Graeme Wheeler’s OCR decision this morning – perhaps he will tell us how many of his advisers backed this one? – was the wrong decision. Core inflation measures remain well below the midpoint of the inflation target, and there are few or no pressures taking inflation sustainably back to the midpoint, even though it is now almost 11 months since the Reserve Bank began unwinding the ill-fated 2014 tightening cycle.

Keeping medium-term inflation near 2 per cent is the monetary policy job that has been given to the Governor. Nothing else matters very much in the Policy Targets Agreement. There has been talk in some quarters that the inflation target should be lowered. The Minister of Finance says he hasn’t found that case persuasive, and he sets the target.

But if it was the wrong decision, it perhaps wasn’t too surprising a decision. Graeme Wheeler has been reluctant to cut the OCR all along. He continues to talk of how “accommodative” monetary policy is, but that appears to be referenced against a view that the “neutral” interest rate is 4.5 per cent (their last published estimates, although one hears that they tell investors in private meetings that that estimate is now around 4 per cent – perhaps reflecting the fall in inflation expectations?). He thought he was getting things “finally” back to normal when he launched the 2014 tightening cycle, talking confidently then of the prospects of 200 basis points of tightening. It would be better, frankly, if the concept of a neutral interest rate was largely excised from central bankers’ vocabulary for the time being, because neither they nor we have any good sense of what “neutral” actually is. Any such estimates have too often been a dragging anchor, helping hold back central bankers from the sorts of policy adjustments that meeting their respective inflation targets would have warranted.

So the Governor has been consistently reluctant to cut the OCR – and even more reluctant to admit his past mistakes – and has only done so when the weight of evidence has overwhelmed his preferences. Last year it seemed to be some mix of further falls in dairy prices, the failure of inflation to recover, and/or high unemployment. As recently as the start of February, in his forthright speech, the Governor was again holding out against the prospect of further cuts – never ruling them out, but making pretty clear where his inclinations lay. But then the data overwhelmed him again. The new inflation expectations data shook the Bank, and the deteriorating global economic outlook and rising financial market unease (including widening credit spreads) prompted a move in March, with the prospect (projection) of one more cut to come before too long.

But in the past six weeks, there hasn’t been that much news, and little to change anyone’s baseline story. There hasn’t been any new labour market data, the CPI had something for everyone, there was no material new inflation expectations data, and if the global economic outlook still looks unpromising, financial markets have recovered somewhat (including credit spreads banks face) and oil and various hard commodity prices have been rising. If your reference point is that the OCR “really should” be something more like 4 per cent, why would you take the “risk” of cutting the OCR now? It might be different if your reference point was that core inflation measures have been persistently below target for years, and that that gap shows little or no signs of closing.

What of the housing market? I explicitly commended the Governor’s approach to house prices at the time of the March MPS: asked about the risks that a lower OCR could provide a big further impetus to house prices, he had simply observed “well, that’s just something we’ll have to keep an eye on”. It helped that, at the time, the Bank noted that house price pressures in Auckland had been “moderating”. Recall that house prices are explicitly not something the Reserve Bank has a mandate to use monetary policy to target.

Six weeks on and house price issues are all over the headlines again, given added impetus by the Prime Minister’s talk of land taxes for non-residents etc. The Bank’s tone has changed, although it is still somewhat cautious: “there are some indicators that house price inflation in Auckland may be picking up”. Frankly, it would be surprising if it were not – new distortionary policies introduced by the Bank and the government late last year should only ever have been expected to have had short-term effects. Nothing fundamental about the market has changed. It still isn’t the Bank’s responsibility at all, and certainly not something that should be driving monetary policy. But when all his inclinations seem to be against cutting, unless “forced” to by new data, and with a potentially awkward Financial Stability Report only a couple of weeks off, it would have been another reason to hold back.

