It is pretty clear that the main (external) reason our two main political parties have been so reluctant to say very much at all critical of the increasing threats posed – to people in China or abroad (not overlooking there the ethnic Chinese New Zealanders) – by the CCP-controlled People’s Republic of China relates to the fear that New Zealand exporting firms might find themselves subjected to the PRC’s attempts at economic coercion. Quite possibly the flow of political party donations might be part of the story. No doubt the anti-Americanism that pervades much of the left in New Zealand (and a detestation of the current Australian government), combined with that weird belief that somehow New Zealand is better than both – perhaps able to be some sort of “honest broker” – plays some part. That self-regarding nonsense of the “independent foreign policy” – as if we didn’t make our own choices (rightly and wrongly) to support the UK in the Chanak crisis, to support sanctions in the 30s at the League of Nations Council, to enter World War Two, to offer support on Suez, to participate in Vietnam, to provide a frigate at the time of the Falklands, to play a part of the first Iraq war, and not to play a part the second – seems to be there, although mostly as cover, an excuse. Perhaps for a few individuals the prospect of lucrative or prestigious post-government roles plays a part, although I doubt that is really a serious driver for many (though those now holding such posts – and wishing to continue doing so – are themselves effectively silenced).

But no one really doubts that the biggest consideration is trade. There was a time when we used to hear, over and over again, the nauseating line that “New Zealand’s foreign policy was trade”, but if that line hasn’t been heard much in recent years, it is the subtext to so much around the PRC. In fact, often not even the subtext: Newshub had a story in the last day or so in which National’s foreign affairs spokesman Gerry Brownlee is quoted. The first bit sounded relatively encouraging (for the National Party)

Gerry Brownlee, National’s Foreign Affairs spokesperson, hopes Mahuta shares any information she receives with other parliamentary parties. He’s also pushing for an independent observer to be sent to Xinjiang.

“I think that should be advanced as soon as possible as this isn’t going to go away until there is greater certainty about it nor can there be a clarity of action until there is a greater certainty about it one way or another,” he told Newshub.

He said if there are atrocities found to be taking place “on the scale we are told about, that might make the genocide test”.

But….

“But you have got to bear in mind that there are hundreds of thousands of New Zealanders at work today largely because of our trade with China. It is not a simple matter, it is not a straightforward matter, it is one the Government should definitely have a position on.”

“Genocide” (or even “just” gross and systematic state sponsored and administered human rights abuses) or trade. Sounds like Mr Brownlee thinks it a tough choice. (And in fairness, if it is particularly crassly expressed, there is no sign his basic view is much different from of his Labour counterparts).

There seem to be twin (related) mythologies at work. The previous National government sometimes liked to run the (deeply fallacious) line that somehow New Zealand firms’ trade with PRC entities had “saved” the New Zealand economy from the ravages of the 2008/09 recession – which allegedly would otherwise have been much worse here otherwise. No evidence was ever advanced for this proposition – that Murray McCully seemed particularly found of – and it seemed to (conveniently) escape notice that New Zealand’s total trade shares (of GDP) were falling not rising over this period, that New Zealand’s productivity performance over this period was woeful, and that it took 10 years for our unemployment rate to get back to pre-recession levels, slower even that the US – the country at the epicentre of the financial crisis that helped precipitate that recession.

And that mythology – less heard these days – is supplemented by a story that – so it is claimed – much of our prosperity (such as it is) rests of trade with the PRC, with the implication (from some) that we should be suitably grateful, or at least simply keep quiet, think kind thoughts privately, and be thankful for small mercies (our prosperity). Again, the argument simply doesn’t stack up. To a very large extent, countries (all of them) make their own prosperity (or lack of it). We weren’t among the very richest countries in the world in the first half of last century because of any other country, but because of some mix of technology, institutions, people, natural resources and so on. We don’t languish well down the per capita income league tables (albeit still a long way ahead of China) because of anyone else’s choices, but mostly because of our own policies. China didn’t make us rich or poor. It made China first (last century) poor, and eventually middle-income.

