Tomorrow sees the release of the latest Reserve Bank Monetary Policy Statement. My “rule” for making sense of the Governor’s monetary policy choices at present is that he really doesn’t want to cut the OCR – and hasn’t for the last year – as much because of the housing market as anything, and cuts only if reality mugs him, in the form of some key data that he just can’t escape the implications of. I haven’t seen that sort of data in the last month or two. Given the terms of the Policy Targets Agreement, it should have been an easy call to cut the OCR again, but it probably hasn’t been.

There is a nice, fairly trenchant, column from Hamish Rutherford in the Dominion-Post this morning on the Governor’s communications “challenges”. I’m very sympathetic to the line of argument Rutherford is running (including his use of some BNZ analysis of monetary policy surprises). My only caveat is that, in my view, getting policy roughly right is better than being predictable and wrong. There were no major monetary policy surprises or communications problems in 2014. But the repeated increases in the OCR were simply bad policy. Grudging as it may have been, and badly communicated as it undoubtedly was, the OCR has at least been moved in the right direction for the last year.

In this post, I wanted to highlight some issues that it would be good to see the Reserve Bank change its stance on in its statement tomorrow. If I really expected they would do so, I probably wouldn’t bother with the post, but perhaps there will be a surprise in store. Many of them have to do with countering that persistent sense, pervading Bank documents, that the economy is doing just fine. The Reserve Bank has an inflation target, not an economic performance one, but the argument that all is fine in the economic garden has been used repeatedly to justify keeping the OCR as high as it has been. As a reminder, even today, in real terms the OCR now is still higher than it was when the ill-judged 2014 tightenings began.

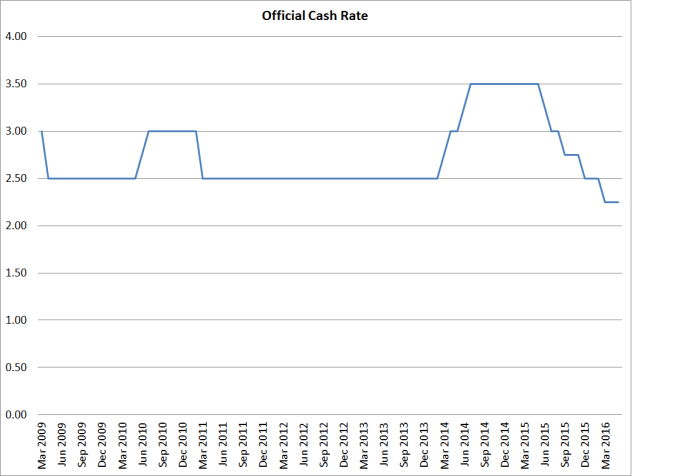

The first is the constantly repeated claim that monetary policy in New Zealand and in other countries is highly “stimulatory”. It appears in almost every Reserve Bank policy statement or speech, and appears to be based on nothing more than the undoubted fact that interest rates (real and nominal) are currently low by longer-term historical standards. That doesn’t make them stimulatory. It has now been more than seven years since the rate cuts during the 2008/09 recession came to an end. For most of the time since then the OCR has been at 2.5 per cent. Today it is at 2.25 per cent.

Adjust for the fall in inflation expectations (around 60 basis points over 7 years on the Bank’s two-year ahead measure), and if anything real interest rates are a bit higher than they’ve typically been since 2009.

The Reserve Bank appears to still believe that a normal (or ‘neutral’) short-term interest rate might be around 4.5 per cent. But there is nothing substantial to back that view. The fact that inflation has been persistently below target for several years, in a weak recovery with persistently high unemployment, argues against there being anything meaningful to a claim that 4.5 per cent is a “neutral” interest rate – a benchmark against which to measure whether monetary policy is “highly stimulatory” or not. Better, perhaps, to look out the window, and check the current data. That isn’t always a safe strategy, but it is better than clinging to old estimates of unobservable structural features of the economy. Having moved to a flat track in its interest rate projections, the Bank appears to be backing away from putting much practical weight on the high estimates of a neutral – or normal – interest rate. But the rhetoric still seems to matter to the Governor, and his reluctance to cut the OCR seems, in part, influenced by his sense that interest rates are already “too low”. He has – or at least has produced – nothing to support that sense – whether for New Zealand, or for most other advanced other countries. Better to put to one side for now any estimates of neutral interest rates, lose the rhetoric, and respond to the observable data as they are.