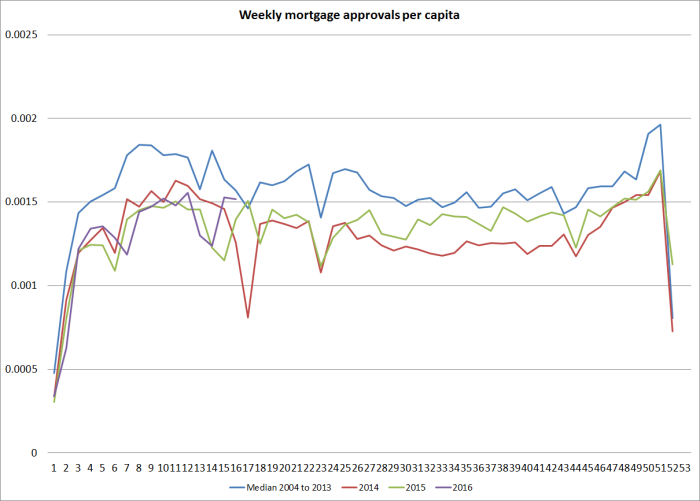

Are house prices really taking off? The Dominion-Post would have one think so, highlighting this morning a sharp rise in the price of a house in the sunny but unprepossessing suburb of Berhampore, perhaps a kilometre from where I sit. In terms of activity levels, I run this chart of the number of (per capita) mortgage approvals from time to time. There doesn’t seem anything extraordinary about current volumes of mortgage approvals (again, the x axis is weeks of the year, numbering 1 to 52/53).

Various people who talk to the Reserve Bank have been telling me since March that the Bank has finally “got it” and recognized that the overall domestic and economic climate is such that materially lower interest rates were needed. I wish it were so, but I think today’s statement confirms my “model”, in which the Bank will cut only reluctantly, and only if – in effect – “forced” to. The Governor just doesn’t seem worried about having the economy is a position where the best guess of next year’s inflation rate would in fact be 2 per cent. He seems content so long as (a) he can mount a semi-credible story that headline inflation gets back above 1 per cent before too long, and (b) so long as the measures of core inflation don’t consistently drop below 1 per cent. Otherwise, house prices seem to play too large a role in his “reaction function” – he can play them down and suggest they aren’t a consideration when they look a bit quiescent, but they act as quite a drag on good monetary policy at any other time.

I’m not overly keen on central banks reacting much to exchange rate movements in most circumstances. Often enough, the exchange rate changes reflect something “real” or fundamental going on. The Bank’s own research has suggested that falls in the exchange rate haven’t materially boosted overall inflation – probably for exactly that reason. But it is the Governor who keeps going on about the exchange rate and how uncomfortable or inappropriate or undesirable it is. And yet the one thing he can do that make a difference to the exchange rate is the stance of monetary policy. A lower OCR, all else equal, will tend to lower the exchange rate. As it, the Governor must have gone into this morning’s announcement knowing that it was almost certain that there would be quite a bounce in the exchange rate. Despite the absence of media lock-ups, there didn’t seem to be much uncertainty about the market reaction this morning.

Trade-weighted index measure of the exchange rate:

And so we are delivered an exchange rate a full per cent higher than the level the Governor considered inappropriately high at 8:59am. That seems unnecessary and unfortunate.

The disastrous New Zealand (especially Auckland) housing market is primarily the responsibility of elected central and local government politicians. It is not something to be controlled or moderated, except incidentally, by good monetary policy (to be aimed at stability in the general level of prices) or regulatory imposts on banks (supposed to be used only to promote the soundness and efficiency of the financial system. If the Reserve Bank thinks banks need more capital, let it make such a proposal, advance the evidence, and consult on it. If it thinks banks are making reckless lending choices, again let them lay out the evidence in the forthcoming FSR, and tell us about the conversations it is having with bankers, and any regulatory measures it is thinking about. But it simply is not a matter for monetary policy.

