On Saturday afternoon I found myself in an email exchange with a couple of people about how the composition of bank lending had changed since 1984. I wasn’t quite sure where the table I was responding to had come from, but when I eventually got to the business section of Saturday’s Herald I found the answer. Brian Gaynor had devoted his column to a discussion of the changing significance of banks in recent decades, portentously headed “Banks’ long shadow over New Zealand economy”. I found myself agreeing with almost none of his interpretation.

My alternative story has two key strands:

- the institutions we label “banks’ have become more important in the financial system as the incredible morass of restrictions built up since the days of Walter Nash were removed, first (too) slowly, and then in a great rush over 1984/85. That has allowed the financial system to become much more efficient. Financial intermediation is now undertaken mostly by those best placed to do it, rather than increasingly by those either subsidized by the government to do it, or just outside the network of controls and so still free to do it.

- total credit to GDP (and especially the housing component) has risen mostly because of regulatory restrictions on building and, in particular, on urban land use. Higher housing credit is mostly an endogenous response to this policy-created scarcity.

There are all sorts of caveats to the story. In some respects, banks are much more heavily and directly regulated now than they have ever been (and that burden is only getting heavier with LVR controls which threaten a new wave of disintermediation). The “too big to fail” problem probably skews things a little too far towards banks (but adequately price deposit insurance and banks will still remain dominant), and at times banks get over-enthusiastic about increasing lending to particular sector and sub-sectors. But, fundamentally, the rising importance of banks (relative to other intermediaries) has been a good thing not a bad one, and if one might reasonably be ambivalent or even concerned about the rise in household credit, that has been an almost inevitable consequence of artificial shortages created by central and local government. Given the determination of our leaders to mess up urban land supply, in a country with a fast rising population, it would have happened in one form or another, and it is better that it has been done by efficient intermediaries. Concerns should be addressed to central and local government politicians who keep the housing supply market dysfunctional, not to bankers.

At this remove, it is probably hard for many to appreciate quite what the New Zealand financial system was like in the heavily regulated decades. Old New Zealand Official Yearbooks will give a good flavour, and the Reserve Bank published in 1983 a 2nd edition of its Monetary Policy and the New Zealand Financial System, which has lots of detail (the 3rd edition is a quite different book – a weird confusion, which I take responsibility for).

In addition to the Reserve Bank – which lent, not just to its staff, but also to the major agricultural marketing bodies – we had:

- trading banks (each established by statute, with no new entrants for many decades)

- private savings banks (savings banks subsidiaries of the trading banks, introduced in the early days of deregulation in the 1960s)

- trustee savings banks (a different one in each region, some large and strong, some tiny)

- the Post Office Savings Bank

- the Housing Corporation (government mortgage finance)

- the Rural Banking and Finance Corporation (govt rural finance)

- the short-term official money market

- finance companies

- the PSIS

- building societies (terminating and permanent)

- life insurance and pension funds (large and fast-growing supported by a tax regime, and fairly large lenders)

- the Development Finance Corporation

- stock and station agents

And that was just the institutional entities – almost all with different statutory and regulatory powers and restrictions. And there was a very large non-institutional market in finance – notably, the role of solicitors’ nominee companies in mortgage finance.

Trading banks had never been dominant providers of finance in New Zealand – since they had not historically provided mortgage finance, whether to farmers or for households – but even in their role as providers of, typically, short-term finance to business, they had been withering (under the burden of regulatory restrictions) for decades. As the Reserve Bank noted in its 1983 book, “trading bank loans and investments have fallen from being around 50 per cent of GNP in 1930 to around 25 per cent of GNP in 1981”. As far as I can tell – it was my impression back then, when writing an honours thesis on the disintermediation process, and it is my impression now – that the only people who benefited from this state of affairs were the people running the entities subject to a lighter burden of regulation. My schooling was mercifully free of so-called “financial literacy” education, but the one message I recall being drummed in repeatedly (reinforcing the one from my father) was that it was very difficult to get a mortgage, and one had to spend years building a track record that might allow one to go, on bended knee, to a lender, seeking as a special favour access to such credit. But if you were on a lower income, the state would provide. Alternatively, coming from a well-off family, or getting a job in an organization with concessional staff mortgages, was the way to go. (Reserve Bank concessional loans were very good, although in the end I had one for only 2 months.)

