Immigration is in the news quite often these days. The government tells us it is planning changes to the rules (in a “having emerged from Covid” world). They’ve asked the Productivity Commission to do a substantial report on New Zealand immigration policy (apparently expected to report after at least some of the government’s policy changes). And, of course, in the short-term while New Zealanders are free to emigrate – to give our government some credit, at least they don’t make departure entirely dependent on the grace and favour of the government as in Australia – it is very difficult for most people who aren’t New Zealanders or New Zealand residents to get into New Zealand at present. There are some compelling human stories (separated nuclear families), but also all sorts of claims about how our individual firms, or perhaps the economy as a whole, might be suffering as a result. Over the last 12 months (to the end of June), there has been a net outflow of 35000 people (New Zealand and foreign) – as a share of the population, the only time there has been a larger net outflow looks to have been in the late 1970s. Quite a contrast to the really big net inflows we’d experienced in the years just prior to Covid.

So it was interesting to see a new research report out from the ANZ economics team looking at “How does immigration affect the New Zealand economy”. As the authors note, it is similar in spirit and technique to a piece the Reserve Bank did back in 2013, which I will come back to later in this post. And has somewhat similar – but probably weaker – results, despite a number of differences, both in data and specification.

It is important to note that (a) these are not highly-detailed structural models of the economy and (b) do not purport to say anything material about the longer-term questions about the economic impact of New Zealand’s immigration policy that are my main focus. The main focus instead is on the impact of some unexpected net immigration over the first two or three years – and the ANZ piece does not even attempt to distinguish between the bits under government control (non-New Zealanders, especially arrivials) and the bits that aren’t (movement of New Zealanders).

Here is how ANZ describes their effort

Net immigration tends to be driven primarily by changes to immigration settings and relative labour market conditions between Australia and New Zealand. At the moment, we can add the pace of border opening. With the

outlook so uncertain, it’s helpful to ask what will happen to the economy if net immigration is stronger or weaker than we expect in coming years. To answer this question we employ a simple model1 that estimates the

relationships between key variables:

Net immigration

Growth in residential building consents

Investment intentions (from the ANZ Business Outlook)

GDP growth

House price inflation

Growth in labour costs

The change in the 2-year mortgage rate

They use data back to 1998 (not entirely sure why they don’t go further back, but perhaps one of the data series isn’t available further back). Note the problem that bedevils so much of this sort of work. If 20+ years doesn’t sounds too bad (80+ quarters), actually the researchers are trying to distill results from what are really only two events (two complete immigration cycles) and so not too much weight can be put on any particular result.

Note too that the immigration series they are now using (the new 12/16 series mostly) is different in character to the series (the old PLT data) used in earlier work. PLT data used self-reported intentions at the time of arrival/departure, and thus was unaffected by anything that happened after arrival/departure. The 12/16 series – which relies on what people actually did (whether they stayed – here or away – for long) – is importantly different. You might have arrived intending not to stay long, but if conditions while you are here change for the better you may choose to stay. In some respects (but not all) it is (eventually) better data, but the difference is one researchers might want to think about.

I’m also a bit puzzled why – other than advertising their own survey – they used the ANZ Investment Intentions series rather than actual investment data from SNZ.

Anyway, what do the results show? They do a first round suggesting (not very surprisingly) that higher (lower) net immigration is associated with higher (lower) house prices and dwelling consents. Then they attempt to do something a bit more sophisticated and isolate causality. In their words

In this section, we make a few tweaks to the model which allow us to be more definitive about the impact of net-immigration on individual variables like wages. We can get the answer to the question: ‘what’s the impact of

an X increase in net immigration on house price inflation, holding everything else constant?’

Overall, our findings are consistent with the forecast scenarios – but with the tweaks we’ve made, we can say that our model shows that an increase in net immigration results in higher house price inflation, rather than saying

is associated with higher house prices. That might sound like semantics, but it’s the difference between correlation and causation.

(For those really technically minded there are footnotes on both these model specifications.)

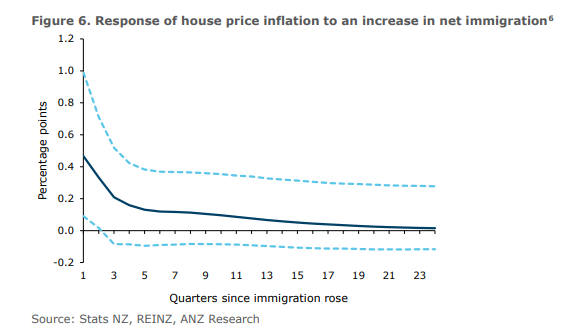

Here are the house prices results

They don’t seem to state the size of the shock, but I guess the point they want to emphasise is that the effect is positive. But actually what surprised me was that, on this model and specification, the effect is only statistically significant for a couple of quarters at most (those dotted lines are 90 per cent confidence bands). Even allowing for the fact that the model is looking at house price inflation not house price levels, that seems a bit surprising.

I’m guessing that the results are stronger for dwelling consents, since they say

The results for residential consents showed a strong positive response to higher net immigration. Together, these findings show that higher net immigration generates sizeable upwards momentum in both prices and activity in the housing market.

