There was an op-ed in the Financial Times yesterday that had all the appearances of being written by a fluent sixth former who wasn’t that smart and certainly wasn’t that deep. But I guess we have to take the FT’s word that the column was in fact written by New Zealand’s Prime Minister, Jacinda Ardern. It read like several of her other efforts (eg here) if with a bit less feel-goodism than some, and a bit more of just making things up.

Since the column is behind a paywall, I won’t be copying chunks of it directly into this post, but even if you don’t have access I hope you get the gist.

She starts with the claim that New Zealand is “tiny”, apparently oblivious to the fact that in the United Nations list of countries and territories there are 100 with populations less than four million. But that claim is really just staging for her opening (and closing) claim about the mouse that roared: “we punch above our weight”. This is the sort of vapid (typically deluded) story that countries – and perhaps especially countries’ ministers and officials – like to tell themselves in private, but which quickly become rather embarrassing, a sign of insecurity and doubt more than anything, when uttered in public.

The only concrete evidence she adduces for this claim is 125 years old: New Zealand being the first country to grant women the right to vote, in 1893. Good for us, but rather a lot of water has flowed under the bridge since then. (And even from that era, I happened to be reading last week a biography of that courageous British campaigner Josephine Butler, who led the push for the repeal of the Contagious Diseases Act (in 1886) – this was, perhaps well-intentioned, legislation that grossly infringed the dignity and civil rights of women. Out of curiosity, I looked up the New Zealand experience: we finally repealed ours almost 25 years after the Brits.)

Almost every country has some “first” to its name, and some black spots from its past. In our short history (whether you think of it as 200 years or 1000) New Zealand is no different. The Prime Minister moves on to the claim that we were “one of the first” to put in place a “cradle-to-grave social welfare system that endures in some form to this day”. Do note that “in some form”, as if the Prime Minister is trying to suggest that in decades since then the welfare system has been ripped to shreds, only the tattered remains enduring, when in fact we now have 300000 working age adults receiving welfare benefits and about 750000 getting universal New Zealand superannuation. And today’s health and education spending (numbers, share of GDP or whatever) puts 1938 in the shade.

(And no mention, of course, of the fact that just a couple of years later, New Zealand was putting in place some of the most restrictive provisions around press freedom and conscientious objection found anywhere in the free world during the war. As I say, even the sainted Peter Fraser – from the Prime Minister’s own party – has his blackspots.)

The Prime Minister moves on to claim that “we are sometimes the first to learn valuable lessons”. This is an introduction to the sixth former’s account of the reform process of the 1980s and early 1990s.

Starting in 1984, New Zealand went further and faster than nearly any country in embracing the prevailing neo-liberal economic experiment. We slashed the top tax rate, dramatically cut public spending, removed regulations that were said to hamper business and vastly reduced welfare benefits paid to the sick, those caring for children and the unemployed.

It isn’t even clear where to start here. There is no recognition that we’d been quite late to the party, have wrapped up our economy in heavy protection and distorting regulation for several decades – more so again than most other democracies. Many – not all – of our reforms were about catching-up again. And yet she can’t even bring herself to acknowledge the costs and distortions (notice that “were said to be”). Or to claim some credit – for her own party – for the overdue reductions in trade protection that the reformers put in place. Or to note that as the top marginal tax rate was cut, so the tax base was broadened, and opportunities to avoid paying tax were substantially diminished.

Here is the evil low-tax regime that was created, as illustrated with OECD data on general government total receipts as a share of GDP going back to 1995 (which is about when the reform process ended, and also when the OECD has fairly complete data).

Over that quarter-century, we’ve basically been the median OECD country (literally so in in several years this decade). The comparable spending chart isn’t so very different (although we spend less than most relative to tax receipts – another way of saying we’ve avoided deficits and kept debt low), although the one period in the last 25 years in which government spending looks quite low by international standards is……the first half of the term of the previous Labour government.

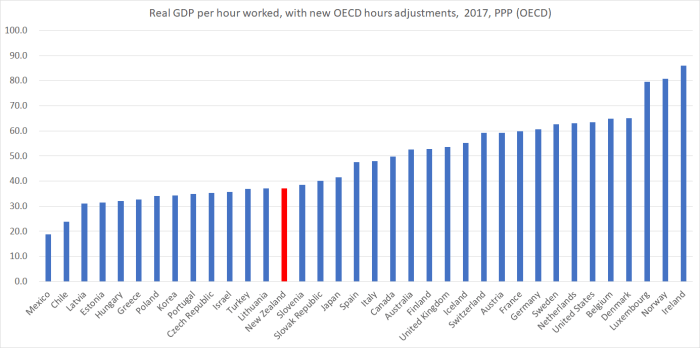

But even now the Prime Minister is just warming up because her theme appears to be inequality. Never mind that the labour share of GDP hasn’t changed much in 30 years now, or that wage growth has been running ahead of growth in GDP per hour worked. Never mind the indications that inequality measures haven’t changed much here for 25 years, or that much of any concerning developments seem to relate to the spiralling costs of housing – a development only made possible by restrictions imposed and maintained by successive National and Labour governments. No, it is all the liberalising economic reforms that are “to blame”.

