It must be relatively unusual for a political party in office to change tax law, and provide extra budget funding, to enable research to be done towards that party’s next campaign manifesto. But such it appears to be with the High-wealth Individuals research project, the report on which was released yesterday, loudly championed by the Minister of Revenue, David Parker. Not many government department research papers – and that, we are told, is all it is – get a Foreword from a senior Cabinet minister.

Whether or not there was a strong case for doing the research in the first place using the coercive powers of the state, and whether there is – in the broad – anything very surprising in the report (I don’t think I’ve yet seen/heard anything), no doubt there will interesting tables and charts that flesh out our understanding of the selected facts at least a little.

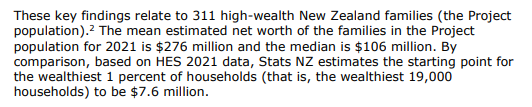

Perhaps the first snippet worth paying attention to is this

That is quite a lot of money in total – measured, by chance, at the very peak of a huge asset price boom – but what struck me was that only 155 families had estimated net worth in excess of $106 million. Quite possibly no readers of this blog fit that category, but in the grand scheme of global wealth NZ$106 million (measured at the peak of an asset boom) was if anything less than I might have expected.(By contrast, at his talk yesterday Parker told us he’d asked some of his rich mates to guess what the average number would be and none had gone for a high enough number).

Perhaps not unrelatedly, it is worth remembering that we don’t tax families, we tax individuals, and most of the families studied in this report included two spouses/partners. The median individual wealth is going to have been quite a bit lower than $106 million.

All of which seems consistent with the fact that the New Zealand economy has not exactly been a staggering success in recent decades. Setting the tax debate to one side for the moment, in a successful economy one might have hoped that there would be many more really wealthy families, at least if that wealth had arisen from the creation and development of new businesses/products. Few begrudge Bill Gates the wealth created via Microsoft.

But there is some important stuff that wasn’t in the report, or in the political framing of it. Thus, David Parker made much of the poor put-upon wage and salary earner who pays tax on every dollar of earnings, in contrast to the 300 rich families. It was all such an evidently unfair system we were told.

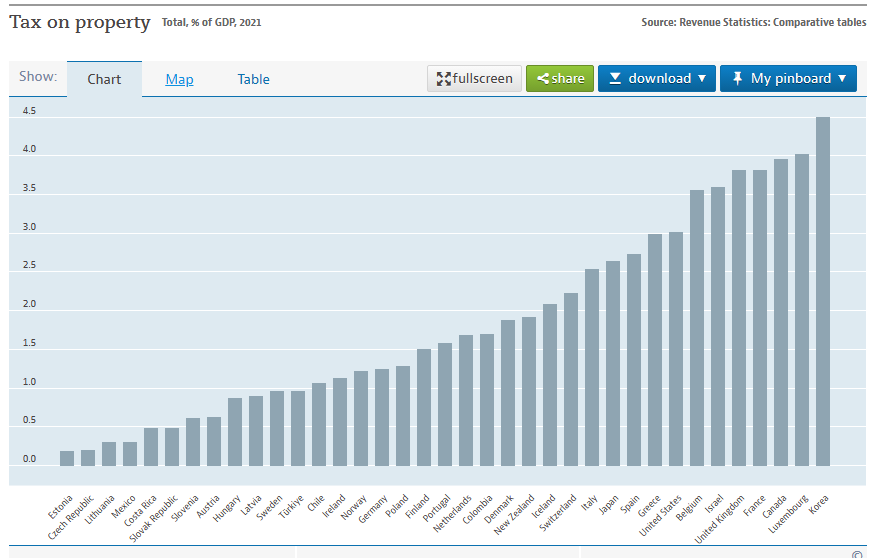

There were some comparative OECD charts in the minister’s presentation. These two weren’t among them

Tax on property – as a share of GDP a bit above the OECD median – is defined here as

This chart was also missing (NZ second from the right). It includes any tax levied on business capital gains.

