Some months ago the Governor of the Reserve Bank inaugurated his audacious bid to have his institution – seen by most as a official agency created by, and accountable to, Parliament – seen as some sort of local pagan tree god, with him (I assume) as the high priest in the cult of Tane Mahuta. We’ve been told, by the Governor, that a people – New Zealanders – walked in economic darkness until finally the light dawned with the creation of the Reserve Bank. It is pretty absurd stuff, not even backed by decent history or analysis, and one might be inclined just to ignore it, but the Governor seems serious. In particular, he keeps returning to his claim. In fact, he was at it again – claiming the mantle of Tane Mahuta – yesterday with another little release that poses more questions than it offers answers (and which presumably means we’ll end the year still with no substantive speech from the Governor on anything he actually has statutory responsibility for).

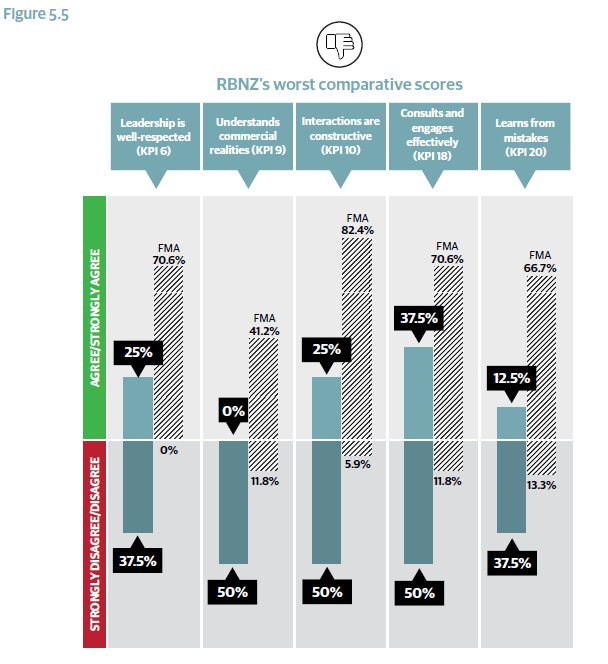

Readers might recall that there was a damning report on the Reserve Bank as financial regulator, drawing on survey results of regulated institutions, released in April by the New Zealand Initiative. This chart summed it up quite well

It has, presumably, been a priority for the Governor to improve the situation. After all, even the Bank’s Board – always reluctant to ever suggest any weaknesses at the Bank, even though their sole role is monitoring and accountability – was moved to comment on this report, and the issues it raises, in their Annual Report this year.

And thus the Governor begins

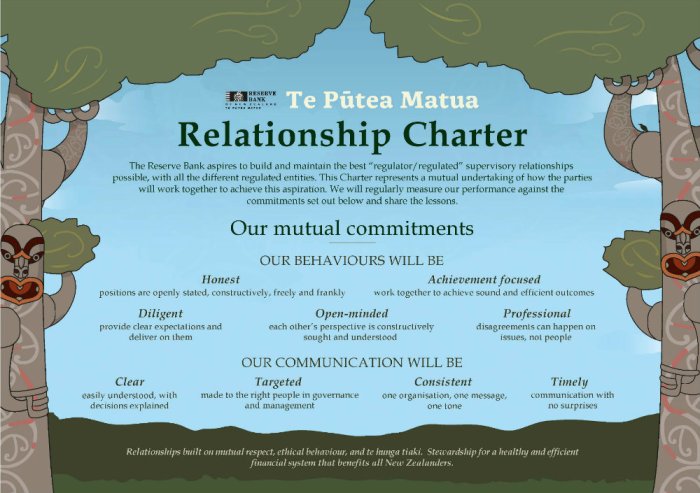

In a step toward achieving the best “regulator-regulated” relationships possible, the Reserve Bank (Te Pūtea Matua) has established a Relationship Charter for working effectively with banks. The Charter will also be discussed with insurers and non-bank deposit takers in the near future.

One might question just how “best” is to be defined here – after all, the public interest is not the same as that of either the Reserve Bank or of the banks, and there have been many examples globally of all too-comfortable relationships between regulators and the regulated.

But it was the next paragraph that started to get interesting.

Reserve Bank Governor Adrian Orr said the Relationship Charter commits the Bank and the financial sector to a mutual understanding of appropriate conduct and culture. “This is underpinned by the principle ‘te hunga tiaki’, the combined stewardship of an efficient system for the benefit of all,” Mr Orr said.

