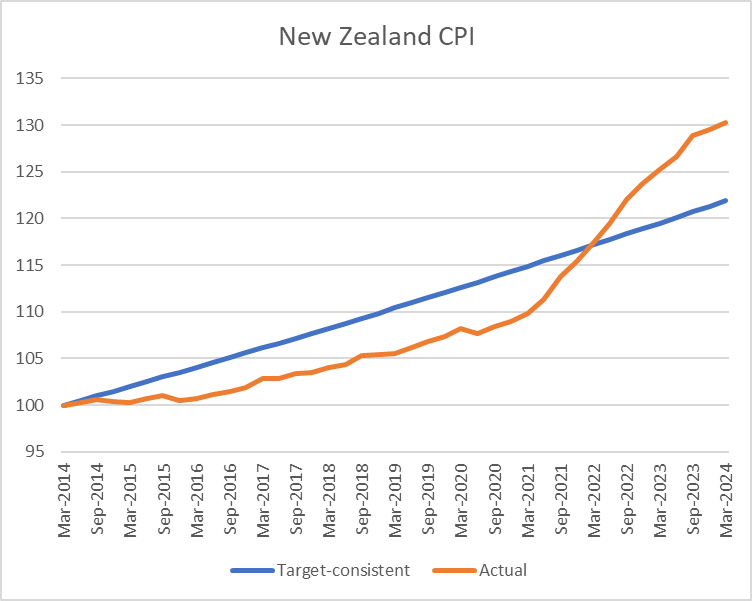

I got curious yesterday about how the Australia/New Zealand real exchange rate had changed over the last decade, and so dug out the data on the changes in the two countries’ CPIs. Over the 10 years from March 2014 to March 2024, New Zealand’s CPI had risen by 30.3 per cent and Australia’s CPI had risen by 30.4 per cent.

And that piqued my interest because the two countries have different inflation targets: New Zealand’s centred on 2 per cent per annum and Australia’s centred on 2.5 per cent.

So I drew myself this chart

Over the full 10 years, the two CPIs have increased by almost exactly the same amount, but they haven’t kept pace with each other steadily over that full period. Up to just prior to Covid, the Australian CPI had been increasing faster than New Zealand’s, as one might have expected given that the RBA had been given a higher inflation target than the RBNZ.

Now, before anyone objects, I should get in and note that in neither country is there a price level target. But if economies are subject to fairly similar shocks over a period of time one should normally expect a country with a higher inflation target to have experienced a higher cumulative price level increase than a country with a lower target.

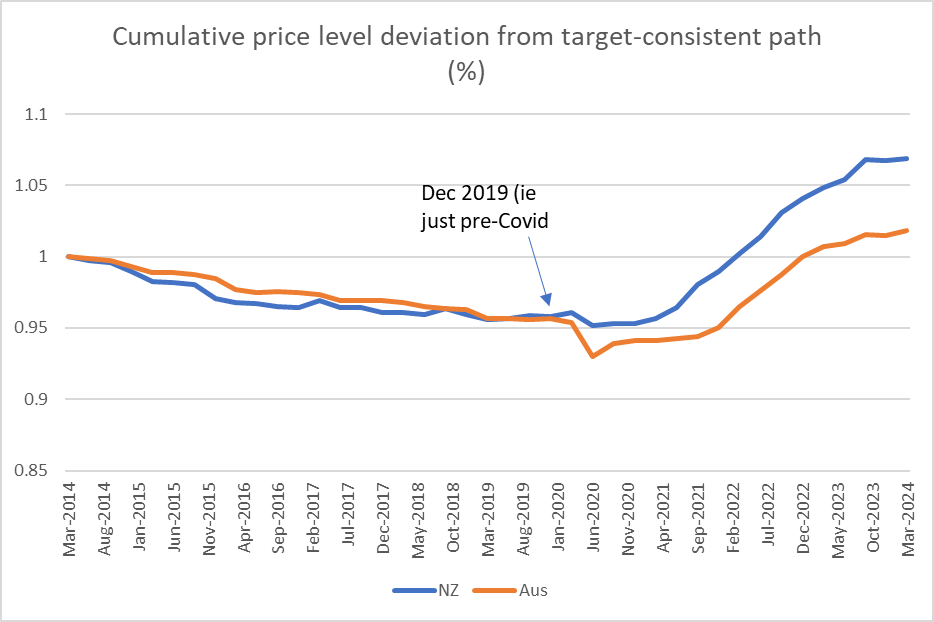

Over the 10 years here is Australia’s CPI relative to the price level that would have been implied by being consistently at target midpoint

and the same chart for New Zealand

And in this chart I’ve put it all together

Over the half-decade or so to the end of 2019, the RBA and the RBNZ had both ended up undershooting (on average) their targets by about the same extent. If you look closely, the RBNZ was undershooting more earlier, and the RBA more towards the end of the decade, but there wasn’t a great deal in the difference.

But where the difference really becomes apparent is in the years (four of them) since Covid hit. Over that period, the RBNZ has generated/tolerated much more of an increase in the price level, in excess of what is implied by their target, than the RBA did. (And for those – like Orr – who like to try distraction with things like oil shocks, wars and rumours of wars, and supply chain disruptions, Australia faced all those too.)

There is a lot of focus in Australia – and apparently reasonably enough – on whether the RBA has yet done enough with monetary policy. It has certainly been puzzling that they reckoned they could get away with materially lower policy rates than in other Anglo countries, in the face of (still) near-record low rates of unemployment and a quite stimulatory fiscal policy. But so far, and overall, they’ve done a bit less badly than the Reserve Bank of New Zealand through the last four years taken together.

It remains somewhat remarkable how little serious accountability there has been for serious Reserve Bank policy errors, for which now pretty much everyone (except them) is paying the price. in one form or another.

(By the way, for anyone interested, the NZD/AUD exchange rate averaged 0.933 in the March 2014 quarter and 0.932 in the March 2024 quarter, so over that particular 10 year period there was no change in the real exchange rate at all.)

I’ve been rather tied up with other stuff for the last few weeks (including here) which is why I’ve not previously gotten round to writing about the first piece of monetary policy communications from our Reserve Bank this year. That was the “speech” by the Bank’s chief economist (and MPC) member Paul Conway given to anyone and no one in particular over the internet last Tuesday. It had been a couple of months since anything had been heard from any MPC members, in what are not exactly settled or uninteresting times, and it is still several weeks until we get the first formal monetary policy review and MPS this year. We really should be able to expect better……but then if it were that sort of central bank, lots of things about the last few years would have been done differently, including the Bank might not have lost the taxpayer the mindbogglingly large amount of $11bn or so (with not the least sign of any contrition or of anyone having been held accountable).

Conway’s fairly short piece was a puzzling document. What was the pressing need that called for a speech on ‘the importance of quality research and data”? And what made it sufficiently pressing that they couldn’t even wait to find a real live function/audience to address? And if there is no particular function/occasion that needed a speech, but rather just something the Bank had chosen to do, wouldn’t you have expected (I certainly would) to have found some substance. The bit (the bulk) of the speech under that headline title was in fact much more notable for what wasn’t there. Is any serious observer going to dispute the likely value of quality research and data? And especially not against the backdrop of the actual New Zealand situation: poor (if very slowly improving) data and very limited volumes of macroeconomic and financial research (with the Reserve Bank’s own output in the last half dozen years notably diminished).

You couldn’t help but think that the “speech” was really just an excuse for putting out a page and a half of comment on recent economic data. I’m all in favour of individual MPC members putting their individual views and their analysis into the public domain (one of the few ways we see the quality of the analysis and thinking of these statutory officeholders). Perhaps all the more so when it had been two months since we’d heard anything, but then one was left wondering why they felt the need to wrap an entire speech around those brief comments rather than (say) just stick out a press release with the recent data comments.

But if the process was a bit puzzling, my main interest was the substantive content of the short address.

I’m going to take the material in reverse order. At the back of the speech there is a page a half of text on “a policy-relevant research agenda” and “the importance of quality data”. On the first of those headings, the speech is simply devoid of content. One might have hoped they would be releasing some new research or touting how policy-relevant research papers had shaped their thinking and understanding over one of the most turbulent periods for monetary policy in decades. Or even just foreshadowed a couple of specific papers that were almost ready for release. Instead there was nothing of substance at all, just a stylised graphic highlighting areas they were interested in, a list looking pretty much like any monetary policy research agenda in recent decades for almost any advanced country central bank.

What of data? Better data would be great. At a macroeconomic level, New Zealand is one of only two OECD countries with only a quarterly CPI, something Conway glides over in welcoming the recent additions to the partial monthly prices data. We also don’t have monthly unemployment data, a pretty basic measure of excess capacity/slack, and all our main macroeconomic data comes out later, with longer lags, than most of our OECD peers. It really isn’t a satisfactory situation, when so much rides on reading the economy well. But what Conway offers is mostly honeyed words about “a consultation process” with SNZ “to better understand data needs and priorities”. If one wanted to look on the bright site I guess one could note that they are “exploring collecting much more detailed data from banks to support economic analysis and research” and “we are also developing new sources of higher-frequency data to incorporate into the MPC’s assessment process”, which sounds fine directionally, but so far doesn’t seem to have amounted to much.

Right up front, in the introduction to his speech, Conway claims that “the economy is now significantly different to how it was before COVID-19”. His claims appears to be that this is so for both the world economy and for New Zealand. Again, it is a lead-in to what is, at best, a once-over-lightly treatment: one page of text and two charts, and simply isn’t very persuasive at all (especially as regards the functioning of the economy as it affects monetary policy).

Inflation went up, to very uncomfortably high levels, and then is coming back down again. But what about how the economy works is materially different now than it was five years ago? Conway really offers no hints at all. Instead he notes that government deficits have been large and government debt has increased (as he notes, by more as a percentage of GDP in New Zealand than in the typical OECD country) but what, if any, implications are there for monetary policy? It isn’t obvious and Conway offers no suggestions.

Then when we get the common line about globalisation changing, with supply chain resilience and geopolitics more in focus. It is a common line, and this might have been an opportunity to illustrate the point with specific reference to New Zealand macroeconomic and inflation dynamics. But no…. I’m still a little sceptical that there is much to the story (of macroeconomic significance) and took that line too from a recent Martin Wolf piece in the FT. Perhaps there is a story that matters to the Bank, but Conway made no effort to get beyond the cliches.

We also heard - what we all know - that traffic through the Suez and Panama canals is down at present (the former for geopolitical reasons, the latter for climatic), but nothing at all about what it might, or might not, mean for cyclical or inflation dynamics. The Suez Canal, for example, was shut completely and for several years a few decades ago. In what way did it matter and to whom?

And then we got Conway’s take that “the pandemic has sped up the digital transformation”, which was he thought a good thing. I can’t claim to have read all the papers on the subject, but my impression had been that there just wasn’t much there (in terms, eg, of improved productivity). And if in some places more people are working from home (less a thing here it seems than in some US big cities) in what material way would it matter for a central bank?

Perhaps there were substantive points to be made. Perhaps there were things New Zealand (eg RBNZ) research might have shed light on. But….nothing.

Most of whatever interest the speech commanded was inevitably going to be on Conway’s short comments on recent data. When the MPC hasn’t spoken for two months, and was then last heard talking up the possibility of a further OCR increase, it was going to be lot of few drops of rain falling on travellers crossing a parched desert. It wasn’t as if that November MPS statement itself had been overly persuasive (this was the Bank that was talking of further OCR increases even as it forecasts showed inflation collapsing over the next few quarters).

Whatever you own view of the data, you can see why Conway might have wanted to be cautious. The Bank had been talking of a further OCR increase while the market was now very focus on when, and how aggressively, rate cuts would start (here and abroad). Last week’s short comments seem to have been designed basically to try to dampen market enthusiasm, not necessarily because Conway and such of his colleagues who were consulted had a markedly different firm view than the market, but so as not to create a rod for the Bank’s back if, come late February, the Committee as a whole does conclude that there is no OCR cut in prospect any time soon. The more the market had already moved, the harder it would be for the Bank to drive home its message (without quite nasty snapbacks in market pricing).

What, if any, insights were there in Conway’s comments? Not much.

There seemed to be three points:

revisions downwards to the level of GDP over several years past don’t necessarily tell us anything much about the inflation outlook. And, of course, every serious analyst already recognises this : if those data suggested the underlying productivity picture was a bit worse than had been thought, they don’t tell us much, if anything, about capacity pressures and how they are changing. We already have the inflation data for those earlier periods when the level of GDP itself was a bit lower than had been thought.

We (they) really don’t know what is going on with immigration (either the numbers – itself a reflection of data weaknesses reintroduced to the system a year or two before Covid – or the net pressures on capacity and inflation). There was a footnote suggesting NZIER had done some work for the Bank on migration and inflation, which is described as “forthcoming” but no useful insights were offered from that work.

Inflation is falling but – on the measure Conway chose to highlight (annual non-tradable inflation) – still far too high. But there was no supporting analysis at all.

