I had heard that The Treasury was thinking of starting a blog, and the other day I noticed on their website two new pieces under the heading “Treasury Staff Insights: Rangitaki”. On checking, ‘rangitaki’ appears to be the Maori word for blog.

Blogs are becoming a bit more common in official agencies these days: several of the regional Federal Reserves have them, as does the IMF. And the Bank of England launched one last year. I wrote about the Bank of England one here, welcoming it, but being rather skeptical as to whether its avowed aim could, or even should, be met.

Bank Underground is a blog for Bank of England staff to share views that challenge – or support – prevailing policy orthodoxies.

I don’t read Bank Underground all the time, but I’m not aware that anything they have published in the last year has in fact challenged “prevailing policy orthodoxies”, unless it was in areas where the Governor himself wanted something challenged.

The Treasury description of their aim is less ambitious – and, hence, probably more realistic.

In their Staff Insights: Rangitaki articles staff are writing in their individual capacity or in a Treasury team’s capacity and the views are not necessarily a “Treasury” view. The goal is to focus on the analytical content and insights.

In that respect, it isn’t so different from the approach taken to formal working papers, policy perspectives papers etc that Treasury has published over the years – or to stimulating work in progress pieces such as the one by Struan Little that I wrote about a few weeks ago. The Reserve Bank does something similar with their Analytical Notes series. The main difference, at present at least, is that the blog pieces are rather shorter.

In general, I welcome having the analytical work of public servants in the public domain, and favour more rather than less pro-active release of material Treasury (and other departments) have been doing. But there is a balance to be struck. Treasury exists primarily as the adviser to the Minister of Finance – it isn’t an independent agency, and over time its effectiveness can be compromised if, say, a Minister were to feel that Treasury was attempting to use its publications (and perhaps especially ones like this) to make end runs around government policy, pursuing its own agendas. And equally, we would want to be cautious that pieces on the blog weren’t being used, in a rather informal way, to champion government PR messages. Time will tell how the model works – and how robust it proves to be to a different Minister of Finance.

One of the blog posts, on the insurance market’s move to sum insured house insurance policies, has already had quite a bit of media coverage. But it also highlights some of the limitations of the blog format for a policy agency. It discusses some potentially interesting investigative work Treasury has done, but provides no details, so we have as readers and citizens have no way – without OIAing the underlying papers – to gauge whether the Treasury approach is reasonable. Blog posts to promote new, more detailed, background papers might be more helpful.

The second blog post, by Mario di Maio, is headed “Chinese-New Zealand investment flows”, (although actually the focus of the piece is not on flows at all, but on changes in stocks). The author starts

Foreign investment flows into New Zealand assets raise a host of legal, political and economic issues. Often the political issues of the day and the source of the investment can obscure the longer-term trends. At the moment, risks around a smooth transition of the sources of growth for the Chinese economy have seen an acceleration of capital outflows. We decided to abstract from these near-term issues and take a longer perspective on what might happen to two way flows and stocks of investment between New Zealand and China over the next several decades.

In fact, they only look out to 2030, which is now not much more than a decade away. (And note that delicate public service phraseology “at the moment, risks around a smooth transition of the sources of growth” – not a hint of political crackdowns, inadequate protection of property rights, or fear of devaluation).

The author reports a scenario in which if China liberalizes its capital account the stock of Chinese investment in New Zealand and New Zealand investment in China would increase reasonably materially between now and 2030.

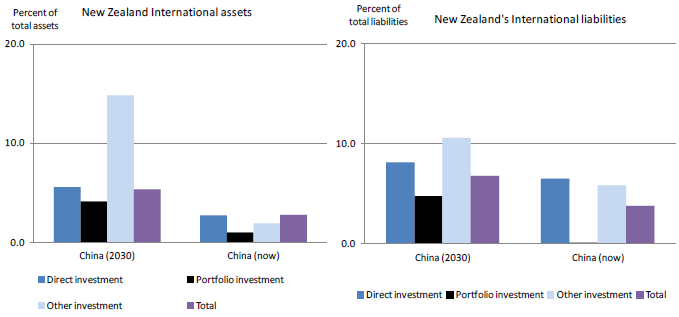

Here is the chart

Again, it cries out for more detail. The broad direction of change looks plausible enough (as one scenario), but why (for example) would we expect to see such a huge increase in the “other investment” component of New Zealanders’ investments in China? I presume there is a good reason, but it isn’t outlined here. Overall, what is perhaps noteworthy is how small the net position vis-à-vis China remains: in 2030 New Zealanders’ liabilities to Chinese entities would be around 7 per cent of New Zealanders’ total external liabilities, and New Zealand entities’ claims on Chinese entities would be around 5.5 per cent of New Zealanders total offshore assets.