The second point I would like to see signs of the Reserve Bank taking seriously is the persistently high unemployment rate. At 5.7 per cent it has barely changed in the last year. I noticed that the OECD in its new forecasts seems to treat 5.8 per cent as the natural rate of unemployment (or NAIRU) for New Zealand. Few others do, and both the Treasury and the Reserve Bank have tended to work on the basis that our regulatory provisions (welfare system, labor market restrictions etc) are such that the unemployment rate should typically be able to settle nearer 4.5 per cent without creating any inflation problems. Someone forwarded me the other day a market economist’s preview of this MPS, noting with some surprise that the unemployment rate wasn’t mentioned at all. I sympathized with the person who sent it, but pointed out that it was the Reserve Bank the market economists were trying to make sense of, and the Reserve Bank gives hardly any attention to this key indicator of excess capacity in the labour market. Reluctance to cut the OCR might make more sense if the unemployment rate were already at or below the NAIRU. As things stand for the last few years, there is an inefficiently large number of people already unemployed, and the Governor’s reluctance to cut just condemns many of them to stay unemployed longer than necessary. The Governor should at least recognize that trade-off, and explain the basis for his judgements.

The third point it would be good to see the Reserve Bank explicitly addressing is the mistakes it has made in monetary policy over the last few years. Depending on the precise measure one uses, inflation has been below the target midpoint – a reference point explicitly added to the PTA in 2012 – for many years now. Some of that might not have been easily foreseeable. Some of it might even have been desirable in terms of the PTA (if the one-off price shocks were all one-sided, which they weren’t). Humans – and human institutions – make mistakes, and one test of a person or institution is their willingness to recognize, respond to, and learn from their mistakes. Since the Governor is unwilling even to acknowledge that there were any mistakes, it is difficult to be confident that he or the institution has learned the appropriate lessons and adapted their behavior.

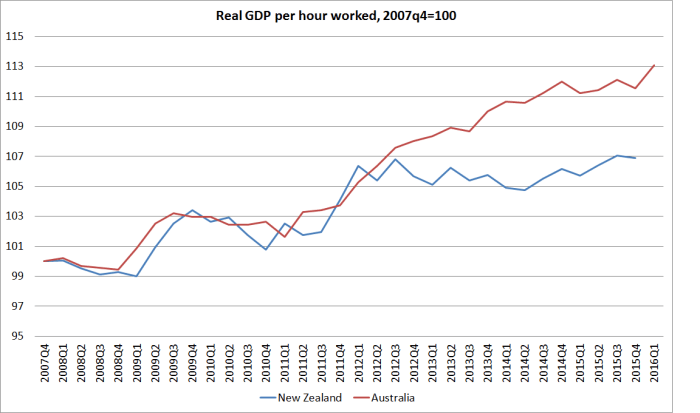

The fourth point it would be good to see the Reserve Bank acknowledge is how poor New Zealand’s productivity and per capita real GDP performance has been. For example, here is real GDP per hour worked for New Zealand and Australia since the end of last boom.

Maybe data revisions will eventually close the gap, but that is the data as it stands now.

And here is per capita real GDP growth rates.

A pretty dismal recovery phase, by comparison with past cycles.

My point is not that monetary policy can or should target medium-term productivity growth or real GDP growth, but simply to illustrate the climate in which the Governor has been making his monetary policy calls, holding the OCR consistently higher than the inflation target required. He likes to convey a sense – akin to the tone of the government’s own “glee club” – that everything is fine here but actually it is pretty disappointing. Perhaps holding interest rates higher than was really necessary might make a little sense if the per capita GDP growth or productivity growth had been really strong – leaning a little against the wind – but they’ve been persistently weak. Again, the Governor should explain the basis for his trade-offs, not pretend they don’t exist. We’d have had a better cyclical performance if the OCR had not been kept so high.