And, of course, in the minister’s framing there was no mention of the fact that New Zealand over the decades has had relatively low rates of investment (relative to OECD averages for countries with our sort of population growth) in land development, in building new houses, and in business investment more generally. What one aspires to have more of one generally should not seek to tax more heavily. And IRD even seems to recognise in the report that what one taxes more heavily one will get less of, noting in the Summary

For the Project population, much of their income is derived from business entities that they control. Failing to tax forms of income that are earned predominantly by those who are better off …… is also likely to impose other economic costs through influencing the pattern of investment in the economy.

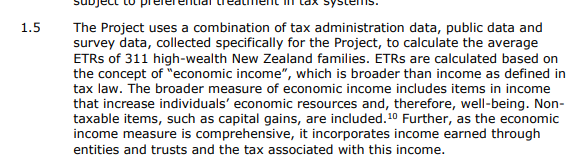

The IRD is keen to assert that what they are doing in this study is measuring “economic income”, in their own words “items…that increase individuals’ economic resources and, therefore, well-being”

In principle that is fine. I have no problem with the notion that unrealised real capital gains add to the economic resources and future purchasing power of the owner (whether or not those gains should be taxed is quite another question). But increases in asset values that simply keep pace with general inflation do not add to future real purchasing power and are in no meaningful economic sense (including the Haig-Simons approach IRD is fond of) economic income. We don’t have an inflation-indexed tax system at present, but the point of this study was not to describe the current system, but to use analytical tools to get a sense of real gains to purchasing power.

Now, most capital gains in the period under study were well in excess of the general CPI inflation rate, and inflation itself was relatively modest (but inflation cumulates, and even 2 per cent per annum inflation is about 22 per cent in total over a decade), so adjusting for inflation – which could relatively easily have been done – might not have changed many of the headline-grabbing numbers very much. But it was just knowingly dishonest of IRD not to have made the adjustment and to have presented as real income what no economist will regard as real income. But it will have suited their political masters (and perhaps reflected their longstanding institutional unease with an indexed tax system). And, as readers will be well aware, inflation will have made a great deal bigger difference to the numbers for 2022 and 2023.

David Parker’s approach to tax is – perhaps in line with prevailing New Zealand orthodoxy in recent decades – that all forms of real economic income should be taxed alike (at his talk yesterday he even seemed attracted to a capital gains tax on unrealised gains, something I’m not aware that any country does on any sort of comprehensive basis). If you believe in that approach, I guess yesterday’s research results will be troubling (or grist to your political mill).

I don’t, and to the extent it matters (if one cares about productivity and wider economic performance over time) generally economic theory tends not to back such an approach either. Not only do I think there is a good case for taxing returns to labour much more heavily than returns on capital (one example of my advocacy is here) but there is also a good case for a consumption-focused approach to tax (tax people on what they spend not on what they produce/earn, ideally through a progressive system). Frame your research in terms of tax as a percentage of “economic income” and you will get one set of answers, but frame it as a percentage of consumption and you will get quite another. If I was looking for a “tax switch” in New Zealand – David Parker implied that he was, rather than looking to increase total revenue – I’d be looking to substantially reduce New Zealand’s ranking on that taxation on corporate income chart above (and yes, I do know about dividend imputation, so this isn’t a statement of detail but of direction – but more foreign investment, and foreign investors are most affected by NZ company tax rates, would generally be a good thing).

For all that, I am not one of those who is adamantly opposed to a capital gains tax in principle. It wouldn’t affect me personally, I don’t mix in the circles of the 300, and I fully accept that there are elements of a “fairness” argument to be had. I’m certainly not someone who would change my vote on the matter. In general, I summarise my CGT position as one of profound ambivalence. One could be put in place, but a well-designed and politically realistic one would not raise much revenue over time, all while adding to the structural procyclicality risks around fiscal policy (sucking in most revenue when revenue is abundant and drying up almost completely when times are tough and other revenue is depleted). And since most of the political angst around capital gains in New Zealand is not about the likes of Bill Gates (or Rod Drury) but about escalating land values, those issues could – and should – be dealt with directly by systematically freeing up land usage and collapsing the artificial scarcity central and local government restrictions have created. As it happens, in this government the minister of land use rules in also the Minister of Revenue, but does one hear David Parker advocating policies that would collapse peripheral urban land prices to the best alternative agricultural use price? No, he (and opposition parties) will run a mile for the very idea) and experts tell us that the legislation he is now piloting through the House may actually worsen the situation. The rigged land market is scandalous, a true moral evil. But governments refuse to fix that.