Highlighting annual non-tradable inflation – and suggesting it is a “rough approximation of inflation generated within the New Zealand economy – was really a bit naughty in a couple of ways. As other commentators have pointed out, non-tradables inflation is almost always higher than general inflation, and it is general CPI inflation that the MPC is charged with focusing on. The MPC isn’t given an option of just being indifferent to tradables sector inflation. And you’d expect central bank analysts and policymakers to be fairly heavily focused on recent quarterly inflation (especially when the OCR only got to the current level last May), rather than lagging annual measures.

Conway mentions that core inflation measures are falling, but again chooses to illustrate the point using annual data only. That said, what used to be the Bank’s preferred measure – the sectoral factor model – is both annual and prone to revisions (up when inflation keeps rising, down when it keeps falling, but was already showing core inflation at 4.5 per cent, down from a peak of 5.7 per cent just a couple of quarters ago.

What about some of the quarterly core measures, probably reflecting the impact of monetary policy early last year? SNZ provides a breakdown into tradables and non-tradables only at the 10 per cent trim level. For tradables, the December quarter saw the lowest quarterly inflation rate since mid 2020, for non-tradables the lowest since the start of 2021. The picture is pretty similar for the weighted median quarterly data.

But perhaps the thing that surprised me most about Conway’s speech – in its reflection on recent data – is that there was no sign of any cross-country comparative perspective. Now, each country’s core inflation outcomes are ultimately the responsibility of its own monetary policy, but when core inflation in a bunch of countries rose pretty much at the same time, and then central bankers raised policy rates at pretty much the same time, and often to somewhat the same extent, you might think there would be value in posing cross-country comparisons, especially when many of those countries have more frequent and more recent data than we do. The common story seems to have been that (core) inflation has been falling away, a little earlier and easier than had seemed likely to many at (say) the start of last year. It isn’t obvious that New Zealand was a particular laggard in tightening (weren’t particularly early either) and so one might take some comfort from what is happening in other countries.

The comparison with the US might have been a particularly interesting one to touch on. The US has, so far, seemed to have experienced a sharp reduction in annualised core inflation with, as yet, little sign of any substantial or sustained economic slowdown. As Westpac’s Michael Gordon points out in a nice piece this morning, the US has been quite unusual on that score, and the economic data in both New Zealand and Australia have been materially weaker than we observed in the US (and that is especially so when one looks at per capita GDP growth). Quite why the US outcomes have, to date, been so favourable is a bit of mystery, not often explored by commentators in an international context, but when our economy has been so much weaker it seems that our inflation outlook should generally be positive. At very least it would be good to see some of this ground traversed in the MPS later in the month.

Before Christmas I wrote a piece here on monetary policy turning points in which I ended by noting that it wasn’t inconceivable that by the end of February an OCR cut might be appropriate here. Whether the data support such a case may be a bit clearer by Wednesday afternoon (after the quarterly suite of labour market data are out), although I don’t suppose that whatever the data show an early OCR cut is at all likely.

There is an interesting piece in the Financial Times today on “Why central banks are reluctant to declare victory over inflation”. Setting aside the fact that such language is more George Bush “Mission Accomplished” and never likely to be heard from central bankers – my old line (with acknowledgements to von Clausewitz) about inflation was “the price of price stability is eternal vigilance” – it nonetheless touches hardly at all on what must be one of the biggest factors weighing on the minds of central bankers. Having stuffed up so badly (a description rarely heard, although it should be more openly acknowledged) and delivered us into very high inflation and all the attendant unexpected wealth redistributions etc, central bank reputations took something of a well-deserved hit (a change since 2019 that of course Conway chose not to mention). They were too slow to reverse the easings of 2020 and the public paid the price. For them, reputationally, perhaps the worst possible thing now would be to begin easing, cutting policy rates, only to find in a few quarters time that inflation really wasn’t securely settling near target. There would be considerable public and political unease if they were soon tightening all over again. By contrast, people are attuned to the idea that squeezing out inflation involves some pain, so why not take the free (to them) option until they are 100 per cent sure inflation really is on course).

One problem then is that the interests of the individual central bankers – mostly still holding the offices they did in 2020/21 – aren’t necessarily well-aligned with the wider public interest. To be 100 per cent sure that inflation was well on course towards the target midpoint also necessarily then means quite a high risk of overshooting (both that inflation ends up going below target midpoint – as in so much of he pre Covid decade, here and abroad) and that output and employment are unnecessarily sacrificed. That, in turn, might be less of an issue in the US, where the economy has held up, then (say) here where we’ve already had last year some of the very weakest per capita GDP growth of any OECD country.

Much of the discussion about the possibility of rate cuts this year tends to proceed – perhaps not consciously but it is the effect – as if the two choices were to keep rates at current levels or to take them quickly back to neutral (wherever that unobserved variable might be – our RB thinks somewhere under 3 per cent). But those aren’t the choices central bankers actually face. I very much doubt it would be prudent for interest rates to be anywhere near neutral right now, but relative to how things looked when the OCR got to 5.5 per cent first in May 2023, there is a lot more reason now to be confident that the worst is past. Back then it was purely prospect but now we have some hard evidence, and we know that monetary policy works only with a lag. More disinflation is, as it needs to be, in the works. It isn’t impossible than an OCR of 5 or 5.25 per cent would now be better than one of 5.5 per cent.

Of course, none of any of this was in the Conway speech, which really did seem to be just about buying time/space to get the MPC through to the end of February (after its inexcusable three month summer break).

In conclusion….well, this was Conway’s

It was really quite remarkable for its avoidance of any responsibility. You’d note know from this that any central bank’s conscious and deliberate choices played any part in inflation being well above target for three years in succession. When you can’t acknowledge your part in a really bad, costly and disruptive, set of outcomes, it is really hard to be confident that you are really any sort of “learning organisation” or that the much-vaunted (but as yet unseen) research will be for anything other than support rather than illumination.

Central bank monetary policy speeches are rare enough in New Zealand. On the rare occasions MPC members do speak we deserve better than Conway’s effort. The Governor is due to speak next week. HIs speeches to the Waikato Economics Forum have tended to be substance-free zones, but I guess we can always hope.

And I hope the Minister of Finance and her advisers are taking note, and are looking to find and appoint rather better people to fill the two MPC vacancies arising in the next few months.

The Herald ran an op-ed yesterday under the heading “Why the Government’s new Reserve Bank mandate may lead to worse outcomes”. It was written by Toby Moore who served as an economic adviser in Grant Robertson’s office while he was Minister of Finance (a fact the Herald chose not to disclose to its readers).

I’m more interested in the substance of his argument. Moore is a serious guy, and I suspect he’d run his arguments whether or not he’d ever taken up a role with Robertson. But I think his core argument ends up not very persuasive.

Moore opens his article pointing out that there isn’t an overly strong economic case for having reverted to something very like the old statutory objective for monetary policy. There are certainly bigger economic challenges (albeit probably not ones the law draftsmen could tackle as quickly). As the Governor repeated again yesterday – while trying to minimise the extent to which the previous wording was actually a “dual mandate” (a point on which he was correct, but not a point he’d have made often under the previous government) – no monetary policy decision in the last few years was made differently because of the revised wording of the statutory mandate. That is entirely convincing: the Reserve Bank’s big mistakes (and they were very big mistakes) were forecasting ones. Given their forecasts their OCR choices made (more or less) sense. But they misunderstood how the economy was operating and how real the inflation risks were.

But then Moore attempts to argue that much of the previous 30 years would have been different (and better) if only the Reserve Bank had spent those decades operating under the statutory mandate it had from 2019 to 2023. The episode I want to focus on is that from a decade or so ago. These are his words

One can see the issue more starkly in this chart

As one added bit of context, in 2012 a requirement was added to the Policy Targets Agreements requiring the Governor to focus on delivering inflation near 2 per cent, the midpoint of the 1-3 per cent target range.

I agree with Moore that a series of bad monetary policy choices were made by the Reserve Bank during this period. In fact, while I was still at the Reserve Bank I argued against the proposed tightening cycle that eventuated in 2014 on the twin grounds that core inflation was very low, and (consistent with this) evidence from the labour market suggested quite a lot of slack still in the economy. Once I left the Bank in early 2015, it became a regular theme in commentary on this blog.

But…..the key point is that, once again, economic forecasts were very wrong. The Bank’s forecasts during this period usually had core inflation coming back to the midpoint and needing higher interest rates to keep it there.

And actually I think there is a fair argument - that should appeal to Moore, although not to some others - that during in 2010s one problem was that the Governor, having recently returned from a long sojourn in the US, became fixated on the housing market and the US crisis of 2007-09, and constantly wanted to orient policy to lean against such risks, without ever stopping to consider (a) similarities and differences between NZ and the US, or (b) his statutory mandate. It wasn’t the biggest factor in setting monetary policy wrongly – policy that delivered core inflation bouncing near the floor of the target range for years – the problem was forecasting failure and bad models – but it didn’t help either.

A central bank in the early 2010s (a) strongly focused on the inflation target, and (b) with better forecasts/models (or just looking out the window) would have delivered a lower OCR during that period, and in particular would not have championed a substantial tightening in 2014. That would have had better outcomes for inflation and for unemployment.

Reasonable people can differ on how best to specify and to articulate what we look to the Reserve Bank to deliver with monetary policy, but the problem a decade ago wasn’t some excessive focus on inflation, but a poor understanding (shared of course with many others here and abroad) of just what was going on. Arguably, looking out the window - at actual headline and core inflation - might have given a better steer during that period. A ‘dual mandate’ simply wouldn’t credibly have made any difference, given all else we know. The unemployed paid a price for those limitations/mistakes (as holders of fixed nominal financial assets have paid a big price for central bank mistakes in the last year or two).

Excellent central banks matter. They make a difference to real people, real outcomes. It would be good if we had one, and/or a government seriously resolved to deliver a better one.

