I’m less interested in what the Reserve Bank will be doing at next week’s OCR review, or the one after that (or the one after that) than in what they should be doing. The Bank’s MPC do few/no thoughtful speeches (or really any at all on economic developments and monetary policy), publish little research, and have something of a record at times of lurching unpredictably from one review to the next. Banks employ people who will try to wheedle morsels of information out of Reserve Bank staff and MPC members and read those tea leaves. My interest is mainly in what the Bank should be doing, both absolutely (what is first best policy) and consistent with the mandate they’ve been given by the government of the day. I used to run the line that eventually policymakers will do the right thing (and we will all grope towards knowing what that is, no matter how fervently we champion our individual views), and I guess that is probably still true if avoiding serious outright deflation or runaway inflation is the test. But my confidence has taken a bit of a knock in the last 18 months.

The Reserve Bank went into Covid manifestly ill-prepared. They’d talked up the perfectly normal tool of a negative OCR – used in a variety of advanced countries in the last cycle, regarded as effective by no less than the IMF – only to find just a month or two before the crisis hit that actually banks had technical obstacles (systems issues) that, the Bank concluded, meant they couldn’t use their preferred instrument. It was truly astonishing – not only had they had 10 years’ notice from the rest of the world, and an internal working group that had highlighted to the Governor that specific (work with banks to be ready) issue 7-8 years earlier, but they’d been publishing work and giving interviews on their thinking about the next downturn. And yet they simply hadn’t done the basic operational work to be ready. It was an extraordinary failure, on their own terms – a failure of management (Wheeler, Spencer, Orr, Bascand et al), of the MPC, and of the Board paid to hold the Bank to account on our behalf, as citizens and taxpayers.

Taxpayers? Well, yes, because one of the great things about conventional monetary policy – official short-term interest rate adjustment – is that it costs (and makes) the taxpayer nothing. A key overnight interest rate is adjusted, nothing much about the public sector balance sheet changes, and no material financial risks are assumed on behalf of the taxpayer. The private sector, subject to all the appropriate self and market disciplines, does the substantive adjustments, to spending, investing, saving etc choices. It is one of several reasons to prefer monetary policy as a stabilisation tool – at the other extreme, expansionary fiscal policy just involves writing large cheques with other people’s money.

But unable (so they judged) to take the OCR negative, and unwilling (for reasons they’ve never attempted to explain) to even take the OCR quite to zero, the Bank lurched into the Large Scale Asset Purchase programme (LSAP), in which they have been buying up huge quantities of (mostly) government bonds, heavily concentrated at the highest risk long-end of the bond market where if they affect rates at all they aren’t rates that anyone much in the private sector pays. Short-term rates (out to perhaps a couple of years) are what matter in this market, and the Bank could very easily have managed those rates without (a) many asset purchases at all (market rates respond to expectations of future monetary policy) and (b) without anywhere near as much financial risk (short-term bond prices don’t fluctuate much).

I’ve been running an argument for the last year or more that the LSAP was really little more than performative display (“see we are doing lots, really”), in substance no more than a large-scale asset swap (Bank buys back long-term bonds and issues in exchange short-term liabilities with exactly the same credit risk), in turn exposing the taxpayer to a lot of market/refinancing risk. Of course, the Bank claims otherwise – they claim significant effects on bond rates (but if so, so what) and the exchange rate – but have never provided much supporting analysis. And they have their defenders in the markets – you could read this interesting piece from the ANZ, although you may come away thinking that the ANZ bank thought LSAPs were a good idea as (financial) industry assistance. At best, if there was a case for the LSAP it had long since passed by the end of last year (by when even the Bank recognised that it could have used a negative OCR). And yet they went on – albeit staff (but not the MPC) have been reducing the scale of purchases more recently, partly because there are fewer bonds to buy.

