As I noted in Saturday’s post about The Treasury, the Secretary to the Treasury – he of the rushed citizenship presumably on the grounds of some exceptional services the previous government thought he might offer to New Zealand – gave a speech last week on productivity.

One can feel a little sorry for senior public servants venturing into the public domain. After all, there are limits as to what the head of a government department can really say, while still retaining the confidence of his/her minister (let alone that of the State Services Commissioner). Political masters change and with those changes there are changes in what can’t really be said in public by their most senior advisers. All of which is probably a good reason why heads of government departments shouldn’t really give any but the most anodyne (or perhaps obscurely technical) public addresses (in fact, most simply keep quiet in public – do a search for speeches by the Secretary of Justice or the chief executive of MBIE and you won’t find much, if anything). After all, their primary job is to advise ministers, not to act as public lobbyists for their own policy preferences Upon leaving office they are, of course, free to champion whatever causes they like.

But all that assumes some idealised fine public servants, who have laboured to generate judicious but penetrating insights. Wise men and women whose words shed light in dark corners, enrich our understanding, and could – if only we listened – help resolve some of these intractable challenges that face any modern government and society.

And then there are the Makhlouf speeches. I written about several of them here (eg here, here, here and here). They often read fluently enough at a first glance, before quickly turning to dust under any close examination.

Last week’s effort wasn’t that much better. At least the Secretary to the Treasury was talking about productivity – something I noted was strangely totally absent from The Treasury’s Briefing to the Incoming Minister last year – but he didn’t have a credible or robust story to tell.

The speech was delivered in Queenstown, so Makhlouf began with some local colour – some good, some bad. Among the less positive indicators was

The mean income for people in the Queenstown-Lakes District in 2017 was about $51,000 compared with the national mean of $59,000. With low incomes but the highest average weekly rental cost in the country and an average house value of more than $1.1 million, the housing affordability problem in Queenstown is in the same league as Auckland.

To which the Secretary’s response was

In response, the Government’s Housing Infrastructure Fund is contributing $76 million in 10-year interest-free loans to support an increase in Queenstown’s housing supply.

So the Secretary to the Treasury now thinks interest-free loans by the government are sensible economic policy? This isn’t supposed to be some local MP’s party-political broadcast, but the Secretary to the Treasury, guardian of the public purse.

The Secretary then touches on the failure that is New Zealand productivity growth, recognising that we’ve done poorly (while taking no responsibility as head of the leading economic advice agency). But there is nothing new, and litttle specific.

There are various unsupported assertions (emphasis added)

We know that our productivity levels stem from a number of factors including weak international connections, the small size of domestic markets, low investment in knowledge-based capital and weaknesses in the allocation of labour.

as if symptoms (in some cases arguable ones) are causes, and then a string of platitudes

It remains a fundamental truth that successful economies need, among other things, a stable and sustainable macroeconomic framework, sound monetary policy and a prudent fiscal policy. It remains true that a well-regulated financial system matters, that properly functioning markets matter, that price signals matter and that incentives matter. And, perhaps most important of all, it remains true that productivity matters.

No doubt largely true (I’d quibble about the “well-regulated” financial system, substituting “sound and stable) but New Zealand has had these features for decades, and we are just slowly drifting further behind.

The second half of the speech builds off this paragraph

The Treasury believes there are a number of factors that always matter for productivity: our human capital, the management of our resources, our international connections, the dynamism of our markets and the effectiveness of our rule-making. I want to say a few words about each of these. To improve our productivity we will have to be more effective in their utilisation and the interactions between them.

First, skills matter. As if we didn’t know.

There seemed to be two areas of focus

In the Treasury’s view, to help achieve this there should be an emphasis on attainment of cognitive and non-cognitive foundational skills and social skills that are transferable and support life-long learning, as well as greater rates of progression to higher tertiary qualifications.

But I’m not sure what the first half of the sentence really means (Great Books programmes for all, to teach people to think and write?) and the second half looks like a bid for even more tertiary education, when there is little sign that the massive public and private spend on tertiary education in recent decades has been reflected in commensurate increases in productivity or earnings. And none of this seems embedded in some comparative analysis about whether, and to what extent, New Zealand is doing worse than other advanced countries.

The other specific was slightly surprising

I should also add that we will need to look carefully at whether our social welfare system – which was initially set up to help people make transitions from one job to another in what was expected to be a similar trade – is optimal for the changing world ahead of us.

I presume he means the bits of the system around the unemployment benefit (or whatever it is now called) since most of the social welfare system wasn’t set up to support employment transitions at all (age pensions, widows’ pensions, DPB, sickness and invalid pensions etc), but as his current political masters have, as a matter of policy, been weakening the sanctions in the welfare system that were, supposedly, designed to assist such transitions, I’m left a bit puzzled as to what the Secretary means by this cryptic observation. Perhaps he is toying with notions of a Universal Basic Income (but, charitably, I’ll assume not)?

