The Reserve Bank announced last month its decision to require banks to classify all loans secured on residential investment properties separately from other residential mortgage loans. This applies not just to large commercial operators, but to borrowers with just a handful of investment properties. The Reserve Bank will now require banks to use higher risk weights (ie have more capital) in respect of the former than in respect of the latter.

This has been quite a saga. The Bank went through a couple of rounds of consultation on earlier proposals last year (then focused on larger operators), and then came back earlier this year with a revised proposal. I made a brief submission on that consultative document, as no doubt did a variety of other people (although we don’t know who, as the Reserve Bank – unlike parliamentary select committees – does not routinely publish the submissions it received). The Reserve Bank’s summary response to the submissions can be found half way down the page here (various specific links on the RB website don’t appear to be working today),

The proposal that the Reserve Bank consulted on in March/April, and which it recently adopted, had a strong feel of being reverse-engineered. The Governor had apparently decided that he wanted to be able to impose additional direct controls on lending for residential property investment, and to do that he needed banks to have systems in place which would clearly delineate between investment property loans and owner-occupied loans. To support that prior policy conclusion, the Bank has sought to argue that loans on residential investment property are, all else equal, riskier than other residential mortgage loans. To be clear, the Reserve Bank is asserting that a loan is riskier because it is secured on an investment property, even if the initial LVR, the initial date at which the loan was taken out, the nature of the house itself, the borrowers’ income etc were all exactly the same as those for an owner-occupied loan.

What has always been a bit surprising is how little in-depth effort the Bank has put into demonstrating that its argument is correct. It has run a variety of arguments in principle about why investment property loans might be riskier than those to owner-occupiers. Most of those have never seemed overly compelling, especially not in a New Zealand context. Indeed, there are some reasons why the result could be reversed (for example, unemployment is probably the largest single risk, all else equal, in respect of an owner-occupier mortgage, but rental income flows – which help service investment property loans – tend to be less discontinuous).