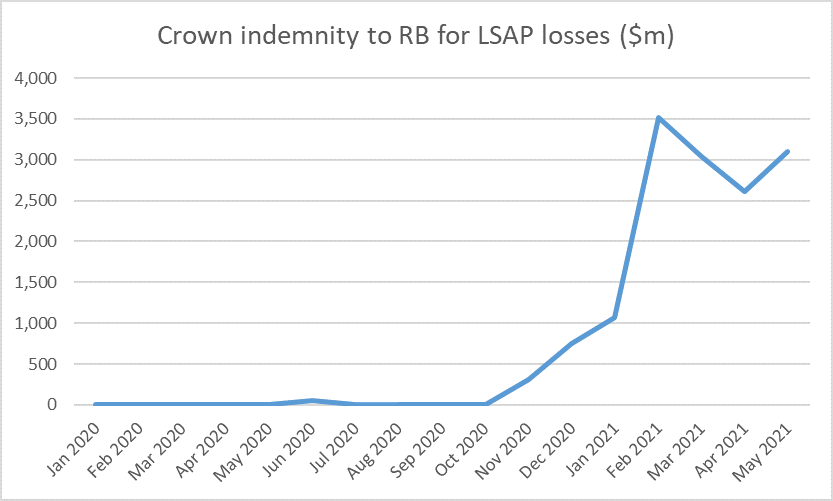

What about that financial risk? The Reserve Bank has about $3 billion of capital, and although capital isn’t a technical constraint on a central bank – it can still run with negative equity – Governors and MPC tend to be reluctant to take on lots of risk for their own institution relative to the amount of capital the institution has. So the Bank persuaded the government to provide an indemnity, covering any losses the Bank ended up making on the LSAP programme. And now there is a line item on the Reserve Bank balance sheet representing those losses, and the claim the Bank now has on the government.

The published data are only to 31 May, and as rates fluctuate (down and up) the market value of the losses changes (as of today probably a bit lower than 31 May), and the Bank also continues to buy bonds. But a $3 billion loss looks like a reasonable point estimate. That is about 0.8 per cent of GDP gone and most probably – since there is no reason to suppose rates are more likely to fall than to rise from here over the years ahead – not coming back. Transferred from you and me, to those lucky enough to offload their bonds to the Crown near the highest prices ever experienced. The pedestrian/cycling bridge in Auckland has been a recent benchmark for reckless public spending, but this has cost four bridges – without even the consolation of somewhere to go sightseeing on a holiday to Auckland.

It is almost certainly the most costly (to the taxpayer) Reserve Bank intervention since the devaluation crisis of 1984 – and at least in that case the Bank’s losses resulted from a refusal of the government to follow Treasury/Reserve Bank advice. It swamps the cost of the 2008 deposit guarantee scheme, which some continue to inveigh against to this day. The public sector as a whole could have locked in the long-term debt funding it needed at last year’s low rates. Instead, the MPC, the Governor and the government acted to prevent it, at great and preventable cost to the taxpayer.

Preventable? Recall, they should have been able to deploy negative rates (their preferred option) which would have cost nothing. They could have focused what purchases they did much more heavily on short-dated bonds (on which losses would have been very limited). And they could have stopped the programme eight or nine months ago, once the negative OCR tool was back on the table. (None of this requires second-guessing purely with the benefit of hindsight the Bank’s macro forecasts – this would have been sound advice on their own contemporary numbers.)

Instead, even as recently as the last Monetary Policy Statement they were on record as suggesting

The Committee agreed that the OCR is the preferred tool to respond to future economic developments in either direction.

In other words, they planned to keep on buying up bonds per the ongoing programme even if economic developments meant overall conditions needed tightening. They’d keep on running up financial risk to the taxpayer and raise the OCR at the same time.

We might hope for a rethink next week, but who knows whether it will happen – there is a often a preference for making significant moves at full MPSs – but what they should be doing is discontinuing the LSAP now (not just letting staff run down new purchases, but winding up the programme completely, and publishing plans to manage – ideally relatively aggressively – the unwinding of their huge bond position). An apology for the losses would be nice too, but instead no doubt we’ll have claims repeated about the great gains the programme has offered with – as is now customary – no attempt to a cost-benefit analysis of this or of alternative approaches.

But, expensive as it has been, no one is probably now arguing that continuing – or discontinuing – the LSAP at current purchase rates is now making any macroeconomically significant difference. So whether or not it is ended isn’t really relevant to the macroeconomic question of what to do about the emerging economic data and the inflation outlook. What should be being done about that?

On balance, I think it is now hard to make a compelling case for the status quo on monetary policy (of things that make a difference, the OCR and the Funding for Lending programme). I’m very conscious of the mistakes the Reserve Bank made in prematurely tightening in the 2010s (on two separate occasions), and the way markets here and abroad often got ahead of themselves in looking to tightenings in that decade. And there is always a risk in using as a reference point rates as they were pre-recession – recall how Graeme Wheeler in particular always used to talk about getting rates “back to normal”.

But there are some important differences this time. Take two (quite important ones): inflation and unemployment.

When Alan Bollard started raising the OCR in 2010 core inflation has been falling sharply , the unemployment rate was about 6 per cent, and the employment rate was well below pre-recession levels.

And when Graeme Wheeler started raising the OCR in 2014, talking confidently on his plans to raise it by 200 basis points, the Bank’s preferred (slow-moving) core inflation measure was around 1.2 per cent, the unemployment rate was about 5.7 per cent, and the employment was still well below (although a bit less below) pre-recession levels. Perhaps the strongest elements in his case for tightening then were the strong terms of trade and the ongoing demand effects of the Christchurch repair and rebuild process.

