I’ve never known much about Romania. There was Olivia Manning’s Balkan Trilogy, Richard Wurmbrand was one of the Christian heroes of my youth, and there were the bleak last years of Ceaucescu culminating in a firing squad on Christmas Day 1989. But that was about it. I had occasionally used it as an example of a rare country that had managed less growth in per capita income than New Zealand over the 20th century. The rule of law, private property, strong institutions and freedom have quite a lot to be said for them.

And then the other day, an eastern European immigrant to New Zealand was commenting here. I was curious why an east European had chosen New Zealand, as several of the eastern European economies seemed to have pretty good prospects, perhaps even better than those of New Zealand. I had in mind especially the Czech Republic, Slovenia and Slovakia (each now with GDP per hour worked very similar to that in New Zealand). In our subsequent exchange, it turned out that he was Romanian.

And that prompted me to go and check out some data on Romania. It was a pretty sobering story, for a New Zealander.

Romania had its ups and downs in the 20th century. Just prior to World War One (when we were one of handful of richest countries in the world) Romania was doing well. GDP per capita is estimated to have been 75 per cent of that of, say, Norway. They did really badly for the following 30 years, and then – on these measures – quite well economically for the first few communist decades (large scale industrialisation etc). As with many of the eastern bloc countries, things worsened again for them in the 1980s. Older readers may remember accounts of the “austerity policy” in which everything – particularly citizen living standards – was subordinated to repaying the government’s foreign debt.

Things actually got quite a lot worse for Romania (at least in bottom line economic numbers, even if they were free), as for many of the former eastern bloc countries, in the years immediately after end of communist rule (so many distortions to unwind, so many governance problems etc). In Romania’s case things finally bottomed out – at least relative to New Zealand – in 2000.

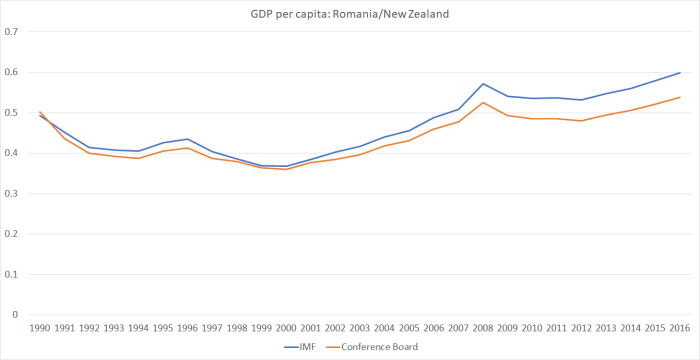

Absolute levels comparisons between Romania and New Zealand are a bit fraught. Romania isn’t in the OECD, and while they are in the EU we aren’t. Here are ratios of Romania’s GDP per capita, in purchasing power parity terms, relative to New Zealand since 1990 from (a) the IMF World Economic Outlook database, and (b) the Conference Board Total Economy database.

Those of you who want to be relatively more upbeat on the New Zealand story might choose to emphasise the Conference Board number, and to note that – even after ending decades of communism – on that measure Romania now isn’t much higher relative to New Zealand than it was in 1990. Personally from all the accounts I’ve seen, I’m more than a little sceptical that Romania’s real living standards in 1990 were in fact half those of New Zealand. Things are better measured now.

