In a couple of posts earlier last week, I used the regional (nominal) GDP data, showing how weak Auckland’s per capita GDP growth appears to have been over the last 15 years (the period for which the data exist). And it didn’t appear that terms of trade changes could explain the regional patterns, since most of the gains in New Zealand’s terms of trade has reached our shores in the form of lower import prices, the effects of which should have been quite pervasive across the economy.

But as I got to the end of the second of those posts, I started to get a bit uneasy about the data. I had noted that over the 15 years, Auckland’s population had increased by 30 per cent, and that of the rest of the country by only 13 per cent. And yet, over the years (to 2013, for which we have detailed industry breakdowns), construction had been a smaller segment of Auckland’s GDP than in most other regions in the country. This was the chart:

I started digging into the data a bit further, and also got in touch with Statistics New Zealand (who provided me with some prompt, very helpful, assistance, including suggesting that some readers might be interested in how they put the numbers together). My digging didn’t resolve any puzzles, but it didn’t highlight any very obvious errors either.

In a city with a rapidly growing population one would normally see a larger share of GDP devoted to construction (than at other times, or other places). Construction isn’t just about houses, but the whole panoply of structures that a growing population needs over time.

Over the 15 years to 2015, Auckland accounted for 50 per cent of all the population growth in New Zealand. And yet here is the Auckland share of the value of all building consents, and the Auckland share of the construction component of GDP (for which we only have regional data to 2013).

One wouldn’t expect an exact mapping, since the two series are measuring quite different things (quite a bit of construction won’t need a building consent), but both are a long way below Auckland’s share of population growth (and Auckland’s share of population growth was highest in 2001 and 2002).

The regional GDP data also have two components that should normally have a strong relationship with housing, and also with population growth. These are:

| Rental, hiring, and real estate services |

| Owner-occupied property operation |

The latter series is straightforward – in effect, the rental value of living in an owner-occupied house, which is proxied using market rental data.

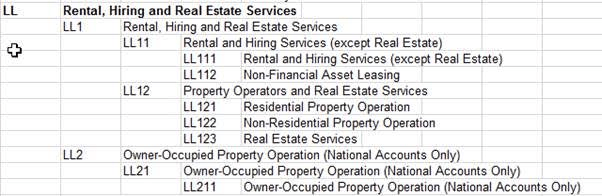

The “rental, hiring, and real estate services” is more complex. It includes various sub-categories, for which the data are not provided separately. Here is what is included, from a table SNZ sent me:

Ideally, I would like to look at only the LL12 and LL2 components, and thus exclude the non real estate leasing services (eg cars, machinery etc), but the data aren’t publicly available.

Surely, I thought, if Auckland’s population has been growing so much faster than the population in the rest of the country, this should be reflected in faster growth in these components of GDP. I didn’t really expect it in respect of owner-occupied dwellings, because although Auckland rents have risen a bit faster than those in the rest of the country, rates of owner-occupation have been falling faster. But everyone needs to live somewhere, renting if not owning, so I thought the effect should still show up if I combined the two components. After all, the rental component also includes non-residential property, and more people generally implies more offices and shops too.

But this scatter plot is what I came up with (population growth on the x axis and growth in the sum of the two GDP components on the y axis):

I’d expected to see an upward-sloping relationship (recall, these aren’t GDP per capita components, but total GDP). As I put it to SNZ, isn’t it a bit puzzling that growth in these two nominal GDP components over 13 years was greater in Southland than in Auckland? Given where all the other regions sit, in a well-functioning housing market surely one might have expected the growth in these GDP components for Auckland to be up in the 140 to 160 range?

SNZ were able to tell me that there was a large growth, from a low base, in non-financial non real estate asset leasing in Southland. That might help explain why these GDP components together grew surprisingly fast in Southland. But it doesn’t explain why Auckland has been so weak relative to almost all the other regions (given the extent of its population growth).

Here is a chart showing Auckland’s share of total nominal GDP for each of these two components.

And yet over this period Auckland’s share of the total population increased from 31 per cent to 33.5 per cent.