Now, middle-income only as the PRC may now be, there are a lot of Chinese, so China’s share of total world economic activity and demand is substantial, and likely to be growing for some time. And perhaps there are a few products and a few countries where it might be said that China makes a real and sustained difference to the country concerned: Australia, for example, has 30 per cent of the world’s iron ore reserves (and a larger share of production) and China currently consumes a very large share of world iron ore production. But even if Chinese demand makes a difference to Australian average incomes, Australia was a prosperous first world country before Chinese iron ore demand became so large, and would be still without it. Total gross iron ore exports from Australia are equal to about 5 per cent of Australia’s GDP.

The world price for commodity products is determined by world demand and supply conditions, a point given far too little attention in the timid New Zealand discussion of PRC issues. A severe and sustained recession in China would represent a significant (but cyclical) blow to the world economy, and to New Zealand – and would do so whether or not New Zealand firms traded much directly with PRC counterparts. That is also true – as we saw in 2008/09 – of severe US recessions. That sort of shock – and others like them, at home or abroad – is why we have a floating exchange rate and discretionary monetary and fiscal policy.

What is much less clear is how significant the economywide impact might be of any one country – the PRC – attempting economic coercion on New Zealand. There would clearly be an impact on some individual firms (big and small) but that shouldn’t be a first order consideration for New Zealand governments in setting foreign policy and considering articulating perspectives on human rights abuses.