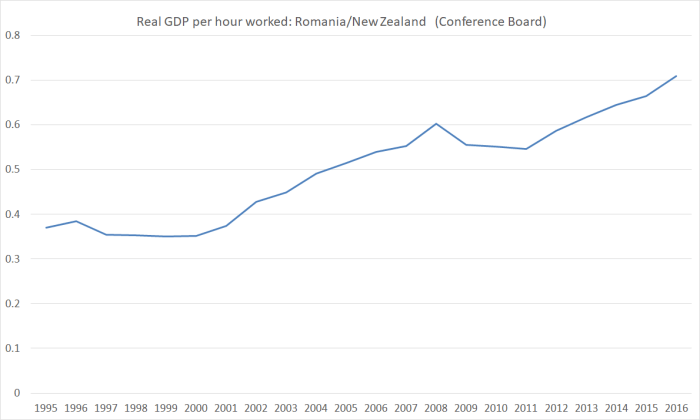

But here is the Conference Board’s real GDP per hour worked series (Romania relative to New Zealand). The Romanian data only go back to 1995, and these days Romanian statistics are part of Eurostat (ie they won’t be perfect, but I’m not sure there is more reason to doubt statistics for them than for us).

In absolute terms it isn’t such a stunning achievement – since New Zealand productivity growth has lagged that of most other advanced countries over this period – but………..one of the once-richest countries of the world is on course for having Romania, almost a byword in instability, repression etc for so many decades, catch us up. It would take a while if current trends continue. But not that long. Simply extrapolating the relative performance of just the last decade (and they had a very nasty recession in 2008/09 during that time) about another 20 years.

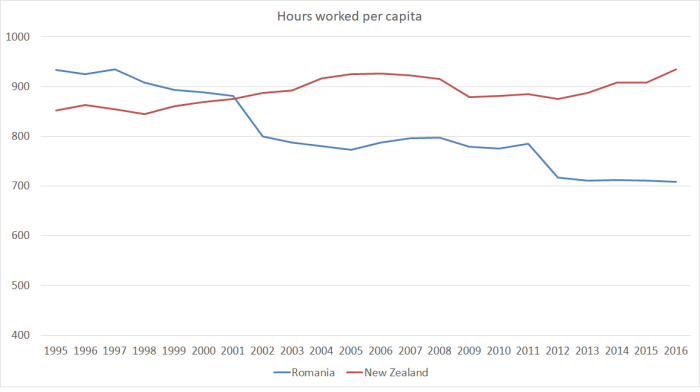

So how we do maintain a big lead in GDP per capita? Simply by having more people work more hours. Here is hours worked per capita (ie per man, woman, and child of all ages).

The next time you hear Steven Joyce, or some other minister or business cheerleader, boast that we have more people working than most countries, do try to remember that labour is a cost (to individuals, who would often do other stuff instead if they could) and that the Stakhanovite cult – extolling the virtues of tireless labour – was a feature of the communist system, not ours.

Of course, if people do want to work and can’t, then there is a problem. We measure that through the unemployment statistics. Romania’s unemployment rate is a bit higher than New Zealand, but at 5.5 per cent the difference is pretty small. We still do a lot things better than Romania: we score top of the Transparency International rankings, while Romania is 57th. We top the World Bank’s ease of doing business index, and they are 36th (not bad at all given where they came from, but a long way off us). But look at the bottom line growth and productivity performances.

Of course, sometimes what you find in countries with a run of impressive-looking fast growth is that:

- it is built on big government deficits, or

- big ill-founded private credit booms, reflected in

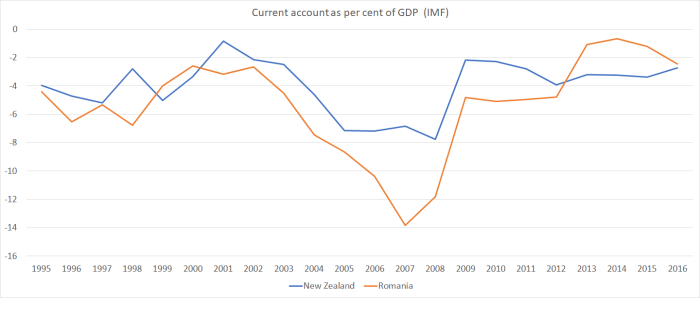

- big current account deficits, and

- appreciating real exchange rates, with an economy increasingly skewed towards construction and domestic demand.