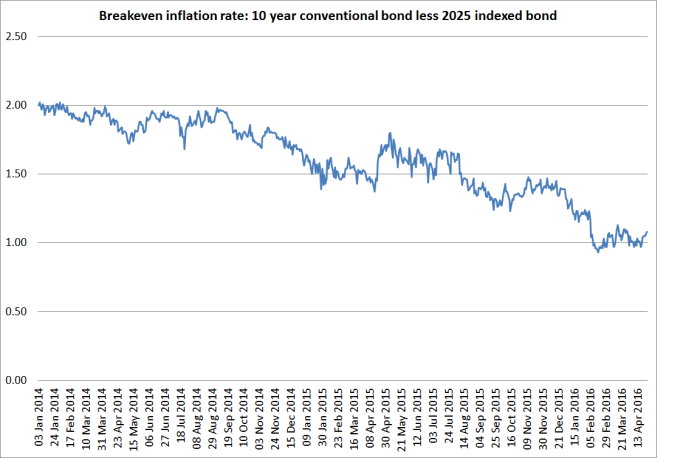

Looking ahead, there is not much key New Zealand macro data due before decisions are made on the June MPS. The quarterly labour market data are out shortly, but after the noise in the unemployment rate recently, it may be difficult to get much very new from that data yet. Perhaps as important might be the next Survey of Expectations, and particularly the inflation expectations results in it. Today’s statement is quite relaxed about inflation, and adamant that “long-term inflation expectations are well-anchored at 2 per cent” (not “seem to be”, not “close to”, but “are” and “at”).

That certainly isn’t the message from financial markets. Yes, I know that the implied inflation expectations from indexed bonds aren’t a perfect indicator – then again, neither are the other measures of expectations or core inflation – but the current level, just above 1 per cent, seems pretty close to the average of the various core inflation measures the Reserve Bank highlighted in the last MPS. The central view just doesn’t seem to be that we can count on 2 per cent average inflation any time soon. That should be a mark against the Reserve Bank.

In closing, I should note a couple of small aspects of the Bank’s press release that I welcome. I (and no doubt others) had lamented the Governor’s recent high profile focus on a single, complex, prone to end-point issues, measure of core inflation. In this statement, that is replaced with a simple “core inflation remains within the target range”. Only just within, I would argue, but it is better than putting so much official weight on a single measure.

And in the final paragraph, I have noted for some time an unease at how much weight the Bank has been putting on recent and near-term headline inflation in these statements – in the near-term, headline inflation is thrown around by all sorts of things. This time, they have gravitated towards something more (PTA consistent) medium-term in focus: “we expect inflation to strengthen as the effects of low oil prices drop out and as capacity pressures gradually build”. One could reasonably question whether there is any sign that capacity pressures really are building, or are likely to over the next year or two – after all, they have been relying on this “gradual build” for some years now – but at least it puts the emphasis in the right place: the factors that shape the medium-term outlook for inflation.

Changing the makeup of the CPI to include “housing costs” would very quickly see inflation at way above 2% and the governor could quickly increase the OCR to his “neutral 4.5%.

Then we could all sit back and watch the present systemically unstable debt-based monetary and banking system collapse as the housing bubble burst!

Then perhaps our “great leaders” would begin to learn about the systemically stable Sovereign Money banking and monetary system, in which banks are money lenders, not money creators.

In the present system, banks are money creators, not money lenders in the sense of being financial intermediaries. However, all of our schools, polytechnics and universities — and the text books they use — teach their economics students the nonsense that savings equal investments and that banks are financial intermediaries that earn an honest living from the margins between the interest rates that they pay savers and the interest rates that they charge borrowers.

LikeLike

I was in NZ in the 1990s when land prices were part of the CPI index. House price inflation was around 20%, inflation was around 20% and interest rates were around 20%. But yes my wages were also around 20% increments, well at least for me but I did hear of lots of folk that did not have 20% wage increases that were struggling. Businesses were certainly struggling with the weight of 20% interest rates and 20% wage expectations.

Housing materials cost is factored into the CPI index. It is actually now cheaper to import cement rather than to manufacture here in NZ. There is now a 30,000 ton plastic cement silo called the giant Auckland boob right on the harbour front filled with imported cement.

LikeLike

Banks create customers like any other business, they create lending agreements with borrowing customers like any other business creates a sale agreement with a buying customer. With $152 billion in savings from savers and only $163 billion of bank created lending where is this magical debt that is not supported by savings? This leaves only $11 billion shortfall easily funded by shareholders capital or retained earnings or Foreign savings.

http://www.rbnz.govt.nz/statistics/c22

LikeLike

getgreatstuff, has it occurred to you that bank lending, of money created out of nothing, creates deposits?

has it not occurred to you that the recipients of the proceeds from the sale of their houses deposit the just-created money in their bank accounts?

Maybe it’s now time for you to read the Bank of England papers to which I have previously referred you!

Michael, perhaps it’s time for you to intervene and teach getgreatstuff how the present banking and monetary system actually works ? He sure doesn’t want to learn from me!