And then there is the political conundrum. Most real-world CGTs emphasise realised gains, but if you do that then the people you hit are the asset holders most likely to be forced to sell at some point. As Parker himself recognised, the richer you are – and the bigger vehicles you hold your wealth in – the more likely you are to be able to defer a CGT almost indefinitely. In his younger days, Adrian Orr used to regale us with tales of mates of his who were firemen (or the like) with a couple of investment properties. A realisations-based CGT – actually like the extended brightline test – will catch them, but it will bear much less heavily on Parker’s 300 families.

Perhaps that means Parker will be trying to get his Labour colleagues to run with a wealth tax or death or inheritance taxes. They don’t have the particular problems that go with a CGT, but they have others (personally, I have no real problem with a moderate inheritance tax with fairly high thresholds, but I’d be really surprised if such a tax were to raise much money – although perhaps for advocates the revenue would not be the point).

Rather than run through afresh all the issues around good CGTs – loss-offsetting, double-taxation, efficient markets approaches to asset pricing etc – I’m going to end by cutting and pasting from a 2017 post, which I also used when the TWG reported in 2019.

Rather the block quote it, all that follows to the end of this post is direct from that 2017 post:

Going through some old papers to refresh my memory on capital gains tax (CGT) debates, I found reference to a note I’d written back in 2011 headed “A Capital Gains Tax for New Zealand: Ten reasons to be sceptical”. Unfortunately, I couldn’t find the note itself, so you won’t get all 10 reasons today. But here are some of the reasons why I’m sceptical of the sort of real world CGTs that could follow from this year’s election. Mostly, repeated calls for CGTs – whether from political parties, or from bodies like the IMF and OECD – seem to be about some misplaced rhetorical sense of “fairness” or are cover for a failure to confront and deal directly with the real problems in the regulation of the housing and urban land markets.

Anyway, here are some of the points I make:

- in a well-functioning efficient market, there are typically no real (ie inflation adjusted) expected capital gains. An individual participant might expect an asset price to rise for some reason, but that participant will be balanced by others expecting it to fall. If it were not so then, typically, the price would already have adjusted. In well-functioning markets, there aren’t free lunches. It also means that, on average, capital losses will be pretty common too, and thus a tax system that treated capital gains and losses symmetrically wouldn’t raise much money on average over time. A CGT is no magic money tree. And there is no strong efficiency argument for taxing windfalls.

- if you thought, for some reason, that people were inefficiently reluctant to take risk, there might be some argument for a properly symmetrical CGT. In such a system, the government would take, say, a third of your gains, but would also remit a third of your losses (the overall risks being pooled by the state). The variance of an individual’s private after-tax returns would be reduced, and they might be more willing to take risk. But, in fact, no CGT system I’m aware of is properly symmetrical – there are typically tough restrictions on claiming refunds in respect of capital losses (one might only be able to do so by offsetting them against future gains). There are some reasonable base-protection arguments for these restrictions, but they undermine the case for a CGT itself.

- All real world CGTs are based on realised gains (and losses to an extent). That makes it not a pure CGT, but in significant part a turnover tax – if you never trade, you never pay (“never” isn’t literal, but tax deferred for decades discounts to a very small present value). And that creates lock-in problems, where people are very reluctant to sell, even if their circumstances change or if a new potential owner could make much more of the asset, for fear of crystallising a CGT liability. In other words, introducing a CGT introduces a new inefficiency to asset markets, making it less likely that over time assets will be owned by the parties best able to utilise them.

- Basing a CGT on realised gains will also, over time, bias the ownership of assets subject to CGT to those most able to avoid realising the gains. A long-lived pension fund, or even a very wealthy family, will typically be better able to count on not having to sell than, say, an individual starting out with one or two rental properties, or some other small business, where changed circumstances (eg a recesssion or a divorce) might compel early liquidation. Large funds are also typically better able to take advantage of loss-offsetting provisions. The democratisation of finance and asset holding it certainly isn’t.

- CGTs in many countries exclude “the family home” altogether. In other countries, they provide “rollover relief”, enabling any tax liability to be deferred. Most advocates of a CGT here seem to favour the exclusion of the family home, even though unleveraged owners of family homes already have the most favourable tax treatment in our system. Again, a CGT applied to investment properties but not owner-occupied ones would simply trade one (possible) distortion for another.