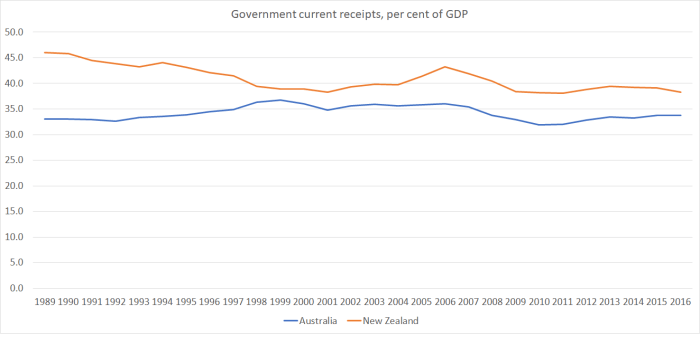

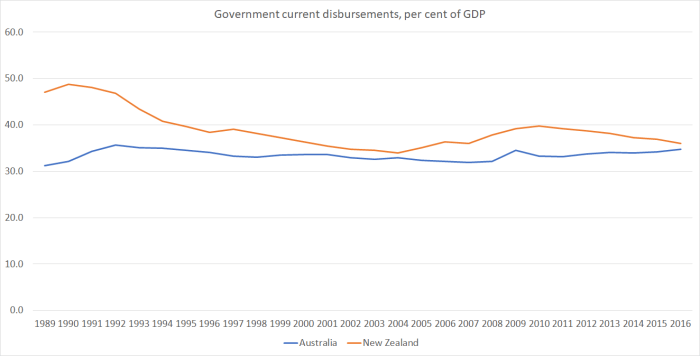

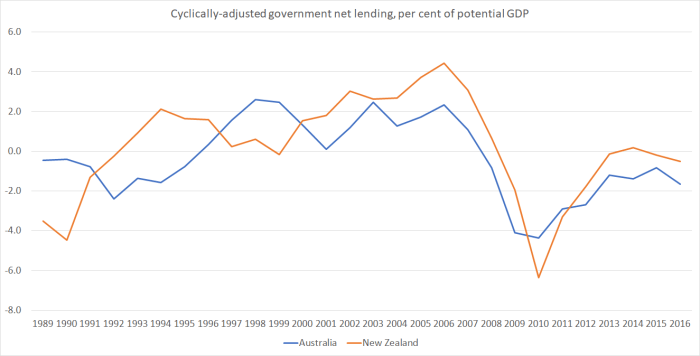

Our government finances are in better shape than theirs. The Romanian government (on IMF numbers) has a deficit of about 2 per cent of GDP, while we have a small surplus. Gross government debt in New Zealand is about 30 per cent of GDP, and in Romania it is about 40 per cent. But even that is pretty low by advanced country standards. And for my friends who like to emphasise size of government, (still on IMF numbers) both revenue and expenditure as a share of GDP are a bit smaller in Romania than in New Zealand.

Romanian private credit was very rapid, and looked rather risky, in the years leading up to 2008. But not now. There is a chart at the link, and overall domestic credit growth has been running at under 5 per cent per annum for the last few years.

Reflecting the pre-crisis boom in private credit, the Romanian current account deficit widened sharply. But these days, deficits in Romania are similar to the modest ones we currently have in New Zealand.

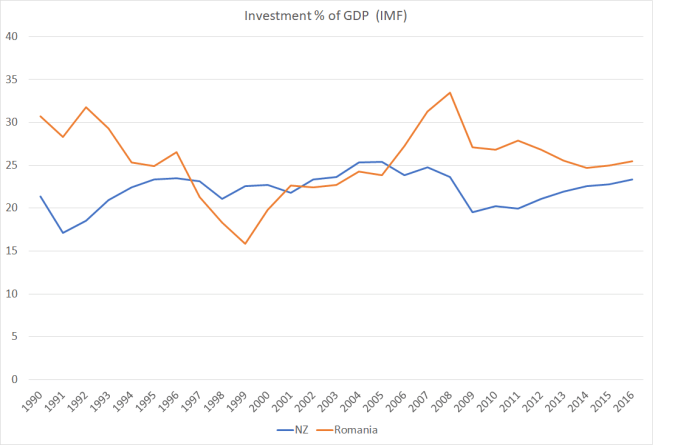

Romanian investment has fallen back from what they experienced in the credit boom period. Then again, it is still higher, as a share of GDP, than that in New Zealand.