Then there is a section on resources. Some of it seems sensible enough, including around water use rights. I’m right with him when he favours congestion charging. But I’m left wondering whether he or The Treasury really believes that either is a significant part of the story explaining our severe relative underperformance. I don’t.

And lets just say that I rather doubt the robustness of The Treasury’s analytical framework when the Secretary includes these sentences.

The Emissions Trading Scheme is a good example of a tool that can promote the more productive use of resources. Including agriculture within its scope would provide incentives for investment in R&D or innovation in on-farm practices and improve productivity.

An ETS can, no doubt, be a good mechanism for constraining emissions, and even for doing so in a way which might be economically efficient. But it simply isn’t a way to improve New Zealand’s economywide relative productivity and/or incomes. Impose an impost (perhaps quite justifiably) on firms in a particular industry, and those who survive will have to adapt their production techniques, perhaps even lifting their own firm productivity. But it will also considerably shrink the industry in question, when it is an internationally tradable industry, when efficient alternative technologies don’t yet exist, and when other countries aren’t adopting the intervention The Treasury proposes. All else equal, New Zealanders would be poorer rather than richer if this bit of the Secretary’s prescription was adopted – the government’s own commissioned economic modelling, by NZIER says as much.

Then Makhlouf moves on to “international connections”, one of the ill-defined buzzwords in this debate.

Mostly it is just empty conventional slogans

Improving the flow of people, capital, trade and ideas will help improve productivity. Strong people-to-people relationships build confidence and understanding and promote learning. They help our businesses to identify capabilities that will help them improve their productivity and ultimately compete and succeed in both domestic and global markets.

All of which would have sounded good in 1984, and yet we greatly liberalised immigration, got rid of most tariff barriers, signed up to all manner of trade agreements, and……the productivity gaps are larger than they were, and actual trade (exports and imports as a share of GDP) is smaller than it was. The Secretary is either unaware of these basic facts, or simply chooses to ignore them.

I’m closer to the Secrerary’s position when it comes to foreign investment – where he has to step delicately around the recent legislative choices of his masters – but there is no sign that he has thought hard about why foreign investment here isn’t more attractive or, indeed, why not many New Zealand based firms do much foreign investment themselves.

There is a section on “markets” that I’m going to skip over. I don’t particularly disagree with much in it, but there also isn’t much specific there, and nothing to suggest The Treasury has thought seriously about the connection to sustained New Zealand relative productivity underperformance. Much the same goes for the section on Rules. I’m all in favour of robust policy evaluation – it is a shame it hasn’t been applied to Treasury advice on productivity – and I’m sure there are real opportunities there, but again is there any evidence that things on that score are worse here than in other countries? Perhaps, but if so he doesn’t mention it.

(The dig at the massive taxpayer subsidy to the cattle industry was interesting, and welcome

Speaking of incentives, I find the situation around the eradication of mycoplasma bovis an interesting one. Responsibility for the genesis and subsequent spread of the mycoplasma bovis outbreak sits with the cattle industry. The question is, should the taxpayer compensate those affected, or should the industry pay for the consequences of the industry’s making? We might also ask what incentives are signalled to the industry by these different options.

And yet, how different is it anywhere else? )

There was an odd section on co-operatives, as if it was a matter for governments to decide on the appropriate sort of vehicles through which business activity is undertaken, and one on public sector productivity, which was really no more than a footnote.

And then there was tax reform. Mostly, it was in praise of the New Zealand tax system, including the – highly questionable – claim, that

the New Zealand tax system is much less distortionary than the tax systems of other OECD countries

That might be true, more or less, if we look only across activities in the same time period, but is demonstrably not true once we take account of intertemporal dimensions. Not consuming your income now and delaying until later (ie saving – particularly retirement savings) is much more heavily penalised by the tax system here than in almost any other advanced economy. That is a distortion The Treasury has been consistently reluctant to address or (it seems) even acknowledge.

There is also no recognition of the possible connections between low rates of foreign investment, and low rates of business investment (symptoms he touches on elsewhere) and business tax regime, where (for example) our company tax rate – a key consideration for foreign investors – is now towards the upper end of the OECD range.

And then it was interesting to see that in a speech on productivity, the specific policy proposal that the Secretary devotes most space to (in the entire speech, not just this section) was the call for a capital gains tax.

But there is one area where we stand out as an outlier and which I think needs further attention. The current approach to the treatment of capital income – in particular, capital gains – is highly inconsistent. Some gains are already taxed but others are not. The result is therefore something of a patchwork, the results of which can be unfair, regressive and distortionary. A more consistent approach to the taxation of capital gains would increase the fairness of the tax system, and reduce distortions by levelling the playing field between different types of investments.

For these reasons, the Treasury has long believed there is a real case to extend the taxation of capital income. I recognise that this would come with its own risks, and give rise to higher compliance and administration costs. But there are interventions available to address these risks. The extent to which the impacts are realised – whether positive or negative – will depend significantly on the design of policy.