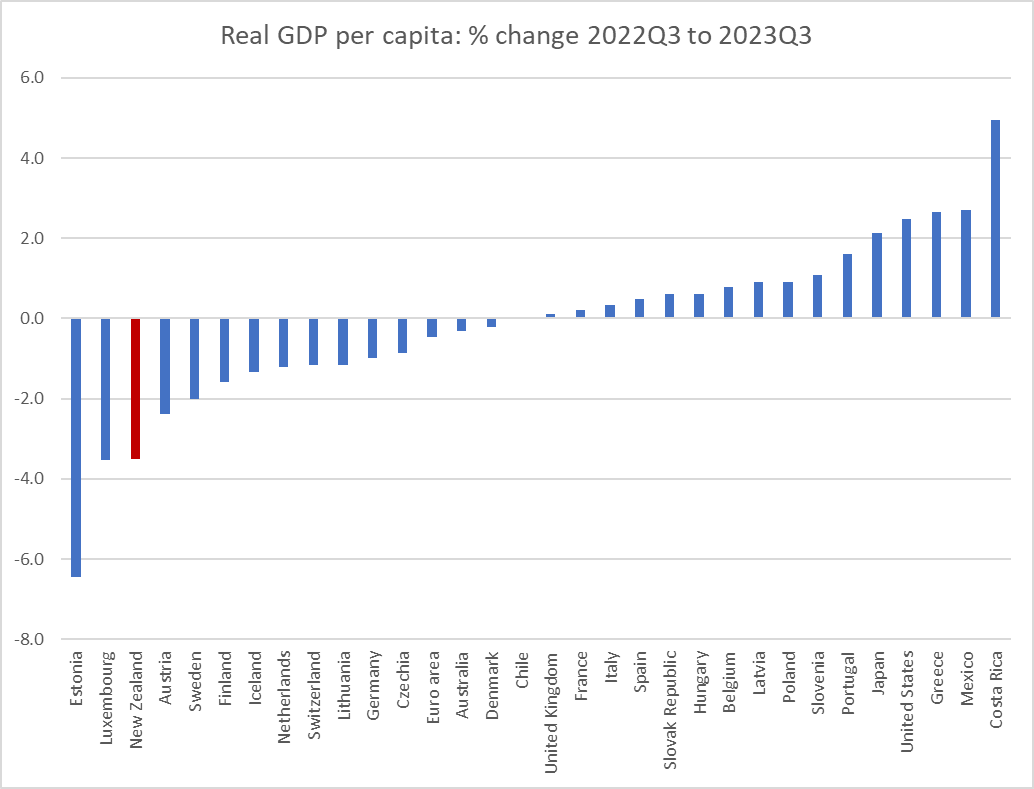

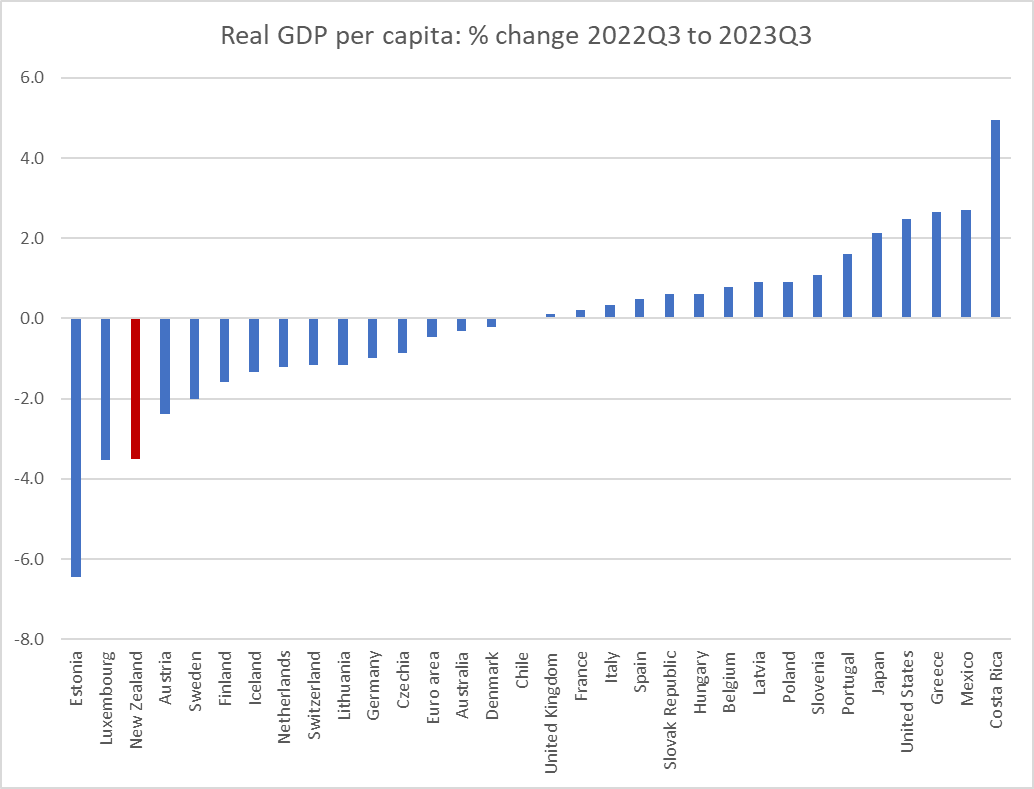

The fall in New Zealand’s per capita real GDP (averaging production and expenditure measures) over the last year has been quite striking set against other advanced (OECD) countries for the same period. We are equal second-worst, and quite a bit worse than the next country with its own monetary policy (Sweden) - I’m mainly interested in the inflation situation. The fall in real per capita GDP in New Zealand thus far isn’t much short of the fall experienced in the 2008/09 recession.

With recent data it is certain there will be revisions and thus it isn’t impossible that the last year might end up looking a bit less bad. But for now, the published data are the best official guesses - for us, and for fiscal and monetary policymakers.

The OECD has data on quarterly real per capita GDP, going back a fair way (a lot further for some countries than for others, but pretty comprehensive for current members from the mid 1990s). I was curious how common falls in real per capita GDP had been in that database.

For the 1980s there isn’t data for many countries, but we find large annual falls in real per capita GDP as follows

Australia 1982/83

Canada 1982 (at worst about -5% per annum), and

the United States 1982 (the recession that saw them get inflation down.

Coming forward to the early 1990s we find

Finland 1991/92 (some mix of domestic financial crisis and the fall of the Soviet Union)

Canada 1991

Iceland 1992

(New Zealand would probably be on the list but our official population series begins in the middle of the early 90s recession)

Moving on a few years and we have

Chile 1998/99

Israel 2001/02

In 2008/09 all but a handful of countries saw a significant fall in real per capita GDP. It was, of course, the recession that ushered in the decade or so of surprisingly low inflation. At worst, per capita real GDP fell by about 5 per cent per annum in the US and 6 per cent in the euro-area (and about 4 per cent here).

In and around 2012 various euro-area countries (but notably Greece) did dreadfully, but the euro-area as a whole only saw real GDP per capita falling at about 1 per cent per annum during that period.

Covid intervened – when we shut down economies for a time and deliberately wound back economic activity – but otherwise there are no big falls in per capita GDP on an annual basis in places with their own monetary policy until……New Zealand right now.

What we have seen over the last year isn’t normal or small, but a large fall, of the sort seen in advanced economies only in pretty adverse times.

Why focus on real per capita GDP? The public commentary tends to focus on GDP itself, with all the attention on whether the total size of the economy is rising or shrinking. But for most economic purposes, and certainly for inflation purposes, it isn’t a very relevant measure. Zero per cent growth in GDP means something a great deal different if the population is static or falling than if it is growing at 2.5 per cent per annum. It is (much) more likely that excess demand pressures are easing if – absent really nasty supply shocks – per capita real GDP is falling, even if there is still some headline growth in GDP itself.

That said, all such comparisons, especially across time, take one only so far. In an era of really strong underlying productivity growth, even a moderate GDP or real per capita GDP growth might be consistent with easing excess demand pressures, and if productivity growth is historically modest – as it has been in much of the advanced world for almost 20 years now – even falling per capita GDP might not be consistent with much or fast easing in capacity pressures.

But a fall of 3.5 per cent in real per capita GDP over the last twelve months probably deserves more attention than it has been getting thus far (even if headline unemployment has still been quite low).

When the Reserve Bank MPC came out late last month with its last words on monetary policy before its extended summer break, my post then was headed “Really?“. It was a commentary on the disjunction between the Reserve Bank’s inflation forecasts on the one hand, that showed quarterly inflation collapsing (not really too strong a word for it) over the next few quarters, and on the other hand the Bank’s OCR projections that showed a better than even chance of a further OCR increase early next year and an OCR at or above current levels well into 2025.

It wasn’t as if the Reserve Bank even gave us a compelling story as to why (a) they expected inflation to be just about to collapse or b) why they were talking in terms of further OCR increases. It just didn’t make a lot of sense, and they seemed doomed to be wrong on one count or another. And here remember the lags (something the Governor himself reminded people off in his press conference): whatever core inflation is going to be by the middle of next year is (unknown but) baked-in already. Changing monetary policy would make little or no difference to most of next year’s inflation.

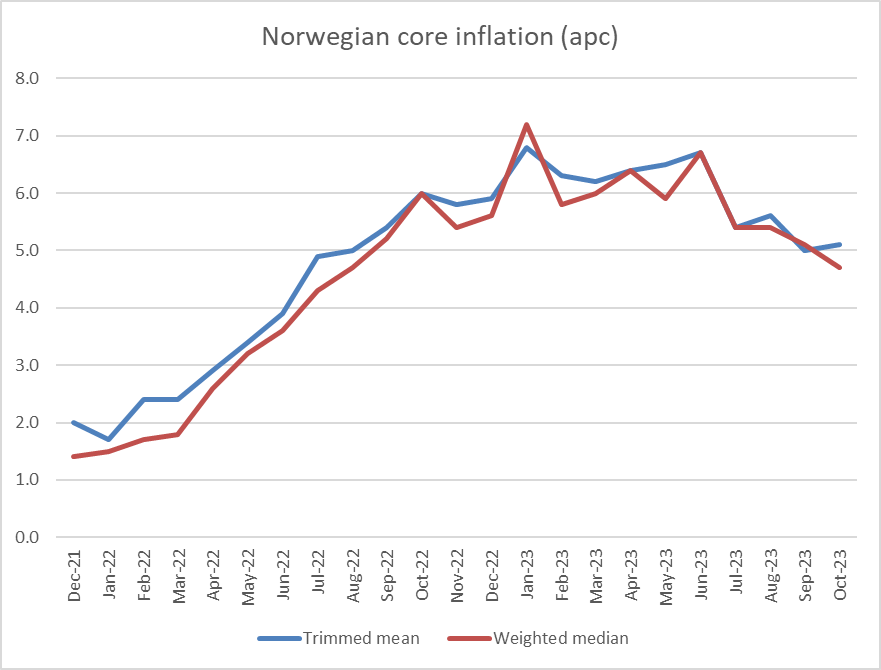

Now, it is quite fair to note that there hasn’t been much sign so far in the official CPI data of the core and persistent parts of inflation coming down much, if at all. As ever in New Zealand, things aren’t helped by infrequent and lagging data (our last comprehensive CPI data are reading things as at mid-August). Neither the trimmed mean nor weighted median measures are done on seasonally-adjusted data (SNZ, please fix this), but the latest quarterly observations for both measures were about the same as in the September quarter a year earlier. We do have a seasonally-adjusted quarterly non-tradables inflation data, and the latest observations are down from the peak, but the September quarterly inflation rate was still no lower than June’s. There is enough in those official data to suggest core inflation has definitely peaked - which isn’t nothing - but having gotten things so wrong a couple of years ago you can understand why MPC members might still be a little nervous if they were just looking at the CPI (although if you were really that nervous why project such a sharp fall in inflation so soon?)

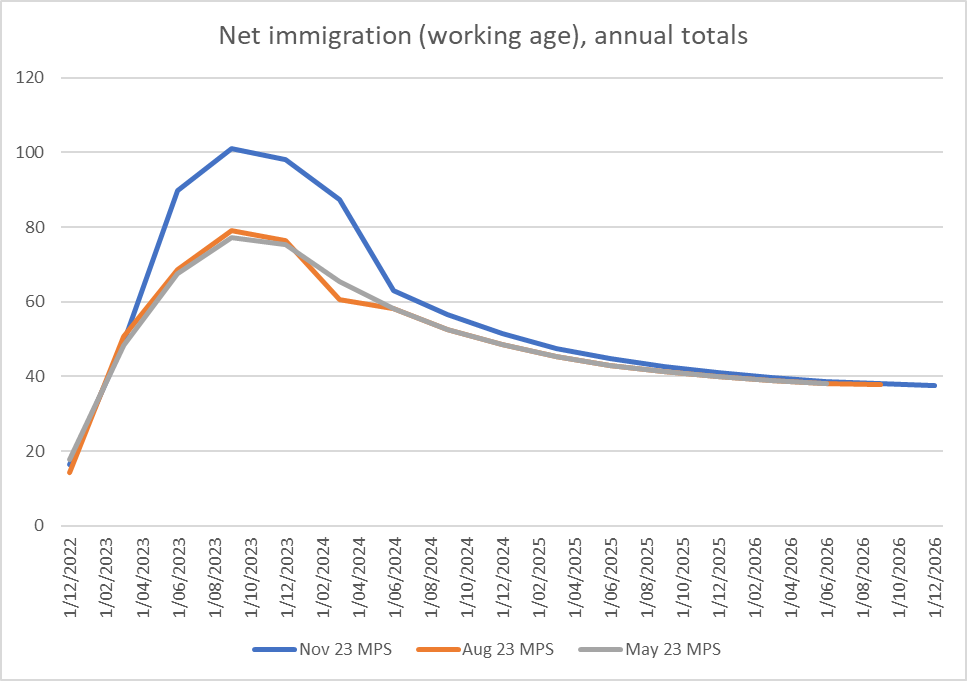

The issues are compounded for the Reserve Bank - and anyone else trying to make sense of what is going on now and what might happen soon – by the fact that two big and powerful countervailing forces have been at work. On the one hand, we had the OCR raised by 525 basis points in little more than 18 months, an usually large move in such a short space of time (the only move really comparable was in 1994 - focus then on the 90 day bill rate). And, on the other hand, record net migration inflows. In isolation one is a sharply disinflationary force while the other has added to inflationary pressures (although on the Bank’s forecasts net migration is forecast to be sharply lower next year, and if so that is likely to be a disinflationary shock). Since the Bank’s models - and anyone else’s – didn’t do very well at all in picking the sharp increase in core inflation, there is probably little reason for them (or anyone else) to have much confidence now.

All that said, it is getting increasingly hard not to think that inflation is about to fall away pretty sharply, and would keep doing so for some considerable time if the OCR were left at current levels or even raised a bit further.

