Four months ago, in the December Monetary Policy Statement the Reserve Bank indicated that they believed that the surge in immigration over the last few years had eased capacity pressures and contributed to a reduction in inflation. That was a view quite contrary to their own past research, or to the historical consensus of New Zealand economists that – whatever the long-term economic effects of immigration – in the short-term the demand effects outweighed the supply effects.

The Bank might be right, but they provided no analysis or background material in support of their change of view. So I asked for the background material. Almost two months ago they refused to release any of that material. I have appealed that decision to the Ombudsman, and was pleased have an indication from the Ombudsman’s office yesterday that they are about to investigate it (less than two months after the complaint was lodged, suggesting that the new Ombudsman really is making progress). At the time, the Bank indicated that it had other material that might shed light on the Bank’s view on immigration that was being worked on with a view to later publication.

Two such papers were released finally yesterday, accompanying an on-the-record speech by the Bank’s Deputy Governor, Geoff Bascand, “Inflation pressures through the lens of the labour market”. It was a little curious to have a speech on such a major economic topic given by someone who is, in effect, the Bank’s chief operating officer. Bascand has responsibility for things like notes and coins, property and security, HR, IT, and NZ Clear (and chairs the Bank’s ill-governed and troubled superannuation scheme). But, of course, he does have a background in economics and, having taken a step downwards in becoming Deputy Governor, is generally assumed to see himself in the running to be the next Governor, perhaps as early as next September.

It was a curious speech. The accompanying press release – designed no doubt to highlight the key messages – begins with the claim that “rapid growth in the workforce…has helped create strong economic growth over the past four years”. GDP growth in the last four year has averaged 2.85 per cent per annum. I know it is an age of diminished expectations, but if that is “strong”, I think my dictionary needs updating.

Despite the (alleged) biggest immigration surge in 100 years, neither average nor peak growth got anywhere near the levels reached in the previous couple of cycles.

Between the speech, press release, and the Analytical Notes, the Bank is clearly going to great efforts to stress the line that this is “the largest recorded surge in migration in 100 years”. In particular, they want to have us believe that this event is bigger than the surge of immigration over 2002/03. But they know that is simply not true. In some places they are more careful, and only claim that it is the largest net inflow of (self-recorded) permanent and long-term migrants, but even then they know that those numbers do not always represent very well the actual net inflow of people (total, or even just those who stay for more than a year – the PLT vs visitor threshold).

Why do I make this point so strongly? Because when I was at the Bank, and with the full knowledge of senior Bank managers, in 2014 I prompted Statistics New Zealand to produce Alternative methods for measuring permanent and long-term migration. The issue arose from something like this chart

It illustrates that over 2002 and 2003 in particular there had been a huge divergence between the self-reported PLT numbers and the (accurate) count of the overall net flow of people into New Zealand. Many more people (net) came in – all needing a roof over their head – than had said they were intending to stay for a year or more.

Statistics New Zealand had done nice work, using several different methods, to estimate what actually happened (eg did the person actually leave the country again, or come back, within 12 months, even though they said they were PLT). And they produced this chart.

Net PLT inflows in 2002 and 2003 proved, using these techniques, to be 50 per cent higher than the initial monthly data had suggested. New Zealand’s population was around 4 million in 2003, and is around 4.6 million now. Even just focusing on PLT numbers, the population surge resulting from immigration was just as large then as it has been over the last year or two.

And yet there is not a single mention of this work, or this issue, in any of the material that the Reserve Bank put out yesterday. It is unfortunate that (a) the estimates go back only to 2000, (b) they are only annual (c) that SNZ has no money to do this work on an ongoing basis, and (d) that inevitably these better estimates have a 12 month lag on them. But it is simply materially better information about immigration over the last 15 years, produced by our national statistical agency, than is in the monthly data the Bank makes so much of.

The total (net) arrivals data are noisy – eg changing timing of school holidays, and/or major events such as Lions tours or the Rugby World Cup can add a lot of noise – but here are the PLT and total net arrivals series (rolling annual totals) for the last 20 years or so.