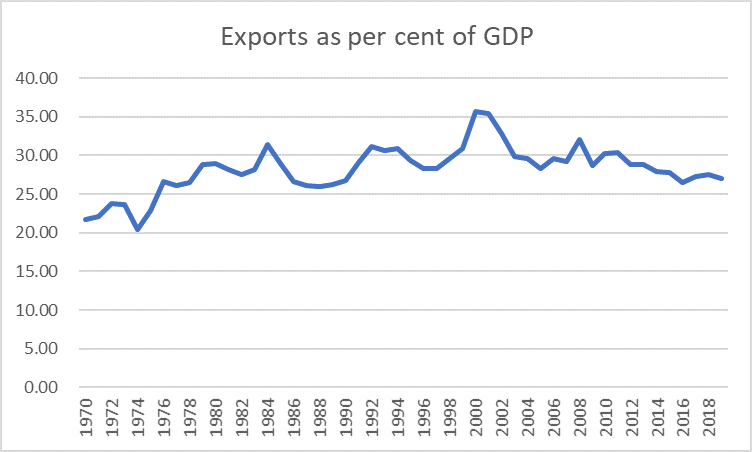

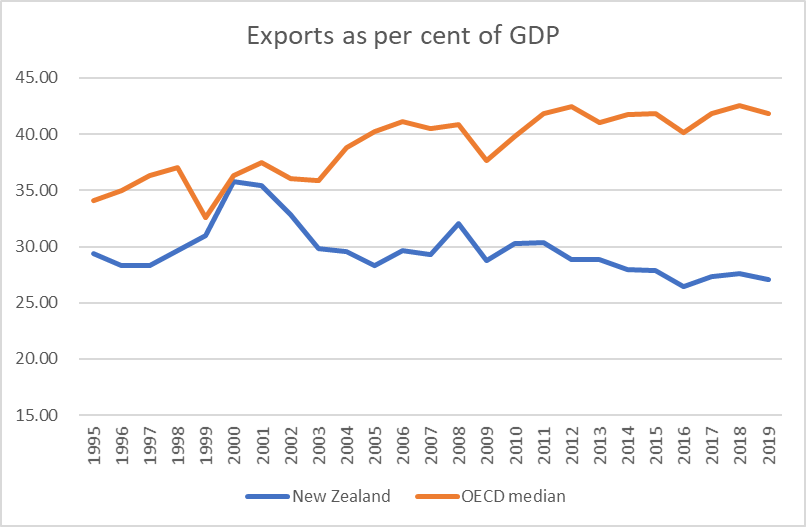

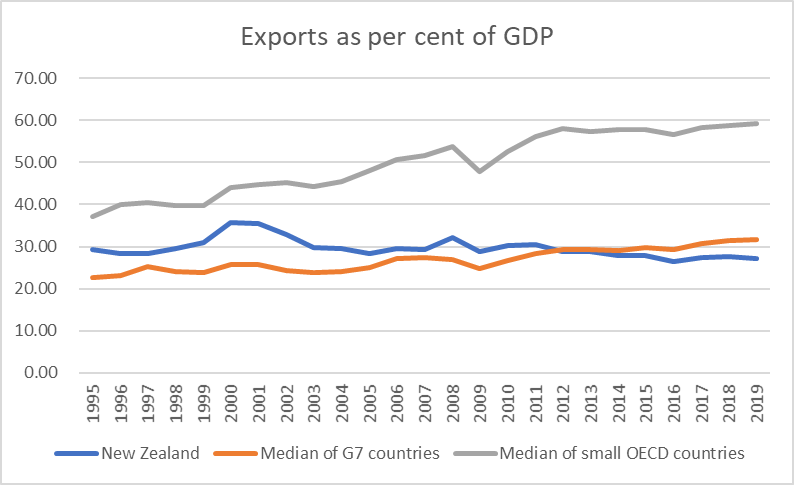

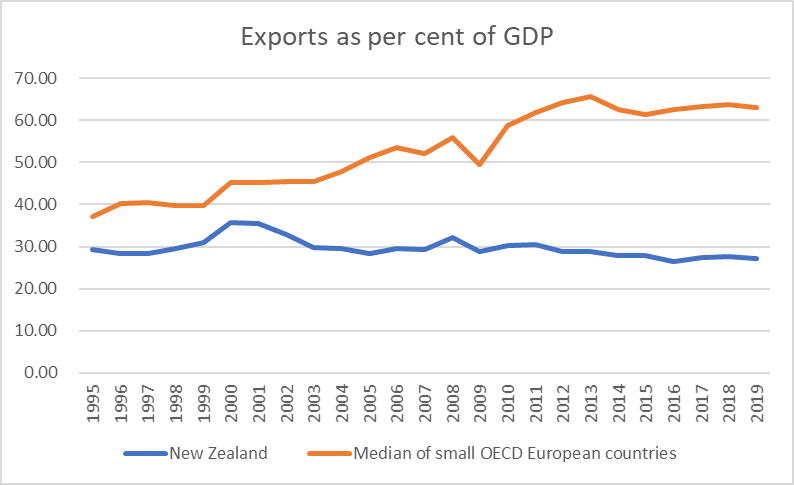

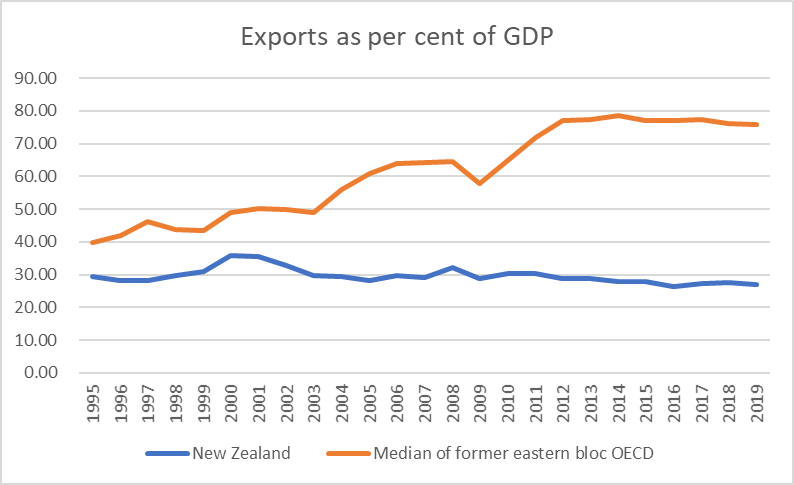

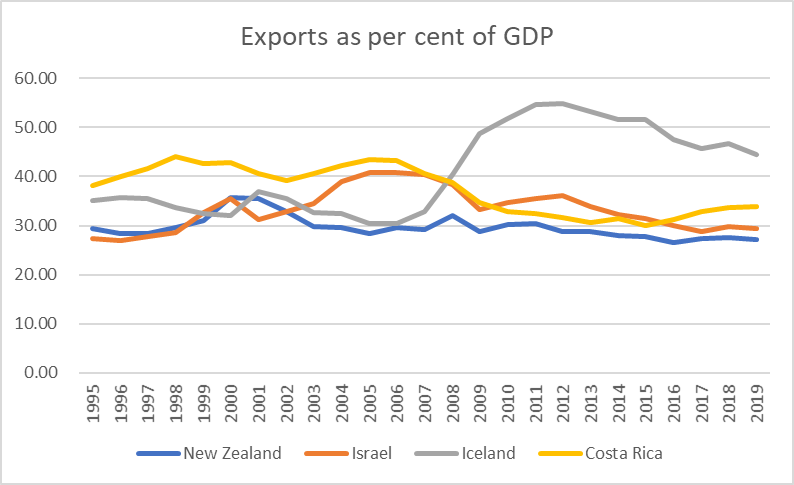

We can set some issues to one side. Yes, we are small, but that isn’t terribly relevant to anything. Yes, New Zealand firms trade internationally, but contrary to the rhetoric about being a “small highly open economy”, actually the share of our economy accounted for by foreign trade (exports and imports) is (a) much less than one would normally expect for a country our size, and (b) has been shrinking. And, yes the PRC recently moved a bit ahead of Australia as the country where the most two-way trade is done with, but – as people have noted for decades – one notable thing about New Zealand is that our trade isn’t very concentrated with any single other country/region (much less so than is the case for Australia). Total New Zealand exports to China, pre-Covid, were about 5 per cent of GDP. Even the EU apparently now has the PRC as the country with which the most foreign trade is done.

I’ve written on this issue before, and suggested then that the sectors of greatest vulnerability might be export education and tourism. As it happens, Covid has dealt to those particular markets for the time being (as it has for Australia). That isn’t a good thing in and of itself, but it does take those considerations off the table if the government were to think of taking a stronger stance at present. The focus for now is commodity exports (dairy, forestry, meat, crayfish etc).

And here it is helpful to look at the experience of (a) the Australian economy, and (b) Australian firms – keeping the two as distinctly different – in the face of blatant PRC economic coercion over the last year or so. There are some sub-sectors and firms that appear to have had it very tough – watch the ABC documentary screened the other day – and listen to the anguish of some of the small crayfish operators (who could still sell crayfish, but only at much lower prices). For reasons that aren’t clear to me, the wine producers exporting to China don’t yet seem to have been able to re-direct their sales (fortunately, in that sense, New Zealand wine exports to China are small). On the other hand, barley producers don’t seem to have been that much adversely affected at all. That is pretty much what you’d expect in a commodity product: some cost, some disruption, some stress for firms involved, but at the end of the day overall global demand and supply conditions won’t have changed much if at