But they don’t show the results. If so, it would be a little surprising, since the general story has tended to be that immigration shocks boost house prices first, and only later have a large effect on consents.

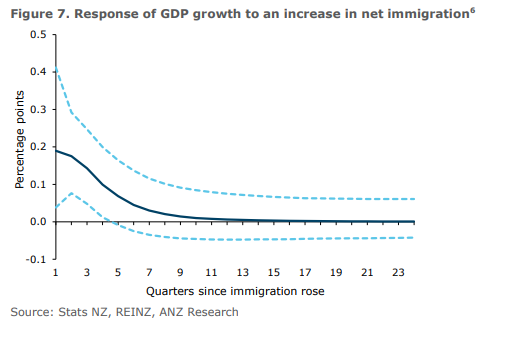

What about the other variables in the model? They do find a boost to GDP growth, for the first year or so (not at all surprising, since there are more people, whether as workers, consumers, or people needing a roof).

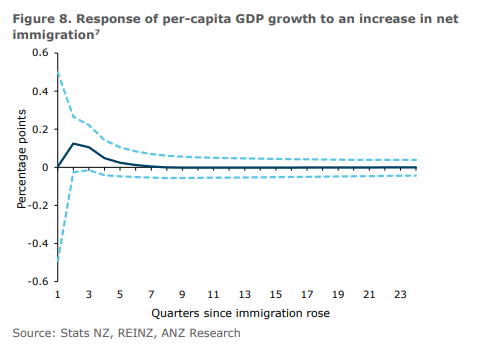

They report no effect (positive or negative on wages). But what about GDP per capita growth?

They describe this is “it doesn’t look like there’s a strong effect”, but given the confidence intervals it would be fairer to say it is no effect at all. And, frankly, that is a surprise (a point I’ll come back to).

The final observation ANZ make that I wanted to pick up on was their observation that they do not find significant impacts on investment intentions. They don’t make anything of it, but if that result were robust – and I’m sceptical – it should be really rather concerning. There is, on this scenario, an unexpected change in the number of people in New Zealand, and there is no impact on firms’ investment intentions, and yet additional workers need additional physical capital (be it a computer, or tools, or a van, or a desk, or an office or whatever?). I’ve shown cross-country data previously suggesting that in advanced countries business investment (as a share of GDP) has tended to be negatively correlated with population growth, so in a way I’m not overly surprised, but the prevailing official New Zealand story surely requires a belief that more people results in more investment, if simply to maintain pre-existing capita/output ratios. I wouldn’t want to put too much weight on this result – which may depend on the specific variable they chose to use, or whatever – but it should be a slightly disconcerting straw in the wind nonetheless.

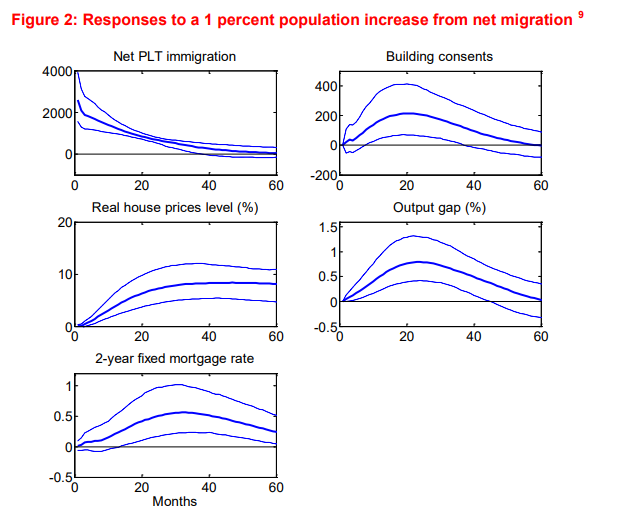

So what about that 2013 Reserve Bank paper I mentioned earlier? (Disclosure: I was the editor responsible for the paper, and although I asked for some of the specifications in it, all the results are those of the author – now one of the Bank’s key economics managers.)

That Reserve Bank set out to look specifically at the impact of migration on the housing market, as net migration was just beginning to pick up strongly again. In what is described as a “fairly simple model” this is what the author set out to do.

Using the output gap has some attractions and some disadvantages. From a central bank perspective, one is less interested in whether headline GDP rises and more interested in whether migration shocks add to or ease overall resource pressure. On the other hand, output gap estimates are subject to revision, and are actually revised quite a bit (the 2013 series that McDonald used clearly describes the same economy as the Bank’s latest estimate, but with important differences, including that at the time he wrote the Bank’s official view was that the output gap was already slightly positive, while now they think it was still reasonably negative).

These were McDonald’s summary results (noting that the confidence bands here are 68 per cent confidence bands)

In this model, after five years house prices are still 8.1 per cent higher than otherwise after a 1 per cent of population immigration shock.

