We’ve been hearing quite a bit from the Reserve Bank recently (in addition to the OIA disclosures of the Governor’s antics last year), just not much about monetary policy, short-medium term economic developments, or financial stability and regulation. In a few weeks the Governor will have been in office for two years, and in that time we’ve not had a single serious and thoughtful speech from him on either financial stability/regulatory issues or on monetary policy and cyclical economic issues. It is extraordinary, and not the sort of thing we’ve seen here in the past or in other advanced countries today. As it happens, the new MPC members have now been in office for 11 months, and we’ve not seen or heard a word from any of the external members at all.

But what of Bank management? If they haven’t been talking about core business (that small matter of the statutory responsibilities they are funded for), they’ve been out championing other causes, including themselves.

Last Wednesday the Governor (and accompanying senior managers) turned up at Parliament for the annual Finance and Expenditure Committee financial review hearing. The Governor’s opening statement is here. The only bit that immediately caught my eye was this

Amendments to the Reserve Bank of New Zealand Act, which came into effect on 1 April, gave responsibility for monetary policy decisions to the newly-established Monetary Policy Committee.

This framework has now been implemented and is working well, with six Official Cash Rate decisions by our new Monetary Policy Committee. The Summary Record of Meeting provides insights into how decisions are reached, and improves our stakeholders’ understanding of each Committee member’s contribution.

That final sentence, and particularly the second half of it, is at best spin, more accurately just a lie. The Governor explicitly states that the Summary Record “improves our stakeholders’ understanding of each Committee member’s contribution”, when of course – go and read them for yourself if you like – that is simply false. Not only does the Summary Record give no real sense of “how decisions are reached” but, by explicit choice and design (endorsed by the Minister of Finance), there is no reference at all to the views, arguments, analyses etc of any individual Committee member. And – did I mention this? – none of the externals has been heard from in any other fora. We have no idea whether they are making any contribution at all. It is breathtaking that the Governor can so actively and deliberately – in writing – lie to a parliamentary committee. In isolation perhaps it is a small point, but if we can’t count on a very and powerful public official in the small and visible points, how do we trust him more generally.

The FEC appearance was also an opportunity for the Governor to bid for more resources – a lot more resources we are told. According to the Stuff account, the Governor is bidding for a “30 per cent perhaps” increase in the Bank’s funding, claiming that (in respect of bank supervision)

