At the time the PREFU was published in August, I ran a short post illustrating that not even Treasury seemed to believe there was any prospect of increasing the export share of GDP in the next few years. Their projections were that, on the then-government’s policies, the decline in the export share would continue unabated over the years to 2021.

The next set of Treasury forecasts were published in the HYEFU yesterday. We have a new government – even a Minister for Export Growth – so I was curious to see what the updated forecasts looked like.

This chart captures the actual export share of GDP, now through to the June 2017 year, and shows separately the PREFU and HYEFU forecasts.

There is a bit of a lift between PREFU and HYEFU, but interestingly the downward trend is still in place in the last set of numbers.

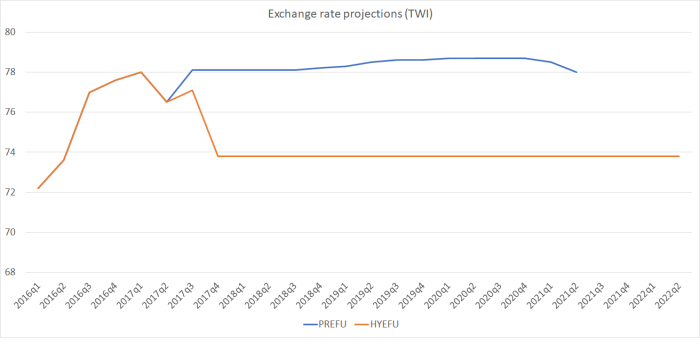

What has changed? Mostly the exchange rate. Here are the assumptions/projections for the exchange rate in the two sets of forecasts.

Over the full forecast horizon, the exchange rate is now assumed to be around 5.5 per cent lower than was previously assumed – more or less just treating the fall in the last few months as if it will be sustained. Some of that fall will flow through into the domestic price level, but it is still a real exchange rate fall of around 5 per cent. But even though that fall is assumed to be sustained for several years – 4.5 years to the end of the forecast horizon – there is no sign of the decline in New Zealand’s export share of GDP being reversed. Presumably it would need (policy changes that brought about) a much larger sustained decline to really begin to make a substantial difference.

I know some commentators think the exchange rate could soon fall quite a bit further – after all if the US keeps on raising interest rates, they’ll soon have a Fed funds target rate equalling our OCR. But Treasury doesn’t think that is likely: they still have large increases in the OCR (and 90 day rates) forecast for the next few years, far larger (and sooner) than anything in the Reserve Bank’s numbers. Frankly that still seems unlikely, but these are the projections/advice of the government’s leading economic advisory agency. On their numbers, the prospects for the tradables sector don’t look good.

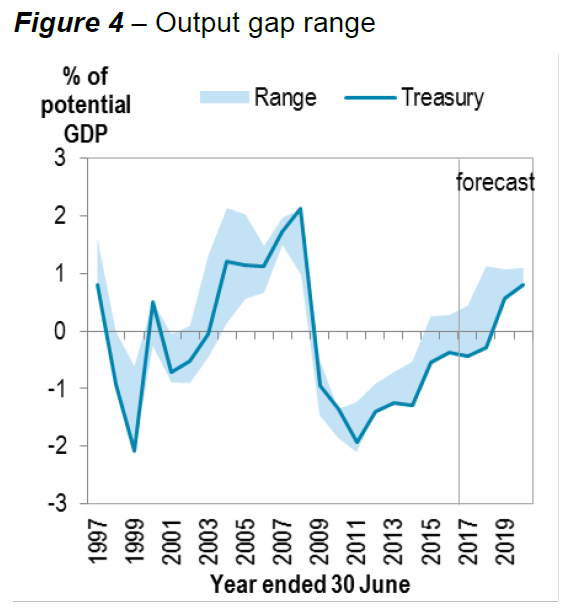

There are other sobering aspects in the numbers. Take this chart for example.

The solid line is the Treasury estimate – on their numbers the output gap is still estimated to be negative, bringing to 10 years the period in which our leading economic advisers think the economy has been running below capacity. When things like that happen – and they shouldn’t – it is usually an adverse reflection on macroeconomic management. It also isn’t very clear why things should suddenly come right next year – with a forecast of the biggest change in the output gap in the last decade, suddenly moving the economy into an excess demand situation. We’ll see.