There isn’t a lot of noise around 2002/03, or in fact around the current period. And the patterns over time are not necessarily typically different. But there were simply somewhat more people coming into New Zealand (net) in 2002/03 than there have been in the last couple of years, and as percentage of the population the difference is even larger. The immigration surge in the last couple of years has been big, but 2002/03 was simply a bigger event. Here is the same chart shown as percentages of the population.

The Reserve Bank knows all about this. It is strange, almost inexcusable, that it is not even mentioned. Not explicitly recognizing the issue undermines the confidence we might have in the rest of their analysis and interpretation.

What of their two Analytical Notes? The first, by Tugrul Vehbi, a recent recruit from Treasury (his bio says he joined in Dec 2015, so clearly this wasn’t analysis that fed into the December MPS view) tries to look at “The macroeconomic impact of the age composition of migration”. Using data for only the period since 1994 (so in effect only about 2.5 cycles) he constructs a small model to look at how several key economic variables respond to net migration by, on the one hand, those aged 17 to 29, and on the other hand those aged 30 to 49. It isn’t entirely clear why he divides the groups where he does (or, hence, whether any results are sensitive to slightly different classifications). Loosely, I suppose he is distinguishing between the “young” (but independent) and the “not young”. For the same sized shock, he produces results which – with wide error bounds – suggest that the net demand effects of increase in immigration of 17 to 29 year olds are less than those for the 30 to 49 year olds. In the current cycle, there has been a disproportionately large increase in the net inflow of 17 to 29 year olds.

I have several problems with the analysis.

The first point relates to the earlier discussion, and the apparent material underestimation of the PLT inflow (in the monthly data the Bank uses) over 2002/03. It is generally recognized that much of that issue related to students (typically in Vehbi’s younger age group). As this chart shows, drawing from MBIE visa approvals data, there was a huge increase in the student visa numbers granted over that period. Since his estimation effectively uses only a fairly short run of data, only 2.5 of so cycles, mis-measurement in the biggest of those cycles is a potentially severe problem.

Related to the small sample problem, the (one standard deviation) error bounds on his estimates are sufficiently large (see Figure 3 in the paper) that we can’t say with any confidence that the effects are different between the two age groups, even if all the immigration data are correctly measured. Moreover, Vehbi runs an useful alternative estimation leaving out the last couple of years data, and although he describes the effects as “qualitatively similar” in the two runs (and no error bounds are shown for the alternative), for at least some of his series (residential investment and consumption) the quantitative effects are quite materially different.

But perhaps a more important effect still is that he simply looks at the two ages ranges 17 to 29, and 30 to 49. In most cases, we can probably think of the actions of 17-29 year olds as being independent of other age groups (eg they won’t be coming with children – or parents for that matter). The same can’t be said of people in the 30 to 49 age group, many of whom will be bringing children with them. You can see that in this chart, going all the way back to the 1970s, and simply using the PLT data (with all its weaknesses, as discussed above)

All the main age range groups cycle together to some extent, but the 17-29 year old group behaves materially different from the 0 to 16 and 30 to 49 age group in particular. In the early decades, most of the net migration outflow was young people, and right now much of the net inflow is. But the key point is that when the 30-40 age group numbers increases there is almost always a very similar sort of increase in the inflow of 0 to 16 year olds (as one would expect, children mostly come with parents). But if you test how the economy responded when 17-29 year old inflows increases and compare that with a same sized shock to the 30 to 49 age group, of course you should see large net pressures on resources from the older age group, because you are ignoring the fact that these people bring with them a lot more people (the kids). Kids don’t add anything much to labour supply, but they need housing, schooling and the other basic necessities of life. The model might be better rerun comparing, say, the impact of a shock in the 17 to 29 year old inflows with the impact of a shock to the other age groups taken together (or even just the 0 to 16, and 30 to 49 age groups together.

It is (always) good to have the Analytical Note out. But the measurement problems around PLT numbers (which SNZ themselves recognize), the short sample, and the failure to allow for kids who accompany the older people means we can’t really have much confidence in the results at all.

