urge changes to Kiwisaver and the NZS, but again make little effort to illustrate how policy parameters in these areas explain savings behaviour. All in all, it seems like a rather weak basis on which to rest quite strong policy recommendations.

The other aspect of this issue which they just seem to take for granted is the alleged vulnerability that the NIIP position gives rise too. Buried deep in an Annex to the report, they do produce a chart making clear that there has been no worsening trend in the NIIP position for over 25 years – the negative position tends to widen in boom times and narrow in downturns, but has fluctuated around a pretty stable trend level. At present, the negative NIIP position is actually below (less negative) than the average since 1988.

The report has no analysis of the nature of the vulnerability that this NIIP position gives rise to – even though addressing this vulnerability is considered “critical” by staff and Board. And it gives no example of any country, anywhere, ever, in which a stable (but quite high) negative NIIP position over 25-30 years has been (causally) followed by a crisis. I’m pretty sure there are none – and remind that IMF that for most of its first 100 years, New Zealand’s negative NIIP position was materially larger than it has been over the last 25 years, again without ending in crisis. There are plenty of cases where a rapid worsening in the NIIP position over a few years led to trouble – Spain, Ireland, and Greece are three recent advanced country examples – but that is a very different situation from the New Zealand situation in recent decades. As has been the case for many years, the IMF simply seems to struggle to come to grips with New Zealand.

Most of the negative NIIP position is represented by (net) banking system borrowing from abroad. But that creates serious macroeconomic risks only if the assets that are financed by the overseas borrowing are of poor quality. Often that is the case when foreign debt is rising quickly – but that hasn’t been the New Zealand story. Perhaps the Fund believes that the New Zealand banking system is shaky? But Directors noted that “the banking system is resilient and well-supervised” – the resilience conclusion is certainly backed by the Reserve Bank’s own stress tests, which I discussed at length last year.

New Zealand deserves better quality analysis and insights from its membership of the IMF than it has had in the main part of this report.

The report also contains brief sections headed “Authorities’ views” – the wording of which will have been approved by our Treasury and the Reserve Bank. I was surprised to find that “the authorities agreed that raising national saving was an important policy objective”, going on to state that the authorities would “consider measures to boost private saving….in the future”. There isn’t much elaboration of the point, but the statement itself was something of a surprise. Last I had heard, the Minister of Finance was very sceptical that there was a “national saving problem” in New Zealand, and particularly that there was an issue materially amenable to policy remedies. If one can’t convincingly identify policy distortions that materially lower national saving rates relative to those in other countries, it is hard to see a good case for policy interventions to encourage people to save when, on their own, they would not. It would be interesting to know what was behind this latest, apparent, change of view.