Last week the Reserve Bank released an interesting Analytical Note on “Crypto-currencies – An introduction to not-so-funny moneys” . If, like me, you hadn’t paid a great deal of attention to Bitcoin and the like, it is a very useful introduction to the subject, from a monetary perspective (including some of the potential policy and regulatory issues). At least for me, it struck just the right balance of detail and perspective.

Analytical Notes are published with the standard disclaimer that the material in them represents the views of the authors rather than, necessarily, of the Bank. (That said, I’m pretty sure nothing has ever been published in one that the Bank was unhappy with.) They are mostly written by researchers rather than policy people. So it was interesting, and perhaps a little surprising, to get to the second to last page of this paper and find this

Work is currently under-way to assess the future demand for New Zealand fiat currency and to consider whether it would be feasible for the Reserve Bank to replace the physical currency that currently circulates with a digital alternative. Over time, analysis associated with this project will filter through into the public domain.

Interesting, because that is quite a radical and specific suggestion: to replace physical currency with a digital alternative. And surprising because there was no hint of this work – on a pretty major issue affecting all New Zealanders – in the Reserve Bank’s Statement of Intent released only a few months ago. Statements of Intent can seem like just another bureaucratic hoop to jump through, but the requirement to prepare and publish them was put in place for a reason: it is supposed to be the vehicle through which the Minister of Finance can inject his or her views on what the Bank’s work priorities should be, and is supposed to enable stakeholders and the public more generally to get a sense of what the Bank is up to.

I’m pleased the Reserve Bank is now doing this work on the future of currency. Over the last couple of years I have been critical of the fact that, in published documents, there was no sign of any such preparatory work going on (including, more generally, around dealing with the problems of the near-zero lower bound, which will almost certainly become binding for New Zealand in our next recession). In this year’s Statement of Intent, for example, published as recently as the end of June, there was 1.5 pages (pp 28-29) on the Bank’s currency functions, and not a hint of any work on the possibility of replacing physical currency with digital currency. Perhaps doing the work is an initiative of temporary “acting Governor” – but then he was required, by law, as Deputy Governor, to sign the Statement of Intent. Or perhaps it was just the Bank deliberately keeping things secret?

As usual with the Bank, they talk loftily about how the analysis will eventually “filter through to the public domain”. That isn’t good enough – this is publicly funded work on a matter of considerable potential significance – , and I have lodged an Official Information Act request for the research and analysis they have already done.

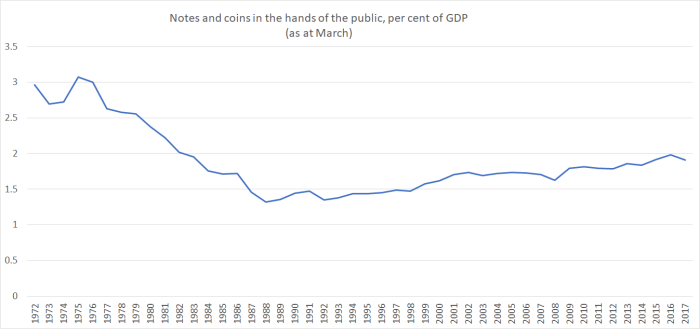

I’ve come and gone for decades on what the best approach to physical currency is. I’ve long been troubled by the monopoly Parliament gave to the Reserve Bank over the issuance of physical notes and coin. There is no good economic reason for it (nothing about the efficacy of monetary policy for example) – and for half of modern New Zealand history it wasn’t the situation in New Zealand. For decades it may well have led to inefficiently low currency holdings: in a genuinely competitive market there is a reasonable chance that (eg) serial number lotteries would have provided a (expected) return to holders of bank notes. In the high inflation years – and especially as interest rates were deregulated – holding as little currency as possible was the sensible thing to do.

As the chart shows, the ratio of notes and coins (in the hands of the public) to GDP troughed in the year to March 1988 – when inflation and interest rates were both high (and, of course, returns to holding currency were zero).

At one level, the partial recovery in the amount of physical currency held isn’t too surprising. Inflation has been low for decades, and interest rates are now very low too. Holding physical currency isn’t very costly at all.

Then again, there have been huge advances in payments technologies. Even when I started work, the Reserve Bank still offered to pay its staff (I think perhaps only the clerical and operational staff) in cash, and that wouldn’t have been too uncommon then. ATMs didn’t exist then – it was the queue at the local bank branch each Friday lunchtime – let alone EFTPOS, internet banking and so on. These days, by contrast, a huge proportion (by value) of transactions occur electronically. Even school fairs – often held out previously as the sort of place one really needed cash for – have often gone electronic to some extent at least.

And although the ratio of cash to GDP is quite low in New Zealand (by international standards – in many advanced economies something around 5 per cent isn’t uncommon – there is still a lot of cash around. The numbers in the chart are equivalent to a bit more than $1000 per man, woman, and child. For a household like mine, more than $5000. I’m a slow adapter, and almost always do have a reasonable amount of cash on me, but I’d be surprised if on an average day our household had more than $250 in cash in total (surveys from other countries suggest that isn’t unusual). I’m not sure I’ve ever had a $100 bill, but Reserve Bank data suggest that on average each man, woman, and child has $400 in $100 bills.

As it happens, last week I was reading (Harvard economics professor) Ken Rogoff’s book The Curse of Cash. As he notes, in the United States, there is around $3400 per man, woman, and child outstanding in US $100 bills – while surveys of what ordinary consumers are actually carrying suggest that no more than 1 in 20 adults has a $100 bill on them at any one time. Rogoff makes a pretty strong case that the bulk of physical currency holdings – even allowing, in say the US case, for the use of the USD in other countries – is held to facilitate illegality. That could be outright illegal activities – the drugs trade for example – or tax evasion in respect of the proceeds of lawful activities. The likely revenue losses, on his estimates, are very substantial. The scale of the problem is probably smaller here, but there is no point pretending that the issue is specific to the United States (and, as Rogoff documents, a number of European countries have now put limits on the maximum size of cash payments – although such rules seem more likely to catch those who comply with the law, rather than those who knowingly break it).

