Charles I was a good man, but (was generally reckoned) a bad king. His reign ended. following the Civil War, with his beheading on 30 January 1649.

In their amusing take on English history 1066 And All That, Sellar and Yeatman offer this caricature of Charles’s views:

Charles explained that there was a doctrine called the Divine Right of Kings, which said that:

(a) He was King, and that was right.

(b) Kings were divine, and that was right.

(c) Kings were right, and that was right.

(d) Everything was all right.

Sometimes I wonder if Graeme Wheeler sees himself, and the Reserve Bank, in much the same light.

I wrote the other day about my request to the Reserve Bank to provide summary information on the OCR recommendations made by the Governor’s designated advisers for each of the OCR reviews since mid 2013. The Governor himself had disclosed that information for the March Monetary Policy Statement review in an interview conducted only a day or two after the release of that particular OCR decision.

As I noted the other day, I didn’t expect them to respond positively to my request.

I finally got the response late yesterday afternoon, just before the end of the maximum allowed time of 20 working days. I wasn’t surprised by the decision to withhold all the information, but was more than a little surprised at the argument they sought to rely on. Here is what they had to say:

Decision

The Reserve Bank is withholding the information under the grounds provided by section 9(2)(d) of the OIA, to protect the substantial economic interests of New Zealand.

Reasons

Official Cash Rate (OCR) decisions clearly relate to the substantial economic interests of New Zealand and it is clearly in the public interest that the Governor is able to decide the OCR as the Reserve Bank of New Zealand Act intends and requires.

The Governor has a statutory position as the sole decision-maker on the OCR. While the Governor chooses to take advice from the Monetary Policy Committee (MPC) and others prior to making decisions, the advice does not bind or compel the Governor to any particular decision. MPC policy recommendations are simply advice that the Governor is free to accept or not. What matters under the law is the Governor’s decision.

Given the Governor’s sole responsibility for determining monetary policy settings and the limited objective value of the information, the Bank considers the public interest in knowing this selective aspect of the advice of the MPC is not strong.

Moreover, there are serious risks that mis-informed commentary on this partial aspect of advice could detract from the Governor’s ability to implement monetary policy. This could adversely impact on the effectiveness of monetary policy, likely damaging the substantial economic interests of New Zealand.

As noted in responses to two previous OIAs requests from you (24 and 25 September 2015), the underlying analysis and advice for OCR decisions are published in summary form in a programme of carefully drafted media statements, Monetary Policy Statements, news media press conferences and media interviews. The Bank considers that the public interest in understanding OCR decisions made by the Governor is sufficiently met by these existing information disclosures.

The Governor may choose, on occasion, to publicly state that his decision on monetary policy settings accords with the views of the MPC or anyone else that he receives advice from or wants to refer to.

For those not familiar with the details of the Official Information Act, the relevant provision allows for information to be withheld if to do so is

“necessary [emphasis added] to avoid prejudice to the substantial economic interests of New Zealand”

“unless in the circumstances of the particular case, the withholding of that information is outweighed by other considerations which render it desirable, in the public interest, to make that information available”

The operative word there is “necessary”. There being some remote possibility that some harm could be done is not sufficient. Nor is a higher likelihood that some minimal inconvenience or discomfort to officials might ensue. No, it must be ‘necessary” to withhold that specific information to avoid prejudicing the substantial economic interests of New Zealand. And even then the wider public interest needs to be considered, in the context of an Act designed to make information available to public, to assist public understanding and to strengthen the accountability of ministers, officials, and official agencies.

The Governor’s case is already severely undermined by the fact that he chose to disclose this information, about the most recent OCR decision. Could he be sure that that information would not be misinterpreted, and lead to commentary that might make his life difficult? But he took the (surely very modest) risk anyway, and made the information available, presumably concluding that there was no material risk of prejudice to the substantial economic interests of New Zealand.

But then how can he seriously argue that the release of the same information for, say, the July 2013 OCR review has such serious risks that it is “necessary” to withhold it to avoid prejudicing those “substantial economic interests of New Zealand”? Or the July 2014 review? Or the July 2015 review – now eight months in the past. There is no sign in the Bank’s response that they have considered each piece of information separately, and evaluated the risks (which might well be different for information six weeks old than for information almost three years old). That sort of blanket refusal is inconsistent with the Act.

The substance of the Governor’s claim is that there are

serious risks that mis-informed commentary on this partial aspect of advice could detract from the Governor’s ability to implement monetary policy. This could adversely impact on the effectiveness of monetary policy, likely damaging the substantial economic interests of New Zealand.