I guess the key result I always focused on in this paper was the output gap estimates. Immigration shocks in New Zealand over this specific period tend to have added more to demand (including for labour) in the short-run than they add to the economy’s supply potential (but after 3 years and more – recall these are monthly numbers – that effect fades out, leaving the output gap effect basically zero). That has implications for interest rates (in these models the two year mortgage rate, but there is quite a correlation with the OCR). (It is also consistent with at least some initial boost to per capita GDP – see above – since a given pool of resources in being worked more intensively.)

McDonald also looked at arrivals and departures separately (didn’t seem to make much difference) and at movements of New Zealanders and non New Zealanders separately (where there were some differences – notably the output gap effect is zero for New Zealanders, possibly because the comings and goings of New Zealanders are more purely endogenous). There appeared to be some differences by country of origins (arrivals from Europe/UK boosted house prices a bit less, and more slowly, than arrivals from Asia).

The broad thrust of these results should not really surprise anyone. The notion that immigration has added more to demand than supply in the short term was just a standard feature of New Zealand macroeconomic analysis for many many decades (whether historically or in the forecasts/write-ups of places like the Bank and Treasury more recently). That it is so says nothing – nothing at all – about the pros and cons of large scale policy-led immigration longer-term. The short-term effects are more likely to be that way round in a country that mostly imports “people like us” – often people with a reasonable degree of education and skill, often actually New Zealanders – than, say, in a country where a large chunk of migrants are lowly-skilled illegals (again, whatever the long-term case for either sort of immigration).

And yet, if these results shouldn’t surprise, they clearly do surprise many businesses and business lobbyists, operating entirely with a single firm perspective and either unaware of or deliberately choosing to ignore the macro analysis. Here is eminent economic historian Gary Hawke’s take – from a 1981 chapter in The Oxford History of New Zealand.

“Ironically, the success with which full employment was pursued until the late 1960s led to frequent claims that labour was in short supply so that more immigrants were desirable. The output of an individual industrialist might indeed have been constrained by the unavailability of labour so that more migrants would have been beneficial to the firm, especially if the costs of migration could be shifted to taxpayers generally through government subsidies. But migrants also demanded goods and services, especially if they arrived in family groups or formed households soon after arrival and so required housing and social services such as schools and health services. The economy as a whole then remained just as “short of labour” after their arrival.

Whatever the possible longer-term microeconomic case for access to a wider pool of skills, a new migrant labourer may ease an individual firm’s constraint or problem – perhaps even a sector’s if they can get a disproportionate share of the arrivals – but large scale migration simply does not ease overall macroeconomic resource pressure.

All that is really a protracted intro to a point I have been toying with. I recall writing a post early last year – probably February – suggesting that the building downside risks to the economy were such that I would be very hesistant to then recommend a significant cut in non-citizen immigration, for fear of exacerbating the near-term economic downturn. For much of last year, my comfort with the pessimistic economic forecasts the Reserve Bank and Treasury were publishing was reinforced by this short-run immigration story: demand effects typically exceed supply effects over the first couple of years so a big net outflow (enforced by Covid border restrictions) seemed likely to exacerbate/extend the economic weakness.

And yet, here we are, borders still closed, still monthly net outflows, significant sectoral dislocations but……the economy at more or less full employment (more jobs filled now than there were early last year, even though fewer people are physically here), and business and consumer sentiment really running rather strongly, investment intentions included.

Where does immigration fit with the story? I’m surprised things are running as strongly as they are but so (presumably, if they have thought about it) must be those constantly rushing to ministers and newspapers to claim that the economic costs of not having access to another migrant labourer are very high (on some rhetoric “threatening our entire recovery”. I’m not trying to suggest that all is rosy about our economy – it clearly is not in any structural sense, but in a short-term cyclical sense (the focus of both the ANZ and RB work) you can’t really complain about things here. The market now thinks official interest rates will/should be on the way back up before the end of the year. Core inflation might even get past 2 per cent for the first time in a decade. Workers often find employers competing for their services.

My honest answer to my own question is that I’m still not clear. I’ve put a lot of weight on the swings in the structural fiscal position – the swing from a near balanced budget 18 months ago to huge cyclically-adjusted deficits now is a really big boost to demand – and official interest rates are lower than they were, all in an economy where the net loss of purchasing power from other factors has been pretty limited (to put it mildly, having in mind the strength of the terms of trade). The short-term macro effects of swings in migration seem pretty clear – need for a roof etc hasn’t changed – so I can only deduce that we’ve had a series of factors at play:

- fiscal policy (really big boost to demand)

- monetary policy (modest boost to demand – through the OCR, little or nothing through LSAP)

- some slight dampening to demand from restrictions on overseas tourism and export education (most NZ offshore tourist spending seems to have been displaced to additional demand for other things),

- some boost to net incomes and demand from the rising terms of trade, and

- a significant dampening to demand from the move from a net migration inflow to an outflow.

It would be consistent with a story in which the overall economy might now be running as strong (cyclically) or even a bit stronger than it was early last year, and one which – all else equal – a significant reversal in the net migration flow – would simply exacerbate (forcing higher interest rates or tighter fiscal policy) rather than relieve.

I’ll have a few thoughts specifically on monetary policy tomorrow.