But it also isn’t clear what assumption the author is making about China’s own overall NIIP position. He assumes New Zealand’s remains at around the current level which – unsatisfactory as it for such a low productivity growth economy – at least has the appeal of being the level around which it has fluctuated for the last 25 years or so. But the authors – and those he draws from – appear to be optimistic on China’s ability to continue towards upper-middle income status (closing those gaps highlighted in this morning’s post) in a generally much freer economic environment. But in such an environment it might not be unreasonable to expect to see China running material current account deficits for many years – many successful emerging economies (including Singapore and Korea) did. If so, we might still expect to see some gross outflows from individual Chinese people and firms, but it would be a quite different environment than the climate of the last decade or so, in which large current account surpluses and then large accumulated reserves made first for large official capital outflows, and more recently large private capital outflows. I don’t know what the right answer is – and am probably more skeptical than the author on China’s future progress – but his scenario probably doesn’t have much information in it without a lot more supporting detail.

Which does raise the worrying concern that the point of the blog piece might have been more about promoting a political message. Following the scenario, the piece continues:

Foreign investment from (and into) China is likely to increase significantly over time. This could potentially take some time or might occur more rapidly and would contribute positively to New Zealand economic performance at the margin. The maintenance of a stable and predictable business environment will be an important factor in ensuring that foreign investment flows from China benefit New Zealand.

Even the first claim is arguable – as his chart shows, even countries like South Africa and Argentina (neither the most repressive nor the freest) have gross international assets and liabilities not much different than China’s level today. But the second claim – that this “would contribute positively to New Zealand economic performance at the margin” seems to built on not very much at all. As I’ve said repeatedly, I’m generally supportive of a pretty open approach to foreign investment, but…..(a) di Maio’s scenario is built on the assumption that the net IIP position for New Zealand doesn’t change (as a share of GDP) so increased Chinese foreign investment largely (net) just replaces some other foreign investment, and (b) China is not an economy where market disciplines are consistently allowed to work, and as is well-recognized all major Chinese firms effectively operate within the limits set by the Party, and (c) China (and Chinese firms) have not shown the capacity to generate world-leading economic performance. Against that backdrop (and without suggesting that Chinese investment should be restricted), there is likely to be much more open question about the benefits to New Zealand of increased Chinese investment than the author allows. Curiously, he writes that “the maintenance of a stable and predictable business environment will be an important factor in ensuring that foreign investment flows from China benefit New Zealand”. Actually, I’d have thought it was much more important that the business environment in China become more stable and predictable, governed by the rule of law amid secure property rights. Then we really could be more confident that increased foreign investment would benefit both sides. But I guess Treasury officials – even speaking in a personal capacity – probably couldn’t say that openly.

The final paragraph of the post also tilts towards advertorial,

Some specific investments have been taken that can smooth two-way investment flows between China and New Zealand.This includes negotiation of a swap agreement (RMB 25 billion / NZ$5 billion) between central banks to provide liquidity to support trading in RMB; (ii) the issuance of RMB denominated corporate debt by Fonterra; and (iii) the registration of three Chinese-owned banks in 2013 and 2014. That most of the increase will occur in portfolio and other investment flows suggests where attention might focus in the coming decade.

“Investments” is an odd choice of word, but even setting that to one side the argument seems a little flimsy. The New Zealand dollar trades freely, and our central bank does not have (or need) swap agreements with the central banks of other countries with liberalised current accounts. The RMB swap agreement, like those other countries have done with China, is best seen as a piece of political theatre – not harmful, but of no real value to New Zealand in anything other than political terms either. Similarly, the choice of a major corporate which has a very large investment in China to issue some RMB-denominated bonds also doesn’t look like an “investment”, or something that will “smooth two-way investment flows”, although the ability for Fonterra to issue those bonds might be a welcome reflection of China’s liberalization to date. And finally, the choice of three government-controlled Chinese banks to set up here, doesn’t look like an “investment” either (at least not by New Zealand). If anything, we should probably think of it as a new area of risk for New Zealand. Government-owned or controlled banks have a bad record globally, often allocating credit in directions, or on a scale, not that conducive to economic stability or efficiency. It should also be a concern that all three banks are chaired by former National Party MPs, only one of whom has any past banking experience. That choice by the Chinese shareholders suggests that they have imported their “connections” model of doing business to New Zealand. One would hope that our political and official institutions are strong enough, that those connections really don’t matter, but it should be worrying trend, not a reassuring one.

And I’m left puzzling what the final sentence means. Even if this (single) scenario were correct and there was the be a material increase in Chinese portfolio investment into New Zealand in the next decade, it isn’t obvious that that has any particular policy implications. But perhaps I’m missing something obvious.

The Staff Insights blog series is an interesting new initiative. It is in the spirit of the generally quite open approach that Treasury takes to things (including the Official Information Act). I will certainly keep an eye out for future releases in this series, but I suspect they still have some way to go in finding quite the right model for the sorts of material to present in it.