Earlier in the week, Graeme Wheeler completed his term as Governor and left office. Even in a week with little real news to report, his departure didn’t seem to receive any notice in the media. Not even the Herald managed an enconium. Surely his departure must go unlamented almost everywhere, even if, no doubt, the Bank’s Board – supposedly guardians of the public interest, but in fact guardians of the Governor – gave him a good dinner on the occasion of their meeting last week?

And now Grant Spencer – erstwhile deputy chief executive – purports to be in charge, as “acting Governor” until a permanent appointment can be made by the incoming Minister of Finance. I like Grant. He was my boss in two separate stints spread over many years, and – in the late 80s – was a voice of reason and moderation in an age when young hotheads didn’t always welcome such perspectives. Now that he purports to wield so much untrammelled power – not just monetary policy, but all the Bank’s regulatory functions – I’m sure his management skills must also have improved further. I like to tell the story of the two years, very early in my management career, without any structured performance feedback from him: the only way I could really be confident I must have been doing ok was through the annual pay round, but when he came to deliver that news I was on the phone, so Grant scribbled the number on a piece of paper, dropped it on my desk, and left. But I’m sure he would be a safe pair of hands, minding the store.

Unfortunately, his purported appointment – probably sensible in intention if Graeme Wheeler couldn’t have been persuaded to take a temporary extension – is, as I’ve been pointing out for months, probably unlawful. (If, as a new reader, you are puzzled by that claim, you can read for yourself my thoughts on the summary of Crown Law’s legal advice on the issue. I still have with the Ombudsman a request for (a summary of) the Reserve Bank’s own lawyer’s advice.)

And if his appointment is unlawful then so, presumably, are all the acts the Bank takes – or purports to undertake – under his authority over the next few months. Including setting the OCR.

Again, that proposition might puzzle you. Surely even if there was some question over the lawfulness of the appointment of an acting Governor in these circumstances, there would be no question of the lawfulness of the Bank’s actions? I had a look at the legislation a few months ago.

Does it all matter? Sometimes laws contain provisions stating that any problems in the appointment of an officeholder, or doubts about the validity of the appointment, don’t affect the validity of enforceability of the actions/decisions taken by that person.

In fact, the Reserve Bank Act has one of those provisions. For the Board. Under section 54(4)

The validity of any act of the Board is not affected by—

(a) any vacancy in its membership; or

(b) any defect in the appointment of a director; or

(c) the fact that any non-executive director is disqualified from appointment under section 58.

But there is simply nothing comparable for the Governor. Curiously, there is protection for the Deputy Chief Executive when exercising delegated authority from the Governor. Under section 51

The fact that the Deputy Chief Executive exercises any powers or functions of the Governor shall be conclusive proof of the authority to do so, and no person shall be concerned to inquire whether the occasion for doing so has arisen or has ceased.

But there is nothing like it for the Governor, or any acting Governor. There is simply a requirement on the Board and the Minister to make a proper appointment, and to have that person in place once the previous Governor’s term ends (and presumably an expectation that Governor appointments are sufficiently high profile, and as all powers of the Bank rest with the Governor, no questions should ever arise about the authority of the Governor him or her self to make decisions.

(Again, it is perhaps worth noting that there are also no such protections in the 1964 Act – the one in place when the 1989 Act was being drafted. The drafters presumably made conscious choices about what to add and what not to.)

If the appointment of Spencer as acting Governor is unlawful, it looks as though any actions taken by him – or under his (purported) delegations during his term – would also be unlawful.

Perhaps it won’t matter very much. Few people expect the OCR to be changed in the next six months, and if so perhaps they could argue that successive OCR decisions aren’t actions but inactions – just leaving things as Wheeler left them.

But the Reserve Bank does lots of other stuff. They commit to commercial contracts, they deal in New Zealand in international markets. They take enforcement actions against financial institutions that fall foul of the law, or of the Bank’s rules. And so on. In a crises, they (the Governor) has substantial regulatory powers.

The situation should never have been allowed to arise. As I’ve noted for months, it was easily avoidable, with a simple temporary change to the Reserve Bank Act (which there is no obvious reason for the Opposition parties to have opposed – either on the substance, or as regards Spencer personally, whom everyone regards as a decent and honourable person). But now we have an unlawful appointment, and Spencer purporting to exercise the powers of (acting) Governor.