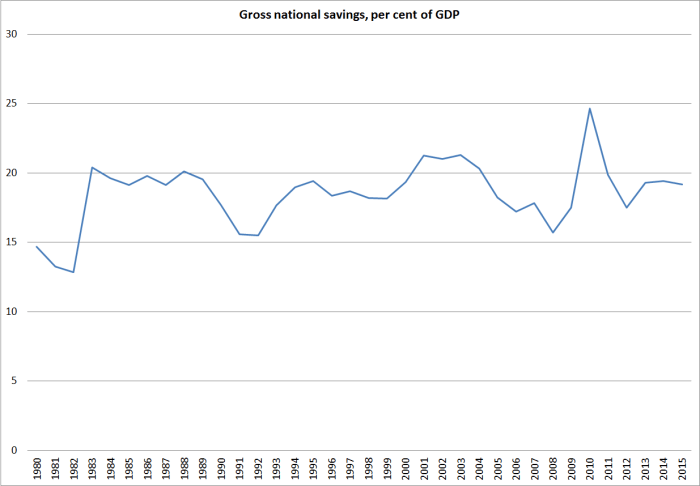

I could go on. The Governor could usefully highlight that, although he is uncomfortable – as everyone should be – with current house prices, there is nothing in the turnover or mortgage approvals data (per capita) to suggest an excessively active market (high turnover is often associated with excessive optimism, and unjustifiably loose credit conditions). And there is nothing in the consumption or savings data to suggest that high or rising house prices have spilled over into unwarranted additional consumption, putting upward pressure on inflation more generally. I showed the chart of private consumption to GDP in a post yesterday – stable over almoat 30 years, despite really large increases in house prices and credit. This chart shows the national savings rate, since 1980. There is a little year to year variability, but again no trend over 35 years now.

House prices are a national scandal, but there is no reason to think they should be treated as a monetary policy problem.

I do think the OCR should be lower – perhaps 50 or 75 basis points lower than it is now. In time, the Reserve Bank is likely to recognize that. But my point here is really that when he makes his choices – and they are personal choices, not those of a Committee – the Governor should, and should be seen to, engage with world as it is, not as he might wish that it would be. In that world, the unemployment rate lingers high, productivity and income growth have been persistently weak, inflation has been persistently below target, wage inflation is weak, house price inflation isn’t splling into generalized inflation pressures, and historical reference points around normal or neutral interest rates seem increasingly unhelpful. Perhaps there is a good case for keeping the OCR at current levels, but a good case can’t simply pretend everything is rosy in the garden or that – finally – everything is just about to come right.

(And all that without even mentioning the exchange rate which is not only high by historical standards – again raising doubts about those “stimulatory” claims for monetary policy – but this morning is at almost exactly the same level it was at a year ago. The fall in the exchange rate from the 2014 highs was supposed to help get inflation back to target. It was a half-plausible story when the fall first happened. It is less even than that now.)

http://www.stuff.co.nz/business/80793091/The-Reserve-Banks-job-is-not-to-keep-people-guessing

LikeLike

That’s just one persons opinion

Conjures up a picture of the WSJ telling Alan Greenspan he’s unpredictable

Greenspan would have laughed – and did so – frequenlty

LikeLike

Hi Michael, just like to say first up that I am thoroughly enjoying the blog. Very well written and reasoned.

I would like to question your view on interest rates being stimulatory. I take your point that rates have barely moved since the GFC, and once inflation is taken into account real rates may well be higher. But my query is around the effectiveness of further easing. Until recently the RBA governor spoke on the diminishing effects of rate cutes (although the weak CPI has put paid to that). On an anecdotal basis, firms are not struggling with the price of debt, and it is not this that is constraining their investment decisions but a lack of desire to take on more risk. Will three more rate cuts really change playing field? It hasn’t seemed to overseas (apart from maybe avoiding a depression).

LikeLike

Thanks Sam

I think the key way a lower OCR cut would help here (raising activity and, in time, inflation) is through the exchange rate. That channel works – not mechanically, and one can always cite what look like counterexamples, but on average over time).

As for other countries, yes, but remember that most of them reached the limit of what they could do – interest rates around zero. We (and Australia) haven’t, so when inflation is below target and the economic performance/unemployment etc are pretty underwhelming, I think the RB really should be doing all they can.

LikeLike

Michael

I don’t agree that NZ needs more economic stimulation so I can see zero value in a rate hike.

In any case there seems to be next to no evidence that OCR changes now have much impact on saving, consumption or investment (presumably the OCR impact on the value of the NZ$ does feed through to local production, but I guess that effect is lost in the noise). Sans such evidence and with the NZ economy doing OK (I don’t think your “per capita” point has much relevance in this particular debate), the RBNZ is better to “do nothing”.

But I am curious about one fact which you may be able to help with. The massive population jump and the slump in productivity presumably reflects poor per-capita investment rates and hence a fall in capital per capita. Is that what has happened?