- In practice, most of the arguments made for a CGT in New Zealand have to do with the housing market. But, on the one hand, all major (and minor?) parties claim that they have the fix for the housing market (various combinations of RMA reform, infrastructure reforms, changes to immigration, restrictions on foreign ownership, state building programmes or whatever). If they are right, there is no reason to expect significant systematic real capital gains in houses. If anything, real house prices should be falling – a long way, for a long time. Of course, prices in some localities might still rise at some point, if unexpected new opportunities appear. But “unexpected” is the operative word. Enthusiasm for a CGT, at least at a political level, seems to involve a concession that the parties don’t believe, or aren’t really serious about their housing reform policies.

- Oh, and no one I’m aware of anywhere argues that a realisation-based CGT applied to (a minority of) housing has made any very material difference to the level of house prices, or indeed to cycles in house prices.

- In general, capital gains taxes amount to double-taxation. Think of a business or a farm. If the owner makes a success of the business, or product selling prices improve, expected profits will increase. If and when those profits are achieved, they would, in the normal course of affairs, be subject to income tax. The value of the business is the discounted value of the expected future profits. It will rise when the expected profits rise. Tax that gain and you will be taxing twice the same increase in profits – only with a CGT you tax it before it has even happened. Of course, at least in principle, there is a double deduction for losses, but as noted above utilising losses (whether of income, or capital) is a lot more difficult. If you think that New Zealand has had less business investment than might, in some sense, have been desirable, you might want to be cautious about applauding a new tax that would fall heavily on those who took business risks and succeeded.

- Perhaps double taxation of expected business profits doesn’t bother you. But trying reasoning by analogy with wages. If the market value of your particular skills has gone up, your wages would be expected to rise. When they do you will pay taxes on those higher wages. But by the logic of a CGT, we should capitalise the value of your expected future labour income and tax your on both that “capital gain” and on the later actual earnings. Fortunately, we abolished slavery long ago, but in principle the two cases aren’t much different: if there is a case for a CGT on the value of a business, it isn’t obvious why one shouldn’t have one on the value of a person’s human capital.

- (I should note here, for the purists, that there are other concepts of double-taxation often referred to in tax literature, none of which invalidate the point I’m making here.)

- Real world CGTs also tend to complicate fiscal management? Why? Because CGT revenue tends to peak when asset markets and the economy are doing well, and when other government revenue sources are performing well. CGT revenue doesn’t increase a little as the economy improves and asset markets increase, it increases multiplicatively. And then dries up almost completely. Think of a simple example in which real asset prices had been increasing at 1 per cent per annum, and then some shock boost asset prices by 10 per cent. CGT revenue might easily rise by 100 per cent in that year (setting aside issues around the timing of realisations). And then in a period of falling asset prices there will be almost no CGT revenue at all. Strongly pro-cyclical revenue sources create serious fiscal management problems, because in the good times they create a pot of money that invites politicians to (compete to) spend it. If asset booms run for several years, politicians start to treat the revenue gains as permanent, and increase spending accordingly. And if/when asset markets correct – often associated with recession and downturns in other revenue sources- the drying up of CGT revenue increases the pressure on the budget in already tough times. It is easy to talk about ringfencing such revenue (mentally, if not legally) but such devices rarely seem to work.

None of this means that I think there is no case for changes in elements of our tax system as they affect housing. The ability for business borrowers to deduct the full amount of nominal interest, even though a significant portion of that interest is simply compensation for inflation (rather than a real cost), is a systematic bias. It doesn’t really benefit new buyers of investment properties (the benefit is, in principle, already priced into the market) but it is a systematic distortion for which there is no good economic justification Inflation-indexing key elements of our tax system is highly desirable – at least if we can’t prudently lower the medium-term inflation target – and might be a good topic for a tax working group. In the process, it would also ease the tax burden on people reliant on fixed interest earnings (much of which is also just inflation compensation, not a real income).

