I did a brief radio interview this morning on the (hardly surprising) news that the Reserve Bank had approached the Minister of Finance for initial discussions on the possibility of adding loan to income limits to the list of (so-called) macroprudential instruments the Reserve Bank could use. Preparing for that prompted me to dig out the material on what has been done in the UK and Ireland.

It is worth remembering that the Reserve Bank does not need the Minister’s approval to impose loan to income limits. Some years ago, Parliament amended the Reserve Bank Act in a way that seems to have given the Reserve Bank carte blanche to impose pretty much any controls it chooses, so long (in this case) as they can squeeze them under the heading of matters relating to

risk management systems and policies or proposed risk management systems and policies

This was the basis they used for the two rounds of LVR controls, and various amendments, to date. In principle, controls could be challenged, on the basis that they were inconsistent with the statutory requirement to use the regulatory powers to promote the soundness and efficiency of the financial system. But the reluctance of banks to take on the Reserve Bank openly – the Bank always has ways of getting back at banks – and judicial deference on contentious technical matters effectively leaves the Governor free to do pretty much whatever he wants, at least as far as banks are concerned (the legislation gives him much less policy power over non-bank deposit takers, and none at all over lenders who don’t take deposits).

The memorandum of understanding with the Minister of Finance is non-binding, but ties the Bank’s hands to some extent. The MOU contains an agreed list of the sorts of direct controls the Bank might use. Legally the Bank can ignore that list. Practically, it can’t. But the Minister of Finance is also in something of a bind. Since the government has been unwilling to do very much to deal with the fundamental factors driving house prices, it would risk accusations of complete dereliction of duty if the Governor came asking for the power to impose new direct controls and the Minister turned him down. The controls might be daft, costly, and probably ineffective, but refusing the Governor’s request would be a gift to the Opposition (“do nothing Minister just doesn’t care; ignores sage Governor”, and so on). So most probably, if the Governor wants loan to income limits added to the MOU list, they will be added. It is still the Governor’s decision whether and how to use those powers, and if they go wrong, or prove unpopular, blame can be deflected to the Governor. (Unlike the Minister, the Governor doesn’t have to front up in Parliament for question time each day, can’t really be sacked, and generally faces limited effective accountability – ie questions with consequences.)

If and when loan to income restrictions are added to the list of permitted controls (not just when the Bank wants to deploy them), we should expect to see some rigorous and comprehensive analysis from the Reserve Bank, complemented by the Treasury’s advice to the Minister. Something that showed signs of thinking hard about the possible pitfalls, and which addressed the strongest case sceptics might make would be particularly welcome from the Bank – and novel.

Loan to income ratio limits have been applied recently in the UK and Ireland. I was interested to see a comment yesterday from Grant Robertson, Labour’s Finance spokesman, indicating that

his party could be willing to back central bank debt-to-income ratios, if they can be tailored to target investors.

However, Mr Robertson said it would not support a blanket debt-to-income ratio being introduced by the Reserve Bank as it would unfairly target first home buyers.

Presumably Robertson is unaware that in both the UK and Ireland loans to finance the purchase of rental properties (“buy to let” loans as they are known there) are explicitly excluded from the loan to income limits. It is an instrument that, if used at all, is in effect targeted at first home buyers, usually the owner-occupiers who will borrow the largest amount relative to income (quite rationally, since they also have the longest remaining span of working life).

The fact that a few other countries adopt controls does not make them a sensible response in New Zealand. But it is worth bearing in mind that the UK controls – under which mortgage lenders cannot lend more than 15 per cent of their total new residential mortgages (by number) at loan to income ratios of 4.5 times or above – were explicitly envisaged as non-binding at the time they were imposed. The Bank of England indicated that “most lenders operate within its new limit, so the measure will simply insure against potential risks to financial stability if mortgage lending standards loosen markedly in the future”.

Ireland is a little different, having come through an extreme house price boom and bust cycle, although even they noted that there was little sign that bank lending behavior was a problem in Ireland at present. In Ireland, no more than 20 per cent of the euro value of all new housing loans for owner-occupied properties can have loan to gross income ratios in excess of 3.5.