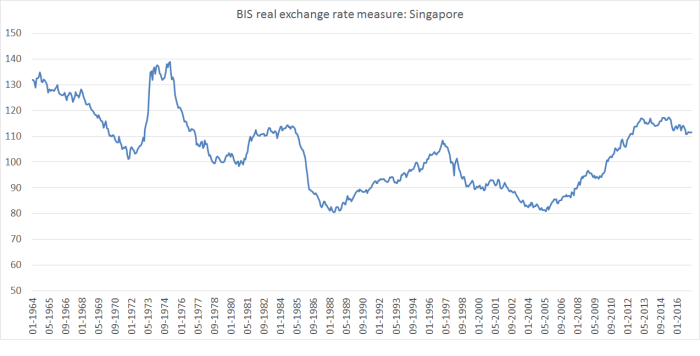

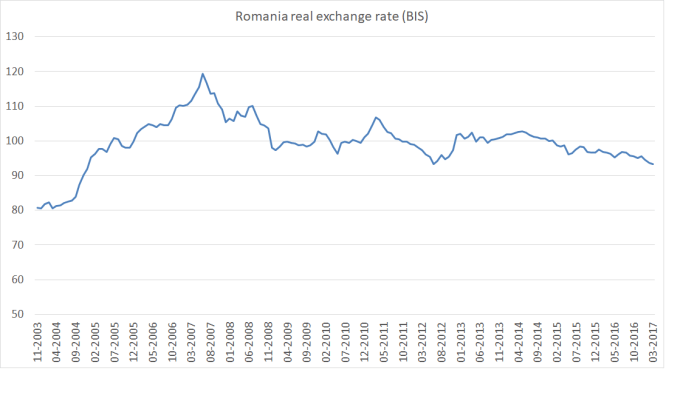

In fact, they had exactly the sort of worrying real exchange rate appreciation one might have expected in the credit-boom years.

But after that credit boom ended, the real exchange rate fell back.

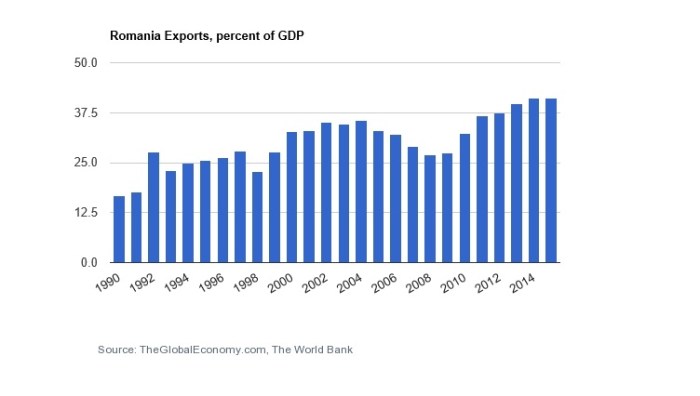

Perhaps consistent with that, firms based in Romania seem to have been doing rather well in international markets. Exports look as though they were squeezed out during the credit boom, but the subsequent recovery and trend growth is pretty impressive. For a country with a population of about 20 million people, it is a reasonably high foreign trade share (this is exports, but imports are equally important). Australia, for example, is around 20 per cent of GDP.

(You will recall that New Zealand has been going backwards on this metric.)

(You will recall that New Zealand has been going backwards on this metric.)

And there was one other interesting comparison.