Somewhat reluctantly, Rogoff’s book has shifted my perspective on the physical cash issue. As a macroeconomist, my main interest in this area in recent years has been to do something about the near-zero lower bound on nominal interest rates. If the Reserve Bank cut interest rates to, say, -5 per cent, it would be attractive for people to pull money out of banks and hold it in physical currency in safe deposit boxes. If that happened to any large extent it would substantially undermine the effectiveness of monetary policy. The fear that it might happen has already constrained central banks in various countries, and no one has been willing to cut official interest rates below 0.75 per cent (which was also about how far we thought the OCR could be cut when I led some work on the issue at the Reserve Bank some years ago).

Getting rid of physical currency altogether would solve the problem. If there is no domestic cash, clearly you can’t hold any. Of course, you could always seek out foreign cash, but the process of doing that would lower our exchange rate – one of the ways monetary policy works, and thus not a problem. But one doesn’t need to get rid of cash – or even just large denomination notes – to limit that risk. There are various clever options that have been developed in the literature (effectively involving an exchange rate between physical and electronic cash), and as I’ve noted here previously, one could achieve the same result by simply putting a physical limit on the amount of currency the Reserve Bank issues, and then auctioning it to the banks (if demand surged this would, in effect, introduce an exchange rate or a fee). It is disconcerting that, as far as we can tell, no country is properly prepared to use options like these in the next recession (which, in itself, risks exacerbating the recession because smart observers will recognise that governments have fewer options than usual) – no one has (at least openly) done the preparatory legal work, or prepared the ground with the public. Our Reserve Bank is, as as we can tell, no exception.

I’ve resisted the idea of getting rid of physical currency on both convenience and privacy grounds. There is, as yet, no real substitute for cash if – say – one wants to send a child to the local dairy to buy the newspaper when one is on holiday. And the ability to conduct entirely innocent transactions without the state being able to know what one is spending one’s money on (or one’s bank for that matter) remains a very attractive ideal.

And yet….and yet…..I wonder if it is a real freedom now to any great extent anyway. We might not gone all the way – yet – to China’s “social credit” scoring system, but you have to be pretty determined to avoid the gaze of a government determined to find out what you’ve been up to. Some of that is voluntary – people choose to carry phones around, for example, which locate you – and some of it isn’t (local councils put up CCTVs, and so do all too many retailers). AML provisions, and know-your-customer rules are ever more pervasive and intrusive. Sure, using cash enables one to keep from a spouse what one spent on a birthday present, or where it was bought from, but it is a pretty small space left.

And so perhaps it is best for us to think now about serious steps towards phasing out physical currency. Rogoff himself doesn’t recommend complete abolition at this stage, but rather ceasing to issue, and then over time withdrawing, high denomination notes. Our largest note isn’t very large at all (NZD100 is only around USD70) but as I noted earlier a huge share of currency in circulation is in the form of $100 bills, even in New Zealand, which few people use for day-to-day transactions that are both lawful in themselves and where there is no intention to evade lawful tax obligations. But if we were to amend the law to prohibit the Reserve Bank from issuing notes larger than (say) $20 – and this is a decision that should be made by Parliament or at least an elected minister, not by a single bureaucrat – we’d still make small cash transaction easy enough (school fair, or the kid sent to buy the newspaper, while greatly increasing the difficulty of a major flight to cash in the next serious recession, and increasing the difficulty of tax evasion and other criminal transactions.

If the government were to choose to go this way, it would still make sense for active precautions to be taken now to reduce the risk of the effectiveness of monetary policy being undermined even by a flight to $20 notes – they take up roughly five times as much space as the equivalent amount in $100 notes, but you can still fit a lot of money in a secure vault. Whatever the mix of measures, it is really important that the authorities – Bank, Treasury, IRD, government, FMA – adopt a greater degree of urgency. No one knows when the next serious recession will be, but it isn’t prudent (ever) to assume it is far away.

And what of the Reserve Bank’s own scheme: the possibility of replacing physical currency with digital Reserve Bank currency? We need to see more of what they have in mind. My own long-held prediction is that they are two quite different products – only the RB can issue physical notes, while anyone can issue electronic transactions media – and that in normal times demand for a Reserve Bank retail-level digital currency would be almost non-existent. That doesn’t mean they shouldn’t do it: there is something about the democratisation of finance, in enabling the public to hold the same sort of secure liability banks already can (in their case electronic settlement account balances), and – as we saw globally in 2008 – banks runs can still happen. Unless society decides to completely up-end the entire monetary system (and I have readers who favour that), we need an “outside money” that people can convert their bank liabilities into if/when they lose confidence in the issuing institution or system. For most purposes, a digital Reserve Bank retail currency should be able to do that at least as well as physical banknotes.

Most….but not necessarily all (when serious people worry about EMP attacks on/by North Korea, there is no point pretending electronics is the answer to everything). Those are the sorts of issues that need to be carefully examined, preferably in an open way, rather than with conclusions loftily filtered out to the public when it suits the officials.

Rogoff’s book is worth reading, especially (but not only) if you are new to the issue. He covers a range of issues I didn’t have space for, including natural disasters (where cash might be more useful than cards, but most people don’t hold much cash anyway, so it actually isn’t that much of a help.) Like the Reserve Bank paper, he also points out that things like Bitcoin offer a lot less effective anonymity than many people realise.