I’m not sure that understanding is necesssarily advanced when an institution operating in English introduces little-known phrases from another language to their press releases. Here is how Te Ara explains “te hunga tiaki”

Te hunga tiaki

The Te Arawa tribes use the term ‘te hunga tiaki’ instead of kaitiaki, explains Huhana Mihinui.

The prefix ‘hunga’ is more common than ‘kai’ amongst Te Arawa, hence te hunga tiaki rather than kaitiaki. The essence of hunga is a group with common purpose. Hunga may also link with the sense of communal responsibilities. The same meaning is not conveyed with ‘kai’ … te hunga tiaki likewise invokes ideas of obligations to offer hospitality, but also to manage and protect, with the implicit recognition of the group’s mana whenua [customary authority over a traditional territory] role in this respect. 1

Which sounds pretty problematic frankly. Banks and the Reserve Bank do not have a common purpose or a common set of responsibilities. The Reserve Bank has legal responsibilities to the people of New Zealand, and the banks have legal responsibilities to their shareholders. The two won’t always be inconsistent, but at times they will and there is little gained (and some things risked) from trying to pretend otherwise. In both cases – but particularly in that of the Reserve Bank – there are limits on the ability of the principals (citizens and shareholders) to ensure that the boards and/or managers are actually operating according to those responsibilities. Shareholders can sell. Citizens are stuck with the Governor.

The statement goes on

“Writing it was the easy part. Operating consistently with the conduct principles is the challenge. We will regularly mutually review behaviours with the industry. Appropriate conduct is critical to the trust and wellbeing of New Zealand’s financial system, and the Reserve Bank – the ‘Tane Mahuta’ of the financial garden,” Mr Orr said.

It is the tree god again – a tree god that has some considerable way to go in improving its own conduct, be it around attempting to silence critics or whatever.

But this is also where I started to get puzzled. In both those last two paragraphs from the statement, there is a suggestion that this document is some sort of agreed position between the banks and the Reserve Bank. It is there in the charter document itself – a one pager, complete with cartoonish tree god characters.

(What I didn’t see was, for example, “we will avoid abusing our office and putting pressure on regulated bank CEOs to silence their economists when those economists write things we don’t like”.)

The word “mutual” is there twice, clearly suggesting that the banks have signed on to this.

But, if so, isn’t it a little strange that there are no quotes from any bankers, or the Bankers’ Association, in the press release, just the Governor’s own spin? And when I checked the Bankers’ Association website, there was no statement from them. In fact, I checked the websites of all the big four banks and there was not a comment or statement from any of them. Frankly, it doesn’t seem very “mutual”. It looks a lot like gubernatorial spin.

And, to be frank, I don’t really see any good reason why there should be such mutual commitments. Regulated entities don’t owe anything to the regulators. They may often be intimidated by them, (privately) derisive of them, or even respect them. But the regulated entities are just private bodies trying to go about their business in a competitive market. By contrast, the Reserve Bank – the Governor personally – carries a great deal of power over those entities, and they have few formal remedies against the abuse of that power. What might reasonably be expected is unilateral commitments by the Governor as to how his organisations will operate in its dealings with regulated entities, standards (ideally measurable ones) that they and we can use to hold the regulator to account. But that is different from what purports to be on offer in yesterday’s statement.

Of the brief specifics in the list of commitments, I don’t have too much to say. There is a big element of “motherhood and apple pie” to them, and a few notable elements missing. There is nothing about analytical rigour, nothing about transparency, nothing about remembering that the Bank’s responsibility is primarily to the New Zealand public, nothing about maintaining appropriate distance between the regulator and the regulated. But I guess those would have been inconsistent with the fallacious claims about all being in it together and working for common goals.

It is at about this point that the Bank’s press release changes tone quite noticeably (not quite sure what happened to “one organisation, one message, one tone”). Deputy Governor Geoff Bascand takes over and claims

Deputy Governor Geoff Bascand said the Reserve Bank’s recent announcement of a consultation with banks about the appropriate level of bank capital highlights the usefulness of the Relationship Charter.