And there are also some heroic forecasts for productivity growth. Recall that we’ve had no productivity growth at all for five years now. Treasury don’t expect any this year either. But then suddenly things come right, and over the subsequent four years growth in real GDP per hour worked is expected to exceed 1.5 per cent per annum. On quite what basis – other than wishful hope – it isn’t really clear. Apart from anything else, the optimistic assumption probably flatters the fiscal numbers.

But in some ways the biggest mystery in the entire document is the bottom line fiscal numbers themselves. As I noted before the election, I found it hard to conceive that people voting for a change of governmnet, for a left-wing government, were really voting for government spending as a share of GDP to keep on falling. On the government’s – perhaps over-optimistic numbers, core Crown expenses in the last forecast year is expected to be smaller, as a share of GDP, than in any year of the previous National-led government. To be sure, lower government spending will keep some pressure off the real exchange rate, but there are other ways to deliver that outcome. And it is curious to think that the governing parties campaigned on the existence of all sorts of deficits in the provision of public services, and yet their fiscal numbers keep net debt (including the assets in the NZSF) dropping away to almost nothing.

I doubt it will happen: the economy is likely to be weaker (and it would be unprecedented if we got to 2022 without a recession) and spending pressures are likely to be greater than allowed for in these numbers, but these are plans the government is articulating and defending. I’m not entirely sure why.

But that is something to speculate on next year. This is the last post from me for the year. I imagine I’ll have found interesting stuff to write about – and the urge to do so – by the second week of January or even earlier, but it might depend on whether the glorious Wellington summer continues.

Wishing you a happy Xmas with family holiday time in Wellington. That sentence contains assumptions: I’m judging school is out and you have kids to amuse you, the weather in Wellington is mentioned because that is where you intend staying and that you still belong to a denomination that celebrates Xmas. There is some small finite chance you are enrolled for a month in a Buddhist retreat or facing a month in jail. The point is assumptions and that is what your article is about.

I was skeptical of the “” projections/advice of the government’s leading economic advisory agency “” before reading your article and it has done nothing to change my mind. It seems they spend too much effort doing fancy extrapolations and too little preparing for the unexpected.

While you have a month off I might look up PREFU and HYEFU and how they impact on the life of my family. Meanwhile advice: invest in the purchase of suntan lotion – a wise investment even when sadly it is not needed.

LikeLike

Can we assume the following realtime information sites are Real or are they Fake?

They have been around for some time and never been questioned or ridiculed or lapsed or disappeared as nonsense things usually do

What are the odds of NZ Treasury or NZ Government providing Real Realtime data like this – obviously it is do-able

Realtime US Debtclock

http://www.usdebtclock.org/

Realtime World Energy consumption

http://www.usdebtclock.org/energy.html

LikeLike

Can we assume the following realtime information sites are Real or are they Fake?

They have been around for some time and never been questioned or ridiculed or lapsed or disappeared as nonsense things usually do

What are the odds of NZ Treasury or NZ Government providing Real Realtime data like this – obviously it is do-able

Realtime US Debtclock

http://www.usdebtclock.org/

Realtime World Energy consumption

-http://www.usdebtclock.org/energy.html

LikeLike

When Tourism and International students became a $15.5 billion dollar industry and our largest exports, the flow through into domestic GDP is almost 100%. Do not expect Export GDP to increase as a percentage of Total GDP. That measure is redundant in our current Export mix and does not mean anything much.

LikeLike

Thanks for your insights this year Michael. Happy Christmas to you and your family. Look forward to reading your thoughts in the new year.

LikeLike

The title as Minister of Export growth is just rather silly. It has to be better defined because it is not just any export growth we want. We want high productive and high skilled export growth which does point towards our budding Space Centre, Rocket Lab in Gisborne or basically the next Samsung. Note that Samsung is a significant Korean government subsidised company from its inception to even now as a matured export entity competing on the global stage.

Better to make it clear that it is High Productive and high skilled Export Minister.. Otherwise we get more of the same low skilled Tourism and International students and very doubtful primary sector high productivity(because NZ economists can’t do maths) when you start to count the 10 million cows and the 30 million sheep thats missing from the productivity denominator calculations.

LikeLike

Perhaps the title should be High Productive(not including Primary industries) and High skilled Export Growth Minister would be more appropriate.