Is it credible that the young (17 to 29, say) migrants could have a materially different impact on net capacity pressures than other age groups? In principle, it is possible. Take a scenario in which all the young were working 60 hours a work, living in extremely cramped conditions, and remitting most of their earnings home. In that scenario one would certainly expect quite weak pressures (perhaps even negative) on inflation. Perhaps that describes illegal Latin Americans in the US, or even the stereotyped Polish plumber in the UK?

But about as many of our young PLT migrants arrive as students, as come on work or residence visas (and many more shorter-term arrivals, all consuming and not able to work legally, are students). The Reserve Bank makes quite a bit of the change in policy allowing students limited work rights in New Zealand, but even under that policy most students only have a legal right to work 20 hours a week, and then only under certain conditions. But even if all the students could work, it is still only 20 hours week – roughly half what a typical full-time worker will do (or the same as a couple raising kids, in which one parent works fulltime and another is at home). And the students still have to live, pay tuition etc, all of which puts pressure on New Zealand resources (export earnings, so generally welcome, but demand nonetheless).

Perhaps the fact that our current migrants are disproportionately quite young does result in less net demand pressure per migrant. (And it is quite plausible that students put a bit less pressure on resources than they once did.) But on the information presented so far, at best it is “case not proven”.

The other new Analytical Note is “Why drivers of migration matter for the labour market”. One of the authors is Chris McDonald, author of a 2013 piece illustrating the way the net migration inflows to New Zealand have typically added materially to inflation pressure.

In the new paper, the authors set up a very small model in which they try to distinguish between net migration flows that result from fluctuations in the strength of the Australian labour market from those arising from other factors (eg changes in New Zealand immigration policy). In their model, the latter sorts of flows have the conventional expected effect on domestic demand and inflation pressures – higher migration inflows, for example, lower the unemployment rate. But

a higher Australian unemployment rate that generates positive net immigration [to New Zealand] typically coincides with a higher New Zealand unemployment rate.

But – as the authors acknowledge as a possibility in their final paragraph – mostly what this is telling us is that New Zealand and Australian economic cycles have tended to be quite correlated and that Australia affects New Zealand through a variety of channels. Australia is our largest trading partner (and largest source of FDI) so that when the Australian economy is weak (proxied in this model by an “unemployment gap”) economic activity here is also, to some extent, adversely affected. As I’ve noted here previously, it has never been clear what the net effects of an Australian slowdown on New Zealand are: we face some losses of demand in our direct trade (and probably investment, if Australian firms rein in their investment spending), but on the other hand when Australia slows we get fewer New Zealanders (net) going to Australia. That adds to demand here. The net effect is clearly different from, say, the net effect of an exogenous immigration policy change (say targeting 20000 more permanent residents from other countries), but it isn’t necessarily that the effects of the migrants themselves is any different. When they get here, they still need houses, schools, shops, roads, factories, and they can supply some labour. Capital stock requirements are typically more than a year’s labour, so generally short-term demand effects from the migration choice typically exceed supply effects. It isn’t clear to me that McDonald and Armstrong have really (even attempted) to show that those effects are different across the two classes of migrants. Of course, if all they are saying is that there are offsetting shocks – weakness in Australia’s economy offsets the demand effects of the resulting migration choices, then I can happily agree.

In the end there is little reason still to depart from the longstanding consensus of New Zealand economists, going back many decades, and of the Reserve Bank’s own past analysis (formal and otherwise) over more recent decades, that net migration inflows put more pressure on demand than on supply in the short-term. But if major trading partners are weak at the same time, an upsurge in net immigration won’t typically be a basis for tightening monetary policy and worrying about inflation.

There is a more material on other topics in Bascand’s speech, and another whole Analytical Note on other labour market issues which I haven’t read yet. I might come back to them next week.