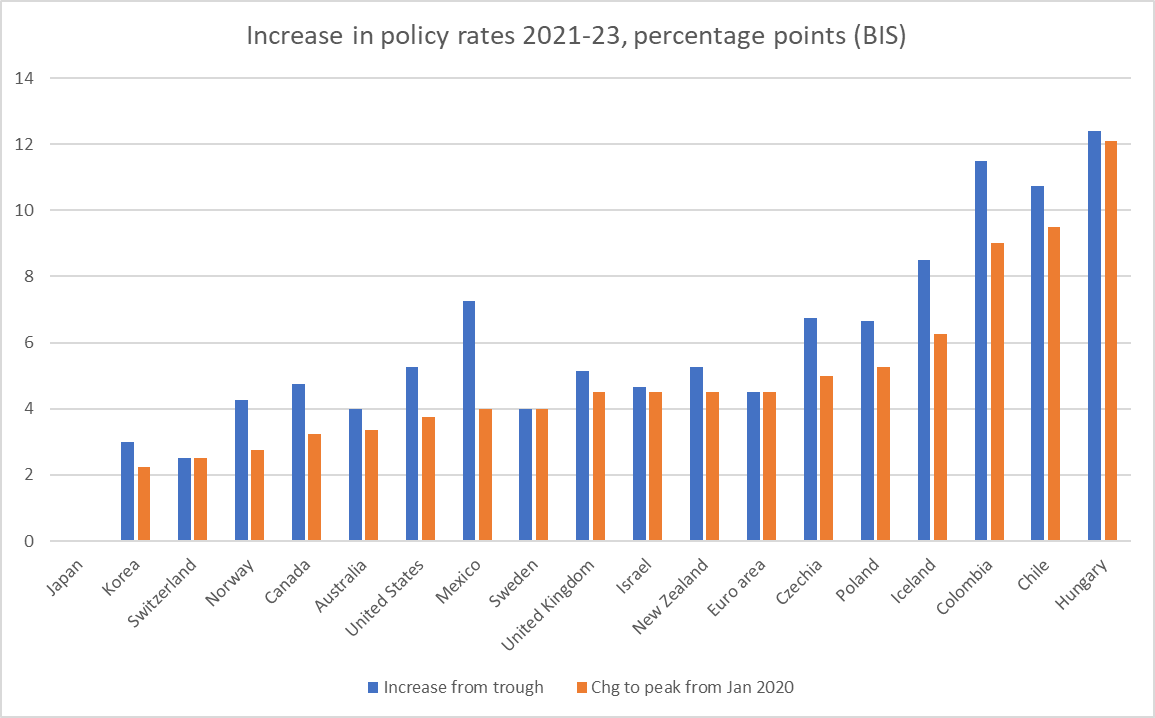

There are straws in the wind from the partial (monthly) price data that SNZ releases. Indicators from the labour market suggest it is much easier to find staff (much harder to find a job) than was the case just a few months ago (at the level of anecdote I’ve been surprised by stories from my university student kids about how much problem many young people they know have had getting holiday jobs). The experience of several other countries is also not likely to be irrelevant - where inflation has also (finally) seemed to have begun to fall away faster than seemed to likely to policymakers earlier this year (and bear in mind that if the RBNZ was not one of the first advanced country central banks to raise the OCR in 2021 (it was about 7th), it was moving earlier than central banks in the US, the euro-area, Canada, or Australia.

But then there are things like the GDP data. This was from my post on Saturday

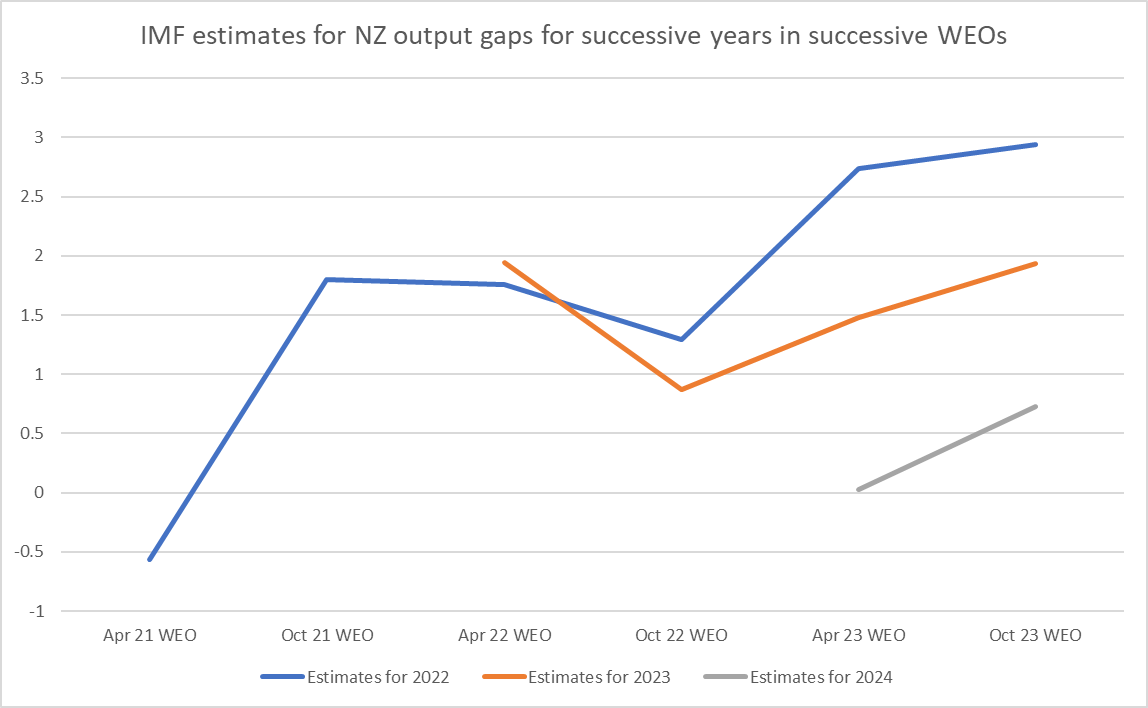

Now, it is fair to note that on some international estimates New Zealand had a larger positive output gap than most other advanced countries when inflation pressures were at their peak last year. On that basis, it might take more work - more loss of output - to get inflation back down here than in many other advanced economies. But when you have the second worst growth in GDP per capita of any OECD economy (and materially weaker, on current estimates, than the next country with its own monetary policy - Sweden) it might seem like a reasonable hunch that enough has been done. Of course, there will be revisions to come, but the December quarterly GDP release (ie last week’s) is generally the least unreliable because it benefits from the recent updates of the annual national accounts.

Now, is it impossible that inflation could stay high - or fall only very sluggishly - even if GDP (and GDP per capita, which is more important here) are very weak. In extreme scenarios of course not. But the economy hasn’t been suffering from really nasty adverse supply shocks over the last year, extreme political instability is not a feature (transfers of office happened as normally as ever), and……inflation expectations have stayed encouragingly subdued throughout the last couple of years, and are modest now. In a rag-tag sort of way the system seems to have worked (central banks messed up really badly in 2020 and 2021 - and that can’t be lost sight of – but when all the alternatives had been explored seem to have done what was required). The high inflation of the last couple of years is going to be a nasty memory for quite a while (here as elsewhere), but there is little sign anyone much thinks inflation is going to settle outside the target range.

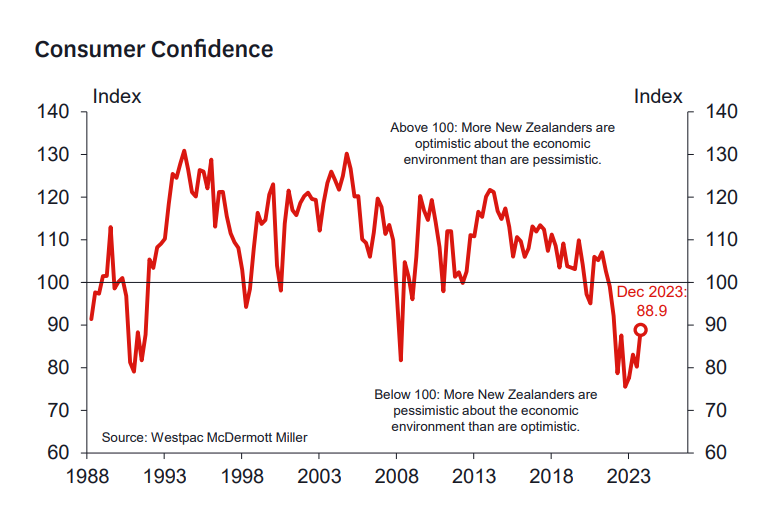

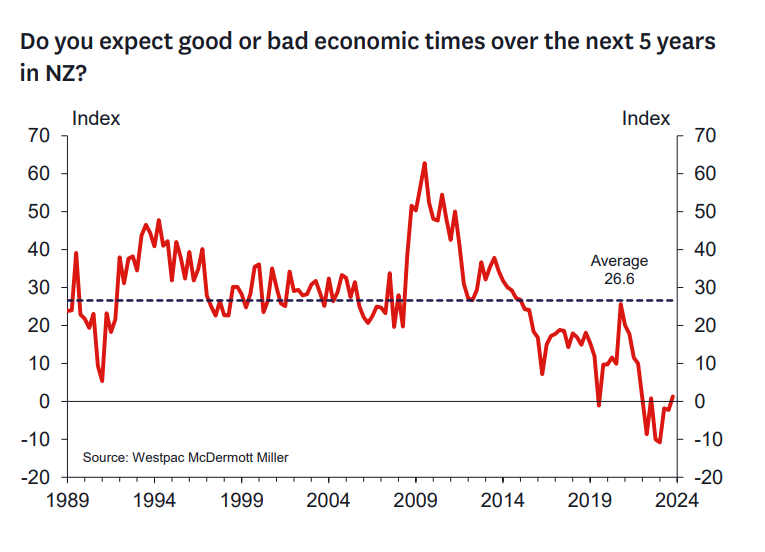

Worriers may point to recent pick-ups in confidence survey measures. This (Westpac) one just turned up in my email inbox

Being off the lows here still leaves it not far above troughs in the most recent two severe recessions in New Zealand. All the confidence measures are still in contractionary territory, and the medium-term mood is about as bleak as ever.

One reason sometimes mentioned for why central banks would be cautious is that - after the mistakes of 2020 and 2021 - it would be quite unfortunate if they were to sound softer now only to find that inflation was hanging up and that renewed tightening was eventually needed to finally get things back near target.

As a psychological consideration it is no doubt real. But central bankers shouldn’t be purging their own “guilt” or past incomprehension by holding tight indefinitely. Rather they need to recognise those personal biases etc and correct for them.

Against that backdrop I found it useful to look back at some of the last big easing cycles that the Reserve Bank presided over. A couple of weren’t very enlightening: the increases in the OCR in 2014 were never justified in the first place so when they were finally unwound didn’t offer much. And in the mid 90s there was enough weirdness - and volatility - about the management of monetary conditions (for those with long memories, think of the Monetary Conditions Index). But I had a look at 1990/91 and at 2008. In both cases, short-term interest rates fell by 500+ basis points (in the first case, accommodated by the RB – this was pre OCR – and in the latter by direct Reserve Bank decision). In both cases, inflation had been or become quite a problem. In 1990 core inflation had been stuck around 5 per cent and the goal – a couple of years out - was 1 per cent (midpoint of the 0-2 per cent range), and in 2008 headline and core inflation had moved persistently above 3 per cent, the top of the target range (best current estimates have core inflation peaking in that cycle near 4 per cent).

Go back to 1990/91. The first negative GDP quarter was March 1991. That data won’t have been available until late in the June quarter of 1991, but by the month of March 1991 90 day bill rates had already fallen by about half (250 basis points) of that total fall that year. At that point, the most recent (December) quarterly inflation data were hardly better than they’d been a year earlier (although it was to fall away very sharply in the next few quarters). Two-year ahead inflation expectations were still about 4 per cent.

With the benefit of hindsight, if anything we were too slow and reluctant (for a long time) to let interest rates fall that year. Much as we expected inflation to fall, we (like almost everyone else) was taken by surprise be the speed and size of the fall.

What about 2007/08, when the inflation target was much the same as it is now, and the monetary policy implementation system (the OCR) was the same?

Going into 2008, the OCR was at 8.25 per cent, a level it had been raised to in mid 2007 (at the time on the back of rising international commodity prices, when core inflation had already got troublingly high). What was to become labelled as the “global financial crisis” is conventionally dated as beginning in the northern hemisphere in August 2007 but even by mid 2008 it wasn’t seen as a huge factor in New Zealand (within the Bank there were competing views) - the galvanising events (eg Lehmans) weren’t until September that year. The world oil price had peaked - at still all-time highs - a bit earlier that year.

The New Zealand economy could hardly be said to have been in fine good heart. The lagged effects of several years of OCR increases were increasingly evident. But the unemployment rate by mid year was only a little off its lows (3.8 per cent), there’d been just a single quarter of falling GDP published (and some of that had been weather-related), but the first OCR cut was in July 2008. Two-year ahead inflation expectations are the time were about 2.9 per cent (a touch higher than they are right now). I recall the MPC/OCRAG debates at the time, which with hindsight were a bit surreal as there was much discussion about whether just possibly we might be able to cut by as much as 100 basis points over the following year (actual 575 basis points, and probably should have been more).

With hindsight - and here I would put more stress on hindsight – we were too slow to start moving then. It was perhaps understandable given where core inflation was, and the difficulty of anticipating the full gory mess about to break on us from abroad, but it was too slow. But my point was that it was long time afterwards before it was clear that core inflation was actually back near target or even that the unemployment was back around some sort of NAIRU (it was early February 2009 before the Bank knew the unemployment rate had got to 4.4 per cent).

Have there been mistakes in the other direction? Of course. The 2020 monetary policy easing was clearly a mistake. But there have also been a couple of times when we (the Bank) thought we’d done enough only to have to resume tightening (one might think of 2005/6) but the message from the data now is becoming fairly clear. At some point - perhaps before too long - much the bigger risk is likely to be holding the OCR at peak for too long.