LikeLike

[…] Michael Reddell, author of the Croaking Cassandra blog, takes a look at some aspects of the HYEFU re… […]

LikeLike

Thanks for supplying the elusive ‘free lunch’: very much appreciated. Enjoy the break and happy Christmas!

LikeLike

“To be sure, lower government spending will keep some pressure off the real exchange rate.”

By ‘pressure off’ I am assuming you mean it will keep the exchange rate lower?

Excuse my little plebian very amateur brain once again, but could someone more learned than me who has studied economics explain to me why lower government spending will necessarily keep the exchange rate low?

Is it through the idea that increased government spending would raise interest rates (via OCR increases because of inflation rising or via increased yield demands on bonds via government borrowing passing through into other areas of th economy – crowding out etc) and this would lead to capital inflow raising the exchange rate?

Is that the mechanism?

Hasn’t NZ had periods of low exchange rates combined with high public debt since the currency floated? Mid 90s? Hasn’t the exchange rate been quite high recently even though the government has been running surpluses?

So the idea is that if the new government spent a bit more they would harm exports via the exchange rate going up?

LikeLike

Just very briefly, there is no reason to think low govt spending will keep the exchange rate low, just a bit lower than it otherwise would be. As you suggest , lots of other things influence the level of the exch rate at any point in time.

LikeLike

Lower government spending does not actually equate to a lower exchange rate. The exchange rate is dependent on someone selling the NZD and someone else prepared to buy the NZD. What drives the NZD is mainly supported by the high interest yield. Micheal with no correlation studies points to immigration demand but with $500 million to $1 billion in NZD traded everyday, it is difficult to correlate $200 billion to $300 billion in NZD trading to migrant arrivals of only 15k a year, say they are all wealthy and bring in $1 million. The total NZD brought in a year equates to only around $15 billion. If we count the international students, around 125k each year requires around $4.5 billion. Tourists would have a large impact of $11 billion a year.

Therefore it is global speculation but driven usually by the interest rate yield compared to the rest of the developed world and the OECD. Interest rates are set by the RBNZ through the OCR which underpins the trading pattern for the 90 bank bill rate. The lack of competition and the monopoly by Australian owned banks prevent competition. The RBNZ also controls the setting for Loans as a percentage of local deposits which in effect prevent the large international banks from competing in our local market with their massive overseas savings deposits as they are required to attract local savers with higher interest rates which makes their lending uncompetitive against the Australian banks who have a large installed base of savers.

LikeLike

Note that when I arrived as a migrant I had only $250 dollars in my pocket not $1 million. So not all migrants arrive with $1 million.

LikeLike

Oh and have a great break! I’ll miss your blog though – I’ll have to read old ones instead.

LikeLike

Michael it has been such a pleasure. A great year for the blog. Hope you and your family have a good xmas and keep enjoying the good weather. The 2 degree temperature difference in Island Bay is now working to your benefit.

LikeLike

Oh and the MBIE comment on immigration not helping GDP per capita. Declare victory on that one.

LikeLiked by 1 person

Labour’s new immigration minister already recognised that it is the jobs that are driving the immigrant numbers and have now gone off having exact numbers. He has indicated clearly that it is not a numbers issue but an issue of getting the right people with the right skills in the right place and at the right time. Finally some common sense from the Labour government.

LikeLike

Not too sure how a victory can be declared when a solution has not been proposed. It is like saying that finally, you have got MBIE to comment that the Soul Bar, a top class restaurant in Auckland has 15 chefs and 30 waiters and its a problem. Therefore MBIE acknowledges there are too many waiters. But to Soul Bar which is a commercial enterprise aiming to make a profit, thats the correct number of chefs and waiters to provide the correct balance of great service and profit. So what?

LikeLike

Wallace Chapman had this man on

https://www.socialeurope.eu/immigration-and-economic-growth-is-keynes-back

He didn’t discuss GDP per capita

https://tradingeconomics.com/sweden/gdp-per-capita

And he used the line that people in Sweden are ageing so “who is going to do the work?”

LikeLike

I see some want to lower wages to smooth out unemployment problems – all eyes on the refugees.