LikeLike

getgreatstuff, here is an excerpt from the Bank of England paper “Money creation in the modern economy”:

“In the modern economy, most money takes the form of bank deposits. But how those bank deposits are created is often misunderstood: the principal way is through commercial banks making loans. Whenever a bank makes a loan, it simultaneously creates a matching deposit in the borrower’s bank account, thereby creating new money.

The reality of how money is created today differs from the description found in some economics textbooks:

• Rather than banks receiving deposits when households save and then lending them out, bank lending creates deposits.”

Do you think the authors — professional economists employed by the Bank of England — made this stuff up?

LikeLike

If house prices fall, lending assets is impaired. In order to prevent a run on depositors savings, ie a run on savings, OBR has been introduced by the RBNZ to freeze a banks operations.Accountants are then appointed to assess the balance sheet. No one contacts the Bank of England or economists. Accountants then decide to sell the bank as is, or sell assets ie sell loans to borrowers or give shavers a haircut to restore a banks balance sheet, ie to reduce liabilities ie to reduce savings. If banks freely create deposits and freely create debt you would not need to trigger OBR. when a bank becomes insolvent ie net asset position goes negative, the RBNZ does not call the Bank of England, they call accountants to sort out what to do. It boils down to selling performing assets, ie borrowers that still pay their mortgages or giving savers a haircut in order to restore a banks solvency. NO MAGICAL DEBT mate.

LikeLike

Getgreatstuff, please don’t assume that I do not understand exactly what the OBR is and what it was designed to do – i.e. steal money off bank depositors and gift it to banks in trouble.

None of what you have written refutes the facts that:

1. Banks are not financial intermediaries, they are MONEY CREATORS.

2. EVERY TIME A BANK GRANTS A LOAN IT CREATES EX NIHILO A MATCHING DEPOSIT.

3. In New Zealand, approximately 98% of the money supply is bank deposits that were created ex nihilo by banks when they granted loans.

4. When a bank loan principal is repaid, the money disappears back into the nothing from whence it came.

As a consequence, economic growth is dependent upon increasing private debt.

As Mark Twain so famously observed:

1. It ain’t what you don’t know that gets you into trouble.

It’s what you know for sure that just ain’t so.

2. Sometimes I wonder whether the world is being run by smart people who are putting us on,

or by imbeciles who really mean it.

The Nobel prize-winning chemist turned monetary reformer Frederick Soddy, in his book ‘The Rôle of Money’, published in 1934, wrote:

“A very slight knowledge of our actual existing monetary system makes it abundantly clear that, without democracy knowing or allowing it, and without the matter ever being before the electorate even as a secondary or minor political issue, the power of uttering money has been taken out of national hands and usurped as a perquisite by the moneylender. Practically every genuine monetary reformer is unanimous that the only hope of safety and peace lies in the nation instantly resuming its prerogative over the issue of all forms of money, which, legally, it has never surrendered at all.”

US President Andrew Jackson, speaking in 1836, said “If the people only understood the rank injustice of our money and banking system, there would be a revolution before morning.”

LikeLike

Reluctant as I usually am to intervene in the debates between you two, can I just say that I agree totally with PJM’s 1 to 4 above on the mechanism, but depart (fundamentally) when you get to the “as a consequence”. Economic growth depends on innovation, markets, and the energy and drive of individual firms and products.

Poor credit decisions, on a large enough scale, can wreak havoc. But they toss the economy around, rather than determining its longer-run trend.

LikeLike

That is why when a bank gets into trouble you call an accountant and not an economist. Accountants deal with facts rather than DISH OUT THEORY without understanding the full picture that it is a zero sum game. I have already said time and time again banks do create debt in the same way that a business creates sales BUT there inadvertently is a balancing act between savings and loans. That is why it is called bank stability ie has the loans got ahead of the savings, has the loans got ahead of Housing value that can cause impairment. Is there too much savings that impair a banks profitability and solvency? Is there enough capital to cover in case?

