Sitting in the sun, reading the Herald over lunch, I found my own name leaping out at me.

An Auckland immigration lawyer – I’m going to treat his argument on its merits, but do note the vested interest here – Alastair McClymont had an op-ed headed Beware ignorant debate on motivated migrants. I am apparently one of the “ignorant”.

Just who are the migrants supposedly stealing our houses and jobs? There have been plenty of knee-jerk reactions recently about the appropriate number of migrants that New Zealand can absorb each year. There has also been evidence of much ignorance on the subject.

In the 12 months to April, New Zealand received 68,000 net migrants (long-term arrivals minus long-term departures). New Zealand First leader Winston Peters has suggested the number be reduced to a maximum of 15,000 a year and as few as 7000.

Economist Michael Reddell has stated that cutting migration to 10,000 a year would lead to a reduction in house prices.

But the debate about migrant numbers is more complicated than Mr Peters or Mr Reddell would have us believe.

I am not speaking for Winston Peters, who I have never met or talked to. A fairly prominent person told me this morning that I had changed their way of looking at the New Zealand immigration debate over the last year or so, and noting that he had previously treated immigration as desirable partly because of a reaction against the way Winston Peters had raised the issues 20 years ago. I can certainly understand that.

But as for me, perhaps Mr McClymont could refer me to any suggestion I’ve ever made that migrants are “stealing our jobs and houses”. On the jobs front, I’ve been quite clear that I think the evidence is that immigration boosts demand more than supply in the short-term, and hence that increases in immigration at least temporarily lower unemployment. The Reserve Bank’s research, which I often quote, is consistent with the decades-long experience – implicit in all macro forecasting frameworks – in which, all else equal, interest rates typically rise here when immigration is unexpectedly strong. That is because of the considerable boost to demand – new immigrants need houses, road, schools, shops, just as long-term residents do. As for houses, well I don’t think anyone doubts that increased population pressure – whether immigrants (foreign or New Zealanders) or natural increase – increases the demand for housing, and that the new supply of housing is all too sluggish. So, yes, population shocks tend to boost house prices, and it often takes a long time for supply to catch up. That isn’t controversial stuff.

But apparently “the debate about migrant numbers is more complicated than [I] would have us believe”. I’ve written various lengthy papers and speeches on the issues over several years (for anyone interested, links are here), and have written dozens of posts here over the last 15 months on the issues. I quite agree it is a complex issue, and especially the connection to New Zealand’s long-term economic underperformance – something Mr McClymont does not even mention in his article. I’ve even taken the time to spell out what, specifically, I think should be done about changing our residency programme.

He goes on

Shamefully, Indian and Chinese migrants have too often borne the brunt of our community’s negative reactions to the high number of migrants, but total net migrants also include your German au-pair, the French or British waitress at your local cafe, the young, Aussie, seasonal worker at the ski field or your friend’s son returning home from work in London.

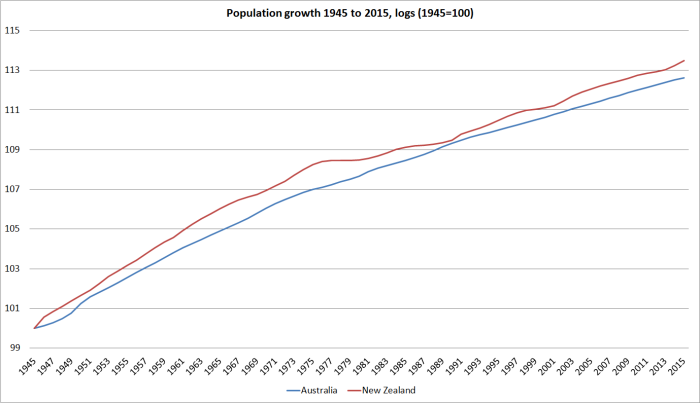

Well, yes. But where is the news? Go back and look at everything I’ve written on this topic, and you’ll find that I have been almost exclusively focused on the economics of the argument. I’ve been clear all along that all the economic arguments apply even if all the migrants were from Yorkshire and Sussex (as mine mostly were). In fact, in the post-war decades, the overwhelming bulk of our migrants were British – and since the new income-earning opportunities weren’t that good here, in fact that rapid population growth seems to have compromised our per capita income prospects. We’ve been in relative decline for 70 years.