But what of the OCR press release – which, as pure commentary, I suppose Spencer is free to issue? It probably isn’t that sensible to make much of minor differences in wording: in some areas Spencer may just use slightly different hobbyhorse phrasing than Wheeler would have. But no one sees it as a material departure from last Wheeler statement, even if (perhaps) the confidence in the growth outlook might be fading. As for what it might mean for actual (or purported) OCR setting, not much. After all, it is quite plausible that a new Minister of Finance and coalition could mean modifications to the Policy Targets Agreement almost straightaway (happened in 1993, 1996, and 1999). And even if that doesn’t happen, Spencer won’t be there to offer his opinion by the end of March, and no one knows who the new Governor will be, or what mandate he or she will be working towards.

The growth outlook was one of the issues I touched on in my comments on the last Monetary Policy Statement. Those comments still seem largely valid now – the June quarter GDP numbers were flattered by big one-off boosts to services exports from the World Masters Games and the Lions tour, and yet still showed growth of only 0.8 per cent.

But perhaps my biggest puzzle is where all the forecast growth is coming from.

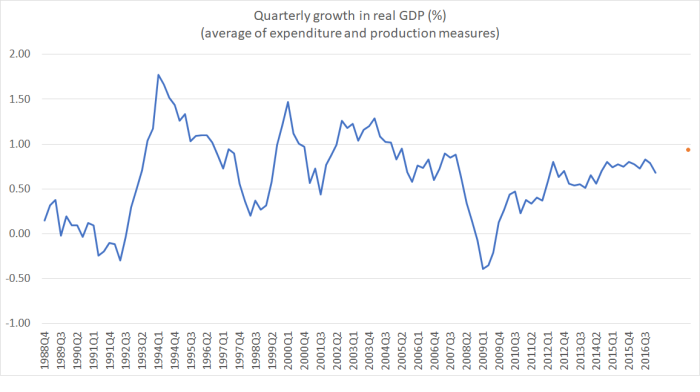

Over the next six quarters, the Bank projects that quarterly GDP growth will average just over 0.9 per cent. This chart shows six-quarter moving average of GDP growth (in turn, averaging the production and expenditure measures).

The orange dot shows the forecast for the next six quarters. Their projections suggest that the economy will grow more rapidly over the next 18 months than it has managed on a sustained basis at any time in the current recovery. You might not think that the difference looks large, but:

- the Bank already recognises that monetary conditions are tighter than they were last year,

- the Bank is forecasting a substantial reduction in the net migration inflow, and no one seriously doubts that unexpectedly rapid population growth has been the biggest single driver of headline GDP growth in recent years. However much immigration adds to supply, it adds a lot to demand.

So why are we to expect a sustained growth acceleration from here? Although it isn’t stated in the document, I hear that the Bank is invoking the expected fiscal stimulus (from promised measures announced in the Budget). In isolation that might make some sense, but against the projected halving in the net migration inflow and the actual tightening in monetary conditions, it doesn’t really ring true. If anything, the risk now has to be that over the next 18 months, headline GDP growth averages lower than we’ve seen in the last couple of years.

Whichever parties form the next government, and as I noted last week, it seems likely that government expenditure will be higher than projected. But it is still difficult to see a growth outlook as relatively buoyant as the Bank projected – and requires if inflation is to get back to target – as the most likely outcome.

And the Bank – and government – still seem grossly underprepared for the next recession, whenever it comes.

Ports of Auckland could be moved to a new “super port” in the Manukau Harbour or the Firth of Thames at a cost of $4 billion to $5.5 billion. That is one of the main findings of a Port Future Study report.

http://www.nzherald.co.nz/business/news/article.cfm?c_id=3&objectid=11666255

Guess a Port move to Marsden Point, Whangarei a Winston Peters bottom line would be a similar $5 billion cost.

LikeLike

If you add in all of NZ usual legal corruption unsavoury practices then the project would likely be around $8 billion with $3 billion in legal corrupt contingencies.

LikeLike

ah, but just think of all the construction activity – complete with “legal corrupt contingencies” – that wouldn’t be necessary if somehow NZF implemented what looks like their immigration policy.

LikeLike

Unfortunately NZF policy on immigration has shifted towards maintaining similar numbers and just a focus on shifting these new migrants towards the regions from Auckland. So don’t hold your breath expecting immigrations numbers to come down.