LikeLike

When a entrepreneur like Grammer Hart goes to a bank and asks for $2 billion to acquire a company. The bank will ask of their funding parties whether they have enough savings, whether they have enough capital or whether they can source overseas savers or pursuade savers to purchase specified bonds or borrow from other banks in order to do that deal. Inevitably a sum of borrowing of that size, one bank will say no because they would not be able to balance all the savings, all the capital available by their shareholders and all their access to alternative funding sources. It ends up being a consortium of banks that would raise the $2 billion so that Graeme Hart can go out there and buy a company like Carter Holt Harvey. If debt was magically created, all it takes is one bank to raise the debt with an easy flick of a computer screen and magically raise the debt but NO!. In real life it requires a consortium of banks and a huge amount of negotiation and risk assessment and funding lines either from savers local, overseas or funded by bonds which still requires savers to purchase those bonds.

LikeLike

Thanks, Michael. I was hoping that you would intervene! You are, of course, correct in disagreeing with me. I apologise – I wrote in too much haste, and was imprecise! I should have said that increasing the money supply, which is mostly, but not exclusively, a precursor to economic growth, depends on increasing a combination of private debt and public debt. IMHO, that is one of the major, if not the major, reasons for most countries’ extremely slow recovery from the GFC.

LikeLike

And I should have added, that economic growth also largely depends on that increase in debt, that equates to an increase in the money supply, being spent on creating productive assets rather than on buying existing assets such as houses!

It’s setting the economic conditions for creating productive assets that is one of the most important the tasks of Bill English and also Graeme Wheeler. Given the way that the present monetary and banking system works, that is a daunting task indeed!

The section of the RBNZ’s website headed “About Us” begins with:

“The Reserve Bank of New Zealand is New Zealand’s central bank. We promote a sound and dynamic monetary and financial system. We work towards our vision by

• Operating monetary policy to achieve and maintain price stability

• Assisting the functioning of a sound and efficient financial system

• Meeting the currency needs of the public

• Overseeing and operating effective payments systems

• Providing effective support services to the Bank”

Hence my questions to the governor of the RBNZ:

1. What research have your people at the RBNZ done to be able to assure the people of New Zealand that the financial system is as sound and efficient as it is possible to be?

2. Have your people investigated the viable alternative system that is a Sovereign Money system, in which ALL of the new (electronic) money with which “we the people” increase our economic activity would be created interest-free and debt-free by the RBNZ on our behalf, and gifted to the government for spending directly into the economy according to its democratic mandate?

LikeLike

The Japanese did that in WW2, it’s called banana cash.

LikeLike

Just to be slightly picky (with RB in respect of that list, as much as with you), the Bank is not charged with ensuring that “the financial system is as sound and efficient as it is possible to be”. It has a narrower responsibility, to use it specific regulatory powers to promote the soundness and efficiency of the financial system. In other words, those considerations constrain how they can use their powers (potential opening actions up to judicial review), it isn’t an independent obligation, and certainly isn’t a maximal obligation to make the system as sound and as efficient as it is possible to be. For example, the Bank regularly reminds us that it does not run prudential policy with a view to preventing all bank failures.

LikeLike

Ha!

Berhampore unprepossessing!

Spoken like a true Island Bay resident… 🙂

Nice piece.

Wheeler all over the show again. Those comments about long term expectations being anchored at 2% while short term expectations are declining would suggest there’s long term issue brewing that is not being addressed.

cheers

Bernard Hickey Publisher – Hive News Work: 04 817 9594 Mobile: 027 866 0011 Home: 04 389 7972

http://www.hivenews.co.nz

Sample our daily email https://www.hivenews.co.nz/email_preview

twitter.com/@bernardchickey

http://www.celebspeakers.com/speaker/bernard-hickey

Mail: Hive News, Press Gallery, Parliamentary Buildings, Wellington, 6011.

Also contributing to Banking Day, Herald on Sunday, Interest.co.nz, Radio Live and Economist Intelligence Unit.

On Thu, Apr 28, 2016 at 2:22 PM, croaking cassandra wrote:

> Michael Reddell posted: “Graeme Wheeler’s OCR decision this morning – > perhaps he will tell us how many of his advisers backed this one? – was the > wrong decision. Core inflation measures remain well below the midpoint of > the inflation target, and there are few or no pressures ta” >

LikeLiked by 1 person

Could have said worse…..but then it does have an excellent bakery, something I Bay doesn’t

LikeLike

The longer term issue at the moment is not Auckland Property prices. Auckland property prices is driven by the incoming Unitary Plan. Auckland property prices have diverged from the rest of the country because Auckland property will allow for future multiple rental incomes. It is called the Xero effect where a company which makes no profits and with a tiny $120 million sales turnover is worth $2.2 billion in anticipation of future revenues and future profitabllity.