Go back a year or so and there was quite a bit of debate about what the neutral OCR might be? No one really had any idea, and in truth no really does now. But……the developments in core inflation globally (and in GDP and jobs ads data locally) given us a much stronger reason now to be confident that policy rates are contractionary than perhaps we’d have had at the start of the year. And central banks do purport to run a system that puts quite some weight on forecasts of inflation. In practice, there is less reliance than is implied by the rhetoric (and models), which reflects the fact that forecasting is hard.

In debates here and abroad about the appropriate stance of monetary policy one often sees mention of two things. First, the notion that “the last mile” might prove materially harder than the first steps downwards in inflation. Mostly that seems like handwaving, especially when the focus is – as it should be - on measures of core inflation. There doesn’t seem to be much evidence from past cycles (including in New Zealand when we were first securing something like price stability in the early 1990s) of a “last mile” problem, and it seems no more plausible this time when inflation expectations have been subdued (and when in New Zealand the exchange rate remains fairly high and stable). The other argument is that central banks need to be sure we are going to get back to target. That is an argument that puts no weight on forecasts at all. I’m not one with any particular confidence in published central bank forecasts, but in most past big falls in inflation it would have proved to be a mistake (as indeed it was two years ago when central banks were slow to tighten). As time passes, there is more reason for confidence than there might have been even six months ago. Even in principle, that confidence isn’t enough to suggest policy rates should be back to neutral - wherever neutral is - but it should be enough to suggest that less contractionary settings might be required to give one the same level of confidence one was seeking 6-9 months ago when policy rates were first approaching what now seems to be the peak. We don’t have any real idea as to whether the OCR settles at 1.5 or 3.5 per cent, but it seems most unlikely it will settle anywhere near 5.5.

I’m still quite deeply perplexed by the Reserve Bank’s stance last month (assuming that it wasn’t - and they say it wasn’t - just about playing games with markets to hold expectations up). It is less than satisfactory that (a) they’ve gone off for a three month summer break (in contrast, the Cabinet seems to get about four weeks between meetings), (b) that there are no speeches or serious interviews exploring the issues, outlook, and risk (without a Parliament there wasn’t even the theatre of an FEC hearing [UPDATE: Shortly after this post went out the RB put out an advisory that there will be an FEC MPS hearing at 8am on Wednesday}). We are left with no insight on the Reserve Bank thinking, or the range of risks, hypotheses etc they are exploring or how well they are marshalling evidence in support etc. It is our inadequate MPC on display again, summoning no confidence in them whatever even if (just possibly) somehow they are right.

If the meaningful dataflow this year is largely already at an end - hard to see the HYEFU or the micro-budget telling us much – the CPI data in late January, the suite of labour market data in early February, and the monthly spending indicators (including those banks are now producing of own customer activity) should be telling us (and the MPC) a lot. If things are as weak as many recent indicators have suggested and inflation pressures are (finally) abating fast, the possibility of an OCR cut in late February shouldn’t be thought completely impossible or inappropriate.

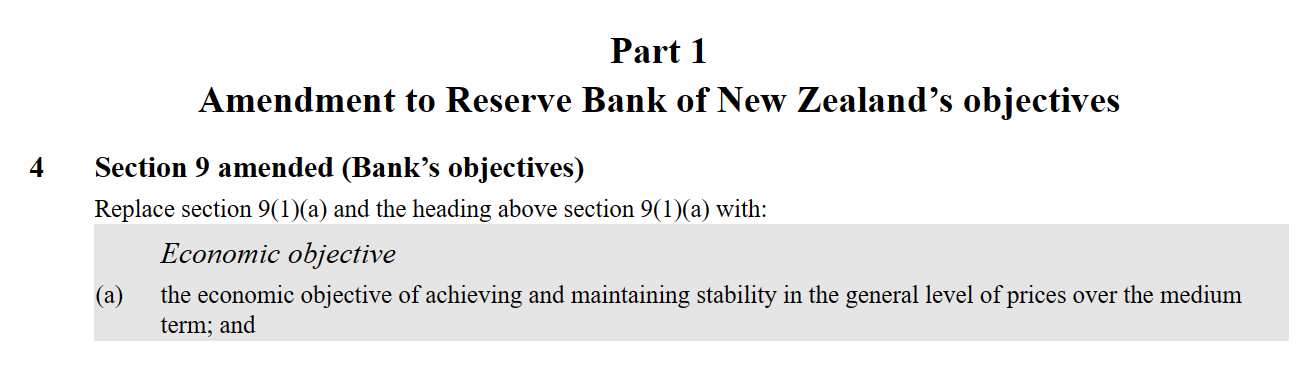

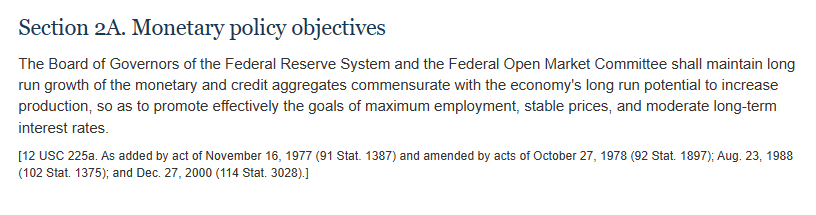

I guess it will be an Act by the end of the day, but for now the short bill giving effect to a return to a single statutory objective for monetary policy is here. Yesterday’s parliamentary debate (first and second reading) is here, here, and here.

The heart of the bill is this clause

Note that this does not return things to as they were in 2018, keeping Labour’s addition of “over the medium term”. My own view is that references to time horizons are better kept for the Remit, which can be written in a more context-dependent way (sometimes it might be really important to get back to “price stability” – which isn’t 1-3% annual inflation anyway – really rather quickly. For example, after three years of inflation well above target?) With a bit more time, it might have been a good opportunity to simplify the 1989 bit of the wording as well. Simply “maintaining stability in the general level of prices” would be an improvement. But those are second and third order issues about this symbolic legislative change.

My bigger concern is that the legislation is not a complement to substance but a substitute for it. There is nothing wrong at all with symbolic steps, but if done in isolation they quickly come to seem like cosmetic distractions.

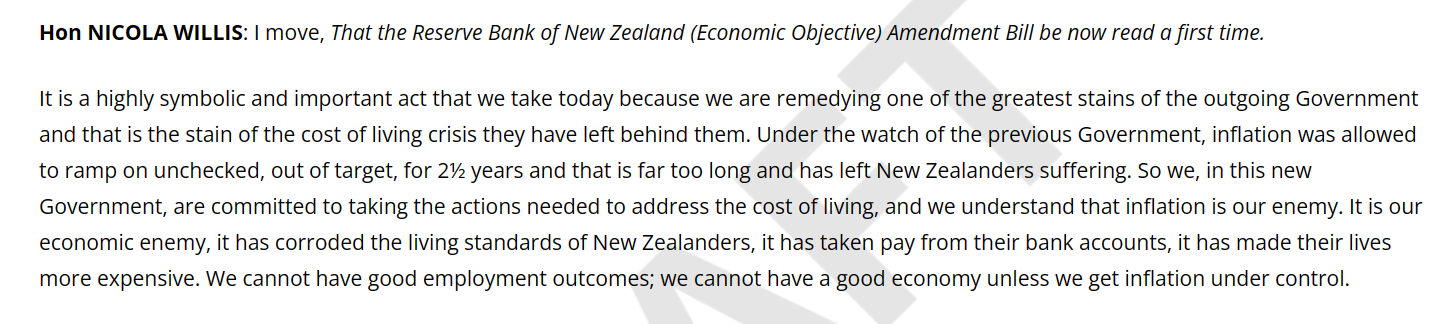

Take for example the Minister’s first reading speech

The bill is certainly a symbolic statement, but on its own it is nothing more than that. What is more, the Minister really should know that. There is nothing in the amendment that will, on its own, be “remedying one of the greatest stains of the outgoing Government and that is the stain of the cost of living crisis”. And there is nothing else even hinted at in the speeches from either the Minister or her associate (Seymour).

There has been a massive monetary policy failure in New Zealand in the last four years by the Reserve Bank of New Zealand (similar mistakes were made in many other advanced countries, but each operationally-independent central bank is responsible for its own country’s inflation rates). But, in part because there is a wide range of statutory legislative goals across countries and most of them ended up making much the same (really serious and costly) mistakes, it simply is not plausible to believe that things would have been materially different had that new “economic objective” been in place rather than the one that was actually on the statute books. There is no evidence at all to suggest that the monetary policy easing in 2020, the huge highly-risk LSAP punt, or the sluggish tightening in 2021 and early 2022 would have been any different at all, since the Reserve Bank’s own forecasts at the time (2020 and 2021) suggested to them that if anything what they were doing wasn’t really quite enough to keep inflation UP to the target midpoint.

This is all familiar ground but it is inconvenient ground (it appears) to the Minister who seems more interested in the rollicking political theatre of blaming her predecessor for his symbolic statutory amendment than in fixing our decayed and failing central bank. I read her speeches yesterday in both the first and second reading debates and there is no hint there that this statutory amendment is a first step in a process to fix the Bank or even to insist on some effective accountability for those whose decisions visited highly costly inflation and $12 billion of losses to the taxpayer on us. They used to talk of launching an independent review of Covid-era monetary policy. I was never entirely convinced of the case for such a review, and as I noted here recently if it is done the choice of reviewer will probably pre-determine the character of the final report, but it was a fairly consistent line from National. But there is no mention of it in yesterday’s speeches (the speech from the Associate Minister seemed more focused on the inflation of the Roman Empire than in actually fixing New Zealand’s central bank now).

The Minister (and her predecessor as Opposition finance spokesperson) has on several occasions been lied to by the Governor at FEC. The chair of the Board appears to have gotten away with lying to The Treasury, and getting Treasury to run spin for he and his Board have banned experts from serving as external members of the MPC. No external members have made even a single speech on monetary policy and inflation in their almost five years in office. The Board is stacked with underqualified mates of the previous government – a couple appointed despite, at the time, clear conflicts of interest, suggesting that not only the previous Minister but also the Governor and the board chair have at best a hazy sense of high standards in public life. Hardly anything is ever heard from the Governor on inflation – speeches from him on climate change are more common than those on the conduct of monetary policy. The Reserve Bank publishes little research, and is a bloated top-heavy regulation-fond expensive bureaucracy.

Not all of those failings could be fixed overnight even if the new government were so minded. The problem is that there is no sign at all that they are seriously interested in fixing any of them. This from a Minister and Associate Minister who did not support the reappointment of the Governor – a serious step for them to have taken then, but apparently meaning little now. There is no hint also that the Minister is going to reopen the selection process for the two external MPC roles falling vacant early next year. If she simply takes nominees who got through the Orr/Quigley/Board and Board recruitment agency process undertaken earlier this year, under the broad aegis of the previous government’s priorities/views, it is a recipe for things being no better in future. Either the nominees she is presented with will be amiable non-entities happy to be guided by the Governor, or (at best perhaps) people who were willing to keep their heads down and say not a discouraging word through the last four years of central bank failure.

Perhaps I’m being too critical too early? But if the Minister is at all serious about things being done differently in and by the Bank, yesterday’s speeches would have been a great (and easy) opportunity to have signalled something. It also hasn’t been too early for some other ministers to have written letters of expectation to agencies for which they are responsible, making clear the new government’s priorities around those agencies. But there seems to have been nothing from Willis.