Even Jacinda Ardern has moved away from targetting foreign worker numbers because she needs those foreign workers and even more for Kiwibuild and monorail. She is now loosely indicating to take 30,000 off International students which wont happen because thats the new intake of international students for the entire year. Never going to happen. That will shave a billion out of a $4 billion export GDP and also the flowon to domestic GDP which is another billion. Thats $2 billion in GDP wiped from any surplus that she is planning to spend.

LikeLike

Oh, I don’t have any real expectations of any of our parties on issues around econ management, and it has been clear for some time that Ardern was backtracking on or downplaying their immigration policy. I just posed the immigration scenario as a slightly playful “what if”. I’ll be surprised if the port moves in the next few years either.

.

LikeLike

I think increasingly Tauranga will pick up the spillover and may become the preferred port over Auckland if they can get a reliable and fast rail link into Auckland, having already spent $400 million increasing the depth of its port and now has the deepest port in New Zealand. There has been in addition around a billion dollars spent in commercial property developments providing the jobs to sustain a growing population.

LikeLike

“The Reserve Bank does lots of other stuff. They commit to commercial contracts, they deal in NZ in international markets. They take enforcement actions against financial institutions that fall foul of the law, or of the Bank’s rules”

Really glad you said that because for some time I have been wondering just what the Bank does and how big it is – I know it has prudential responsibilities and jurisdiction over the balance sheets of banks and insurance companies and also money-launderers who do their dirty washing through the banks – oh and after gathering masses of data occasionally makes an OCR decision which I’m not convinced makes a heck of a lot of difference to the wider internal economy other than altering the cost of imports

But take enforcement action? Really? Do they? Haven’t noticed any – and I have been watching

Don’t see any evidence of it – or – are they another division of that busyness brigade

LikeLike

he RBNZ on Thursday released results of a recent survey it conducted with a sample of 36 of the 89 licensed insurers. This found that the overall level of compliance with disclosure rules was well short of minimum requirements.

http://www.interest.co.nz/insurance/88548/reserve-bank-unhappy-insurance-companies-overall-level-compliance-disclosure-rules

LikeLike

The RBNZ is prolific in issuing warnings

https://www.rbnz.govt.nz/regulation-and-supervision/cautions-and-notices

Hardly consider that to be enforcement action

With the palaver going on in AU with money laundering and the banks we must draw the conclusion that NZ is lily-white with clean-hands and IDMs were never installed in NZ

LikeLike

IDMs

At the very least I would have expected an absolute categorical statement from all the banks and RBNZ that IDMs were never installed in NZ. If they cant provide that statement then I would expect a statement from the RBNZ they are currently going through ASB like a dose of salts

LikeLike

Not obvious to me – but i might be wrong – that it is an RB function. The RB is primarily charged with the soundness of the system. Perhaps there are responsibilities they have under the AML/CFT powers – I never had much interest in those functions and stayed well clear when I was on the relevant oversight and policy committees.

LikeLike

These are some of the specific ones I meant

https://www.rbnz.govt.nz/regulation-and-supervision/industry-notices/

But, more generally, they do require banks to actually comply with their policies. Bank fear breaching RB stds – to a degree almost obsessively so. More importantly, it is when a bank was getting to trouble that those powers become particularly important.

LikeLike

Can you point to one instance of where the RBNZ has taken enforcement against a money-launderer as a result of a notification from one of the banks?

LikeLike

as i understand it, it is not the RB’s responsibility to pursue any launderers themselves, that is a matter for the Police. The Rb responsibility is as regards the banks’ own systems and procedures.

LikeLike

Ping An, a Queen Street, Auckland-based money remitter and foreign currency service provider, has been fined $5.29 million for “serious and systemic deficiencies” in complying with anti-money laundering laws.

Overall, Ping An failed to keep appropriate records for 1588 transactions totalling $105,413,026.44; the identity and verification of 362 customers; and the establishment and continuation of 122 business relationships.

http://www.interest.co.nz/business/90096/auckland-company-ping-fined-529-mln-calculated-and-contemptuous-disregard-anti-money

The margin on the transactions would likely only be 0.1% which equates to a profit of perhaps only $105,413 per annum. A fine of $5.29 million looks rather excessive and uncollectable. Sort of defeats the purpose of a fine and makes the Department of Internal Affairs a bit of a joke?

But where is the RBNZ because there is no way $105 million gets transferred without banks being in the middle of that transaction. The fine of that size only makes sense when it is levied on a bank. It is joke to levy a fine of that size on a $100k company.

LikeLike