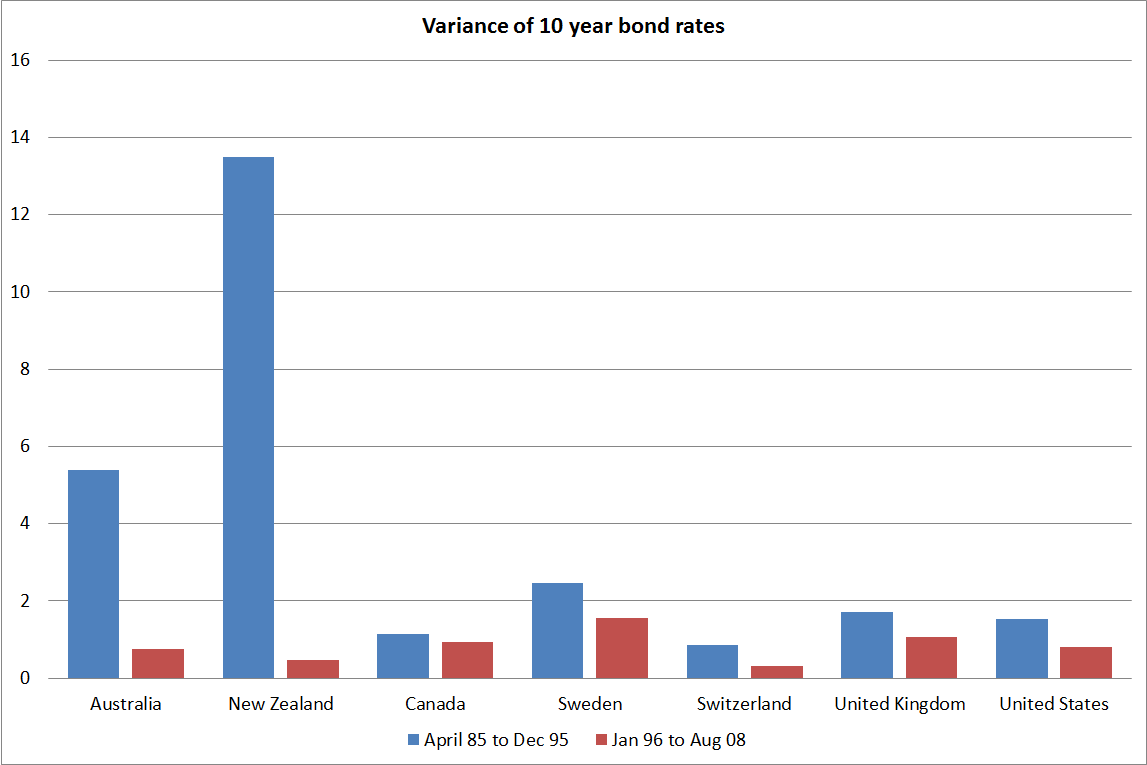

But the issue should ultimately, be an empirical one. All else equal, have investor property loans proved to be riskier than owner-occupier loans? Getting good comparable data isn’t always easy. Material loan losses tend to arise only when nominal house prices fall, and although real house prices fell sharply in the late 1970s, large nationwide falls in nominal house prices haven’t happened in New Zealand since the 1930s. Data from that period aren’t available – although perhaps it is an opportunity for an economic history PhD project working in bank archives. But even more recently, nominal house prices have fallen materially in a number of regions, and I have encouraged the Bank to ask banks for data on the loan loss experience (investor vs owner-occupier) in places like Gisborne, Wanganui, or Invercargill.

In fact, the Bank has tended to rely on a handful of overseas studies, about a handful of overseas experiences. This isn’t one of those areas where there are dozens of studies about dozens of episodes. That makes it all the more important that what studies exist are read carefully and applied and interpreted to New Zealand very carefully. That appears not to have been done. Worse, even when some weaknesses in the way the Bank interpreted and applied such papers were pointed out to them (in submissions on the consultative document), they largely just repeated their assertions and interpretations.

I’ve worked my way through some of the papers, and had had concerns about how the Bank had interpreted and applied the results. My former colleague, Ian Harrison, who consults as Tailrisk Economics, and is much more expert in the specialist risk aspects than I am, has worked his way carefully through each of the empirical papers the Bank has cited, and several that they should have cited, but did not. He has sent me a forthcoming paper “A House of Cards”, in which he has worked his way carefully through each of the Bank’s arguments and pieces of evidence. Cumulatively, it is a pretty damning read. Ian has given me permission to run some excerpts here, and I hope that when his paper is published it will get the attention it deserves.

On the international experience, Ian summarises as follows:

The international literature does not provide support for the Bank’s contention that investor loans are riskier and owner-occupier loans. Four of the four studies that controlled for other loan attributes found that investor status had no impact, or only a trivial impact, on default rates. A European Banking Authority survey of 41 advanced modelling banks found that none identified investor status as a risk driver in their retail housing mortgage lending models.

A good example of what appears to have gone on is how the Bank has represented an important paper on the Irish experience

Lydon and McCarthy 2011 “What lies beneath? Understanding recent trends in Irish Mortgage arrears”

The graph presented in paragraph 11 of the March 2015 Consultation document presents data from the Lydon and McCarthy paper, which addressed the question of whether BTL [buy to let] status was, in itself, a default driver, or whether the higher default experience could be explained by differences in other loan characteristics.

It was found that after controlling for differences in LVR and servicing costs, BTL status had no impact on default rates. The higher increase in observed BTL default rates was due to the fact that a larger share of BTL loans were made in the lead up to the GFC when underwriting standards were at their lowest point and house prices at a peak.

Naturally subsequent default rates were higher for investors who bought at the wrong time and who offered scant protection to the lender, but default rates would also have been higher than average for owner occupiers with the same characteristics.

The results of their analysis are presented in table 7 of the paper which shows that the coefficient for the marginal impact of BTL status is 0.00. This estimate is significant at the 1% level.

In a subsequent presentation (“The Irish Mortgage market in Context – Central Bank of Ireland 2011) the authors said:

“Controlling for LTV & MRTI…

–Relative to next-time-buyers (NTB), FTB borrowers are 2% less likely to be in arrears

–whereas, no relative difference for BTL”(our emphasis)

The data presented in the Consultation document does not provide evidence that Irish BTL loans are a riskier asset class. It is misleading to represent the paper, as the Bank does in several documents, that it provides evidence that BTL loans are riskier.’

Or, in respect of a US study:

Palmer C. (2014) ‘Why do so many subprime borrowers default during the crisis: Loose credit or plummeting prices’

The Bank made the following statement:

“Palmer (2014) reports that default rates increased in a multivariate regression with loan to value ratio and for loans that were declared non-owner occupiers.”

In his paper Palmer uses comprehensive loan-level data to decompose sub-prime loan loss defaults amongst three default drivers. His conclusion is as follows.