all. What we don’t see is any sign of severe economywide consequences: there is no mention of the issue (or risks) in the Reserve Bank of Australia’s latest (lengthy) minutes (by contrast, changes in New Zealand population growth actually get a mention). It seems to a third-order issue at a macroeconomic level – and the overall economy is what governments should be thinking about when they consider economic risks and consequences.

Were it otherwise, by the way, that is what we have macroeconomic policy for, fiscal and monetary, to help smooth the economy in the face of disruptions, whether Covid, coercion, or whatever.

Would it be any different for New Zealand? It is always possible, but it is not as if Australia is the only country the PRC has tried coercion on. They’ve had a go at Norway, at South Korea, at Taiwan, at the Philippines, at Mongolia, at Japan, in one form or another. In some case the governments have buckled – lobbying for special interests will do that – but in no case was there any evidence of a very large adverse macroeconomic effect. Nothing of the bogeyman story that our “elites” would like us to believe, that to offend China would be to jeopardise our very economic security or prosperity.

Of course, people will point out that China has not yet tried sanctions on Australian iron ore (but they did with coal, only to run into problems, because they still needed coal). But isn’t dairy different? The whole path of industrial development and infrastructure does not hang on dairy in the way perhaps it does on iron ore. No doubt, but PRC consumers have a clear demand for milk products, Chinese production is still nowhere near Chinese consumption, and the PRC has a history of attempting coercion mostly on things that don’t affect them, and their people, too much. So, sure China could ban New Zealand dairy exports for a time, but the underlying demand won’t change, and if China takes a large chunk of New Zealand exports at present, China’s imports are small chunk of world production. Now there are complications: “dairy” is not some single homogenous product, and cross-border trade in dairy is small compared to global production, but markets will adjust. Perhaps the world price for our specific products would fall a bit, and for a time, but….the nature of commodity markets is that prices are volatile. Perhaps luxury products like lamb for the restaurant trade might be a more likely target, but then the experience with Norwegian salmon was that total Chinese imports of salmon barely changed, with suggestions that quite a bit of Norwegian made its way back into China via Vietnam.