LikeLike

A disturbing reveal about our erstwhile information provider Statistics New Zealand

Seems like another monumental governmental inability to provide IT Systems

This is a $121 million episode

As time goes on and these events rear their heads it doesn’t give great confidence in these outfits provide

https://www.newsroom.co.nz/2017/12/17/69331/concerns-raised-over-census-it-system

And un-suprisingly they have resorted to the tried and proven obfuscation to an OIA request

It’s an art form

LikeLiked by 1 person

The Dark Art of Deception – or – try the Art of Obfuscation

An interesting Thesis by Matthew Gibbons on Government Expenditure published in Policy Quarterly – Volume 13, Issue 2 – May 2017

http://igps.victoria.ac.nz/publications/files/26d128e4237.pdf – try digesting that

The HYEFU refers to Fiscal Expenditure of $99 billion or 39% of GDP – I went looking for a definition of Fiscal Expenditure – not very successful – Michael refers to Government Spending in 3 instances in the article – I’m mainly interested in the Fiscal Expenditure as that includes the increases in social programs being proposed by the Current Government. As the expenditure is targeted at welfare recipients we can assume 99% of it will translate into consumption and will not be saved or capital created – thus it will be GDP accretive

Fiscal Expenditure is 40% of GDP. The Government is indirectly responsible for 40% of national GDP. Thus it can be extrapolated that GDP will rise by the $3 billion projected in the HYEFU. That is not accounted for any unforseen unbudgeted government fiscal expenditure

The point of this is that increases in Government Fiscal Expenditure do not translate into increases in merchandise exports or for that matter probably don’t translate into increased tourism which will soon produce increased further domestic expenditure in the form of grants to local bodies for the provision of postponed expenditure in the regions for tourist facilities such as toilets and cabin parks and freedom-camping facilities.

It has been stated before that Government tends to self-sabotage. It proposes to increase exports as a percent of GDP but immediately increases the domestic component of GDP at a faster rate than exports can increase. I have stated before that immigration that is not directed directly into the export sector has exactly the same effect

Searching for Tourism as an Export Earner google produces a number of SERPS declaring Tourism is now the largest export earner overtaking Dairy and Meat. Yet on searching NZ Statistics can only find results for merchandise exports

Merchandise Exports Calendar December Y/E

2015 $49 billion

2016 $49 billion

2017 $50 billion est

Fiscal Expenditure HYEFU

2015 $95 billion NZD

2016 $96 Billion NZD

2017 $99 Billion NZD

Imports

2015 $53 billion

2016 $52 billion

2017 $55 billion est

GDP

2014 $200 billion USD 0.80

2015 $176 billion USD 0.70

2016 $185 billion USD 0.75

2016 $251 billion NZD

2017 $270 billion NZD

LikeLike

Economic contribution (year ending March 2016)

Tourism market Expenditure ($b) Growth (pa)

International + 14.5 19.6%

Domestic 20.2 7.4%

Total 34.7 12.2%

+Includes international airfares paid to New Zealand carriers.

Tourism Exports

International tourist expenditure accounted for $14.5 billion or 20.7% of New Zealand total export earnings.

Tourism Contribution to GDP

Tourism directly contributes $12.9 billion (or 5.6%) to New Zealand total GDP. A further

$9.8 billion (or 4.3%) is indirectly contributed. When comparing tourism to other industries, the direct contribuƟon should be used.

Tourism Employment

Tourism directly employed 188,136 people (7.5% of the total employment in New Zealand)

Click to access key-tourism-statistics.pdf

LikeLike

In 2015, tourism became New Zealand’s largest export earner

as visitor numbers set records and dairy prices fell. The wider

Tourism, Hospitality and Recreation sector, the subject of this

report, employed nearly 204,000 full-time equivalent workers

(FTEs) in 2014, or one in 11 workers. It contributed $11.0 billion,

or 4.8%, to New Zealand’s GDP.

The sector covers tourism services like air travel, travel agencies

and accommodation, but also includes hospitality and recreation

services consumed by local residents, such as food and beverage

services, sports venues, gyms, museums, the performing arts,

and regional parks.

Tourism, Hospitality and Recreation provides a large number

of jobs for those with fewer qualifications, including tens of

thousands of part-time jobs. Many of these are students working

toward other qualifications, or new entrants to the workforce.

Westpac

Real wages have fallen 24.5% between 1979 and 2006, that is a lot of people not saving enough to retire on.