What about now? Well, core inflation just did not fall during last year’s recession, and the best read now is that it is about 2 per cent (the Bank’s slow-moving preferred measure is up to 1.9 per cent). As for the labour market, the latest official unemployment rate was still a bit above (4.7 per cent) where it was at the start of last year, and the employment rate was a bit below (both gaps being much smaller than in 2010 and 2014). Meanwhile the new monthly jobs indicator tells us that the number of filled jobs is now above levels at the start of last year, even as the number of people in the country has shrunk, suggesting the official unemployment rate now (early Sept quarter) is probably not much different than it had been pre-recession.

Those indicators alone – absent any good reason to think neutral interest rates have fallen a lot since the start of last year – would make a reasonably good, entirely conventional, case for getting some monetary policy tightening underway, all reinforced by stories about the high (possibly record) terms of trade, and the very large government deficit (underpinning demand). And if business confidence surveys don’t often have much pure predictive power there is certainly nothing in them to suggest it would be reckless or irresponsible to see official actions sanctioning the rise already seen in market rates. There is nothing good or bad intrinsically in lower or higher interest rates – they are simply the balancing price, reconciling all the other evident pressures in the economy.

What would be unwise would be for the Reserve Bank – or anyone else – to be uttering views about the economic outlook with any great confidence. There are more than a few big uncertainties out there, and it is always rash – as Wheeler was – for central banks to talk grandly about multi-year interest rate adjustment plans. Events have a way of overwhelming such hubris. The MPC needs to be led by the data, and for now – and given the stance of fiscal policy, which MPC has to take as given – the data probably do sensibly point in the direction of higher interest rates. It might not six months hence, but the MPC simply needs to be led by the data as it emerges.

That shouldn’t mean aggressive moves. Recall that core inflation has been below the target midpoint for a decade or more, and for the entire time (since 2012) when 2 per cent midpoint has been a formal focal point in the target document. Against that backdrop, there is no harm in core inflation going a bit beyond 2 per cent for a while – doing so might help cement in longer-term inflation expectations near 2 per cent (market price indications are still below that, although higher than they were a couple of years back). But a modest tightening now might well see core inflation rise above 2 per cent if the more inflationary/expansionist indicators are for real, while preventing it dropping below 2 per cent if they don’t. “Least regrets” was the mantra the Bank liked to chant.

That also doesn’t mean the OCR should be raised. The first step (other than the performative signalling LSAP) should be to end the Funding for Lending programme. It was an extraordinary intervention that, while second best, worked, lowering retail rates relative to the OCR. But it was a non-neutral operation – only banks had access to it – and runs against the principles of competitively neutral interventions. There isn’t that much FFL lending outstanding – $3 billion or so at the end of May – and of course those who’ve already borrowed get to keep their loans to maturity – but there is no evident need for the facility to still be in place now. For those who worry that early Reserve Bank action might drive the exchange rate higher, using the FFL rather than the OCR is (a) quite a bit less high profile, and (b) retail rather than wholesale focused. Frankly, exchange rate concerns would be better addressed with a tighter fiscal policy.

And, almost finally, if there is a case for higher interest rates now, it is entirely cyclical and says nothing at all about the fundamental strengths (or travails) of the New Zealand economy. Border closures are likely to have reduced potential output a bit, and so have a whole raft of other government interventions (some of which may also have raised the minimum sustainable unemployment rate) . But monetary policy isn’t about potential output; all it can (and should do) is influence things around potential, however good or bad potential may be. As it was in the 1970s – when potential growth slowed but interest rates needed to be raised to deal with inflation – perhaps to some extent it is now.

Should the stances of other central banks be a constraint? I don’t think so. We’ve already seen a couple of OECD central banks move to raise official interest rates this year, and if institutions like the Fed, the ECB, and the Bank of England are more cautious, well the recoveries in each of those places lag a bit behind that here. As for the RBA, they seem an odd mix – their Governor almost seems to be running some sort of 1980s cost-push wage-targeting mental model – but bear in mind that core inflation in Australia was well below their target midpoint going in to Covid, and still is today. Circumstances differ, even if end goals are fairly similar.

School holidays loom and we are heading away so no more posts here for a couple of weeks.

Thank you – good article – so essentially the RB has cost New Zealand taxpayers $3-$4 billion due to their “incompetence”?

LikeLike

“Choices” anyway. I suspect they were mislead by the experience of countries that did QE last cycle, who were able to ride the long term decline in bond yields further down and mostly will not have recorded significant losses. And some of them may genuinely believe that QE has made a big macro difference – but there is no real opportunity to scrutinise their analysis as they typically won’t release it.