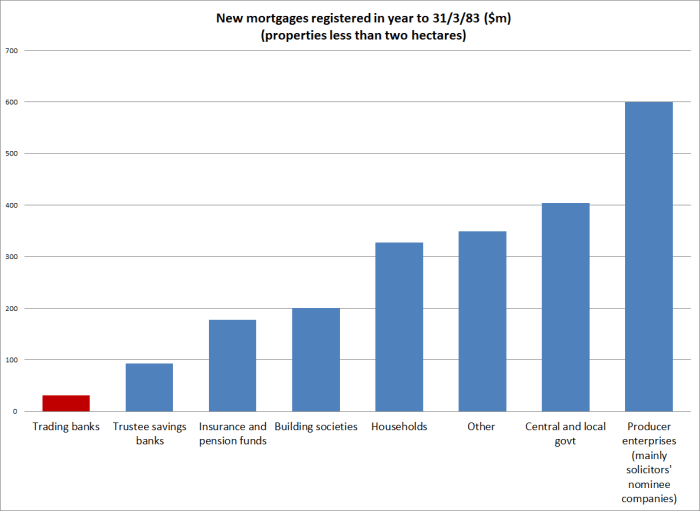

Gaynor quotes statistics showing that trading bank housing lending was 14 per cent of total lending in 1984 and is 52 per cent now. But look who did housing lending back then. This chart is drawn from the 1984 New Zealand Official Yearbook, and shows the flow of new mortgages (on properties less than 2 hectares, so largely excluding farm mortgages) in the year to 31 March 1983.

Trading banks barely figure at all (and this includes their private savings bank loans, and loans to staff). Most mortgages by then were being made through the Housing Corporation, within families, or through solicitors’ nominee companies. Neither of the latter two offered much diversification, a key way of making available affordable finance. Call me a relic of the 1980s if you like, but I count it as huge step forward that large and efficient private sector entities are now the main vehicle for residential mortgage finance.

I mostly want to focus on housing lending, but Gaynor also notes in support of his case

The first point to note is the huge fall in lending to the manufacturing sector, from 24.5 per cent of total bank lending 30 years ago to only 2.8 per cent at present. This reflects the deregulation and demise of manufacturing, which was also the result of policy initiatives by Sir Roger Douglas and the fourth Labour Government.

Yes, the relative importance of the manufacturing sector in the economy has shrunk – perhaps more than it would have in a better-performing economy – but by my calculations drawn from Gaynor’s table, trading bank lending to manufacturing ($1.6 bn) was around 3.5 per cent of GDP in 1984 and at $11.4 bn is around 5 per cent of GDP now. Across all the financial intermediaries that existed in 1984, the share would have been higher, but the overall picture is a quite different one from that Gaynor paints.

But what about housing lending? Gaynor asserts that

The clear conclusion from this is that anyone who bought a house in the early 1980s has been extremely fortunate because aggressive bank lending has been a major contributor to the sustained rise in house prices over the past few decades.

Since 1980/81 was the trough of a very deep fall in real house prices, there is no doubt that it was an ideal time to have bought. And there is also no doubt that there has been an aggressive (and almost entirely desirable) process of re-intermediation. Some entities that weren’t trading banks became trading banks (or ‘registered banks’ as we now know them) – think of Heartland, SBS, ASB, PSIS – or were directly purchased by banks (think of the United or Countrywide building societies, or Trustbank or Postbank), and in other cases banks just won market share away from other participants in the market (no need for a solicitor’s second or third flat (short-term interest only) mortgage when you could get a 80 per cent table first mortgage at the local bank branch).

But is there any evidence that “aggressive lending” by the financial sector (now mostly ‘banks’) has been a “major contributor” to the huge rise in real house prices in recent decades? I think the evidence is against that claim. Why?

First, “aggressive lending” usually ends badly. It did for the banks when they lent on the massive commercial property and equity boom post-1984. It did for the finance companies with aggressive property development lending in the years up to 2007. It did for the banks with dairy lending (both in 2008/09 with a surge in NPLs and perhaps again now – going even by the Reserve Bank’s own stress test). Housing lending, by contrast, has not ended badly, even though the push by banks into housing lending has been going on now for more than 25 years, through several economic cycles and one very nasty recession. It is easy to say “just wait”, but history is strongly against that proposition. Inappropriately aggressive lending goes wrong much faster than that.

Second, while the lending terms of banks have become easier than they were 25 years ago – when banks were just finding their way in this new market for them, and nominal interest rates were still extraordinarily high – they are not noticeably looser (at least in asset-based terms) than the terms applied by other housing lenders in earlier decades. 80 or 90 per cent 30 year mortgages from the Housing Corporation weren’t uncommon (or inappropriate for a young couple with decades of servicing capacity ahead). Banks, including the Reserve Bank, had long lent those sort of proportions to their own staff. And, on the other hand, we have not had any material amount of mortgage business written with LVRs above 100 per cent, or with terms of 100 years or beyond (things seen in various European markets at times). Overall, credit conditions are probably easier than they were, but not in way that is self-evidently inappropriate or overly risky for either borrowers or lenders. The Reserve Bank’s housing stress test backs that conclusion – taking account of the joint risk of losses in asset values, and losses in servinig capacity (if unemployment were to rise sharply).