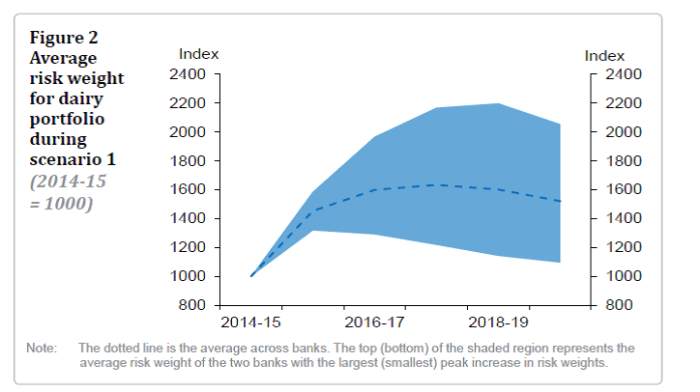

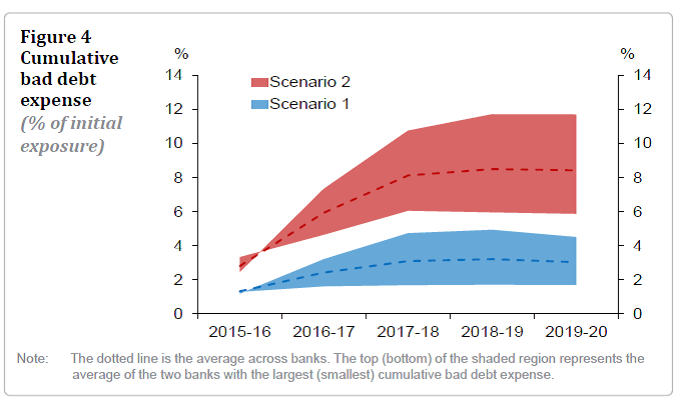

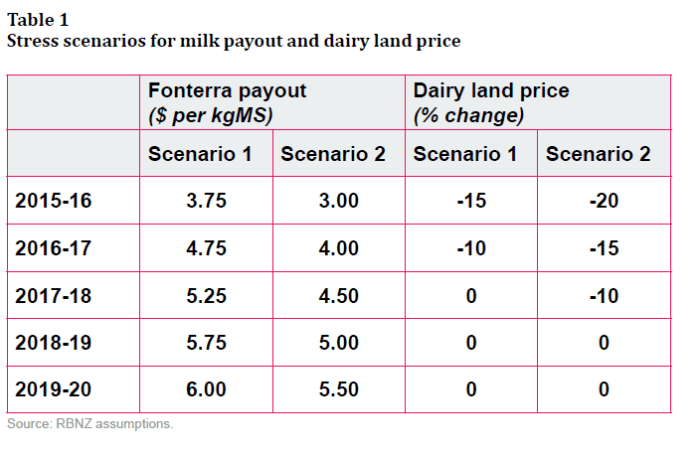

I’m largely going to ignore Scenario 1 from here on. As the long-term average real milk price is probably only around the assumed 2017/18 level, Scenario 1 doesn’t represent much of a stress test at all. The banks and the industry would have to be have been very rickety for a scenario like that to have presented a banking system problem. I think the Reserve Bank should also have discounted these results, rather than highlighting them in their press release.

I’m largely going to ignore Scenario 1 from here on. As the long-term average real milk price is probably only around the assumed 2017/18 level, Scenario 1 doesn’t represent much of a stress test at all. The banks and the industry would have to be have been very rickety for a scenario like that to have presented a banking system problem. I think the Reserve Bank should also have discounted these results, rather than highlighting them in their press release. In a single year, dairy land prices fell by more than 30 per cent – and that was a severe, but very short-lived, fall in milk prices, and a rise in dairy non-performing loans that was still moderate compared to what we see in Scenario 2 in the current stress test. Perhaps deliberately, the Reserve Bank’s stress test does not seem to have taken account of a second round of selling (forced or voluntary), and the potential for that to drive land prices well below what might be a longer-term equilibrium level. Overshoots routinely happen in such markets, where liquidity is thin to non-existent, uncertainty is rampant, and potential buyers are few. As

In a single year, dairy land prices fell by more than 30 per cent – and that was a severe, but very short-lived, fall in milk prices, and a rise in dairy non-performing loans that was still moderate compared to what we see in Scenario 2 in the current stress test. Perhaps deliberately, the Reserve Bank’s stress test does not seem to have taken account of a second round of selling (forced or voluntary), and the potential for that to drive land prices well below what might be a longer-term equilibrium level. Overshoots routinely happen in such markets, where liquidity is thin to non-existent, uncertainty is rampant, and potential buyers are few. As