Graeme Wheeler’s OCR decision this morning – perhaps he will tell us how many of his advisers backed this one? – was the wrong decision. Core inflation measures remain well below the midpoint of the inflation target, and there are few or no pressures taking inflation sustainably back to the midpoint, even though it is now almost 11 months since the Reserve Bank began unwinding the ill-fated 2014 tightening cycle.

Keeping medium-term inflation near 2 per cent is the monetary policy job that has been given to the Governor. Nothing else matters very much in the Policy Targets Agreement. There has been talk in some quarters that the inflation target should be lowered. The Minister of Finance says he hasn’t found that case persuasive, and he sets the target.

But if it was the wrong decision, it perhaps wasn’t too surprising a decision. Graeme Wheeler has been reluctant to cut the OCR all along. He continues to talk of how “accommodative” monetary policy is, but that appears to be referenced against a view that the “neutral” interest rate is 4.5 per cent (their last published estimates, although one hears that they tell investors in private meetings that that estimate is now around 4 per cent – perhaps reflecting the fall in inflation expectations?). He thought he was getting things “finally” back to normal when he launched the 2014 tightening cycle, talking confidently then of the prospects of 200 basis points of tightening. It would be better, frankly, if the concept of a neutral interest rate was largely excised from central bankers’ vocabulary for the time being, because neither they nor we have any good sense of what “neutral” actually is. Any such estimates have too often been a dragging anchor, helping hold back central bankers from the sorts of policy adjustments that meeting their respective inflation targets would have warranted.

So the Governor has been consistently reluctant to cut the OCR – and even more reluctant to admit his past mistakes – and has only done so when the weight of evidence has overwhelmed his preferences. Last year it seemed to be some mix of further falls in dairy prices, the failure of inflation to recover, and/or high unemployment. As recently as the start of February, in his forthright speech, the Governor was again holding out against the prospect of further cuts – never ruling them out, but making pretty clear where his inclinations lay. But then the data overwhelmed him again. The new inflation expectations data shook the Bank, and the deteriorating global economic outlook and rising financial market unease (including widening credit spreads) prompted a move in March, with the prospect (projection) of one more cut to come before too long.

But in the past six weeks, there hasn’t been that much news, and little to change anyone’s baseline story. There hasn’t been any new labour market data, the CPI had something for everyone, there was no material new inflation expectations data, and if the global economic outlook still looks unpromising, financial markets have recovered somewhat (including credit spreads banks face) and oil and various hard commodity prices have been rising. If your reference point is that the OCR “really should” be something more like 4 per cent, why would you take the “risk” of cutting the OCR now? It might be different if your reference point was that core inflation measures have been persistently below target for years, and that that gap shows little or no signs of closing.

What of the housing market? I explicitly commended the Governor’s approach to house prices at the time of the March MPS: asked about the risks that a lower OCR could provide a big further impetus to house prices, he had simply observed “well, that’s just something we’ll have to keep an eye on”. It helped that, at the time, the Bank noted that house price pressures in Auckland had been “moderating”. Recall that house prices are explicitly not something the Reserve Bank has a mandate to use monetary policy to target.

Six weeks on and house price issues are all over the headlines again, given added impetus by the Prime Minister’s talk of land taxes for non-residents etc. The Bank’s tone has changed, although it is still somewhat cautious: “there are some indicators that house price inflation in Auckland may be picking up”. Frankly, it would be surprising if it were not – new distortionary policies introduced by the Bank and the government late last year should only ever have been expected to have had short-term effects. Nothing fundamental about the market has changed. It still isn’t the Bank’s responsibility at all, and certainly not something that should be driving monetary policy. But when all his inclinations seem to be against cutting, unless “forced” to by new data, and with a potentially awkward Financial Stability Report only a couple of weeks off, it would have been another reason to hold back.

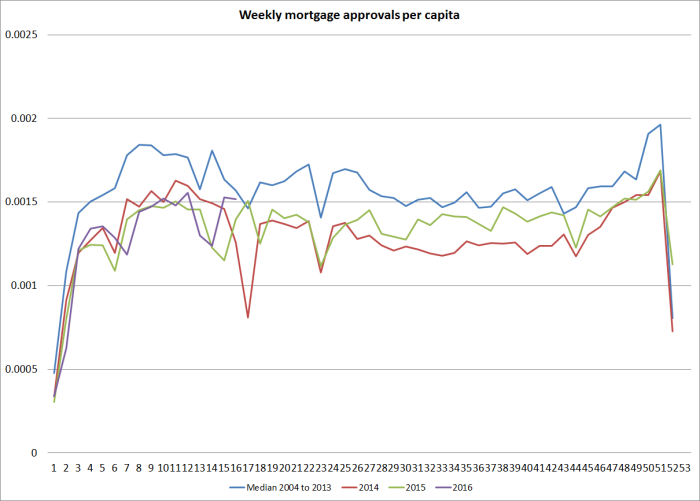

Are house prices really taking off? The Dominion-Post would have one think so, highlighting this morning a sharp rise in the price of a house in the sunny but unprepossessing suburb of Berhampore, perhaps a kilometre from where I sit. In terms of activity levels, I run this chart of the number of (per capita) mortgage approvals from time to time. There doesn’t seem anything extraordinary about current volumes of mortgage approvals (again, the x axis is weeks of the year, numbering 1 to 52/53).