LikeLike

GDP v GNI: The most common metric of economic growth is

gross domestic product (GDP). What GDP measures fail to

account for, however, is where a business is owned, and

therefore the likelihood of profits staying in New Zealand.

The dairy sector is overwhelmingly New Zealand owned,

meaning any profits (or losses) remain in New Zealand.

In contrast, many tourism businesses operating in New

Zealand, particularly in accommodation and air travel,

are overseas owned, which means profit is likely to be

repatriated, reducing the economic benefits, and specifically

gross national income here.

Westpac

LikeLiked by 1 person

New Zealand Government Spending

Government Spending refers to public expenditure on goods and services and is a major component of the GDP. Government spending policies like setting up budget targets, adjusting taxation, increasing public expenditure and public works are very effective tools in influencing economic growth. This page provides the latest reported value for – New Zealand Government Spending – plus previous releases

https://tradingeconomics.com/new-zealand/government-spending

Government Spending in New Zealand increased to NZD $11207 million in the second quarter of 2017 from NZD $11104 million in the first quarter of 2017

Government Spending is running at $11 billion per Qtr or $44 billion per annum

Fiscal Spend $99 bn + Government Spend $44 = $143

Assuming most of Fiscal Spend of $99 bn is consumption then The New Zealand Government accounts for 55% of the NZ economy

LikeLike

The point is, success or failure of increasing exports as a share of GDP is largely in the government’s hands – it has to stop moving the goalposts

LikeLike

Tourism directly contributes $12.9 billion (or 5.6%) to New Zealand total GDP. A further $9.8 billion (or 4.3%) is indirectly contributed.

Therefore for every tourist dollar directly ie export GDP, there is a 78% conversion to domestic GDP indirectly. It is rather more difficult to achieve a higher export GDP to total GDP due to the myriad of domestic goods and services that impact on domestic GDP. Tourism has a multiplier effect on the local domestic economy that other industries would not have nor have a better wealth effect spread.

Most other export industries have only a small number of shareholders and employees that benefit directly and the conversion impact of only around 30% to the local economy due to a high level of imported components and products.

LikeLiked by 1 person

Surprise Surprise

Statistics New Zealand finds a new way of measuring GDP

National accounts senior manager Gary Dunnet explained Statistics NZ had increased its estimate of the size of the economy because of new measures

National Party finance spokesman Steven Joyce said the figures “finally put to bed the fallacy that New Zealand was having a ‘productivity recession'” under the previous government.

https://www.stuff.co.nz/business/industries/100069068/latest-gdp-figure-revealed

LikeLike

Unfortunately until we actually start focusing on a Samsung equivalent type industry we would continue to have productivity poverty with our focus on servicing the 125k international students and the 4 million tourists. When Grant Robertson rather foolishly believes that taxation would be the key towards higher productivity it is another 3 years of productivity poverty without a doubt.

LikeLike

Interesting. I will redo my productivity numbers when i’m Back.

LikeLike

One definition of GDP from Investing Answers

GDP represents the monetary value of all goods and services produced

Thus GDP is a compound calculation comprising PRICE and VOLUME

What is not revealed in the press release is value of each of the two components making up the revisions

2016 growth revision from 2.4% to 3.6% = 50% increase

2017 growth revision from 2.9% to 3.7% = 27% increase

If all of the revision is attributed to PRICE Effect is that productivity?

If all of the revision is attributed to VOLUME Effect that can be subdivided into

(a) population increase natural or immigration

(b) improved capacity utilisation

(c) improved productivity

Stephen Joyce is a bit quick off the mark don’t you think

NZ Statistics needs to clarify

Otherwise the magnitude of the two revisions are questionable

Until we get that analysis I don’t accept the revisions

LikeLike

One thing is clear to me: our society is dysfunctional because some questions cannot be asked (“you can’t pin them down”). You just can’t get the media to ask certain questions and the politicians act like reef fish.

…..

or perhaps I am wrong about that as when Corrin Dann tackled John Key (quoting Kerry McDonald). John Key doesn’t raise an eyebrow, he just says “well we don’t agree with that”?

LikeLike

Tēnā koe Michael,

Excellent work, thoroughly enjoyed, especially the bits I understood. Here’s to our even greater success in 2018.

Ngā mihi nui

LikeLiked by 1 person