I guess that, overall, this is not wholly inconsistent with the divergence that has opened up in the population per dwelling numbers: trending down in the rest of the country but not in Auckland as house prices become increasingly unaffordable.

Out of curiosity, I redid the per capita regional GDP numbers excluding these two real estate related components. In my original chart, Auckland had the third slowest growth in nominal per capita GDP from 200 to 2015. In this alternative chart, we have the data only to 2013. Over that period, Auckland had the slowest per capita total nominal GDP growth of any region.

What about on this adjusted, non-real estate, measure?

It doesn’t improve the picture.

I’m still not quite sure what to make of all this. Ideally, we would have regional real GDP data, but unfortunately that does not appear likely any time soon. But on the basis of what we have, Auckland seems to have done particularly poorly over the last 15 years, despite (or partly because?) all the policy-induced population growth. Some of that seems to relate to the poorly functioning housing supply market. But even abstracting from the direct effects of that, it has to be seen as a pretty disappointing outcome, leaving many questions on the table.

(It also leaves me with some new questions, which I have not yet attempted to work through in my own mind, about my explanation for New Zealand’s persistently high (relative to other countries) real interest rates. A topic for another day.)

I am unsure exactly what you are trying to measure but the results indicate that it is better for NZ to be totally westcoasters. It is better for NZ that we just laze about and go fishing each day and feed off the dole?

LikeLike

Productivity lost to other regions because of Auckland’s woeful transport infrastructure?

LikeLike

average GDP per capita is still higher in Auckland than in most of the country, but growth has been slower, so that gap in Akld’s favour has closed somewhat since 2000.

LikeLike

Hmm, well lots if us live two to a house but not the Indians and Chinese.and maybe others. You also have a huge student influx, many of which probably live in student type hostels. Perhaps it has to do with the type of immigrants. (a favourite subject.Ha). Not sure how this would come to play but Auckland would have had many empty houses like other places over the last few years. Of course many of us who have to deal with Aucklanders would naturally say they drag the chain for the rest of us. How long is the place? How long does it take to go anywhere?

Interesting puzzle.

LikeLike

Travelling distance from leigh, right at the top of auckland region to pukekohe at the south end of Auckland is 129km. Compare that with Houston with 6 million people, from Woodlands at the top to Texas city at the bottom is 118km.

LikeLike

Michael, It may be interesting to break your analysis into sub-periods; namely 2000 – 2005, 2006 – 2010, 2011 – 1014…

The reason is what happened to the Auckland residential and overall construction market in the wake of the GFC and the collapse of finance companies. The collapse of finance companies and the bankruptcy of many developers left a lot of projects stranded (the infamous hole in the ground in Ponsonby now being built into a supermarket for one)…

The collapse of the finance companies (setting aside the many many isses around that) deprived the developer market of a source of funding that has taken some years to be replaced… foreign firms tired to strip 35% returns from developers in the intervening period… and some tried ‘innovative’ equity scheme… just look at the fuss over Albany Heights…

Short point there was a considerable disruption to the developer market, and on top of that the endless issues with the disaster that is Auckland Council and its consenting process…

So by looking at sub-periods it may reveal some new information to help explain the puzzle…

Cheers

B

LikeLike

Nothing to do with the GFC, NZ was already well entrenched in a deep recession due to aggressive interest rate rises with the OCR reaching for 9%. The GFC was a saviour with Allan Bollard suddenly dropping the OCR after giving every indication of pushing the OCR beyond 10% completely ignoring the collateral damage to the building industry.

LikeLike

Thanks. An interesting idea, which I might explore later.

LikeLike

Auckland is more than ever viewed in that context and, as an investment destination, is now fairly seen as equivalent to any city in the world, albeit it a small marketplace.

“The city’s growing population and maturing critical mass means the CBD has already been recognised as a destination by international luxury and fast fashion retailers – one example of the confidence being shown. Also, a record three million visitors came to New Zealand last year, 70 per cent arriving into Auckland.”

http://m.nzherald.co.nz/brand-insight/news/article.cfm?c_id=1503637&objectid=11624569

LikeLike