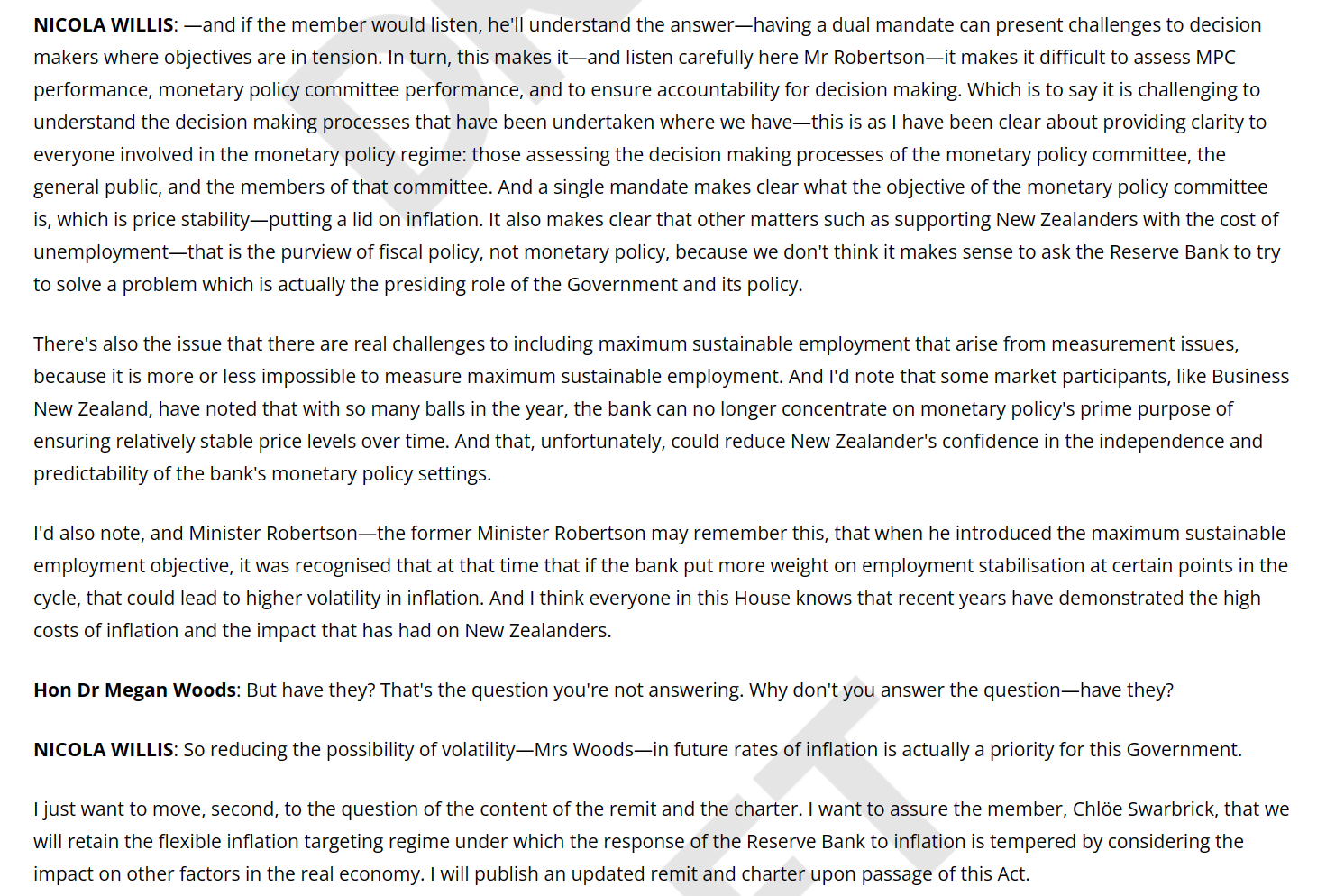

Instead we get examples like this of her economic thinking

As economic thinking, the final sentence is a little embarrassing. There is little or no reason to suppose that there is any medium to long relationship (positive or negative) between the inflation rate and the unemployment rate (or “maximum sustainable employment”). One can have highish inflation and (sustainably) low unemployment or one can have low inflation – even price stability – and (sustainably) low unemployment. The record – across countries and across time – is pretty clear. But inflation – and especially unexpected bursts of inflation – is something the public dislikes, and for good reason. Getting and keeping sustainably low average rates of unemployment should be an important concern for governments, but Reserve Bank monetary policy has little or nothing to do with such outcomes.

Unfortunately there is quite a lot of muddled thinking around monetary policy and the expression of objectives. I could only agree with this line in the Minister’s first reading speech

Flexible inflation targeting, whereby the MPC has regard to the impact of monetary policy on the broader economy when determining how quickly to return inflation to target has been central to New Zealand’s successful inflation targeting regime for many years, and was the case prior to Robertson’s dual mandate hitting the books, regardless of whether there is a single or dual mandate, that remains the case.

and in fact giving expression to that generally shared understanding was one of the motivations for Labour’s legislative change in 2018. But, of course, the issue was never primarily about demand shocks and forecasting errors – like those of the last few years – that delivered us high inflation and unsustainably low inflation at the same time. Failures on the scale we’ve seen recently were simply never envisaged (and should never have happened). By contrast, supply shocks – that tend to drive headline inflation one way and unemployment the other way – aren’t infrequent at all and were always actively envisaged in the design and modification of Policy Targets Agreements over they years. In the face of such shocks it has always been the shared, usually expressed, understanding – and this dates all the way back to the oil shock in 1990 just a few months into the life of the 1990 Act – that faced with such shocks it would generally not be sensible or prudent to attempt to counter the direct price effects immediately, and that to do so would involve unnecessary and undesirable employment and output costs. There isn’t much of a sense of this in the Minister’s speeches – perhaps understandably as it veers to the geeky – but it is important nonetheless.

Finally, approaching the end of this post I wanted to offer a few thoughts on the Treasury’s Regulatory Impact Statement on the removal of the “dual mandate” from the Reserve Bank Act. At five pages long it is perhaps the best advert for the government’s decision not to require RISs for early pieces of legislation that are simply repeals. It leaves readers no better informed on the issues, offers no serious analysis, and actually muddies the ground in places. On the latter, for example, it correctly notes that Reserve Bank and Treasury view that the different mandate made no difference to policymaking over 2019 to 2023 (when the dominant shocks were understood to be demand shocks, likely to affect core inflation and unemployment in the same direction) but simply never engages on supply shocks (see previous paragraphs) or the flexibility long built into both central banking practice and the succession of Policy Targets Agreements. Since the political debate has further muddied this water – reinforced by half-baked media lines (of the sort I heard on RNZ this morning – it might be desirable for the new MPC Remit to make some of this stuff explicitly clear. There are short-term tradeoffs, but no long-term ones.

The RIS also repeats and endorses – and perhaps fed the Minister – the line that price stability is a “prerequisite” for achieving other objectives. It simply isn’t, and Treasury really should know better than to indulge what is not much more than misleading political rhetoric.

In RIS it is customary – perhaps even required – to look at three different ways of responding to the identified “policy problem”. The artificiality of this was never better displayed than in the Treasury RIS, in which they treat as a serious option using the reserve powers in the Act allowing the Minister of Finance to override temporarily the existing statutory economic objective, rather than amending the Act. Unsurprisingly, they recommend against using these never-used (dusted off for refreshing the memory every decade or so), which should never have been considered as an option in the first place – as not only would the market signalling have been terrible, but it would have gone quite against the direction the government was seeking (a permanent change).

Treasury ended up opposing the government’s legislative change, preferring to change just the MPC Remit (which the Minister can do pretty much any time he or she likes). Their only argument for this – eg they don’t seem to invoke any argument about reminding readers of statute of the wider context, or even that it is the Remit not the Act that is supposed to guide the MPC – seem to be a preference not to amend the Act (as if not amending the Act was a good in and of itself). They say “Treasury puts significant weight on the value of a stable and enduring legislative regime for the Reserve Bank” which (a) is weird coming immediately on the back of several years of extensive legislative overhaul around the Reserve Bank, (b) could be as easily seen as an argument for the government’s legislative amendment, which is closer to the “stable and enduring” legislative model that prevailed for almost 30 years, and (c) assumes recent reforms generally got things right, when there are clearly significant problems with the way the Reserve Bank Act reforms were done (including but not limited to making the underqualified board, which has no expertise in monetary policy, primarily responsible for holding the MPC to account and in appointing MPC members and the Governor).

Finally, Treasury seeks to invoke “international best practice” in defence of retaining Labour’s wording. In respect of legislative (or similar wording) they are simply misleading. All four of the most important advanced country central banks – Fed, ECB, Bank of Japan, and Bank of England – have a single statutory objective, even if often accompanied by wording designed to articulate something of why price stability matters. It is certainly true that some central banks have more explicit “dual mandate” wording and others talk openly about the interactions between inflation and employment, sometimes in “dual mandate” terms, but there is nothing out of step with the legislative amendment the government is putting through today. The Treasury explicitly tries to cite the US in its support, but while the Fed likes to talk “dual mandate” rhetoric, its actual statutory objective for monetary policy is (a) a single objective, and (b) one with very outdated – legacy of the 1970s wording.

“So as to” are the envisaged benefits of pursuing and achieving the specified single objective.

It was simply far from being Treasury at its finest, and if time was short there was no obstacle to writing a much better short paper.

As for the government it is early days, but the early signs are not great around the Reserve Bank. I’m quite prepared to believe the new government won’t accommodate more institutional bloat, and that their appointments will be no worse than those of their predecessors, but for now there are no signs leading a reasonable independent observer to expect anything much better about fixing the Reserve Bank (or our diminished Treasury for that matter).

UPDATE:

This is from a speech by the minister at the committee stage

The problem is that she contradicts herself. There are forms of inflation targeting where accountability might be really easy – any time CPI inflation is outside the target range, sack the Governor – but everyone has been agreed for 30+ years that that would not make sense and would generally produce inferior economic outcomes. In fact, the Minister herself agree because she is at pains to point out that the flexible form of inflation targeting (operated for the first 30 years) will be retained. In such a system it is not easy or mechanical to be able to exact accountability. These things -as so often in life – require judgement, and a willingness of ministers to exercise such judgement and, on rare occasions, act accordingly. Grant Robertson failure to do anything – and his decision to reappoint Orr and the 3 externals – is what made him party to their (central bank) failure.

It doesn’t seem to have been the best week for the Reserve Bank since the release of the latest Monetary Policy Statement last Wednesday. Of course, one could make a pretty compelling case that in the Orr years few weeks have been, and especially not any weeks when Bank figures actually say or do anything. But for now we’ll focus just on the last week.

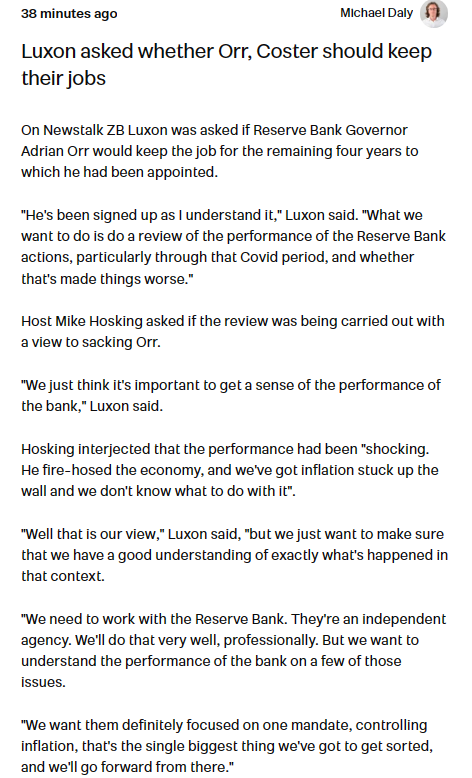

On the one hand there was some pretty clear pandering by the Governor to the instincts and preferences of the new government. There is nothing like losing $12 billion dollars of taxpayers’ money and delivering several successive years of core inflation well above target – with no contrition on either count – to suggest past loss of focus and energy, but we learned from the Herald that

The PM said that during his conversations with Orr on Tuesday he was pleased to hear the governor’s “obsession” with lowering inflation.

If that was really Orr’s word – and it isn’t entirely clear from the story whether it was his word or the PM’s take – and he really meant it (as distinct from just indulging in loose rhetorical pandering) it would be more than a little concerning, when central bankers (New Zealand and abroad) have been at pains for decades to explain that having an inflation targeting regime does not mean they are (in their own words) “inflation nutters”. There are many many examples, in formal literature and less, from here and abroad, but as just one local example this article from Orr’s time as the Bank’s chief economist back in the (allegedly hardline, but always actually quite flexible) Brash years. I don’t think Orr was actually serious about the “obsessive” bit, because when he was asked about inflation in the MPS press conference he was at pains to explain – sensibly – that if there were forecasting errors around how quickly inflation comes down they simply couldn’t be sensibly corrected immediately (lags and all that). But it speaks of a Governor who is simply not a nuanced and serious communicator (consistent with the near-complete absence of speeches from him on monetary policy, through a period of serious policy failures).

In his remarks last week Orr also seemed to be getting on side with the government’s stated intention of legislating to restore the statutory goal for monetary policy to price stability, noting that the Bank’s own work on the Remit review had suggested a more prominent place for the price stability goal. That was all fine, and Orr has been pretty clear all along that Labour’s change to the goal in 2018 had not made any material difference to monetary policy decisions in the last few years, and the Bank – under successive Governors (and chief economists) – has long championed its (internationally standard) flexible inflation targeting approach.

But then the current chief economist was let loose and in remarks to Newsroom is reported under this headline

as having said

which is an astonishingly loose comment from someone paid hundreds of thousands of dollars a year and holding a statutory office as an MPC member. It is no doubt true that one could set up a highly-simplified model in which some arbitrarily chosen reaction function to some specific types of shocks might end up with (temporarily) higher unemployment under one specification of the statutory target than the current one. But….not only would there be other shocks in which unemployment would be (temporarily) lower (when both inflation and unemployment are low), but there is no sign of any work or thought on whether such shocks are at all frequent, or how they were actually dealt with under the statutory goal in place here for the best part of 30 years. And, notwithstanding Conway’s comment, the monetary policy decisions that matter are almost never easy, precisely because they are about uncertain futures. Take the last time core inflation was well away from the target midpoint – in 2008 – and check how many times the Reserve Bank was tightening then. It wasn’t, of course, and was right not to have done so (whatever mistakes it (we) might have made in the previous couple of years). It might be interesting for someone to OIA the Bank and ask what evidence they have for Conway’s claim that the planned legislative amendment will result – even “at the margins” – in higher unemployment.