Of course, at the same time it would be desirable to look again at a couple of systematic distortions that work against owners of investment properties. Houses are normal goods and (physically) depreciate. And yet depreciation is no longer deductible. Perhaps there was a half-defensible case for that when prices were rising seemingly inexorably – but even then most of the increase was in land value, not in value of the structures on the land – but there is no justification if land reform and (eg) new state building is going to fix the housing market. Similarly, when the PIE system was introduced a decade or so ago, it gave systematic tax advantages to entities with 20 or more unrelated investors. Most New Zealand rental properties historically haven’t been held in such entities. There is no good economic justification for this distinction, which in practice both puts residential investment at a relative tax disadvantage as a saving option, and creates a bias towards institutional vehicles for holding such assets. Institutional vehicles have their own fundamental advantages – greater opportunities for diversification and liquidity – but it isn’t obvious why the tax system should be skewing people towards such vehicles rather than self–managed options. As noted above, any CGT will only reinforce that bias. Funds managers, and associated lawyers and accountants, would welcome that. It isn’t obvious why New Zealand savers should do so.

I see that there are more than 10 bullet points in the list above. I’m not sure it covers all the issues I raised in my paper a few years ago, but it is enough to be going on with.

And in all this in a country where we systematically over-tax capital income already. I commend to readers a comment on yesterday’s tax post by Andrew Coleman, of Otago University (and formerly Treasury). As Andrew noted:

“Somehow, New Zealand’s policy advising community decided it would restrict most of its attention to the ways income tax could be perfected rather than question whether income taxes (which are particularly distortionary when applied to capital incomes) should be replaced by other taxes. It is almost as if we have the Stockholm Tax Syndrome – fallen in love with a system that abuses us.”

A broad-based capital gains tax would just reinforce that problem.

Thank you!! Michael

LikeLike

Reblogged this on Utopia, you are standing in it!.

LikeLike

Michael, an excellent post. One minor comment, relating to your first bullet point. To quote you: “In a well functioning efficient market, there are typically no real expected capital gains….If it were not so then typically the price would already have adjusted.” Consider equities with a nominal risk-adjusted cost of capital of 10% and a dividend yield of 4%. Expected capital gains must then be 6%. If inflation is expected to be 3%, there must be real expected capital gains of 3%. The same principle applies to property, with the rental yield corresponding to the dividend yield. Martin Lally

LikeLike

Fair point Martin (i was implicitly assuming all earnings were paid out, but of course reinvested earnings will predictably increase the share price, cet par, but a CGT on those would be the clearest example of a double taxation that the imputation system was designed to avoid). Were I being simppler I’d prob have made the point that in a real CGT what you should be trying to tax are windfalls, fruits of shocks or essentially unforecastable innovations.

LikeLike

Attempting to tax only unexpected capital gains requires an estimate of expected gains, and therefore an estimate of the cost of equity capital. This would present a lot of work for lawyers and financial economists. Another reason not to try and tax capital gains! Furthermore, the probability distribution of unexpected gains is mean zero, and therefore symmetry in the tax system would lead to net such taxes of zero over time, so why bother, as you have indicated in your post. Thus, to avoid double taxation, you must exclude expected capital gains, and therefore will not raise any net revenue over time (if gains and losses are treated symmetrically) but suffer the deadweight cost of the lawyers and the financial economists. Martin

LikeLike

You mentioned Andrew Coleman’s valid comments at the end of your post. I still like his Jan 2019 paper on taxing capital income, [https://www.otago.ac.nz/economics/otago703148.pdf] which does not seem to have had the attention it deserves.

LikeLike

I’m not able to read this in the short-term, with other matters needing attention, but how do unrealised superannuation entitlements get treated, particularly in the wider population?

LikeLike

not sure, altho of course earnings on private super funds are all taxed anyway. NZS is probably just treated as income in the year received

LikeLike

But capital gains on private super funds?

LikeLike

ok, fair point. Not sure. For most households the average Kiwisaver balance is still fairly modest, and there is a CGT equivalent on investment in foreign funds, but yes it looks as tho this could be something that will affect effective tax rates for the rest of the population a bit.

LikeLike

very good comments. You are correct, over the 6 year period, 47% of all the gains arise in the 2021 year, the year that interest rates collapsed, and asset prices ballooned. This qualification is a major qualification and seems to have been over looked by the Minister.

LikeLike