It is the season for books and articles reflecting on financial crises of a decade or so ago, the aftermath, and whatever risks might – or might not – be building today. The collapse of Lehmans – and the wise decision of the US authorities not to bail it out – was 10 years ago this month, and although the US crisis had been underway for at least by a year by then, the Lehmans moment seems set to take a place in historical memory around the Great Recession rather parallel to the sharp falls in US share prices in October 1929 (the ‘Wall St crash’) and the Great Depression. Not in any real sense the cause of what followed, but the emblematic moment in public consciousness nonetheless.

I’ve just been reading the big new book, Crashed: How a decade of financial crises changed the world, by esteemed economic historian Adam Tooze. I might come back to it in a separate post, but for now would simply caution people that it is less good than his earlier books (around the Nazi economy, and the economic history of the West after World War One running into the Great Depression) had led me to hope.

But on a smaller scale, I picked up the Listener the other day and noticed on the front cover ’10 years after the GFC, former Reserve Bank governor Alan Bollard warns of new risks’. Conveniently, I see that the article is freely available online. The sub-heading tantalises potential readers

Former New Zealand Reserve Bank governor Alan Bollard warns that, although lessons were learnt from the global financial crisis, new risks have emerged that could trigger a repeat contagion..

Alan Bollard writes well, and often quite interestingly. Extremely unusually (and in my view quite inappropriately), he actually published a book on his perceptions of the previous crisis in 2010, while still very fully-employed as Governor, a senior public servant. There were quite severe limitations as to who, or what, he could be critical of (as I was reminded last night rereading my diaries of some crisis events I was closely involved in, and the Bollard published perspective on those events). The Bank’s early reluctance to take seriously the emerging issues, as they might impinge on New Zealand, is not, for example, something you find documented in the book.

He must be in a somewhat similarly difficult position now. He is Executive Director of the APEC secretariat, that grouping of Asian and Pacific (loosely defined) countries and territories, that includes China, Russia, the United States, Indonesia and so on. I dare say Xi Jinping and Donald Trump won’t be watching nervously to see what Alan Bollard is saying, but the Executive Director knows that there are quite severe limits to what public servants can say while in office.

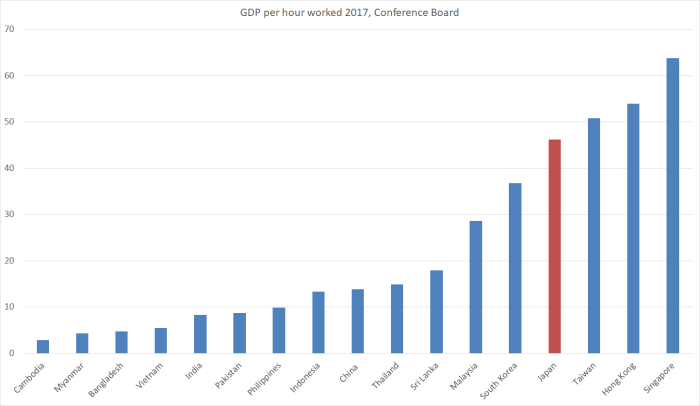

And, thus, much of the Listener article is a bit of a, perhaps slightly rose-tinted, rehash of some of the policy responses here and abroad (I will come back to deposit guarantee schemes on the tenth anniversary, next month). There is some loose descriptive stuff on various developments in parts of the APEC region. There was the suggestion that some countries (actually “much of the region”) in Asia is “anxiously worrying” about whether they could face a Japan-like low productivity future but to me, Japan still looks pretty attractive by regional standards.

(New Zealand, for example, is at 42.)

In fact, I looked in vain for the promised analysis or description of the “new risks” that might “trigger a repeat contagion”. Perhaps that was never Bollard’s intent, but the Listener had to attract readers to a fairly tame advertorial for APEC somehow. The most we get is

We need to remember that the global financial crisis was originally triggered by a building bubble, and that is still on the minds of regulators throughout the region.

and

Meantime, we are very worried about the likely effects of the growing trade wars. It is too early to judge, but the stakes are high – trade growth has been the big driver behind the immense improvement in living standards through the Asia-Pacific region ……We are now on the alert for signs that these trade frictions could weaken exchange rates, hurt commodity prices, hit stock markets or cause financial volatility, against an unusual background of tightening monetary policy and loose fiscal policy in the US.

But then what more could a serving diplomat, not hired to be a high-profile problem solver (unlike, say, the head of the IMF) really say?

And it all ends advertorial style

As a big trader, New Zealand has always been susceptible to these tensions. But one international platform where they play out is coming closer: in just over two years, New Zealand will commence its year of hosting Apec. The organisation is a voluntary, consensus-driven one, where for 30 years we have promoted regional economic ties and tried out new ideas for trade and investment. As the upcoming chair of Apec, New Zealand will have to contend with continuing antiglobalisation pressures, big-economy tensions, climate-change damage and financial risks in the region. It sounds daunting, but there are many positives: We have learnt some of the lessons of the global financial crisis; banking regulation is tougher; banking chiefs are more cautious; economic demand is still growing; and the Asia-Pacific region is tied ever more closely by its trade flows.

It could have been a paragraph from a speech by one of his political masters. I guess one wouldn’t know that one of his members (the People’s Republic of China) poses an increasing political and military threat to another (Taiwan) or – closer to his own territory – that few major economies have very much effective macroeconomic firepower at all when the next crisis or severe recession hits. And really nothing at all about financial sector risks. His final sentence – “September 2018 should be a month much better than September 2008” – is almost certainly true (at least outside places like Turkey and Argentina) but not really much consolation to anyone.