But all that was general high level policy frameworks stuff. What about actual policy and outlook.

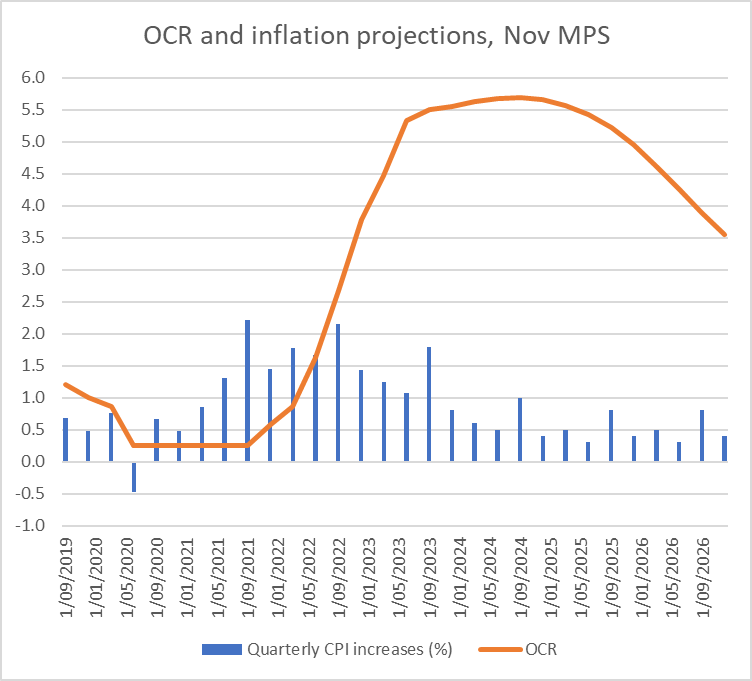

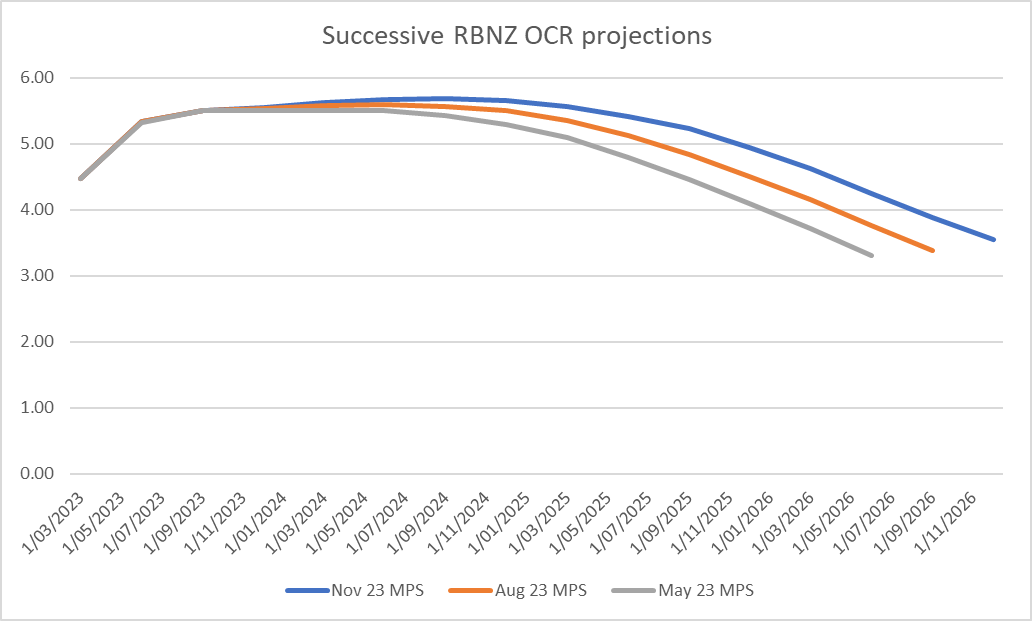

In the MPS – which the Governor described as “a wonderful wise document” – the Reserve Bank again revised upwards their future track for the OCR, lifting both the peak of the track (to the point where they reckon there is a better than even chance of another OCR increase next year) and increasing quite materially the extent to which they expect interest rates will have to stay high. The further out projections have been lifted by about 50 basis points, coming on the back of similar increases at the previous MPS.

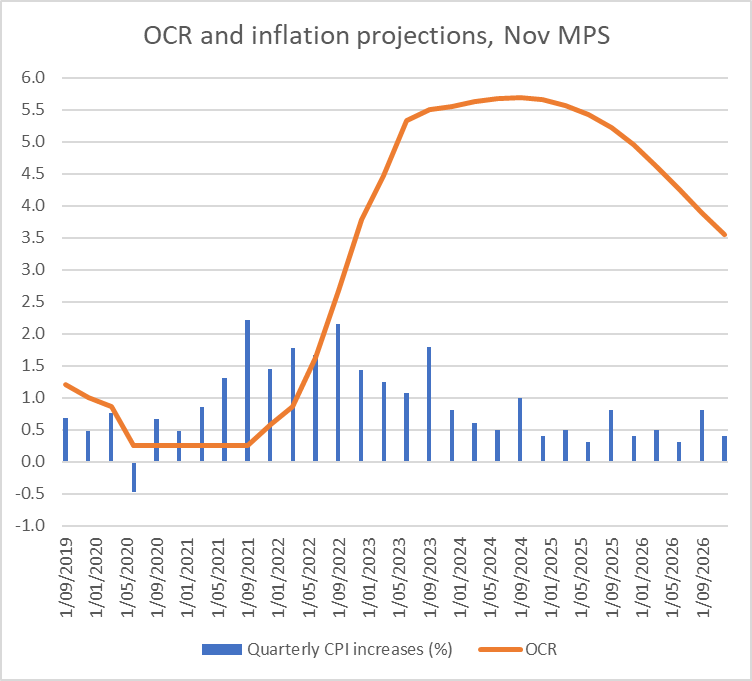

But here is the most immediate problem (from a tweet last week).

Much of the media comment focuses on annual rates of inflation. The Reserve Bank projections have annual inflation finally dropping into the target 1 to 3 per cent range – although still a considerable way from the 2 per cent midpoint the Bank is required to focus on – for the year to September 2024. Even that isn’t far away now, but in thinking about policy it is typically more useful to be looking at the projections for quarterly percentage changes in the CPI.

There is some seasonality in the CPI (September quarters are typically much higher and the other quarters a bit lower than average). Unfortunately the Reserve Bank does not publish its inflation forecasts in seasonally adjusted terms, but on this occasion eyeballing does fine. You can see not only that ever quarter in 2024 has quarterly inflation at about half what it was for 2023, and as early as the June quarter of next year (mostly measured as at mid May, so only five months away) the headline quarterly CPI increase is projected to be already 0.5 per cent. By the December quarter of next year, the quarterly CPI increase is explicitly consistent with annual inflation of 2 per cent.

And how long does monetary policy take to have its largest effects? Views differ but the standard Reserve Bank line – the reason why the Governor suggested that if they are wrong about September 2024 they can’t sensibly immediately fix things – is something like 18 months. Even if it is as short as 12 months, those inflation outcomes next year in the Bank’s projection are the result of the current OCR, not a possible increase next year. And those outcomes are entirely consistent, on a quarterly basis by next November at the latest, with the midpoint of the inflation target range.

So why would you publish projections now showing a further OCR increase next year, and no cuts below the current 5.5 per cent until mid 2025 when (a) your best projections (presumably) are that quarterly inflation will be at target next year, and (b) your routinely repeated view is that monetary policy takes perhaps 18 months to have its main effect on inflation? If anything, that looks like a recipe for keeping the unemployment rate – not expected to peak, at above 5 per cent until mid 2025 – a bit higher rhan otherwise “at the margin”.

One possibility was that it was all just about “jawboning”. In the MPC’s view markets were getting a bit over-enthusiastic looking for the first rate cut so perhaps the track was pushed up and out a bit to send a message (and yes, late messaging changes to interest rate tracks do happen). But…..even if that had been the case, why wouldn’t you also have pushed up the inflation track? After all, the Reserve Bank’s inflation projections (see chart above) show a really sharp collapse in quarterly inflation rates, starting right about now.

But two members of the MPC have been sent out to assure us, via different media outlets, that no, the Reserve Bank was dead serious, and it was not (in a Post article reporting comments from Conway) “talking tough for effect”, or (in a Herald interview with the Deputy Governor) that there were no games going on and “our messages are genuine”.

If genuine, then incoherent. If inflation is doing anything like what the MPC’s own published inflation projections are suggesting (ie very quickly now getting back to target), there is no credible case for keeping the OCR well above (assumed) neutral for the indefinite future, and not cutting at all until mid 2025.

(To be clear, I am not and never have been a fan of published central bank interest rate projections, or any medium-term central bank forecasts – the state of knowledge is so limited that anything is more about messaging and game playing than any real information – but it is the MPC that chooses what it publishes.)

The story really doesn’t add up. Nor is it particularly compelling to suddenly start playing up fiscal pressures on demand (nothing having changed on the expansionary side around fiscal policy settings since the May Budget, and the Governor repeatedly played down demand effects in May and August – when it suited the government of the day for him to have done so). One could say something about immigration pressure (when the huge surge in net non-citizen arrivals has been evident for many months) altho the near-term estimates of the inflow have been increased.

But that big shock – the additional net arrivals – has already happened (quarterly this year), and yet the MPC tells us the think the inflation rate is just about to collapse, on current monetary settings.

Up to this point I have not taken a view on whether the Reserve Bank’s inflation forecasts are likely, just highlighting the tension between what are really quite rosy inflation projections, and that OCR forecast track – and the rhetoric- which is anything but.

The Reserve Bank has also been at pains to make the (obvious) point that they have to set monetary policy in the light of the New Zealand inflation outlook and that whatever is going on in other countries is not necessarily a great guide to what will be required in New Zealand. Which is all true, but…..much of what has gone on around inflation in the last three years has been fairly common to a whole bunch of advanced countries. There were, of course, the largely common supply shocks – ups and downs of oil and freight prices etc – but more importantly excess demand pressures, and extremely stretched labour markets, also became apparent in many countries. And if our fiscal policy looks to have been a bit more expansionary than in most, the biggest demand effects of that seem set to have been in 2022 and 2023 rather than beyond. The surge in immigration has certainly been huge – and my standard model for a decade has emphasised the positive net short-term demand effects from migration but (a) similar things have been seen in Australia and Canada, and to a lesser extent in countries like the UK, and (b) the Bank’s forecast assume quite a sharp slowing (annual net immigration next year is forecast at half the rate of this year.

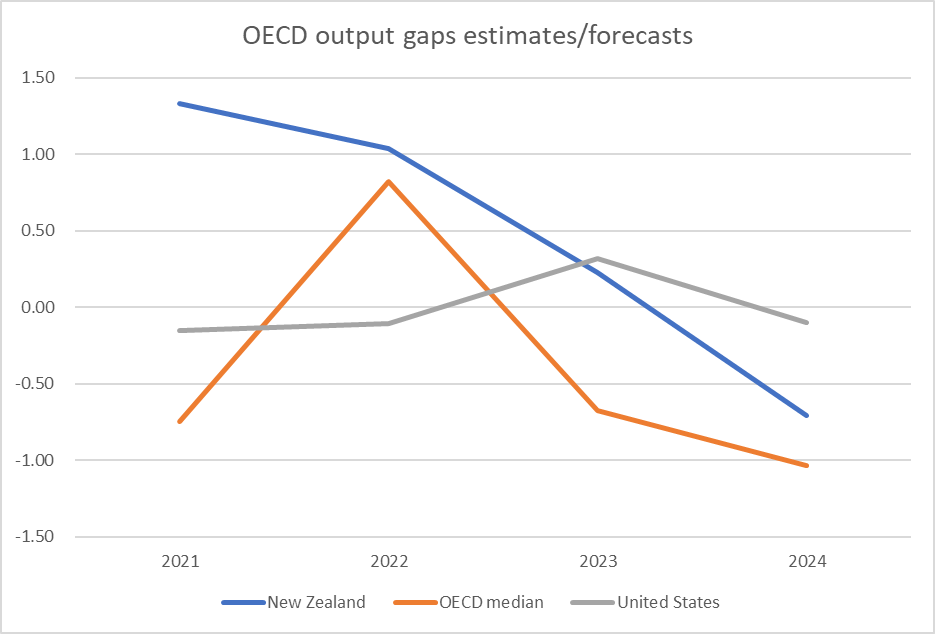

In a post a few weeks ago I highlighted that on IMF estimates New Zealand had had the biggest excess demand (positive output gap) problem of pretty much any advanced country. If so, that would be a reason for caution, why inflation might be tougher to beat here than elsewhere (and it is true that our OCR is only around those of other countries, whereas in most past cycles it has had to go higher). But the OECD’s recent forecasts, out last week, suggest a picture that has New Zealand’s experience closer to the pack for this year and next.

