I wrote about Kiwibank last week, noting that there had never been a good economic reason for the Crown to have established it, and that there was not a good economic reason for the Crown to continue to own it. Doing so undermines (modestly) the efficiency of the financial system, and poses unnecessary risks for taxpayers.

I take it that the Minister of Finance agrees. Listening to him on Morning Report, unable to give any reason why the government should own a bank other than “it is government policy that we do so”, one almost felt a little sorry for him. Then again, he is the Deputy Prime Minister.

What to make of yesterday’s announcement from New Zealand Post? The plan is that NZ Post will sell 45 per cent of its stake in Kiwi Group Holdings (KGH) to ACC (20 per cent) and the New Zealand Superannuation Fund (25 per cent), at a price which values KGH at $1.1 billion.

In some ways, the price tells us what we need to know about Kiwibank. The book value of shareholders’ equity in KGH as at 31 December 2015 was $1.304 billion, and yet the sale is going to go through at the equivalent of $1.1 billion (or perhaps lower if due diligence shows up some problems). That is around 85 per cent of book value.

When I checked yesterday, the four Australian banks appeared to be trading on the stock exchange at anything from 1.2 to 2.1 times book value. And the Reserve Bank of Australia ran this nice chart in their last Financial Stability Review

Note where the Australian and Canadian banks have been trading. By contrast, banks in much of the rest of the world, where there have been real doubts about asset quality or earnings potential have been trading at or below book value since the 2008/09 recession.

The deal also values KGH at eight times last year’s earnings ($137 million). A quick check suggests that five listed Australian banks (the four operating here and the Bank of Queensland) are trading, on average, at prices around 11.5 times last year’s earnings.

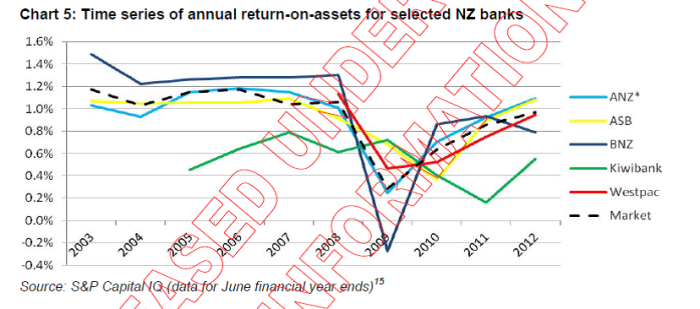

Kiwibank just isn’t a very profitable bank. Last week I showed this slightly-dated Treasury chart:

But, of course, there are other reasons for a fairly low price:

- Given the government’s determination not to privatize Kiwibank (even partially), there were no other possible takers. ACC and NZSF no doubt knew that.

- ACC and NZSF will, apparently, be locked in for the first five years (beyond the next two elections), unable to sell out, and yet without effective control (individually or jointly). Some finance guru could no doubt value that (loss of) option, but I wouldn’t have thought it would be a trivial amount.

As Michael Cullen noted yesterday, if there had been a sale into private ownership it would have “almost certainly led to a higher price” for NZ Post.

At one level, the price of the transaction does not matter unduly, as all the buyers and sellers are ultimately owned by the New Zealand government. In fact, the price should probably be the least of the worries.

The cleaner alternative approach to deal with Kiwibank (KGH) would have been for the government itself to have simply purchased KGH from NZ Post, and established KGH as a proper SOE, subject to proper SOE monitoring and accountability arrangements. In the short-term, it would have made little or no difference to Kiwibank which option was chosen. And it would have had the advantage of totally and immediately separating NZ Post and Kiwibank, enabling the directors and managers of NZ Post to focus solely on their troubled business. But, of course, doing so would have involved immediate Crown cash outlays (to NZ Post, even if much of it came back shortly thereafter as a special dividend), while yesterday’s clever wheeze involves cash flowing into the Crown accounts (from those other government entities, ACC and NZSF) via the special dividend NZ Post will pay. The cash flows don’t change the economic value to the overall Crown balance sheet.

Although the deal has been presented as making it easier for the owners to provide any future capital injections to Kiwibank that might be thought warranted (beyond what retained earnings – the way most banks grow – would allow), that isn’t an argument for the particular form of yesterday’s deal, as opposed to simply taking KGH directly into Crown ownership as an SOE. After all, central government has considerably deeper pockets than either ACC or the NZSF. At least on the basis of last year’s Annual Report, the proposed KGH investment (at $210m) will already be ACC’s largest single equity investment.

It would also appear to be the largest equity holding for NZSF. These don’t seem like organisations with sufficiently deep pockets that they would (or should anyway) be wanting much more exposure to a single entity, a minor (not overly financially successful) player in its own sector, than they will already have if this deal is completed.

I’m extremely wary of the state owning a bank, but if we are going to own it, I’d rather the question of any additional capital was being decided by the elected representatives of the owners, who we can kick out.