In his column in the Dominion-Post this morning, Hamish Rutherford touches a theme of various recent posts here: the limited macro capacity of many countries. He rightly highlights how low global interest rates are, and the much higher levels of government debt in many countries.

To make matters worse, interest rates are already so low that some economists are speculating that if the Reserve Bank was to respond to a slowdown by slashing interest rates, in a bid to stimulate the economy, it may find that little of the money finds its way to households.

Debt levels among the world’s leading economies are, by and large, far higher than they were a decade ago. In the US, as well as threatening to kick off a global trade war, President Donald Trump’s administration is running the kind of deficit that would be wise in a recession, but at the late stage of a long economic growth cycle appears reckless.

But there was one point I wanted to take issue on. He argues

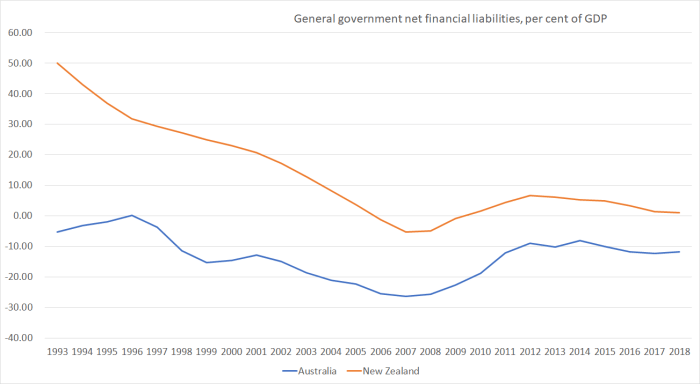

Back in 2008, New Zealand benefited from its largest trading partner, Australia, avoiding recession and having almost no debt. This time Australia’s debt is climbing and there are doubts as to whether Canberra will have the discipline to return to a surplus, as the political state becomes more populist.

I don’t think that is true about either the past or the present. We didn’t get any great benefit out of Australia’s fiscal stimulus in 2008/09, largely because if fiscal stimulus hadn’t been used, the Reserve Bank of Australia would probably have cut their official interest rates further. Fiscal policy can be potent when interest rates have the effective lower limit, but they hadn’t in Australia (or New Zealand). More importantly, and for all the New Zealand eagerness to bag Australian politics and policies, here is the OECD’s series of the net financial liabilities of the general government (federal, state, and local) for Australia and New Zealand, expressed as a share of GDP.

Australia’s net public debt has been consistently below that of New Zealand for the entire 25 years for which the OECD has the data for both countries. The gap is a little smaller now than it was a decade ago, and (on a flow basis) the New Zealand budget is in surplus but Australia’s isn’t. But if there is a desire to use large scale fiscal stimulus in the next serious downturn, debt levels themselves aren’t likely to be some technical or market constraint in New Zealand, and even less likely in (less indebted) Australia.

And finally in this somewhat discursive post, a chart I saw yesterday from the BIS.

A story one sometimes hears is that low interest rates have driven asset prices sky-high setting the scene for the next nasty crisis. Even if there are elements of possible truth in such a story, the story itself mostly fails to stop to ask about the structural reasons why interest rates might be so low. All else equal, had interest rates been higher asset prices probably would have been lower – and CPI inflation would have undershot targets even further. But as this particular chart illustrates, across the advanced economies as a whole real house prices now are much same as they were at the start of 2008. That isn’t true in New Zealand (or Australia for that matter). Interestingly, even in the emerging markets – centre of current market unease – real house prices are still not 15 per cent higher than they were at the start of 2008, when interest rates generally were so much higher.

But then only rarely is the next major economic downturn or financial crises stemming from quite the same set of financial risks as the last one.

Fake

“remember the global financial crisis was originally triggered by a building bubble, and that is still on the minds of regulators throughout the region”

To believe that you have to believe that the events leading up to the GFC were synchronous whereas in reality they are asynchronous and one begets the next

Prior to the GFC the US governments were promoting cheap affordable housing for the peons. Freddie Mac, Freddie Mae and so on which was pushing the peons into liar loans and so on. All well and good. But, what happened in the midst of all this was the price of a US gallon of petrol rose from $2 per gallon to $4 per gallon

Suddenly the poor plebs living from pay-day to pay-day driving 5 litre SUV’s 50 miles to work had a choice – pay their mortgages and stop working or keep working and stop paying their mortgages. That’s what happened – they stopped paying their mortgages – defaulted and sent the keys to their homes back to the banks as jingle mail – and the preceding build up of CDO’s https://www.thebalance.com/role-of-derivatives-in-creating-mortgage-crisis-3970477

That’s what triggered it – when oil hit $147 per barrel – that was the start

I’m not convinced the 2008 GFC is complete – it’s only halfway through

LikeLike

…..a handy shortcut re the book:

http://www.lse.ac.uk/lse-player?id=4501

LikeLike

Real interest rates that people and businesses actually pay in NZ are not low. Business overdraft interest rates are still around 7% to 8% and residential around 5% to 6% compared to the OCR of 1.75%. The reason is that even though the RBNZ shows a public face of easing it is at the same time tightening banks ability to lend through Bank licensing covenants and also a high 35% equity LVR on property investment lending. Credit is being squeezed which puts upward pressure on real interest rates even as the OCR is falling.

LikeLike