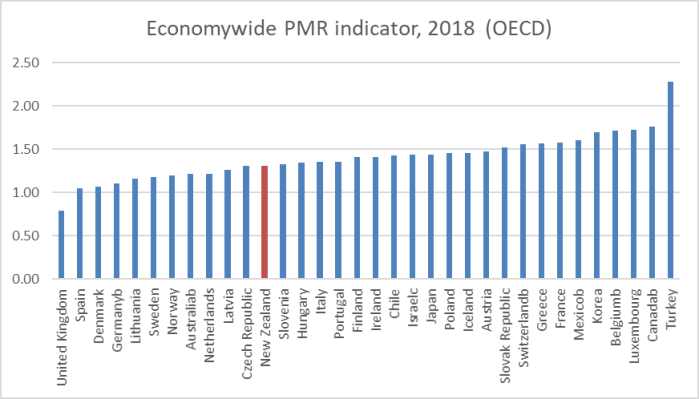

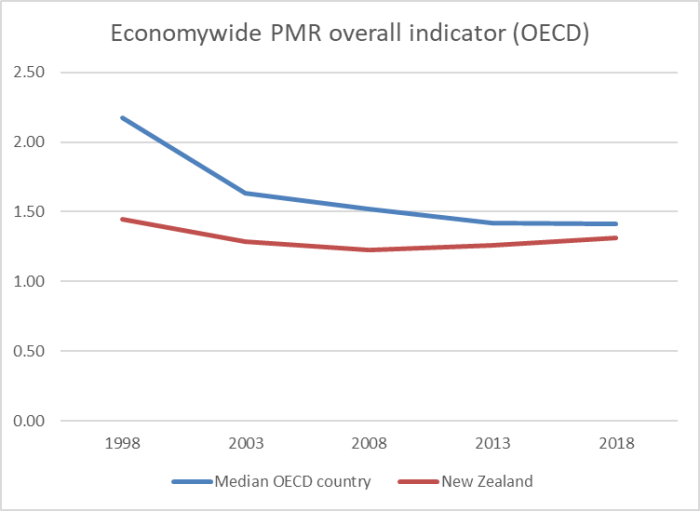

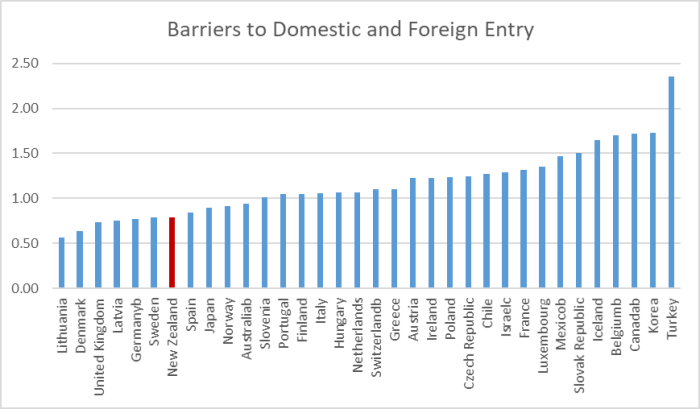

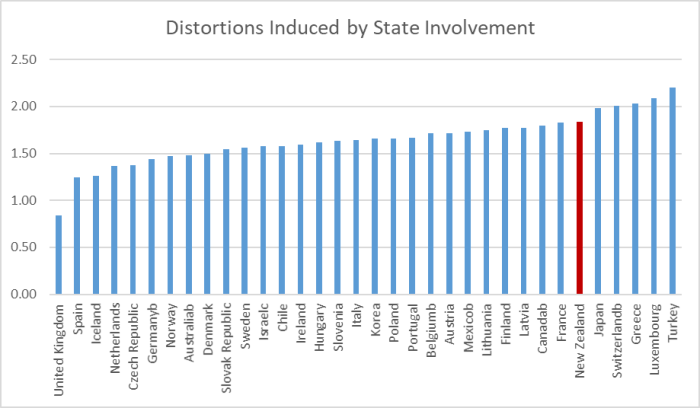

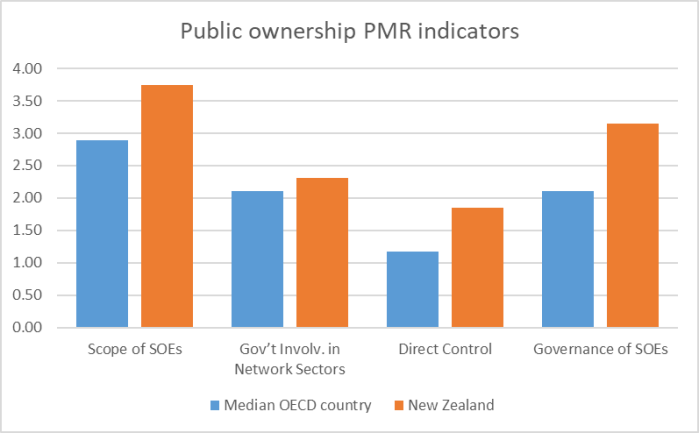

The Reserve Bank’s existing resource was at the the low-end, if not “the lowest”, in the OECD

Which might sound more worrying/inappropriate were it not for the fact that New Zealand is among the smaller OECD countries and one of the poorer OECD countries, and also a country with a record of a sound financial system, and one dominated by banks already subject to serious supervision in another country that also has a long record with a sound financial system.