Quite how a summary of the non-binding opinions of his own chosen advisers, relating to events already some time in the past, could detract from the Governor’s ability to implement monetary policy is really beyond me. Ultimately, the Governor makes the OCR decisions, and communicates his final stance by both the announced OCR itself and his press statement around it. It is entirely lawful, and reasonable, for the Governor to adopt an OCR that a minority or even, on rare occasion, a majority of his advisers disagree with. He is appointed Governor, and he signed the PTA, not them.

Of course, markets and commentators might be interested in which way the balance of advice went but this is lagged information (the most recent event I requested information for was the January OCR review, and my request was lodged after the next OCR decision was already known). If I had asked for named views of each individual adviser it might perhaps have been a little different – people could have fun with evidence that, say, the Deputy Governors disagreed with the Governor. But (a) that isn’t the information I asked for, and (b) in other countries, evidence of such a range of views within a central bank doesn’t seem to impair the ability of the central bank concerned to conduct monetary policy effectively. On several occasions, the former Governor of the Bank of England chose to be in a minority in the vote of the binding MPC, again without impairing either confidence in the individual or the effectiveness of UK monetary policy.

Frankly, the suggestion that the effectiveness of monetary policy could be thus impaired, particularly to extent that could “prejudice the substantial economic interests of New Zealand”, is preposterous.

I’ve highlighted previously the contrast between the pro-active approach adopted by the Minister of Finance and Treasury to the release of advice and papers relating to each year’s government Budget. The Minister of Finance is, in this context, the sole decision-maker, and the Treasury are the advisers to the Minister. The Treasury provides analysis, and advice, and recommendations. Sometimes those views are accepted by Ministers, sometimes regretfully not accepted, and sometimes just dismissed out of hand. That is the nature of good advice, in a world characterized by uncertainty and a range of perspectives on any one issue.

And yet most of that advice is routinely published. Occasionally perhaps it embarrasses either Treasury or the Minister (but embarrassment isn’t grounds for withholding) but no one questions the ability of the Minister to make fiscal policy decisions effectively. It isn’t impaired by knowing that at times the advisers – and that is all they are – disagree with the decisionmaker. What makes monetary policy different?

At times, commentary on official agencies and officials will be annoying, uncomfortable, perhaps lightweight, and perhaps even (the Bank’s concern) “misinformed”. Democracy is messy. We leave the alternative approach to places like Singapore. (And, of course, the usual remedy when there is “misinformation” or misinterpretation abroad, is to make more information available.)

In the end much of this comes down to what I wrote about the other day. The Bank has long considered that the final products that it chooses to publish should be enough – whether for financial markets, the public, or members of Parliament. The only people they are comfortable with providing more information to, apparently, are the members of the Reserve Bank Board. It was the mindset that used to prevail across the whole public sector, here and abroad.

But that isn’t law in New Zealand. Of course it would be tidier for official agencies and Ministers if only the approved “carefully drafted” final documents were ever made public – press releases, Budget speeches, Monetary Policy Statements and so on. But the Official Information Act was not passed in the interests of tidiness, or the convenience of powerful institutions and individuals. It was – and is – about allowing greater light to be shed on government processes, and the background analysis and advice that underpins decisions. That is what an open society is about. It is a big part of how we hold the powerful to account. As the Reserve Bank well knows, much though it may not like, it, the Official Information Act covers drafts as well as final documents – it might be interesting for someone, say, to ask for the various drafts of a particular OCR press release (perhaps one from a few quarters ago, the disclosure of which could not possibly impair current monetary policy).

I experienced this line of argument repeatedly in my time in the Bank. The Bank tends to operate as if it is a world apart. Many of its people think of the Bank – subconsciously I’m sure – more as one of international circle of likeminded central banks, interacting mostly with banks and financial markets, rather than as agency of executive government in New Zealand, accountable to the public (including through the Official Information Act) just as other agencies are.

And I’ve experienced this line repeatedly in responses to OIA requests over the last year or so. Of those relevant to monetary policy:

- after some months’ delay, the Bank grudgingly agreed to release the background papers to a Monetary Policy Statement from 10 years previously. On that occasion I did not ask for either copies of the individual OCR advice, or the summary of the recommendations.

- they subsequently refused to release any of the papers provided to the Bank’s Board regarding the September 2015 MPS

- the Bank refused to release any material background information relevant to the most recent Policy Targets Agreement.

- the Bank refused to release any minutes of meetings of its Governing Committtee (the forum in which the Governor takes the final OCR decision)

- the Bank refused for months to release any material information about the work they had been doing on governance reform, belatedly releasing a small amount only recently, claiming as warrant for doing so an Associate Minister’s answer to an Opposition MP’s supplementary question six months earlier.