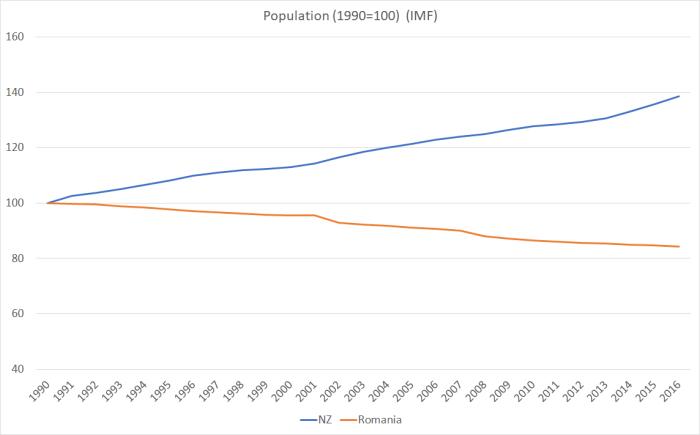

Since 1990, Romania’s population has fallen by 16 per cent, and ours has risen by 40 per cent. There are several differences. As I showed a few weeks ago, New Zealand’s total fertility rate over recent decades has been averaging below replacement. Romania’s has been materially lower still, currently around 1.4. And both countries have had material outflows of their own citizens: we had a net outflow of New Zealand citizens of around half a million people since 1990. Romania has also had big outflows but (as far as I can tell) smaller cumulatively than those from New Zealand (there is a reference here to about 2.3 million Romanians living abroad long-term).

But, of course, the other difference is non-citizen immigration. We’ve for a long time aimed to grant residence approvals equal to around 1 per cent of the population each year. Since 1990, those policies have given us a net inflow of around one million non-citizens.

The OECD’s International Migration Outlook recorded in 2015 that

Romania sets annual quotas for work authorisations to be issued, although historically demand has been lower than the quotas. For both 2014 and 2015, the quotas were set at 5500, including 900 intra-corporate transfers and 900 highly-skilled migrants.

In a country of 20 million people. Not necessarily a policy I’d recommend, but……

Subdued population growth (well, falling population actually) doesn’t seem to have been inconsistent with a pretty impressive period of productivity growth, export growth, strong investment etc etc, all in a country still with its share of governance and regulatory problems. And that investment isn’t largely having to keep up with a rapidly rising population, it is presumably responding the incentives and opportunities firms are finding). Perhaps the Romanians, in aggregate and in some sense, wish their population wasn’t falling – there is still anguishing about the outflow of skilled people – but probably their best hope of reversing that (perhaps slim given the low birth rate) is to keep right on with what they’ve been doing for the last 10 years. In time, perhaps many of the diaspora might even return – as they started to in Ireland after they finally got their act together.

30 years ago, Bob Jones toured the country lamenting that the New Zealand economy had come to resemble a Polish shipyard, a byword for inefficiency and industrial disruption. I do hope in 30 years time there aren’t reforming Romanian politicians campaigning, warning their fellow citizens to avoid the decline and fall of New Zealand. Yes, for now they are still poorer and, on average, less productive than we are. But those gaps have started closing fast, and the foundations of the growth don’t look that bad at all.

UPDATE: I forgot to mention Romania’s 16 per cent company tax rate. Not sure (whether as Baptist or economist) I quite approve of the separate regime for nightclubs and gambling operations.

(On another topic, I discovered that my name was being bandied around in Parliament’s question time the other day – question 2 here. Winston Peters was quoting me, and Steven Joyce was batting him away. All good fun no doubt. But I did notice this comment from the Minister “I appreciate that the member has been talking to Mr Reddell a bit”. In fact, I have never met Mr Peters, I have never talked to him, never emailed him or had any contact with him whatsoever. If he or his office appear to read my stuff at times well, of course, I welcome that, as I welcome any readers. Specific policy proposals, that might actually make a difference, would be even more welcome.)