I wasn’t planning to write today about the Reserve Bank’s proposed new bank capital requirements, announced yesterday. I’ll save a substantive treatment of their consultative document until (after I’ve read it and in) the New Year. But I found myself quoted in an article on the proposals in today’s Dominion-Post, in a way that doesn’t really reflect my views. Perhaps that is what happens when a journalist rings while you are out Christmas shopping and didn’t even know the document had been released. But I repeatedly pointed out to him that, despite some scepticism upfront, I’d have to look at documents in full and (for example) critically review any cost-benefit analysis the Bank was providing before reaching a firm view.

The gist of the proposal was captured in this quote from Deputy Governor Geoff Bascand

“We are proposing to almost double the required amount of high quality capital that banks will have to hold,” Bascand said.

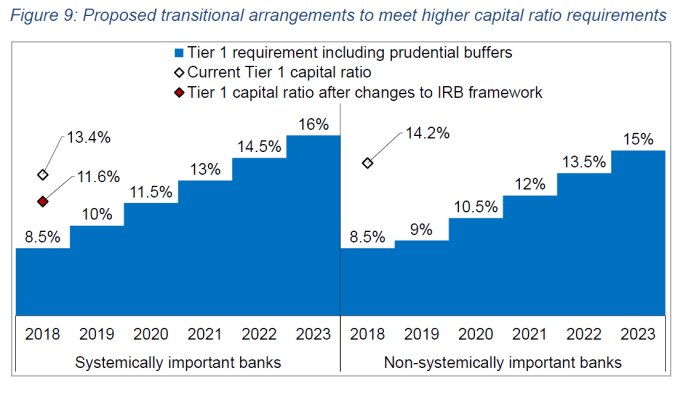

Or in this chart I found on a quick skim through the document.

These are very big changes the Governor is proposing. As I understand it, and as reflected in my comments in the article, they would leave capital requirements (capital as a share of risk-weighted assets) in New Zealand higher than almost anywhere else in the advanced world.

These were the other comments I was reported as making

The magnitude of the new capital required by banks surprised former Reserve Bank head of financial markets, Michael Reddell, who now blogs on the central bank.

A policy move of this scale would have an impact on the value of New Zealand banks, though ASB, BNZ, Westpac and ANZ are all owned by Australian companies listed on the ASX sharemarket.

“If these were domestically listed companies, you would see the impact immediately,” Reddell said.

That would be through a fall in the price of their shares.

Many KiwiSaver funds own shares in the Australian banks.

I think the journalist got a bit the wrong end of the stick re the first comments – perhaps what happens discussing such things, sight unseen, in a carpark. In many respects the magnitude of the increase isn’t that surprising given that the Governor had already indicated – a week or so before – his desire to have banks able to resist sufficiently large shocks that, on specific assumptions, systemic crises would occur no more than once in 200 years. That is much more demanding than what previous capital requirements have been based on – the same ones the Reserve Bank produced a cost-benefit analysis in support of only five or so years ago, and which have had them ever since declaring at every FSR how robust the New Zealand banking system is.

As for the second half of the comments, they were a hypothetical in response to the journalist’s question about whether higher bank capital requirements would be felt in wealth losses by (for example) people with Kiwisaver accounts who might hold bank shares. He was uneasy about the line the Bank used that the increased capital requirements were equivalent to 70 per cent of estimated/forecast bank profits over the five year transitional period (of itself, this isn’t an additional cost or loss of wealth). My point was that if the New Zealand banks (subsidiaries of the Australian banks or Kiwibank) were listed companies, such an effect would be visible directly, because (rightly or wrongly) markets tend to treat higher equity capital requirements as an additional cost on the business, and thus we could have expected the share price of the New Zealand companies to fall, at least initially. As it is, I’d have thought it would be near-impossible to see any material impact on the share price of the parents (or thus on the value of any shares held in Kiwisaver accounts).

My bottom-line view remains the one I expressed here a couple of weeks ago

Time will tell how persuasive their case is, but given the robustness of the banking system in the face of previous demanding stress tests, the marginal benefits (in terms of crisis probability reduction) for an additional dollar of required capital must now be pretty small.

And, thus, I’m looking forward to critically reviewing their analysis, including in the light of that previous cost-benefit analysis. Is it really worth compelling banks to hold much more capital than the market seems to require (even from institutions small enough no one thinks a government will bail them out)?

In thinking through this issue, there are some other relevant considerations to bear in mind. The first is to reflect on just how unsatisfactory it is that decisions of this magnitude are left to a single unelected individual who, in this particular case, does not even have any particular specialist expertise in the subject. And his most senior manager responsible for financial stability only took up his job a year ago, having previously had no professional background in banking, financial stability or financial regulation. The legislation is crying out for an overhaul – big policy decisions like these really should be made by those we can hold to account (elected politicians). And note that banks have no substantive appeal rights in these matters, even though the Governor is, in effect, prosecutor, judge and jury, and (in effect) accountable to no one much.

The other is to note that there is likely to be very considerable pushback from Australia on these proposals – both the parent banks of the subsidiaries operating here and, quite probably, from the Australian regulator (APRA) itself. The proposed new capital requirements here are far higher than those required in Australia (and for the banking groups as a whole). APRA has adopted a standard that Australian banks should be capitalised so that the system is “unquestionably strong”, but their Tier 1 capital requirement is apparently “only” 10.5 per cent. Of course, subsidiaries operating in New Zealand are New Zealand registered and regulated banks, and our authorities should be expected to regulate primarily in the interests of New Zealand. We won’t look after Australia, and they are unlikely to look after us, in a crisis (and coping with crises are really what bank capital is about). But you have to wonder why we should be inclined to place such confidence in our Reserve Bank’s analysis, relative to that of APRA – an organisation with (especially now) much greater institutional depth and expertise. Given the legislated trans-Tasman banking commitments, and the common interests of the two sets of authorities in the health of the banking groups, one can’t help thinking that it would have been more reassuring to have seen the two regulators (and the two governments for that matter – limiting fiscal risks in the event of bank failure) reach a rather more in-common view on the appropriate capitalisation of banks in Australasia.

But perhaps the Governor really is leading the way, supported by compelling analysis. More on that (superficially unlikely) possibility in the New Year. In the meantime, for anyone interested, there is a non-technical summary of their proposal (although not of any supporting analysis) here.