LikeLike

Given that the economy has rebounded with a V shape recovery, the RBNZ and Adrian Orr has done an excellent job. We all should know by now that bank economists are always acting in the best interest of bank profits, the RBNZ and its board should really ignore most of their comments.

NZ is small country which means its local businesses need a wider inflation band as profits come from a much lower volume of sales. History has demonstrated that the hawkish monetary policies of Don Brash and Allan Bollard has led to the decimation of local producers and have severely damaged the productivity of NZ trying to keep inflation within a narrow band and have encouraged China imports instead.

LikeLike

I agree, it is unacceptable in such a difficult situation to speak and face “incompetence” …

LikeLike

I agree with your comment on suspending LSAP and ending FLP. I’m a little more hesitant about rate hikes, just yet…

If you model bank mortgage rates against swaps you find their rates are currently well below their historical relationship to wholesale market rates; we are talking over 100bp in 1y falling to around 50bp in 5y on the blackboard rates for LVR<80%.

Given the stock of mortgage debt outstanding, it’s generally very short fixed rate duration and the high sensitivity of household mortgage debt serviceability at the margin – the flip side of affordability – then a lift in mortgage rates could take the shine off the housing market, and ease pressure on capacity, very quickly.

Add in the fact that capacity is constrained by a temporarily (one hopes) closed border and a good portion of the lift in inflation is in temporary areas (even if core inflation is at the target mid-point and climbing) and the fiscal impulse is turning negative, it all suggests to me the Bank should be measured and deliberate in moving the cash rate.

So, if the RBNZ wants to tighten monetary policy, they don’t need to hike the OCR just yet. They can move on the liquidity programs first and give guidance to banks that they’re ok to see mortgage rates re-price. And any hikes need to be carefully implemented as I think the economy remains highly fragile despite the shrill calls from Bank economists…

LikeLike

I don’t think we are differing. I would be interested to see what difference ending the funding for lending programme would make but it would tighten conditions/raise rates somewhat further. Do that now or in Aug and by Nov there would be both a read on that specific impact, two more core inflation readings, and potentially a bit more clarity on border risks/possibilities.

LikeLike

The elephant in the room on the RBNZ books, that both of you keep forgetting is unwinding the $61 billion IOU to banks called Settlement deposits liability ie owed to banks, created by buying $58 billion in treasury bonds plus the 0.25% pa interest accumulated and yet unpaid. The $28 billion offered to banks is actually an offset loan facility. Currently the takeup is only $3 billion as it is restricted to Commercial business lending and currently no one wants to borrow or lend to run businesses. The question is why only $28 billion? I suspect the RBNZ has $28 billion in Treasury bonds maturing soon. The RBNZ and the government will get increasingly more desperate. Notice the 1.68% loans being offered for New Built homes announced now by 2 banks? This shows increasing desperation by the RBNZ to encourage the takeup of the $28 billion FLP. That FLP will need to go up considerably ie as High as $61 billion otherwise the government will have to pay up to clear the RBNZ Settlements deposit liability still owed to banks.

LikeLike

The RBNZ does have the option of reselling the $58 billion in NZ Treasury bonds it currently holds. However if interest rates rises then the bonds will devalue creating in effect an insolvent Central Bank.

LikeLike

Michael, hopefully the $373,739 Tane Mahuta carving in the Reserve Bank’s new swish lobby will guide the governor and his colleagues to make the appropriate decisions!

LikeLiked by 1 person

We’ve come a long way since the Governor (Brash) used to boast about his frugality, washing his own clothes in hotel rooms in NY/LON.

LikeLiked by 1 person

Stats NZ have ,at last ,identified the start of inflation.

As any economists know in measuring economic data there is an inevitable lag.

So inflation is likely already considerably higher than the 3.3 % stated..

And yet the RBNZ has made no adjustment of the OCR.as required by the terms of their agreement with the Government.

Most banks have moved already.

We have to ask why the inaction by the RB?

LikeLike

The RB will probably be more focused on the core measures, the best of which was at 2.2% yesterday. The Bank would argue that it has taken some action by ending the LSAP.

LikeLike

With already $58 billion exposed to Treasury bonds, the RBNZ is highly exposed to interest rate rises. A 1% increase in interest rates is a bond devaluation loss on the RBNZ Balance Sheet of 20% to 30% on long dated bonds. The RBNZ will have to beg the government for an increase in Crown guarantees on LSAP losses from currently $3 billion loss to $15 billion loss just to stave off bankruptcy.

LikeLike