Some readers will support a capital gains tax. I don’t particularly, partly because a real-world one (ie the sort many other countries actually have) just introduces a whole new set of distortions, but does anyone seriously believe that a capital gains tax – whatever the case on “fairness” grounds – is going to make any material difference to economywide productivity? And if there is such a case, not even the Secretary to the Treasury advances it.

The Secretary, of course, has to keep on side with his masters, so we read this

I should also add that there are many things being done to address points I’ve just raised. The government has been working on education and training, welfare reform, tax reform and trade relations, to name just a few of the actions happening.

If the Secretary to the Treasury really believes that the goverment’s policy agenda – at least as revealed to the public – is going to make a helpful difference in reversing the decades of relative productivity decline, he must surely be the only such person. But I guess that if he is going to speak in public, he has to say such stuff.

In the final paragraph of the speech there is material for both a brickbat and a rare bouquet.

The brickbat?

And the ‘we’ means everyone: businesses, workers and government seizing the opportunities offered by being part of, and closer to, the fastest-growing region in the world.

Which is simply nonsense of course, New Zealand is incredibly remote from Asia, or from any other major part of the world economy. We might be a little less far from some of Asia than we are from Europe or much of North America, but we aren’t even a little close to the major bits of Asia, let alone “part of” it (whatever that means). When the Seceretary was at home in London he was closer to Mumbai or Bangalore or Delhi than he is in Wellington. He was actually a little closer to Seoul or Shanghai too.

It is a fundamentally unserious “analysis”.

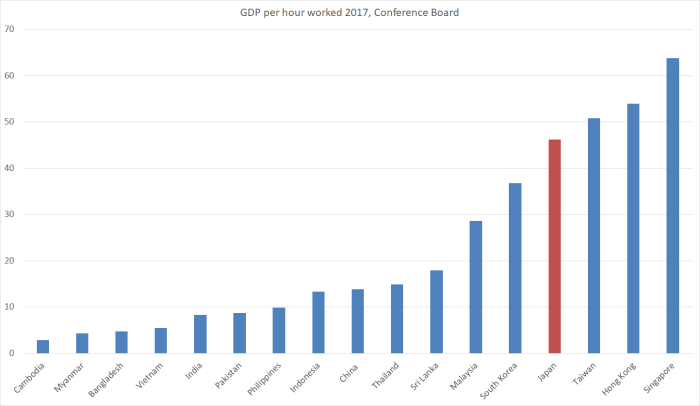

But there is a bouquet. Early in his speech, the Secretary was rather downplaying the failure of New Zealand policy, and policy advisers, in observing that labour productivity is “now about 20 per cent below the OECD average” – an average considerably lowered by the entry to the OECD of a large group of emerging countries (especially in eastern and central Europe), all of whom throughout modern New Zealand history were considerably poorer and less productive than New Zealand.

But the Secretary ends

Recent research indicates that if New Zealand’s productivity caught up with the better-performing countries in the OECD, our incomes would be 50-60% higher.

It doesn’t take much “research” – a quick download of an OECD table does the job. Here is an extract of that table I did recently for a paper I’ve been writing on these issues.

| GDP per hour worked | ||||

| USD, constant prices, 2010 PPPs | ||||

| 1970 | 1990 | 2017 | ||

| New Zealand | 21.4 | 28.6 | 37.2 | |

| Netherlands | 27.4 | 47.5 | 62.3 | |

| Belgium | 25.0 | 46.7 | 64.6 | |

| France | 21.7 | 43.3 | 59.5 | |

| Denmark | 25.1 | 44.8 | 64.1 | |

| Germany | 22.3 | 40.7 | 60.4 | |

| United States | 31.1 | 42.1 | 63.3 | |

| Median of six | 25.1 | 44.1 | 62.8 | |

| NZ as per cent of median | 85.4 | 64.9 | 59.2 | |

| Source: OECD | ||||

If anything, a 50-60 per cent lift is an understatement: it would take a two-thirds lift in New Zealand productivity to match the average of this group of high-productivity countries. And such a lift could be expected to be mirrored in commensurately higher living standards,

But it is great to see the stark magnitude of our failure – and “failure” is the only honest word for it – as the note the Secretary ends on, even if there isn’t much sign the institution he leads has any serious answers.

And, to be entirely fair, the Governor of the Reserve Bank’s own speech last week makes the Secretary’s effort look like a fine piece of public sector analysis and communications by comparison. I will write about the Governor’s extraordinary speech tomorrow.

The peaks on this measure happen when population growth is at its cyclical troughs – unsurprisingly, since the normal base level of replacement and improvement work is still going on.

The peaks on this measure happen when population growth is at its cyclical troughs – unsurprisingly, since the normal base level of replacement and improvement work is still going on.