Mr Clymont seems to want to suggest that I’m not even aware of the different classes of arrivals. So we are treated to a brief description of them – returning New Zealanders, working holiday schemes, foreign students, temporary work visas holders. But barely a mention of the residence approvals programme, with its explicit economic focus (the “critical economic enabler” as MBIE puts it). As McClymont will know, from having looked at what I have written, I have been focused on the residence programme, and have argued for substantially reducing the size of that programme (to something more like the US scale). Treasury themselves have had doubts about the working holiday schemes and the use of work visas in some relatively low-skilled areas. Others have raised concerns around the abuse of the foreign student process. Those mostly look like reasonable concerns, but they aren’t my focus. I’m focused on the residence approvals programme, which is what determines the long-term contribution of non-citizen immigration to our population growth. Perhaps Mr Clymont is focused on the headline PLT immigration numbers – I’m not, and never have been.

As I said, McClymont barely mentions the residence approvals programme, and doesn’t mention at all the 45000 to 50000 annual target – a target which is three times, per capita, the number of residence approvals the United States grants. Instead he falls back on debates around the short-term programmes.

The filling of low-skilled jobs by migrant workers is just a by product of the export education industry. The only low-skilled workers being imported fill jobs in the horticulture, dairy and health care industries.

But hold on, until a few years we didn’t allow foreign students generous work rights here – and actually had as many foreign students in the previous boom of the early 2000s as we do now. So it is a choice we make, not a necessary corollary. It isn’t really my issue – it isn’t something that really affects long-term economic performance – but it isn’t the choice I’d make if I were setting policy.

And his final sentence in that quote rather gives the game away. Those are each rather large industries. But again, my focus is on the residence approvals programme target, something McClymont doesn’t address directly at all.

By the end of the article, he is reduced to anecdote

I regularly speak with employers who are desperate to retain and recruit migrant employees. They all complain about the casual Kiwi attitude towards work and their constant “sick days”, particularly on Mondays.

By contrast, these employers find that migrants are more highly motivated to work and succeed at their jobs.

Many employers testify to the fact that 90 per cent or more job applications come from migrants, so why aren’t Kiwis applying for the jobs?