Tim

LikeLike

Tim

I agree the main channel of any impact would be through the exchange rate. Would it be lost in the noise? Perhaps, but then 25bps isn’t much of a move either. The direction of the likely effect is pretty clear.

I don’t think that is quite the right explanation for the near non-existent productivity growth in the last few years. Investment has been picking up in the last few years (cyclically). One thing that will probably explain some of what has gone has been the increase in building activity, both in Chch and more broadly. Construction sector labour productivity is pretty low – perhaps esp on the sort of repair work that dominated Chch – but the need for that low productivity building activity to some extent skewed economic activity away from other higher productivity sectors.

Of course, over the next couple of years data revisions may change the whole picture of the last couple of years.

LikeLike

Two questions

1.

“then 25bps isn’t much of a move”

25 bps cut is a 12½% reduction on current rates – that’s a lot

2. Data Revisions? – can you explain

LikeLike

I think the appropriate reference point is the value of the principle – 25 basis points is 1/400th of that. I don’t think anyone would think 25bps in isolation would make the much difference – it is the sequence of moves that starts to matter (eg 125bps over the last year).

Data revisions: the HLFS (hours worked) won’t be revised) by there are often quite significant revisions to the GDP numbers. The quarterly data we have are quite provisional, and when SNZ gets the full set of annual data, it re-estimates that quarterly series. They publish annual national accounts each Nov/Dec, but for some of the data there is more than a year’s lag. So, for example, if it turns out that SNZ has been understating the level of real GDP by, say, 2 to 3% over the last year or two or three, that would make a big difference to how one interpreted the productivity numbers. Of course, inflation would still have been just as low it is, but it isn’t impossible that the economic background could look a bit more positive than it appears to have been. Then again, revisions could go in the other direction. In the end, it is really just a reminder that we shouldn’t ever put too much weight on recent GDP out-turns – here or abroad.

LikeLike

The Reserve Bank has an inflation target, not an economic performance one,

Thank you Micheal.

Remember I said the target should be wealth creation for NZ and NZer’s.

When we get that bit right the rest will fall into place.

But and there is always a but ain’t there?

Until the Govt. also accepts that this is also there responsibility nothing will change. everything starts there and it doesn’t include or exclude anything, including dumbed down immigration to supply shop assistance to $2.00 stores and increasing demands on our health and beneficiary systems.

I thought this last night was a very good summary of our position.

http://johnhcochrane.blogspot.co.nz/2016/06/wsj-growth-oped-full-version.html#more

LikeLike

I think Cochrane makes a useful and important point about the costs of regulation, altho I have some sympathy with the critics as to whether the data really support as strong a conclusion as his chart – with its particular way of presenting the information – suggests,

LikeLike

There is a simple principal at stake.

Do we want Kiwi’s to be wealthy or not?

If we do then lets start at that point and make policy to achieve that. Anything else is for losers.

Stop picking individual winners and sector winners and start creating the policy that makes opportunities for anyone to be a winner.

Now not everyone will take it up and not everyone will get it right but the more times we try the more likely we are to succeed. and then we have to stop stealing from people to hand out to others.

Removal of much legislation and Govt.Quangos would be a good place to start.

Most of these are repositories for potentially unemployed people. They go there because they can and fulfill mostly no useful purpose in the scheme of wealth creation. Indeed they become a leech on someone else’s earnings.

If we closed them down imagine what your unemployment figures would be like? (well for a time until they got off their behinds and did something useful).

The old Post Office and Railways of the past have been replaced by more upmarket , interfering social dogooders and we wonder why our productivity is such crap.

Look at the work H & S has created for businesses. There is no end to the paper work because that’s where Worksafe get all the convictions, on the lack of paper work. Never mind that Tradesmen etc should know what they are doing or be responsible for what they say they know. Worksafe have removed from employees any need to be responsible for their day to day effort. Some may argue but follow the court cases and see the affect.

Foss told me that they needed to change attitudes and that’s what this was all about.

It has, many I know are simply shutting up. Can’t be bothered any longer. If you can do a couple of cashies and a pension then why work?

We get pinged for 51KPH but that hasn’t made road deaths any less. Why, because Its the wrong target. So getting rid of stupid and useless legislation that 124 people use to justify their existence in Parliament has a lot of merit.

LikeLike

NZ households has debt of $170 billion(exclude investment property debt) with assets of $1 trillion plus which includes savings of $157 billion and investments in listed shares of $60 billion). Why would you consider NZ households not wealthy?

LikeLike