In neither case is there a blanket ban on loans with high loan to income ratios. Both countries have structured their limits as “speed limits” (as was done with the LVR limits here). Presumably the same would be done here, if LTI limits are introduced. Encouragingly, in both countries there is no differentiation by region, and our Reserve Bank should resist pressure for any regional differentiation here.

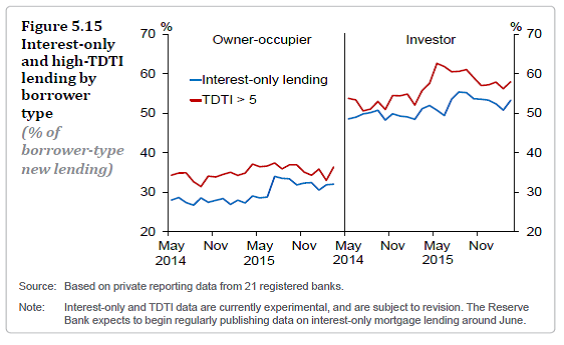

The controls are not easily compared across countries. In one case, the limit is by number of loans, and in the other by value. Both appear to use gross income in the denominator, but tax rates differ from country to country, and so the effective impact of the restrictions will differ for that reason alone. Our Reserve Bank recently published a chart suggesting that around 35 per cent of new owner-occupier loans have a debt to income ratio greater than or equal to five, but since this data is the fruit of “private reporting”, and is described as “experimental and are subject to revision”, we have no way of knowing whether either the “debt” or “income” concepts they are using – which may well differ by bank – are even remotely comparable to those used in the UK or Irish regulation.

(But it is worth noting that in the short run of experimental data, there is no sign of an explosion in the share of high debt to income lending.)

The income of a potential borrower is clearly one of things a prudent lender would take into account in deciding whether to lend money, and how much. The same goes for the value of any collateral the borrower can pledge, any other conditions or covenants that are part of the loan contract, and as host of other factors. But the fact that these considerations might be relevant to assessing the creditworthiness of the borrower does not mean they are things that should be regulated. As the Irish central bank noted in its consultative document

An acknowledged weakness in the use of LTI as a guide to creditworthiness is the fact that income at the time of borrowing may not be a good guide to average income over the life of the mortgage or to the risk of unemployment. Lenders need to take this into account in their lending decisions and must not rely mechanically on LTI.

And yet LTI limits increase the likelihood that banks will manage to the rules – breaches of which expose them to severe penalties – rather than to the underlying credit risk (where, all other factors aside) it is overall portfolio risk rather than the risk of an individual loan that probably matters a lot more – especially for systemic soundness. Curiously, an LTI limit risks making finance relatively more available to those borrowers with highly variable income – borrow in a good year, and your loan might not be excess of the LTI threshold, and no one at the central bank cares much that in another year’s time your income might have halved. It might be an unintended effect, but it won’t an unforeseeable one.

More generally, there is no good external benchmark for what an appropriate or prudent loan to income ratio should be. At least with LVRs there is a certain logic in suggesting that, say, a loan in excess of the value of the property changes the character of loan (the top tranche is unsecured). No one has any good basis for knowing whether a debt to income ratio (however either of those terms is defined) of 3 or 5, or 7 is unwise or excessively risky.

I don’t personally have a high appetite for debt – I’ve taken two mortgages in my life, both were about 2 times income, and both felt forbiddingly large at the time. Then again, the interest rate on the second of those loans were something like 10 per cent. But if, say, nominal mortgage interest rates were to settle at around 5 per cent – not low by longer-term international historical standards – then why would it be imprudent for a young couple aged 25 to take a 40 year mortgage at, say, six times their (age 25) income? The upfront servicing burden would certainly be high, but twenty years hence even general wages increase (no ,movement up respective scales) would have halved the burden. And why would it be imprudent for a bank to have a portfolio of mortgages which had some new mortgages at high LTIs and some well-aged mortgages with much lower LTIs?

(The same might go for investment property loans. If someone is running a rental property business, the prudent ratio of debt to income – whether wage income of the borrower or rental income – is likely to be much higher when rental yields are, say, 4 per cent than when they are 8 per cent.)