On several occasions over the years I’ve been willing to defend or even champion the case that the Reserve Bank is probably a little underfunded. But it gets progressively harder to defend that view as the evidence mounts for how undisciplined the Bank is in the use of the resources it already case. There was the million dollars for the Maori strategy, or the trips to international climate change meetings (and resources devoted domestically to such issues, for which the Bank has no particular responsibility) and there is the sense of a proliferation of staff in the communications/PR areas of the Bank. I can’t yet formally verify that – although I have lodged an OIA to get chapter and verse – but I’m not the only person to note the range of new people/positions (on the bottom of press releases, emails or whatever) and my favourite anecdote was one a friend told a few months ago about being approached by a headhunting firm to consider applying for a job in something like “stakeholder relations” at the Bank, a job my friend characterised as “having coffee with a lot of people, getting paid $180000 a year”. I hope The Treasury and Grant Robertson will be having a close look at whether there is any sort of culture of ruthless prioritisation, frugality etc in how the Governor uses what he has, before offering up yet more public money. There isn’t much sign of it.

Stuff also reports that National’s Finance spokesman Paul Goldsmith challenged Orr on his conduct

National Party finance spokesman Paul Goldsmith questioned Orr on the bank’s reaction to “criticism and debate” during a series of exchanges at the select committee, saying the Reserve Bank governor had “very significant independent powers” over the industries the bank regulated.

“From my point of view it is very important that we have open and robust discussion,” Goldsmith said.

“We wouldn’t want to have an independent governor with a glass jaw or a sensitivity to robust criticism,” he later added.

Orr’s response?

“What I won’t stand for is abuse of my team or myself,” he said.

He keeps claiming he and his team have been “abused” in some inappropriate or unacceptable way, but has not yet shown us a shred of evidence for those claims, suggesting that what is really at work is a powerful public figure who simply can’t cope with being challenged. As one of his former staff put it last week “he could always dish it out, but could never take it”.

I hope Goldsmith won’t let the matter rest, especially if he should become Minister of Finance later this year.

Orr was back on the public stage on Friday with a speech, delivered to a business audience in Christchurch, under the title “Aiming for Great and Best at Te Putea Matua” (that being that Maori label the Governor has chosen to attach to the Bank). The, perhaps rather odd, title refers to the Governor’s vision for the Reserve Bank “Great Team and the Best Central Bank”, the even more overblown goal than the one his predecessor had introduced, aiming to be the best small central bank in the world (when I asked, a few years later, what steps they’d take to benchmark themselves and measure whether they were getting close to the goal, the answer came back “nothing”). Nothing wrong with aspiration and ambition of course – although it is not clear that taxpayers would choose spend resources so heavily that a small, not very rich, country’s central bank would ever be best in the world. The real problem is the delusional nature of the claims, the visions, which seem more about spin than substance. Excellent central banks don’t have thin-skinned bosses, unable to keep their thin-skinnedness under control. Excellent central banks have senior figures who make excellent thoughtful speeches. Excellent central banks are producing a steady stream of insightful research. Excellent central banks underpin major policy initiatives with confidence-inspiring research and analysis, taking seriously alternative perspectives.

(Come to think of it, excellent central banks don’t just make stuff up when testifying to Parliament.)

We don’t have an excellent central bank (although it still has some good people); instead we have an organisation that has become little more than a platform for the Governor’s ambitions, whims, and political preferences, with little or no sense of boundaries, restraint, or the proprieties of public office.

I’m not going to waste a lot of time on a detailed review of the speech. Frankly, it is fairly dull although suffused with the Governor’s personal whims, especially around climate change (important issue and all, but really nothing whatever to do with the Reserve Bank). But do notice just how the Governor operates. There was this line

We have now made six Official Cash Rate (OCR) decisions – as a committee. We have managed robust discussion and come to consensus decisions. The nature of these discussions is published as a ‘Record of the Meeting’ for all to see. We also won this year’s Central Bank award for transparency in how we operate.

It is technically accurate, except that the transparency award they won was explicitly for one small element – the (quite good) Handbook they’ve published on monetary policy – not at all for anything about how the Monetary Policy Committee functions or how the ‘Record of the Meeting’ operates. It is just dishonest. It should be unworthy of – beneath – a major public institution in a sector where trust is supposed to be central.