- the Bank has refused to release any of the background information on its analysis of the economic impact of immigration that led into its material change of view at the December MPS. (this is a good illustration of all that is wrong with the Bank’s argument that the MPS is really quite enough for us mere mortals – since they included no supporting analysis in that MPS to justify their change of view).

Sadly, this latest response is all too typical, even if the particular excuse they must have spent a month crafting has a degree of novelty. It speaks of an organization – and the key individuals – who believe that they are, or should be, above the messiness of the sort of real world scrutiny that we expect in a democracy, and for which the Official Information Act provides. Hence, the Charles I references.

It is a shame, because I really can’t imagine what they have to hide. It shouldn’t be surprise if from time to time advisers disagree with the Governor – it should worry us much more if they never do. From time to time a Governor has gone against the majority view of his advisers – hindsight suggests that sometimes he was right to do so, and on other occasions probably not. But we should be able to see the balance of that advice, perhaps with a modest lag. Sometimes it will suit the Governor (as presumably in March, when he unilaterally released the information) and sometimes not. But what suits the Governor on particular occasions is not a relevant consideration under the Act.

The Reserve Bank of New Zealand was once at the forefront of greater openness and transparency among central banks. Sadly, that is no longer true.

I have appealed this decision to the Ombudsman, on two grounds:

- first, taking 20 working days to issue a blanket refusal (on material that involvement no substantial compilation or review effort) is simply inconsistent with the statutory responsibility to respond “as soon as reasonably practicable”, and

- second, that it is simply not credible that withholding all this information (including that about decisions in 2013) is “necessary” to avoid prejudice to the substantial economic interests of New Zealand.

Hamish Rutherford has covered the story here.

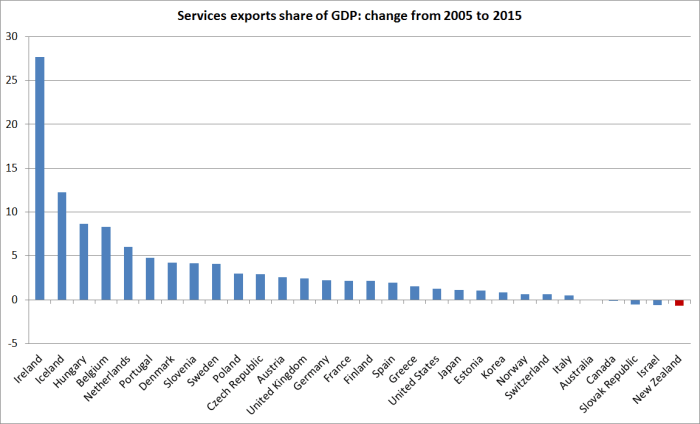

Large countries don’t tend to do as much international trade as small countries – they don’t need to, there are plenty of opportunities and markets at home. I’ve highlighted the large countries (more than 40m people) in green, and the small countries (under 11m, where there is a natural break) in red. New Zealand has the lowest services export share of any of the small countries (and, by the look of it, the lowest real dollar value of services exports as well) . Of course, we are much more remote than the other small countries, but it just highlights the difficulty of generating really high incomes for lots of people in a place so distant.

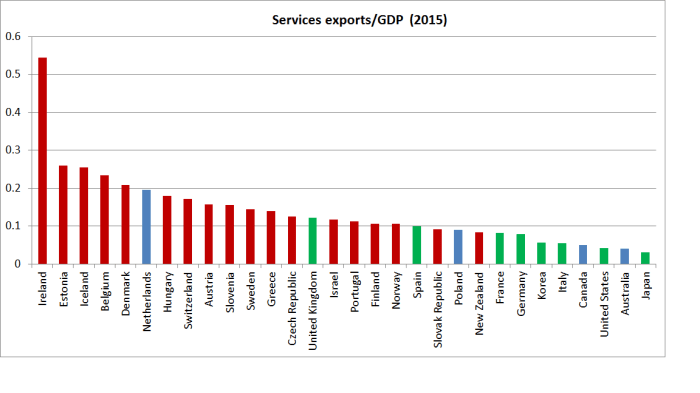

Large countries don’t tend to do as much international trade as small countries – they don’t need to, there are plenty of opportunities and markets at home. I’ve highlighted the large countries (more than 40m people) in green, and the small countries (under 11m, where there is a natural break) in red. New Zealand has the lowest services export share of any of the small countries (and, by the look of it, the lowest real dollar value of services exports as well) . Of course, we are much more remote than the other small countries, but it just highlights the difficulty of generating really high incomes for lots of people in a place so distant.