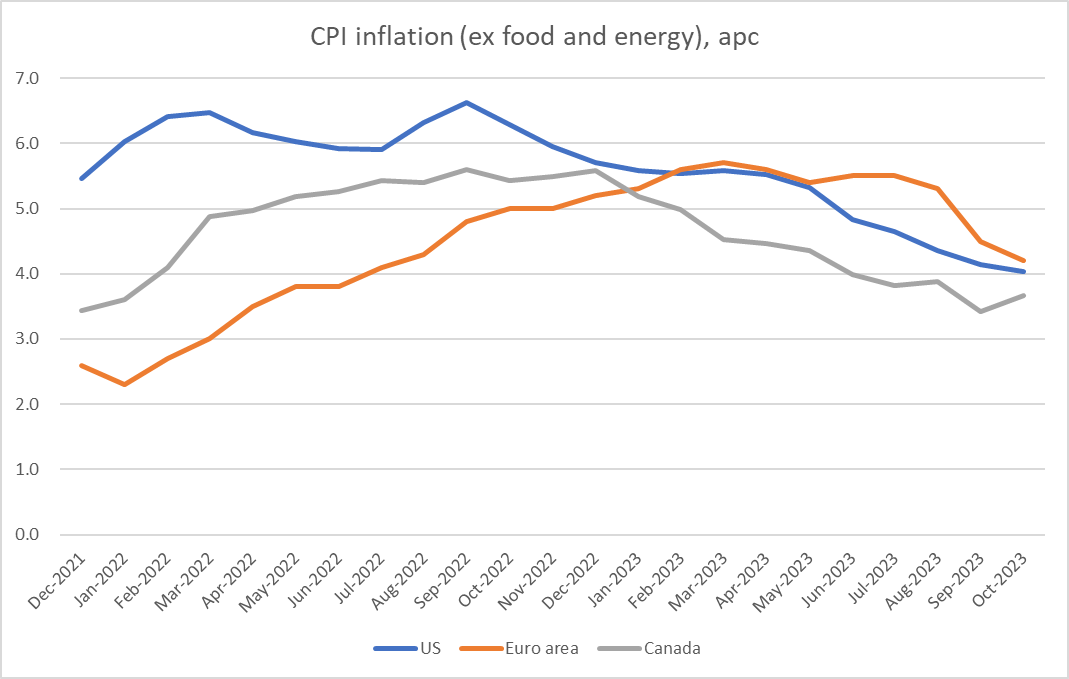

What has happened then to (core) inflation in other advanced economies?

There are positive stories (US and euro area getting a fair number of headlines)

Each of those current annual inflation rates are materially below New Zealand, and the quarterly/monthly data are often more favourable.

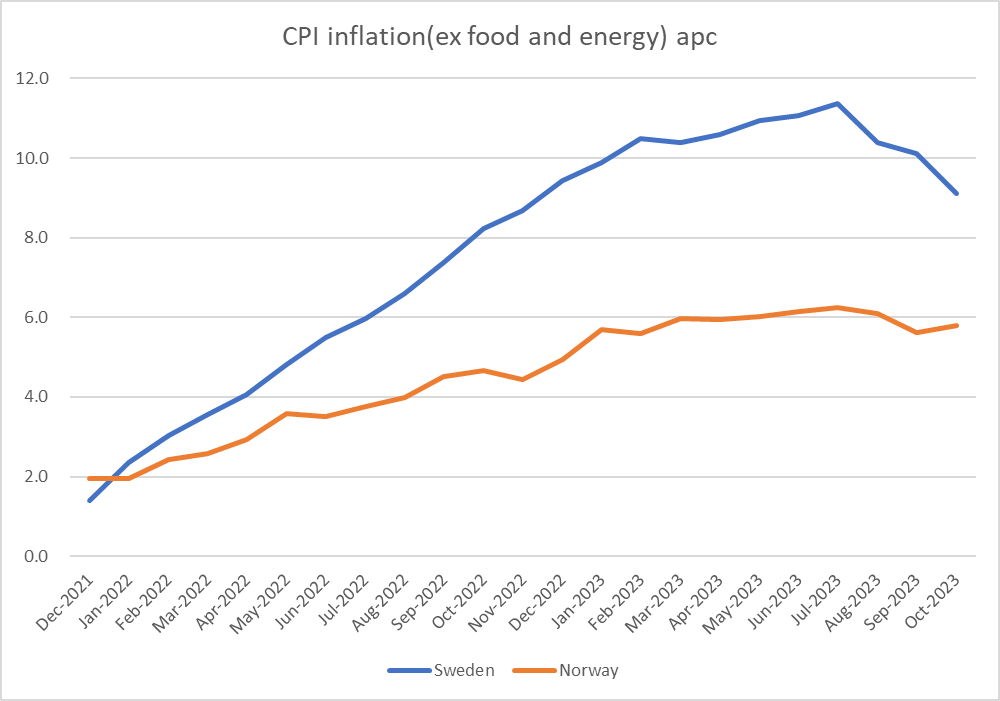

In the Nordics, perhaps a mixed picture

but even then if one looks to the Norges Bank’s core indicators things seem to be heading in the right direction.

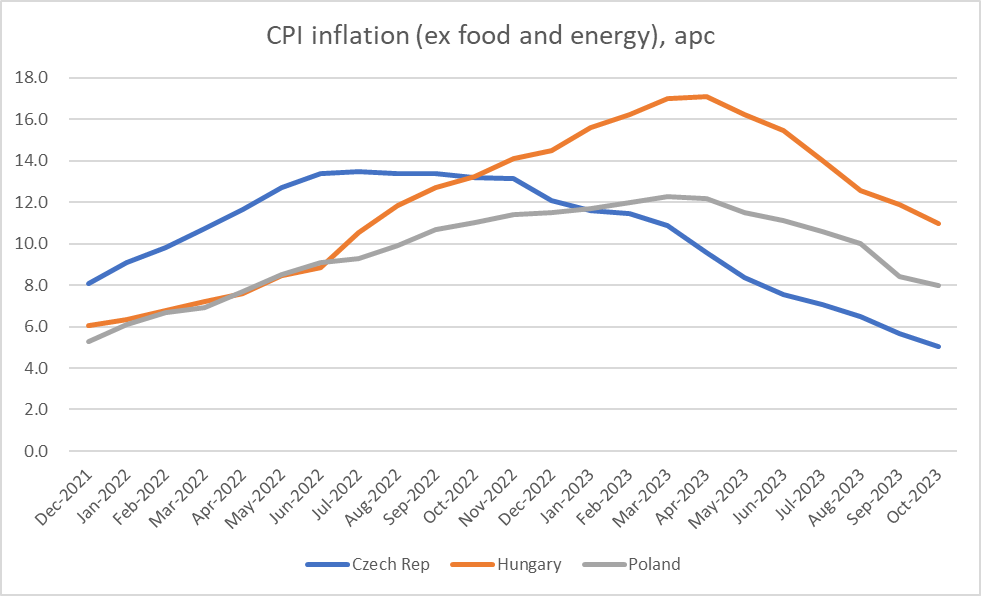

And even in the central European countries there has been a big reduction in core inflation (with a long way to go)

None of this is any guarantee that any of these countries will get to 2 per cent quickly, but the direction seems pretty clear, and it isn’t really obvious why it would suddenly become so much harder to cover the last mile. Nor, thus, is it really apparent why things will prove so much different here – when the RB itself tells us they think inflation is just about to collapse. It wasn’t as if there was any serious sustained analysis in the MPS itself to explain a) why the Bank expects inflation is on the brink of collapsing, or b) why they are really reluctant to believe their own numbers. Sure, the Governor was heard to mutter things about inflation expectations – even, bizarrely, suggesting that 10 year ahead numbers were some sort of personal blow, when we know the Governor will be gone in 4.25 years at most – but the best predictor now would have to be that if headline and core inflation fall away sharply, as the Bank tells us it expects, survey measures of inflation expectations will follow.

The Bank was in a slightly awkward situation last week, as neither they nor anyone else yet had (or has) a good sense of what the new government’s fiscal policy will mean (fiscal impulses etc) but that is no excuse for such an unconvincing set of stories on the data and evidence they do have. And of course now they have gone for the summer, with no speeches, no serious supporting analysis, just those strange plaintive lines from Messrs Conway and Hawkesby “no really, we are serious…..we really think inflation is to fall like a stone next year and yet we really think the OCR will have to stay this high or higher for the next 18 months”. It reflects poorly on the Bank, and should be just another set of evidence around the weaknesses of the Bank that one can only hope Nicola Willis will in time do something about.

But first a correction. As I noted on Twitter and very briefly on the post itself on Saturday, it seems that the gist of my post on Friday was wrong. The repeal of Labour’s tobacco de-nicotinisation legislation – whatever motivated the parties that championed the change – will leave the flow of tobacco excise revenue largely as it was, providing the government an extra flow of revenue – relative to what was allowed for in PREFU – that will, if anything, more than compensate for what National had told us they expected the foreign buyers’ tax would have raised. With the various other bits in the various coalition agreements they are probably back to being in roughly the – very demanding – fiscal situation National thought it would be facing before the election: large deficits, very demanding indicative operating allowances, and an aversion to cutting programmes/”entitlements”,

As for the impact of fiscal policy on aggregate demand, and thus the pressure on monetary policy, they’ve ended up – without really consciously trying, or so it seems, with a somewhat helpful policy switch; dumping the foreign buyers’ tax which was supposed to raise money from wealthy foreigners who mostly would not have been earning or otherwise spending that money in New Zealand (which revenue therefore would not have dampened demand) and replacing it with the reinstatement of the tobacco tax revenue scheme, mostly raising money from relatively low income New Zealanders who will, on average, have a very high marginal propensity to consume in New Zealand. Whatever the substantive merits (or otherwise) of either policy, all else equal the switch is slightly helpful for monetary policy.

A few days after the election I wrote a post “What should be done about the Reserve Bank?” itself if (as I put it in that post) a new government is at all serious about a much better, and better governed and run, institution in future. Perhaps unsurprisingly I stand by all the points in that post, around both individuals (Orr, Quigley, external MPC members, and so on) and the institution.

That post ended this way

That final paragraph was about the fact that unless he leaves more or less voluntarily it would be hard to get rid of Orr (judicial review risks etc and attendant market uncertainty) and yet it would be highly beneficial were he to be replaced well before March 2028.

Anyway, with the release on Friday of the two coalition agreements we know a little more re the options for the monetary policy functions of the Bank.

At a high level, both agreements commit the parties to make decisions that are “focused” to “drive meaningful improvements in core areas including

One might have briefly hoped that this might have resulted in the government lowering the inflation target to something actually consistent with price stability – eg, allowing for index biases, 0 to 2 per cent annual inflation – but it probably only means the abolition of the so-called dual mandate (something both National and ACT had campaigned). The specific material on monetary policy is from the ACT agreement

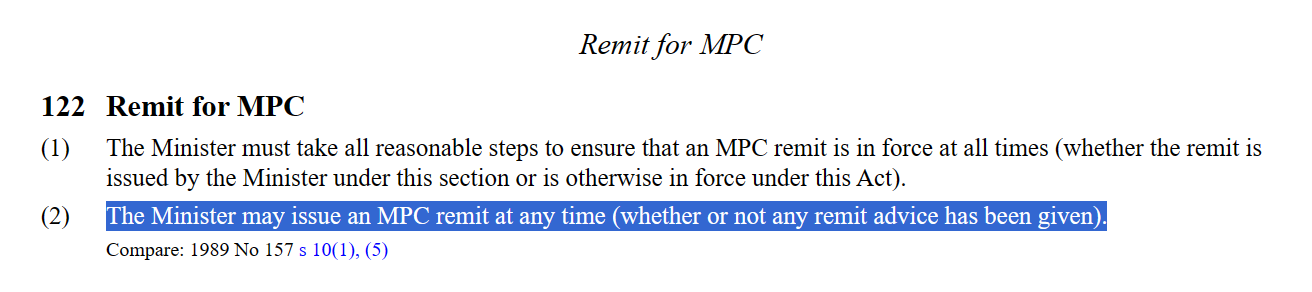

In National’s own 100 day plan the legislation to amend the statutory goal of monetary policy was to have been introduced – not passed – within the first 100 days, but in the coalition agreement there is no indication of the legislative priority. However, the Act makes it clear that the Minister of Finance could issue a new Remit – the actual targets the MPC is supposed to work to – at any time

It would be a simple matter of deleting one short paragraph from the Remit, which would then also have the appeal (to the government) of being clear that the MPC was working to this government’s Remit not the last government’s one. That doesn’t need to await the other advice, it could be done today or tomorrow (perhaps after the first Cabinet of the new government), and before the MPS on Wednesday. If the Minister moved that fast it would no doubt prompt specific questions at the MPS press conference, but…..they are going to be asked anyway. (UPDATE: The Minister is required to consult (but not necessarily have regard to the views of) the MPC before issuing a new Remit, so the next day or two probably isn’t an option, but it need not be an elongated process when the government has a clear electoral mandate for change.)