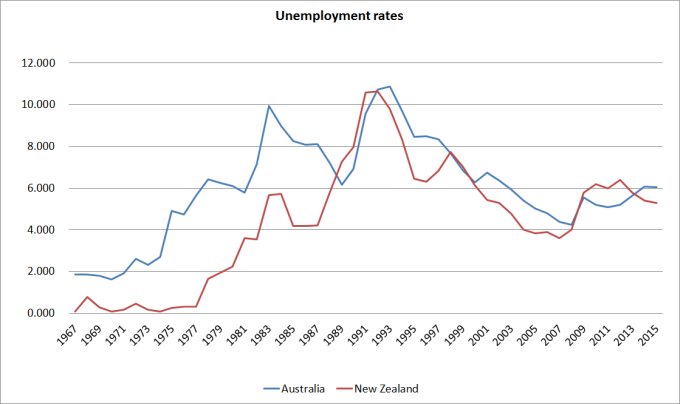

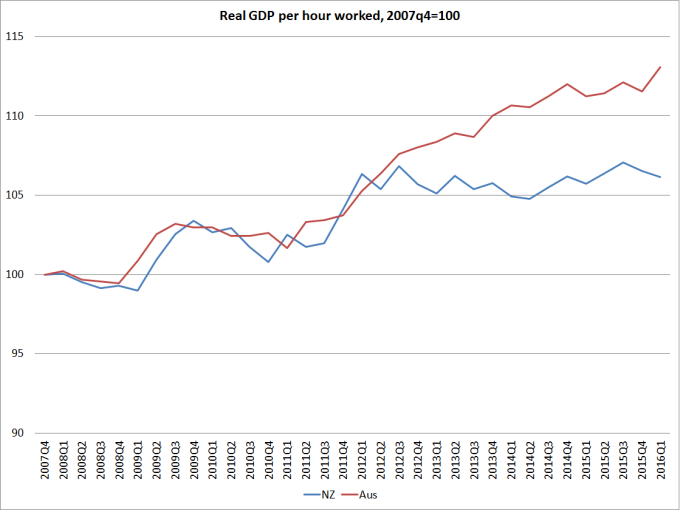

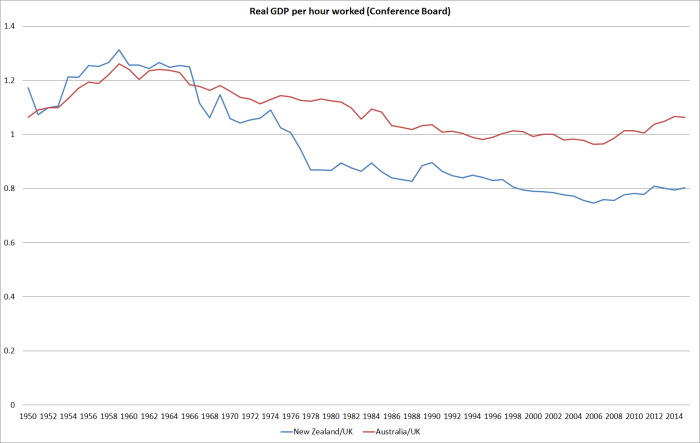

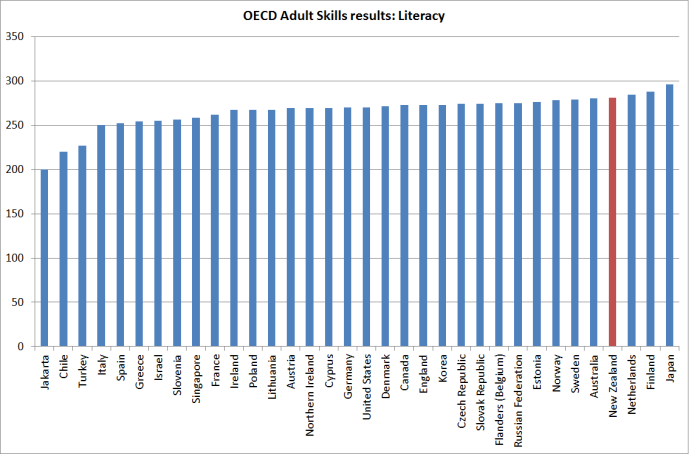

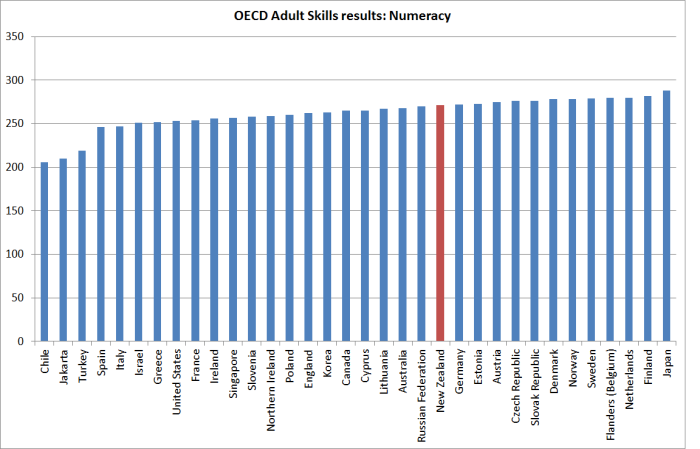

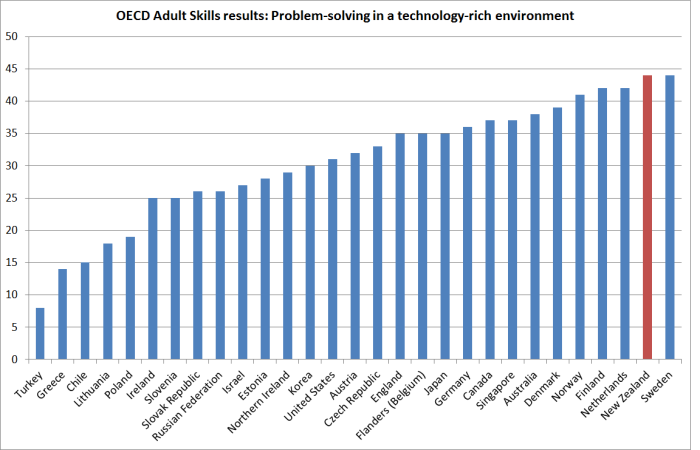

The condescending attitude to his own fellow citizens is pretty unnerving – lets trade in our people for another lot. But even then he seems unaware of the fact that New Zealanders work long hours per capita (longer than citizens of almost any other advanced country), and recently emerged on the OECD’s cross-country skills comparisons as having some of the best developed skills of people in any advanced countries. Could all of us do better? Well, quite possibly – even those of us not in the workforce. And is it any wonder that new arrivals are dead keen to establish themselves and get a foothold in a new country. But the point of the immigration policy is that it is supposed to boost the medium-term economic fortunes of New Zealanders as a whole – not just some individual employers. Somewhat surprisingly, no one has yet been able to produce serious evidence – or even sustained argument supported by reasonable data – that New Zealanders are materially better off as a result of the really large immigration programmes we have run for most of the last 70 years, and which we continue to run today. MBIE hasn’t, the Minister of Immigration hasn’t, Treasury hasn’t, the Prime Minister hasn’t. And Mr McClymont has not even really addressed the issue.

I argue that New Zealanders have probably been made worse off – our exports still rely almost entirely on natural resources, and yet the fruit of those natural resources is spread over ever more people. It would be interesting to know why Mr McClymont thinks such a remote place, underperforming for decades, would have one of the faster population growth rates anywhere in the advanced world. In fact, the “why” is simple: the answer is “policy”, but it doesn’t look like good policy, especially when New Zealanders themselves – who presumably know the opportunities here pretty well – keep leaving,

