At the time the PREFU was published in August, I ran a short post illustrating that not even Treasury seemed to believe there was any prospect of increasing the export share of GDP in the next few years. Their projections were that, on the then-government’s policies, the decline in the export share would continue unabated over the years to 2021.

The next set of Treasury forecasts were published in the HYEFU yesterday. We have a new government – even a Minister for Export Growth – so I was curious to see what the updated forecasts looked like.

This chart captures the actual export share of GDP, now through to the June 2017 year, and shows separately the PREFU and HYEFU forecasts.

There is a bit of a lift between PREFU and HYEFU, but interestingly the downward trend is still in place in the last set of numbers.

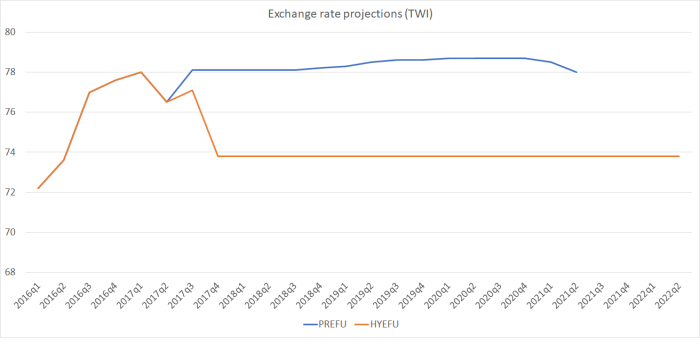

What has changed? Mostly the exchange rate. Here are the assumptions/projections for the exchange rate in the two sets of forecasts.

Over the full forecast horizon, the exchange rate is now assumed to be around 5.5 per cent lower than was previously assumed – more or less just treating the fall in the last few months as if it will be sustained. Some of that fall will flow through into the domestic price level, but it is still a real exchange rate fall of around 5 per cent. But even though that fall is assumed to be sustained for several years – 4.5 years to the end of the forecast horizon – there is no sign of the decline in New Zealand’s export share of GDP being reversed. Presumably it would need (policy changes that brought about) a much larger sustained decline to really begin to make a substantial difference.

I know some commentators think the exchange rate could soon fall quite a bit further – after all if the US keeps on raising interest rates, they’ll soon have a Fed funds target rate equalling our OCR. But Treasury doesn’t think that is likely: they still have large increases in the OCR (and 90 day rates) forecast for the next few years, far larger (and sooner) than anything in the Reserve Bank’s numbers. Frankly that still seems unlikely, but these are the projections/advice of the government’s leading economic advisory agency. On their numbers, the prospects for the tradables sector don’t look good.

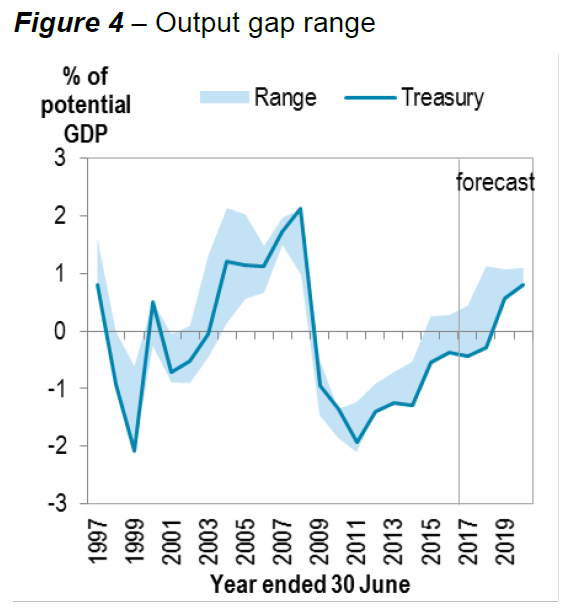

There are other sobering aspects in the numbers. Take this chart for example.

The solid line is the Treasury estimate – on their numbers the output gap is still estimated to be negative, bringing to 10 years the period in which our leading economic advisers think the economy has been running below capacity. When things like that happen – and they shouldn’t – it is usually an adverse reflection on macroeconomic management. It also isn’t very clear why things should suddenly come right next year – with a forecast of the biggest change in the output gap in the last decade, suddenly moving the economy into an excess demand situation. We’ll see.

And there are also some heroic forecasts for productivity growth. Recall that we’ve had no productivity growth at all for five years now. Treasury don’t expect any this year either. But then suddenly things come right, and over the subsequent four years growth in real GDP per hour worked is expected to exceed 1.5 per cent per annum. On quite what basis – other than wishful hope – it isn’t really clear. Apart from anything else, the optimistic assumption probably flatters the fiscal numbers.

But in some ways the biggest mystery in the entire document is the bottom line fiscal numbers themselves. As I noted before the election, I found it hard to conceive that people voting for a change of governmnet, for a left-wing government, were really voting for government spending as a share of GDP to keep on falling. On the government’s – perhaps over-optimistic numbers, core Crown expenses in the last forecast year is expected to be smaller, as a share of GDP, than in any year of the previous National-led government. To be sure, lower government spending will keep some pressure off the real exchange rate, but there are other ways to deliver that outcome. And it is curious to think that the governing parties campaigned on the existence of all sorts of deficits in the provision of public services, and yet their fiscal numbers keep net debt (including the assets in the NZSF) dropping away to almost nothing.

I doubt it will happen: the economy is likely to be weaker (and it would be unprecedented if we got to 2022 without a recession) and spending pressures are likely to be greater than allowed for in these numbers, but these are plans the government is articulating and defending. I’m not entirely sure why.

But that is something to speculate on next year. This is the last post from me for the year. I imagine I’ll have found interesting stuff to write about – and the urge to do so – by the second week of January or even earlier, but it might depend on whether the glorious Wellington summer continues.