The deal has been presented by NZ Post as offering benefits to Kiwibank through the “long-term investment horizons” and “expertise” of ACC and NZSF investment managers. For better or worse, the central government has actually tended to have a longer-term investment horizon than either institution (NZ Post in its current form was set up almost thirty years ago, the predecessor Post Office based bank ran under central government for well over 100 years). And as for investment expertise, well, yes no doubt. But Kiwibank is a retail bank, and neither ACC nor NZSF has any particular expertise in retail banking – and nor would one expect, or want, them to (after all, as NZSF’s head of investment’s noted in last year’s Annual Report, NZSF is statutorily prohibited from having control of operational businesses). Both ACC and NZSF are funds managers. They seem to do that job moderately well (I’m much more skeptical of NZSF, but that is a topic for another day), through some mix of strategic asset allocation and tactical stock selection, but that isn’t the sort of expertise that helps generate a strong profitable retail bank.

Curiously, the sorts of expertise ACC or NZSF might have already seem rather well represented on the Kiwibank board, not one of whom has retail banking experience or apparent expertise. Perhaps the Board will change under the new ownership, but why should we suppose that government funds such as ACC or NZSF will be better able to nominate suitable directors than NZ Post was (and in any case, for now NZ Post will retain the majority shareholding).

The paper-shuffling doesn’t have the feel of a long-term arrangement. ACC, in particular, seems unlikely to be a natural holder of a 20 per cent stake in any company, and NZSF probably shouldn’t be. A constant risk around NZSF has been that it would be used for political purposes: a large pool of money just waiting for people with “good ideas” – and a major ownership stake in a politically totemic, modestly performing, bank is just an example of that sort of risk.

And so this deal has the feel of short-term opportunism. Immediate cash inflows for the government rather than immediate cash outflows (with no difference in economic value between the two), and a way of making it perhaps just a little easier to privatize the bank if political conditions were to change. No doubt for now, if ACC and NZSF wanted out, the Crown would repurchase the shares. But if the political winds change a little, then, for example, the five year minimum holding periods could be waived if it suited the Crown to do so, and it might be rather easier for NZSF and ACC to dribble their shares out into private institutional hands gradually, at one remove from the decisions of politicians, than for politicians to choose a trade sale, or even a modest IPO.

I favour privatization, but also favour good government, and clear transparent lines of accountability. This deal doesn’t look the way we should be running things. We have a fairly good framework for Crown-owned operating businesses, the State-Owned Enterprises Act. It should be used for Kiwibank (and KGH) and when the time comes the debate around privatization, partial or full, should be had directly and openly, between politicians, and citizens (as was done with the power companies, and all past privatisations), not by reshuffling holdings of major Crown assets into arms-lengths agencies that can offer little or nothing new to Kiwibank, and face neither market discipline, or effective public accountability themselves (indeed, in the case of NZSF, that lack of effective political accountability was the whole point of the governance structure).

Having said that the SOE Act has been a pretty good framework over 30 years for governing Crown-owned operating businesses, I was somewhat disconcerted to note yesterday how politicized the NZ Post press statement was. The statement from Bill English and Todd McLay headed “Kiwibank to remain 100 per cent Govt owned” was fairly factual and descriptive in nature. Michael Cullen’s statement, by contrast, was considerably more rhetorical: “Stronger circle of Crown owners proposed for Kiwibank”, “these two Crown investors – both essential parts of the New Zealand fabric”, “time to broaden the bank’s support base within the wider public sector”, “a rare opportunity”. (Mind you, where the NZ Post statement really overstepped the mark for me was when they compared assets under management at ACC ($32bn) and NZSF ($28bn) with the sum of assets and liabilities of Kiwibank ($38 billion). I’ve never heard anyone previously refer to the size of a bank by adding together than assets and liabilities.)

Overall, it seems like an unstable model (perhaps deliberately so). We have a small underperforming bank that will be owned by three government owners, instead of one, none with any great expertise in the business the bank is actually undertaking. One will still have effective control, but less so than previously. And if things go wrong, no one of the direct shareholding parties will be able to call the shots to sort things out, and the risks are likely to fall back on central government anyway.

UPDATE: My unease has just been increased reading these comments from Bill English on the ending of the NZ Post guarantee.

“It wasn’t really an effective guarantee, but now that’s been replaced by an arrangement where the Government underwrites any capital requirements related to the bank coming under pressure,” he said.

“That’s yet to be finalised in detail, but there’ll be a capital facility there so that depositors know that if anything went wrong with Kiwibank then the Government is able to stand behind it,” he said.

“It’s a capital facility. It’s not like a deposit guarantee because in New Zealand we don’t have deposit guarantees, but it is a facility that Kiwibank can call on if in extreme circumstances it needed to repair its capitalisation,” he said.

Perhaps it just makes explicit the reality, and we will need to see the details (will this facility be priced?). Better to have a properly priced deposit insurance scheme across the entire system, and get the state out of owning – or underwriting the equity of – banks.