Don’t get me wrong. There is something obscene about house prices in New Zealand – and a bunch of similar countries with dysfunctional land supply markets. There is no reason why we can’t have house prices averaging perhaps 3 times income – with mortgages to match – but our policy choices have rigged the market, delivering absurdly high house prices. If so, people need to be able to borrow at lot just to get a toe on the ladder. Try to prohibit willing borrowers and willing lenders from agreeing such loans and you simply further skew policy in favour of the “haves”, and create an industry in getting round the controls. There hasn’t been that much effort so far to get round the LVR controls – through quite legal means, involving unregulated lenders – but recall the Deputy Governor’s comments at the last FSR, that controls might now be with us for much longer than the Reserve Bank had first envisaged. I’m not sure why the non-bank (and especially non deposit-taking) lenders have not been more active to date, but a further intensification of controls surely heightens the likelihood of larger scale use of alternative lenders.

Loan to value ratio controls haven’t solved, or materially alleviated, housing market pressures. For all the rhetoric, not even the Reserve Bank’s modelling suggested they would. There is some short-term relief – helping those not affected directly, at the cost of the more marginal potential borrowers – but it doesn’t last. There is no reason to think that loan to income ratio controls would be different. They tackle, rather ineffectually, symptoms rather than causes, and over time mostly alter who owns houses, not how much is paid for them. The Reserve Bank will argue that even if the controls don’t change house prices, they still enhance financial stability, but there is not even any serious evidence of that. First, they have not shown any evidence that financial stability is threatened – and their own tough stress tests keep delivering quite reassuring results – and second, and perhaps as importantly, they have made no effort to analyse what risks banks will take on if controls prevent them lending as much on housing as they might like. Banks are profit-maximizing businesses, and deprived (by regulation) of some opportunities they will surely seek out others.

Far better for the Reserve Bank to recognize that it has no mandate to control house prices (or even the growth of housing credit), and in any case it has no tools that will do much over time anyway. Its responsibility is the overall soundness of the financial system. If the risk weights on housing loans look wrong, let them make the case for higher weights and consult on that. If the overall capital ratios look too low, then again make the case. Using those tools will do less damage to the efficiency of the financial system, and better secure the soundness of the system, that one new wave of direct controls after another. At the current rate, Graeme Wheeler will be giving a good name to Walter Nash, the first person who imposed so many controls on our financial system. (I usually eschew references to Muldoon in this context, but over his full term he deregulated the financial system more than he reregulated it).

Of course, there is still no sign of those actually responsible for the house price debacle doing much about it. I haven’t yet read the full proposed National Policy Statement, but the material I have read is full of central planner conceit, and seems unlikely to achieve very much. And I find it seriously disconcerting – if perhaps not overly surprising – that the Ministry for the Environment released a supporting document yesterday on “International approaches to providing for business and housing needs” . But this survey of international approaches drew exclusively on the UK and two Australian states (New South Wales and Victoria). Since London, Sydney and Melbourne are some of the cities with the most dysfunctional housing markets in the world, indicated by price to income ratios similar to, or even higher than , Auckland’s, you have to wonder why MfE would look to those places for guidance or insight. When the Productivity Commission report on land supply was released last year, I criticized them for a similar focus – they’d visited various places, but not the functioning land supply markets of the US.

One might have hoped that government agencies, and ministers, who were serious introducing a well-functioning competitive urban land market might have devoted at least some serious analytical attention to the experiences of thriving cities in the US which manage to cope with rapidly rising populations with markets in which house price to income ratios fluctuate somewhere near 3.

Having said all this, I’m not very optimistic that the house price problems will be solved. I went to a good lecture yesterday on housing by the Chief Economist of Auckland Council, Chris Parker. He has a lot of good analysis and ideas which I can’t discuss here – he told us it was under Chatham House rules, under which we could say what was said, but not who said it, but he was the only speaker….. – but I wanted to ask him the same question I’ve posed here previously: is there any example anywhere of a city or country that has materially unwound the thicket of planning controls once they were in place. If not, perhaps we can be first. But, if so, it doesn’t look as though we are getting there fast.

(Which does make the government’s continued indifference to the huge population growth, largely driven by immigration policy when there is no evidence that that population growth has been systematically benefiting New Zealanders, ever more inexcusable).