As I noted in my post on Saturday, were I British I would be voting for Brexit, and so I’m pleased to see the polls moving that way. Should that cause succeed, there is likely to be considerable disruption, both to Britain, the other EU countries, and to the wider world economy and financial system. Perhaps it will be the episode which illustrates the point I and others have been making for several years: when interest rates are already at or very near the effective floor, and there is little fiscal room left, any new serious adverse shock will expose countries as having few tools left to respond. Central banks and governments that have done nothing about removing the near-zero lower bound would then have something to answer for.

In the Telegraph a day or two ago, Ambrose Evans-Pritchard had a powerful column articulating his own reasons for voting to leave the EU. It was all the more powerful because it recognized and gave full weight to the transitional disruptions that are all but certain, and to the possibility that even in the medium term there might be some economic costs. The cause of freedom – the ability to set one’s own laws, appoint one’s own judges, and toss out elected leaders – might have a price, and he thinks it is a possible price worth paying.

In my post the other day, I noted that there were other examples of people being willing to pay such a price. By the end of the 19th century Ireland was an integral part of the United Kingdom, with full representation at Westminister and unrestricted markets in goods, services, people, and capital. And yet the cause of Irish independence gained strength rather than abated, and the south eventually gained independence, as the Irish Free State, in 1922. Ireland kept on using sterling, and kept close economic ties to the UK – as one would expect, given the proximity of the two countries and the previously highly-integrated economies. But no one thinks Irish independence was good for Irish material living standards in the subsequent decades.

Here are the data in the Maddison database for GDP per capita. The first observation is for 1913, before the disruptions of World War One, and the subsequent unrest leading up to independence.

I’ve also shown the data for 1929 (the eve of the Great Depression) and 1939 (the eve of World War Two, which Ireland stayed out of). There is always a lot else going on, so the whole story of Irish relative economic decline isn’t (the policy choices/constraints that followed) independence. But much of it was. Today, of course, Irish real GDP per capita is higher than that of the United Kingdom.

I’ve also shown the data for 1929 (the eve of the Great Depression) and 1939 (the eve of World War Two, which Ireland stayed out of). There is always a lot else going on, so the whole story of Irish relative economic decline isn’t (the policy choices/constraints that followed) independence. But much of it was. Today, of course, Irish real GDP per capita is higher than that of the United Kingdom.

Was independence a mistake? Well, it had a cost, but most things people count worthwhile do.

I got curious about some other post-colonial episodes, each involved economies much less integrated with the UK than Ireland’s had been.

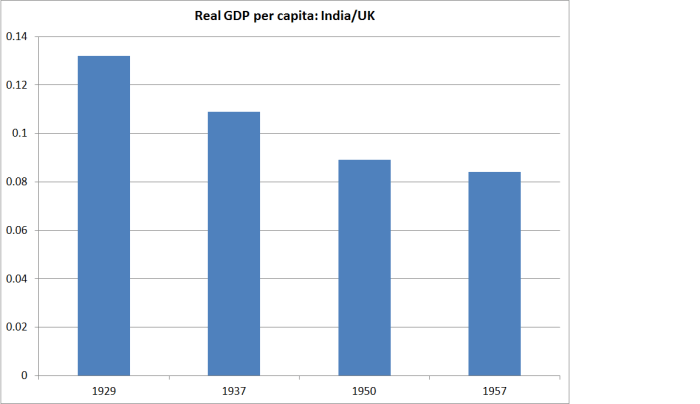

India, for example, became independent in 1947. In the late 1920s, full independence probably appeared to be many decades away, and probably wasn’t influencing investment choices or other economic decision-making.

Independence came at a cost – wars in addition to any economic cost – but with hindsight would the Indians have chosen continued colonial rule? Almost certainly not.

I spent a couple of years working as an economic adviser in Zambia. At independence in 1964, Zambia had had GDP per capita as high as those of South Korea and Taiwan. By the early 1990s it was something of a byword for basket cases (Zimbabwe’s true awfulness was still to come). But here are the comparisons with the UK – not, itself, a great economic success story over these years.

There were a few people who regretted independence – my colleague, the (local) chief economist lamented to me one day that the British had left when they did. But it wasn’t a very common sentiment (or one that was politically acceptable to voice).

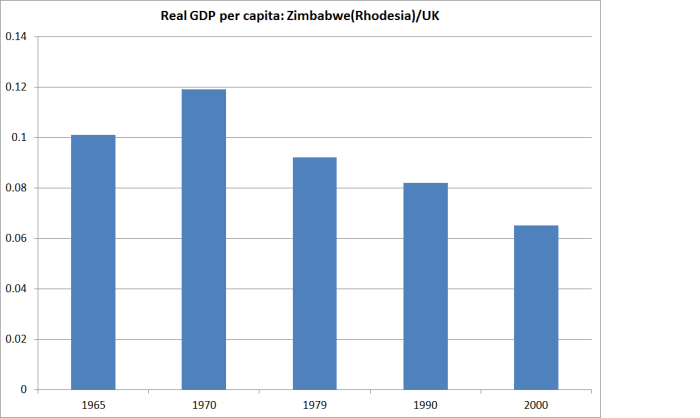

How about Rhodesia/Zimbabwe? There was a two-stage process. The white-minority government declaring unilateral independence in 1965, and then full legal independence with a universal franchise came in 1980.

In the first few years after the UDI there doesn’t seem to have been a material economic cost. Those who supported UDI probably thought of it as some sort of win-win. It didn’t last – the country soon descended into an insurgent war – and of course the economic consequences after independence in 1980 are all too apparent. I can imagine that quite a few Zimbabweans might really regret the course of the last 35 years – though not, I imagine, too many members of ZANU-PF.

My final example is Bangladesh. At Indian independence in 1947, what is now Bangladesh became East Pakistan. But in 1971, after brief but awful war Bangladesh became independent.

Pakistan has scarcely been an Asian tiger – model of economic transformation. Bangladesh has done worse.

Inevitably this has been a rather limited exercise, focusing on countries in which I had an interest (NZ Baptist churches have had missionaries in what is now Bangladesh for 130 years), and where there is accessible – if probably no better than indicative- data.

I didn’t include New Zealand, Australia, and Canada because in all three cases there was no clear point at which the countries broke away from Britain. It was an evolutionary process. Perhaps in an ideal (economic) world, if Britain were going to pull back from the EU it would do so in a similarly evolutionary way. But that option doesn’t seem to have been available.

And there may well be other examples of countries which flourished with independence – Singapore is perhaps the striking example (although productivity growth in Singapore over say 1960 to 2000 was very similar to that in Hong Kong, which was British-ruled for almost all that period). My point is not to argue that independence, or taking back parliamentary sovereignty, is inevitably or even generally costly. I’m sure it isn’t. But it can be. And that may well be a price that citizens, even with hindsight, think is worth paying.

The relationship of Britain to the EU today isn’t that between, say, colonial Zambia and the UK, or even East Pakistan to West Pakistan. But, equally, Britain has strong established institutions and, if Brexit happens, every motivation, and plenty of opportunity, to secure pretty good economic outcomes. If Brexit happens, I suspect that in 30 years time – perhaps 100 years time – scholars will still be debating what the long-term economic consequences of exit were (as indeed, they are still debating the economic consequences for Britain of entering the EU 43 years ago). If so, perhaps the economic issues are not of first-order significance.