“Decomposing the observed deterioration in subprime loan performance, I find that the differential impact of the price cycle on later cohorts explains 60% of the rapid rise in default rates across subprime borrower cohorts. Loan characteristics, especially whether the mortgage had an interest-only period or was not fully amortizing, are important as well and explain 30% of the observed default rate differences across cohorts. Changing borrower characteristics, on the other hand, had little detectable effect on cohort outcomes. While quite predictive of individual default, borrower characteristics simply did not change enough across cohorts to explain the increase in defaults.”

There is no marker for investment property as such in the study, just a marker for whether the dwelling was to be owner occupied or not. It is not clear whether holiday or other second homes would fall. Regardless, the non-occupier marker fell into the borrower characteristic category, which in total provided little independent explanation of deliquency. There was no result that investor status increased defaults. The Bank’s statement was false.

I suggest that you read the entire document when it is available. As far as I can tell, none of the studies the Bank cites appears to have been fairly represented, or applied to New Zealand.

If Ian’s reading of the papers is accurate (and I have no reason to doubt it) it is a very disconcerting commentary on the processes in the Reserve Bank. The Bank has plenty of able people, who would have been well able to pick up on each of the weaknesses Ian Harrison has identified. And yet not just once, but again in the response to submissions, and in the new consultative documents, after the Bank had had time to consider the criticisms that submitters have made, the studies have continued to be explained or applied in ways that are, at best, misleading.

Reasonable people can reach different views on appropriate policy measures. I think the Governor of the Reserve Bank has far too much power in this area, and I disagree with the proposed restrictions. But if citizens cannot trust the Bank to cite evidence in a balanced and accurate way, confidence in the entire policymaking process is likely to be severely eroded.

As I have noted, in such areas the Governor is effectively prosecutor, judge, and jury in his own case. Worse, he is also responsible for the investigative work that is presented in support of the case that he will himself decide. Of course, he has staff to do the work for him, but the staff (and their managers) are hired, rewarded, and potentially fired, by the Governor. A strong Governor will want to know the weakest points in his own case, and to ensure that those weaknesses are appropriately aired, balanced presumably by other strong evidence or arguments for the sorts of regulatory initiatives he is proposing. But the Wheeler Reserve Bank appears to be one in which either no one is willing to stand up and point out the weaknesses or, if someone did point them out, where the Governor and his senior managers said, in effect, “oh just ignore that, continue to repeat the same lines”. One would hope there is a better explanation, but it isn’t obvious. The Bank’s Deputy Governor, Grant Spencer, for example, has spent decades in senior roles in the Bank, and many thought he was a strong candidate to become Governor in 2012. He has direct line responsibility for the two departments dealing with these banking regulatory issues. How did he let documents this weak go out, not just once, but repeatedly? Anyone can make a mistake citing a single paper, but the breadth and repeated nature of what Ian highlights has the feel of something more deliberate.

Even if the Bank could show, with some degree of confidence, that investor property loans were riskier than those to owner-occupiers, other characteristics held equal, the case for the proposed ban on lending in excess of a 70 per cent LVR for residential investment properties in Auckland has serious weaknesses. I elaborated on those in my recent submission (and have also requested copies of all the submissions the Bank has received).

I’ve been critical of the Governor’s conduct of monetary policy over the last couple of years. But reasonable people will, at times, reach quite different views on what monetary policy stance is required. His turned out to be wrong although, as I noted this morning, he had plenty of company for too long. But repeated misrepresentation of data to support a controversial regulatory initiative strikes me as much more serious. It might do less damage to the economy, but it strikes at the heart of the integrity of the institution, and raises serious questions about the extent to which the public can have confidence in the (unelected) Governor’s ability and willingness to carry out his statutory duties in the public interest, in an objective and dispassionate manner. Cynics might expect such standards from politicians. We certainly shouldn’t tolerate them from officials.

I hope that when Ian Harrison’s full paper is published, the Bank’s Board will start asking some pretty searching questions. The Board is charged to, inter alia,

- keep under constant review the performance of the Bank in carrying out—

- (i) its primary function; and

- (ii) its functions relating to promoting the maintenance of a sound and efficient financial system; and

- (iii) its other functions under this Act or any other enactment:

- (b) keep under constant review the performance of the Governor in discharging the responsibilities of that office:

Perhaps the Minister of Finance might refer the issue to Rod Carr, chair of the Board, for his views.