Whatever the potential disruptions for individual firms – and they are real (for them) – it simply is not credible – given the (smallish) size of our total exports, the commodity nature of most, the share of trade with China – that any sort of conceivable economic coercion would represent a serious sustained threat to the New Zealand economy. Production of most of our commodity products would be unlikely to change much at all, and if the prices of some were to fall, well we are not unused to terms of trade fluctuations. And floating exchange rates are part of the mechanism for buffering such shocks if they do end up a bit larger than expected. The Governor continues to swear by the potency of monetary policy and the many champions of active fiscal policy do the same for it. There is little that is unique about our economy or our risks vis-a-vis China. Just the choices of our governments, egged on by business and university leaders (the interesting thing about Australia now is the lack of business voices calling for the government there to pander anew).

Perhaps also we might have more sympathy for individual New Zealand exporting firms if it was five years ago, when PRC issues and risks were just beginning to emerge, and the experience of economic coercion was both newer and little known here. But no firm that trades with Chinese counterparts now can say they are unaware of the risks. They continue to trade with their eyes wide open (or prefer to pretend a different reality). When you sup with the devil, the standard advice is to take a long spoon. It simply isn’t obvious why firms that deal with Beijing – that perhaps have CCP cells in their subsidiaries in China – warrant our sympathy or support at all; one might argue rather the contrary, in that their voices – lobbying the government to do and say as little as possible – serve the interests of Beijing more than those of New Zealanders as a whole. (And one can’t help wondering how willing New Zealand firms will be to send staff to China once travel is easier, given the sort of travel warnings other countries have issued – and the arbitrary kidnappings the regime has engaged in).

Thus, when the government talks of how it wants to “respect” China – and even has the gall to suggest Australia might show more “respect” – the “respect” they want to offer to these thugs and bullies (to understate the evil of one of the very worst regimes of the planet) is a kowtow not on behalf of you and me – the voters who elected them, the citizens they supposedly represent – but a small group of firms (small and large) only too happy to have you and me pay the price of insurance for their business (we see it also in the substantially government-funded China Council which mostly serves business interests too). The government might want people to believe all those interests are aligned, but they aren’t.

The government has talked a little of encouraging diversification, and of the need for firms to have resilience plans. It probably doesn’t have much substance unless and until the government is willing to tell firms that they are on their own, and to back that up consistently. Most firms don’t trade with Chinese counterparts because of any love for the CCP, but because they perceive the risk-adjusted returns are best there. But that risk seems to be underwritten – diminished sharply – at our expense by a government that chooses to go as soft as it possibly can on Beijing, to feed lines that – wittingly or not, and probably not intentionally – give aid and comfort to the regime.

Finally, it is worth remembering that there is no suggestion that New Zealand should cut trade with the PRC (although individual New Zealanders might increasingly choose to avoid tainted products and companies). The trade threat we are discussing here is entirely something the PRC might choose. It isn’t the way normal or decent states operate, and yet our government would prefer us to pretend that the PRC is just a normal state, run by decent “respectful” people. We can’t stop them disrupting two-way trade – which isn’t some gift to New Zealand firms, but of mutual benefit in normal circumstances – but we can be clear about the values we hold, the interests we want our governments to serve, the real threats that everyone knows but which the government refuses to discuss openly. Values are things that you are willing to pay a price for, and the test of whether they really are values only comes when the possible price has to be faced. I don’t suppose Jacinda Ardern, Nanaia Mahuta, Judith Collins or Gerry Brownlee really like the CCP and its action any more than I, or many readers of this blog, do. I don’t suppose the CCP thinks they do either. They don’t care a jot what leaders think privately. It is what they are willing to speak up about, and act on, that bothers them. And they are right to draw the distinction: private thoughts and feelings signify nothing, especially in a purported leader, without follow through.

As it happens, any “price” New Zealand as a whole might pay seems likely to be modest at worst (worse for some firms, but they’ve chosen – entirely voluntarily – to keep trading with the thugs). It isn’t as if any better stance New Zealand might take would now be world-leading or ahead of the pack. And there would be the comfort of working together – with likeminded countries, of the Five Eyes or beyond, to name evil where it is found, where it threatens values we hold dear, other democratic countries, and the freedoms of the Chinese people themselves.