And all this while, oddly (but as she did during the election campaign), appearing to accept that narrative that somehow our economic performance has been just fine. But, of course, there are no mentions of our shockingly poor long-term productivity growth performance (past and present), no recognition that New Zealand export and import performance has been disappointing, no nothing. Far from “punching above our weight”, it is hard to conceive how a country which had built what it had in, say, 1913 could have done so badly in the subsequent 100 years – without even the excuse of the physical devastation of war, military coups, or Communism.

Of course, none of this seems to be based on any analysis or research. Instead, the Prime Minister tells us of her childhood memories, in which kids in the town she was living in “weren’t born into a decade of hope and opportunity, but one of inequality where users had to pay for basic services”. Perhaps she means they had to pay for food and electricity, but then users have always had to pay for those? As for schools and hospitals, they were – and are – more or less free, and we’ve never the British system of generalised free GP visits. So what on earth is she talking about?

And then the violins start up to accompany a mournful tale of the death of democracy and of prosperity from which she, and the New Zealand way, can save us.

We don’t need to start again, but we do need to change the way we do things. In May, my government will present the world’s first “wellbeing budget”.

All, apparently, premised on the weird, tendentious (and borderline dishonest) claim that any government anywhere – especially in the free world – has ever defined success solely in terms of GDP. Perhaps she could pause a moment in her progress among the left-liberal elites to give us some evidence for that claim? Have governments not been spending on education, on health, on defence, on age pensions, even on arts and the culture for generations now? Not just in New Zealand but around the advanced world. Have not cost-benefit analyses – that don’t just cover GDP effects – been part of spending evaluation for decades?

And thus the great mystery of the much-vaunted “wellbeing budget”? Is anything going to be any different from what we might we might expect from a left-wing coalition government anywhere that happened to be running budget surpluses. In her column, the Prime Minister talks of spending more on mental health, especially for young people. You might think that is sensible (I suspect that, even if some of the spending is worthwhile, it is going to be mostly papering over cracks, while refusing to address the social and cultural issues that underlie the problems we observe) but it is what left-wing governments typically do – they throw more money at things. Perhaps it is even what the voters want – after all, globally, government spending as a share of GDP is typically higher than it was 50 years ago – but don’t try to pretend that it is a whole different approach to life, economic management or government management. One only has to look at the wellbeing dashboard to see a grab-bag of vapidity, rather than a serious approach to better policy. It is, among other things, a cover for the utter failure to even begin to grapple with the repeated failure on productivity.

(And, of course, while on the subject of increased spending, there is the oddity that people from the left and right point to: she proposes to change the world, laments how public spending was slashed, but her government published plans just before Christmas that involve

On the government’s own numbers (and these are pure choices, made by ministers), core Crown spending in the coming five fiscal years (including 2018/19) will be lower every single year than the average in each of the three previous governments, two of which were led by National.

She goes on to claim that “this isn’t woolly but a well-rounded economic approach”. Perhaps around the Cabinet table and even among some of her Treasury acolytes they even believe this nonsense. In fact, it is no economic approach at all, consistent with a government that has done nothing – seems to plan nothing – to reverse the decades of relative economic decline, that have so badly limited the possibilities for New Zealanders (reflected, inter alia, in the decades-long exodus of New Zealanders). Weirdly, she claims that this “well-rounded economic approach” is same one she plans to use to respond to (inter alia) climate change, domestic violence, and housing. This in a week when the latest Demographia report again reminds us just dreadfully unaffordable housing is in New Zealand – and when her surrogate senior minister could go through an interview on the subject on Morning Report yesterday and not even (that I heard) mention land liberalisation.

Warming to her theme, the Prime Minister calls on those around the world to look to her “wellbeing approach” could be a “model” for others to respond to the problems of the world. She asserts

I wholeheartedly believe that more compassionate domestic policies are a compelling alternative to the false promise of protectionism and isolation.

Spending more is apparently the answer….but (on her own rules) not more than 30 per cent of GDP. Nothing at all, of course, about lifting productivity growth. Nothing about fixing the huge regulatory distortions that render housing so unaffordable in many countries, notably her own. Just more compassion. More kindness.

As I observed of one of her earlier vapid efforts

We don’t want political leaders who can’t identify with individual need, opportunity and so on. And yet, when one is dealing with five million people – and government policy choices affecting many or all of them – you need to be able to stand back and think about things differently, to analyse issues systematically, to recognise (for good and ill) the force or incentives, to think about the longer-term as well as the short term, and so on. And even to recognise that values and interests can, and often will, be in conflict – in many areas hers aren’t Family First’s or the oil and gas industry’s (or mine for that matter). Politics is partly about navigating those differences, seeking reconciliation where possible, but also about making hard choices and trade-offs.

There is no sign that she brings any of those skills to the job. Just a smile and lots of breezy vapid blather.

The Prime Minister ends her column with another deluded call, suggesting that she hopes New Zealand can once again “punch above our weight” by “forging a new economic system based on this powerful concept [guardianship]”. Which might perhaps be fine if there were any substance to what she is talking about, but there is no sign of any. She wants to spend a bit more (but not much), she wants to eliminate net carbon emissions in an country with seriously high abatement costs which her own government’s consultative paper data suggest will fall most heavily on the poorest, and she does nothing at all to fixing the disgrace that is New Zealand housing affordability, or to even think about reversing decades of relative decline. Perhaps it all sounds good to a few readers – and Davos attendees – but it offers nothing of substance to New Zealanders, let alone to the world.