Various people who talk to the Reserve Bank have been telling me since March that the Bank has finally “got it” and recognized that the overall domestic and economic climate is such that materially lower interest rates were needed. I wish it were so, but I think today’s statement confirms my “model”, in which the Bank will cut only reluctantly, and only if – in effect – “forced” to. The Governor just doesn’t seem worried about having the economy is a position where the best guess of next year’s inflation rate would in fact be 2 per cent. He seems content so long as (a) he can mount a semi-credible story that headline inflation gets back above 1 per cent before too long, and (b) so long as the measures of core inflation don’t consistently drop below 1 per cent. Otherwise, house prices seem to play too large a role in his “reaction function” – he can play them down and suggest they aren’t a consideration when they look a bit quiescent, but they act as quite a drag on good monetary policy at any other time.

I’m not overly keen on central banks reacting much to exchange rate movements in most circumstances. Often enough, the exchange rate changes reflect something “real” or fundamental going on. The Bank’s own research has suggested that falls in the exchange rate haven’t materially boosted overall inflation – probably for exactly that reason. But it is the Governor who keeps going on about the exchange rate and how uncomfortable or inappropriate or undesirable it is. And yet the one thing he can do that make a difference to the exchange rate is the stance of monetary policy. A lower OCR, all else equal, will tend to lower the exchange rate. As it, the Governor must have gone into this morning’s announcement knowing that it was almost certain that there would be quite a bounce in the exchange rate. Despite the absence of media lock-ups, there didn’t seem to be much uncertainty about the market reaction this morning.

Trade-weighted index measure of the exchange rate:

And so we are delivered an exchange rate a full per cent higher than the level the Governor considered inappropriately high at 8:59am. That seems unnecessary and unfortunate.

The disastrous New Zealand (especially Auckland) housing market is primarily the responsibility of elected central and local government politicians. It is not something to be controlled or moderated, except incidentally, by good monetary policy (to be aimed at stability in the general level of prices) or regulatory imposts on banks (supposed to be used only to promote the soundness and efficiency of the financial system. If the Reserve Bank thinks banks need more capital, let it make such a proposal, advance the evidence, and consult on it. If it thinks banks are making reckless lending choices, again let them lay out the evidence in the forthcoming FSR, and tell us about the conversations it is having with bankers, and any regulatory measures it is thinking about. But it simply is not a matter for monetary policy.

Looking ahead, there is not much key New Zealand macro data due before decisions are made on the June MPS. The quarterly labour market data are out shortly, but after the noise in the unemployment rate recently, it may be difficult to get much very new from that data yet. Perhaps as important might be the next Survey of Expectations, and particularly the inflation expectations results in it. Today’s statement is quite relaxed about inflation, and adamant that “long-term inflation expectations are well-anchored at 2 per cent” (not “seem to be”, not “close to”, but “are” and “at”).

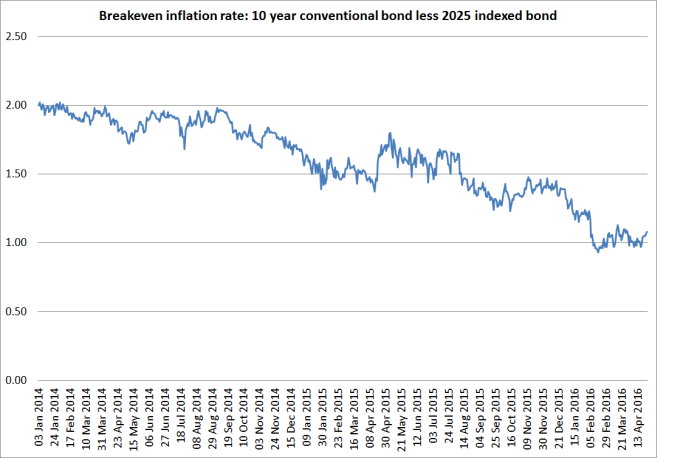

That certainly isn’t the message from financial markets. Yes, I know that the implied inflation expectations from indexed bonds aren’t a perfect indicator – then again, neither are the other measures of expectations or core inflation – but the current level, just above 1 per cent, seems pretty close to the average of the various core inflation measures the Reserve Bank highlighted in the last MPS. The central view just doesn’t seem to be that we can count on 2 per cent average inflation any time soon. That should be a mark against the Reserve Bank.

In closing, I should note a couple of small aspects of the Bank’s press release that I welcome. I (and no doubt others) had lamented the Governor’s recent high profile focus on a single, complex, prone to end-point issues, measure of core inflation. In this statement, that is replaced with a simple “core inflation remains within the target range”. Only just within, I would argue, but it is better than putting so much official weight on a single measure.

And in the final paragraph, I have noted for some time an unease at how much weight the Bank has been putting on recent and near-term headline inflation in these statements – in the near-term, headline inflation is thrown around by all sorts of things. This time, they have gravitated towards something more (PTA consistent) medium-term in focus: “we expect inflation to strengthen as the effects of low oil prices drop out and as capacity pressures gradually build”. One could reasonably question whether there is any sign that capacity pressures really are building, or are likely to over the next year or two – after all, they have been relying on this “gradual build” for some years now – but at least it puts the emphasis in the right place: the factors that shape the medium-term outlook for inflation.