The longer term effect of keeping interest rates higher than our major trading partners does make our companies and businesses uncompetitive against the global competition but it does encourage higher savings which is currently at record levels and rising faster than our debt. This will put banks margins under increasing pressure as interest payable on savings is a cost to banks. We are already seeing our banks profits coming under increasing pressure.

Banks will be under pressure to lend to maintain their record profits which means they would take higher lending risks to other sectors eg small businesses/our Gisborne space industry etc since there is a LVR restriction in place that blocks banks from going low documentation and high LVR loans on property that took place in 2002 to 2007. When Allan Bollard increased interest rates, the critical error he made was that savings started climbing which forced banks to lend out even more as savings rose from the increasing interest rate, in effect he drove up the risks of bank instability as interest rates rose.

You cannot directly slow a property market down from higher interest rates because NZ savings is finely balanced with the debt contrary to what economists believe. It is from the decimation of jobs and the economy that is directly impacted by interest rates. The slowing of property prices in NZ comes from job losses and the decimation of the NZ economy.

LikeLike

That FX chart says it all, for me.

LikeLike

I’ve been reflecting on the last few MPSs and OCR decisions and it just feels like there is something in the decision making framework which is not being articulated. Michael you seem to be assuming that that thing is some combination of hubris and a concern about house price inflation. Is there any merit to the arguments which come out from time to time that NZ ‘needs’ interest rates at relatively high levels due to our reliance on overseas funding?

LikeLike

GT

I don’t think so, and devoted a whole conference paper (and a specific appendix on the overseas funding story) to the general issue of our interest rates.

http://www.rbnz.govt.nz/-/media/ReserveBank/Files/Publications/Seminars%20and%20workshops/Mar2013/5200823.pdf?la=en

The key strand in the counterargument is simple tho: countries that are having to pay a premium to reassure worried foreign investors tend to have low exchange rates, not high ones. Our real exchange rate has averaged persistently high for a long time, despite our relative economic decline.

Mostly, we need higher interest rates in NZ than abroad because we have more demand pressures than in other countries (my specific version of the story says got of demand from a rapidly rising population and a fairly modest savings rate). But over the last couple of years, that general story has been exacerbated by what looks like a series of Rb misjudgements and biases that have resulted in the OCR being held higher than even domestic economic circumstances have warranted. Fix that – which in my view might require perhaps another 75bps of cuts – and we would still have interest rates higher than those in almost all other advanced countries. We’d probably be similar to Australia in nominal terms, but they have a higher inflation target than we do, so our real interest rates would still be higher even than them.

LikeLike

I think OCR at 2.25% is neutral. GDP is growing at 2% to 3% which is good. The building industry is taking off and doing what it should be doing and that is to build more houses. Tourism is at record levels at 3.2 million visitors and contributing $11 billion to GDP with a 31% increase in tourist spending and a increase of 300k people requiring accomodation in NZ. International students number 110,000 of which 90,000 reside in Auckland and the numbers are growing with the education institutions spending $2 billion on student lecture halls, accomodation, cafeterias, half of Newmarket. International students contribute $2.85 billion to the NZ economy and growing in numbers and putting pressure on housing accomodation and on the NZD.

Immigration as an issue is a red herring as it is largely a replacement policy. Sure NZ population is 25% born overseas ie around 1 million but they in effect replace the 1 million New Zealanders that bugger off overseas anyway.

AS NZ households have $152 billion in cash deposit savings in banks and $52 billion in investment share funds with only around $163 billion in debt(including Credit card and student loan debt),

NZ household savings is much higher than NZ household debt.. http://www.rbnz.govt.nz/statistics/c22

Interest rates either higher or lower has very little impact on NZ household spending overall.

Wheeler is correct to do nothing at this time. Except for going bonkers in 2014 with 4 aggressive interest rate increases, Wheelers approach is a lot better than Allan Bollard who went crazy with Interest rates hikes reaching for an impossible 10%, wiping out the building industry off the face of NZ and wiping $6 billion of investor funds in Finance companies collapses that were funding the building sector.

LikeLike