And even in that one sentence he captures some of the mindset risks. As I read the announcement the other day, it was a public consultation about the appropriate level of bank capital, and yet the Deputy Governor presents it as a “consultation with banks”. If the Bank is going to run with this “Relationship Charter” notion, perhaps they could consider one for their relationship with the only people who give them legitimacy, Parliament and the public (having said that, perhaps I should be careful what I wish for).

And then weirdly – in a press release supposed to highlight a new era of comity, open-mindedness etc – the Deputy Governor launches into an argumentative spiel about the proposed new capital requirements.

“There is a natural conflict of interest. Banks will want to hold lower levels of capital to maximise returns for their shareholders. However, customers and society wear the full economic and social cost of a bank failure. We represent society’s interests and will naturally insist on higher capital holdings than any one individual shareholder,” Mr Bascand said.

Strange use of the phrase “conflict of interest”, which usually relates to a person or an organisation having two competing loyalties (perhaps personal and institutional), but even if one sets that point to one side for now, the rest is all rather one-dimensional and not terribly compelling. He seems unaware, for example, that banks often hold capital well above regulatory minima – creditors and rating agencies have perspectives too – or that in most industries firms happily determine their own levels of capital, and somehow society manages (and prospers). And, of course, there is not an iota of recognition of the way in which bureaucrats all too often serve bureaucratic interests (rather than societal ones), of the distinction between loan losses and bank failures, or of how the interventions of official and ministers often create the problems in the first place.

And then there is the final paragraph

“Following our Relationship Charter, we long signalled the purpose of our work and shared our analysis and consultation timetable. We have also committed significant time to engage with banks and provide a sensible transition period to make any changes we decide on. The Charter means what we are looking to achieve can be discussed professionally, while we continue to build appropriate working relationships. Outcomes will be superior and better understood and owned by society,” Mr Bascand said.

Of course, for example, whether the proposed transition period is “sensible” is itself a matter for consultation (one would hope – and not just with banks). Given the high probability of a recession in the next five years – and the limited firepower here and abroad to deal with a severe recession – some might reasonably wonder at just how wise it would be to compel big increases in capital ratios over that five year period, at a time when the Bank’s own analysis repeatedly suggests the banks are sound with current capital levels. Credit availability might well be more than usually constrained.

One might go on to note that the level of disclosure in the consultative document is seriously inadequate for such a substantial intervention – one that would take New Zealand further away from the international mainstream not closer to it. As I noted in a post a few days ago, back in 2012 the Bank published a fuller cost-benefit analysis of the sorts of capital requirements that were then in place. There is nothing similar in the consultative document issued last week, not even (I gather) any engagement with the previous cost-benefit analysis. Given the amounts of money involved, that is simply unacceptable. I’ve lodged an Official Information Act request for the (any) modelling and analysis they’ve done, but I (and others) shouldn’t have needed to; it should have been released as a matter of course. In fact, even better they should have published a series of technical background papers over the year, held discussions with a range of interested parties (not just banks) before coming to the decisions they chose to formally consult on. That is what good regulatory process might have looked like.

And then there is that bold final claim

Outcomes will be superior and better understood and owned by society

I’m all for effective and professional relationships between the Reserve Bank and the banks it regulates. Perhaps that may even lead to better policy outcomes, but there is no guaranteee of that (after all, at the end of it all the law allows the Governor to make policy pretty much on a personal whim – which is a lot like what the proposed higher capital ratios feel like). But quite how a better relationship between the Reserve Bank and the banks will make outcomes “better understood and owned by society” is a complete mystery to me. There are plenty of examples of regulators and the regulated ganging up against the public interest, and others of the regulators ramming through changes that might – or might not – be in society’s interest. There is simply no easy mapping from a better relationship between the Bank and the banks, and good outcomes for society, let alone ones that – whatever it means – are “owned by society”. Good outcomes rely heavily on very good and searching analysis. And nothing in the Charter commits the Bank to that.

When one reads the argumentative second half of the press release it is little wonder the banks themselves wanted nothing to do with the statement. I guess there isn’t much chance of the banks and the Reserve Bank getting too close to each other in the coming months as they (and the bank parents and APRA no doubt too) fight over the billions of additional capital Adrian Orr thinks they should have.

Meanwhile, the Governor can play at tree gods. But it would be much better for everyone, including most notably citizens, if he were to engage openly and (in particular) more substantively on the issues he has legal responsibility for. Cartoons and glib statements don’t build confidence where it counts.