Third, there is a simpler explanation for high house and urban land prices. Regulatory land use restrictions combined with population pressures (including policy-driven immigration ones) are a more persuasive story, including in explaining why house prices in Auckland have increased so much more than those elsewhere. In New Zealand we have only one fairly large city, but think of the situation in the United States: there is a fairly unified financial system (albeit with some state level differentiation in restrictions) and yet we find huge increases in house prices in places like San Francisco (with tight land use and building restrictions) and very modest real increases in large and growing places such as Houston, Atlanta, Nashville and so on. High house prices, and high house price to income ratios, are not an inevitable feature of a liberalized financial system. They aren’t an inevitable feature of tight land use restrictions either, but the correlation across cities is pretty good.

And if finance were primarily responsible, finance would also have brought forth lots of new supply. That is way markets work – it is part of the reason why credit-driven booms don’t last that long. Instead, prices have been bid up largely as a result of regulatory constraints: there are not consistently excess profits lying around that developers can readily take advantage of.

And if finance were primarily responsible, finance would also have brought forth lots of new supply. That is way markets work – it is part of the reason why credit-driven booms don’t last that long. Instead, prices have been bid up largely as a result of regulatory constraints: there are not consistently excess profits lying around that developers can readily take advantage of.

Of course, higher house prices typically mean that buyers of houses need more credit than they otherwise did. If house prices suddenly double because some regulatory change makes land scarcer, then with incomes unchanged either people can wait (much) longer to buy, saving a larger deposit, or they can borrow more to complete the purchase. If the people who wanted to buy, but are reluctant to take on more debt, do hold back, someone else will buy the property. And that person will need finance – either debt or equity. If banks are reluctant to lend on houses, then houses will tend to be owned by people who are least dependent on debt: those with large amounts of established wealth already. All else equal, since few people get into the owner-occupied housing market without debt, that would be a recipe for even larger falls in owner-occupation rates than we have already seen.

Much of the overall increase in housing debt in New Zealand (and other similar countries) in recent decades has been the endogenous response to the higher house prices, rather than some independent factor driving up prices. And these forces take a long time to play out.

In the chart below I’ve done a very simple exercise. I’ve assumed that at the start of the exercise, housing debt is 50 per cent of income, house prices and incomes are flat, and people repay mortgages evenly over 25 years. Only a minority of houses is traded each year, but each year the new purchasers take on new debt just enough to balance the repayments across the entire mortgage book.

And then a shock happens – call it tighter land use regulation – the impact of which is instantly recognized, and house prices double as a result. Following that shock, house purchasers also double the amount of debt they take on with each purchase, while the (now rising) stock of debt continues to be repaid in equal installments over 25 years.

In this scenario remember, house prices rose only in year 1. There is no subsequent increase in house prices or incomes. But this is what happens to the debt to income ratio:

In this particular scenario, 100 years after the initial doubling in house prices, the debt to income ratio is still rising, solely as a result of the initial shock, converging (ever so slowly by then) to the new steady-state level of 1. One could play around with the parameters, but a permanently higher level of real house prices will, in almost any of them, produce a permanently higher level of gross housing debt, and it will take many years to get to that new level. The flipside, which I could also show, is the deposit balances of the other parts of the household sectors – the young who have to save for a higher deposit (even for a constant LVR) and the older cohorts who extract more money from the housing market when they downsize or exit the market. Higher house prices do not, of themselves, require banks to raise more funding offshore.

This is deliberately highly-stylized, but it is designed to illustrate just two main points: higher debt ratios can be primarily a symptom of higher house prices (rather than any sort of cause) and the adjustment upwards in debt levels following an upward house price movement can take many years to work through. And there is one more important point: this a process that mostly reallocates deposits and credit among participants in the housing market: it needn’t materially affect the availability of credit, or economic opportunities, in the rest of the economy.

None of which is to suggest that higher house prices, as a result of some combination of regulatory measures (eg land use restrictions and high non-citizen immigration), are matters of indifference. They have appalling distributional consequences, and prevent the housing supply market working remotely efficiently. But the banks aren’t the people to blame: that blame should be sheeted home, constantly, to the politicians responsible for the regulatory distortions. We get bigger banks as a result – more gross credit has to be distributed from one group in society to another – but if we are going to mess up the housing and land supply markets, bigger banks are almost an inevitable, perhaps even second-best desirable, outcome. The alternative would be whole new waves of disintermediation, and a housing stock ending up (even more) increasingly owned by those not dependent on debt.

The preferable path would be one in which land use restrictions were substantially removed, and house and urban land prices once again reflected market economic factors rather than regulatory impositions. That would be a path towards smaller banks – but just as in my chart above, the adjustment would take many years.