A Stuff story appeared this morning about some more of the Governor’s comments. I first assumed it must be referring to the (published) Christchurch speech, but the article says it is talking about a speech given in Auckland (perhaps he used much the same text?). We get accounts of Orr as populist (also there in the published speech)

“I’m not here to talk to a few narrow specialists. I’m not here to talk to just the institutions we regulate.

“We are the central bank of everyone here in New Zealand, present and future, and we have been too narrow and too lax in our engagement with you all, and it is not going to happen again.”

The problem, of course, is that (a) few “specialists” actually have much confidence in him, (b) in all fields of life, we rely on “specialists” to help us evaluate and hold to account powerful public agencies (something Orr isn’t keen on at all), and (c) all that business about how his predecessors didn’t get out and talk to wider audiences is just so much nonsense, simply inconsistent with the facts. Perhaps Orr has forgotten Don Brash’s in(famous) retail roadshows, or Graeme Wheeler’s repeated talk about how he and the Bank were going to talk to a wider range of people. Some questionably, Alan Bollard even wrote a book (not inaccesible either) while in office.

And the article ends with an account of Orr’s answer to an audience question, which seems like quintessential undisciplined Or

Orr spoke about the importance of economic and social inclusion in response to a question from Jackie Clark, founder of The Aunties whanau support movement, who complained New Zealand was a low-wage economy.

“The owners of capital have been doing a great job over and above the owners of labour,” Orr said.

“It’s been extreme, unprecedented, over the last 40 or 50 years of that ongoing return to the owners of capital, and labour has become a global commodity, where production goes to the lowest common denominator.”

“That’s how we roll. That’s how we have to roll, otherwise create yourself a gated community. Enjoy yourselves, but don’t leave.”

Would have sounded just great in a stump speech from Bernie Sanders, Alexandria Ocasio-Cortez – there is at least some evidence in support of his story in the US – or even Marama Davidson. But (a) this is New Zealand, and (b) you are the Governor of the Reserve Bank, with quite narrow responsibilities for monetary policy (affecting only nominal variables beyond the short-term) and regulation for prudential purposes of some classes of financial institutions. Instead, we get a rampantly partisan/ideological answer (inappropriate in itself, but when did bounds and norms bother Orr?), but one with little or no grounding in facts.

(A prudent grounded answer to the question might have been to note that distributional issues are not an issue for the Reserve Bank, but that in the longer-term only productivity growth will support a much higher wage economy. Both statements would be accurate and uncontentious.)

Those first two sentences in Orr’s answer seemed to be about the labour share of income. The data are summarised in a chart in this post. In New Zealand – it is different in some countries – the labour share of income rose in the 1970s, fell in the 1980s and (depending on your measure – I show three) is now just a little higher or a little lower than it was fifty years ago. You might personally argue for some different split of the pie, but what in the New Zealand experience justifies Orr’s flamboyant off-reservation ideological rhetoric.

Or what about how wages have been rising relative to economic capacity (say, nominal GDP per hour worked, capturing productivity and terms of trade effects). Well, as I illustrate every so often (most recently last month), this century, wage rates in New Zealand have been rising faster than GDP per hour worked. Perhaps Orr doesn’t know that – it certainly doesn’t suit his ideological message – but whether he knew it or not he actively misled his audience, while working on the taxpayer’s dime.

I was going to round off this post with a fairly detailed critique of a truly dreadful speech given a week or so ago by one of Orr’s principal deputies, Christian Hawkesby, the Assistant Governor responsible for economics, monetary policy and financial markets on “The Maori World View of the Reserve Bank” but with quite a bit else – including some atrociously bad history – thrown in, concluding with the absurd hubristic claim that the Orr/Hawkesby Reserve Bank is “putting the New Zealand back into the Reserve Bank of New Zealand”. You’d think they were candidates at this year’s election, not senior (supposedly non-partisan, supposedly operating within the constraints of specifc statutes) statutory public officials. But perhaps I’ll save that speech for another day, rather than risk losing the focus on the Governor who yet again reveals himself as simply unfit for the office he holds. And yet those paid to hold him to account sit idly by.