There are real and important debates to be had on the best immigration policy for New Zealand. I’ve argued that experience suggests a very distant country that has struggled to grow its export base isn’t a natural place for policymakers to try to drive up the population And I’ve repeatedly pointed to the troubling data around our:

- lagging productivity

- weak business investment

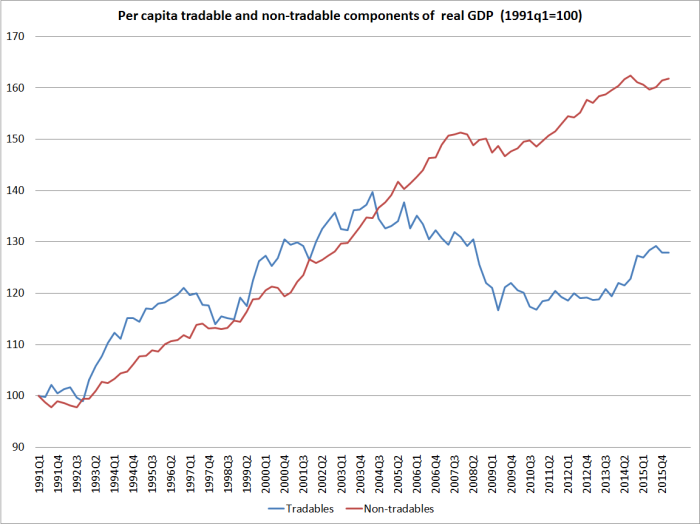

- weak tradables sector and export activity

- persistently high real exchange rates, and

- persistently high real interest rates (relative to those in other advanced countries)

and made a case that our immigration policy is part of what has held our economy back from being able to offer really high material living standards to our people. It isn’t a criticism of the immigrants, who are simply and rationally pursuing their best interests. If there is criticism to be levelled, it is at our own officials and ministers. But it is quite possible that my hypothesis is wrong. And there are also other – non-economic – motivations for immigration (humanitarian, through the refugee quota, or perhaps even a general sense that migrants will be better off even if we aren’t). Those are respectable arguments, and there are considered alternative perspectives to some of the points I’ve raised – few issues in economics are ever totally clear-cut. Lets have the debate – looking at the data, and the evidence, and trying to develop a compelling narrative of New Zealand’s economic performance, and immigration policy’s role (for good, ill, or not much difference) in it. But pretending that people raising questions about the programme are simply ignorant, and need it all explained to them once again, this time slowly and clearly, isn’t really likely to be very constructive.

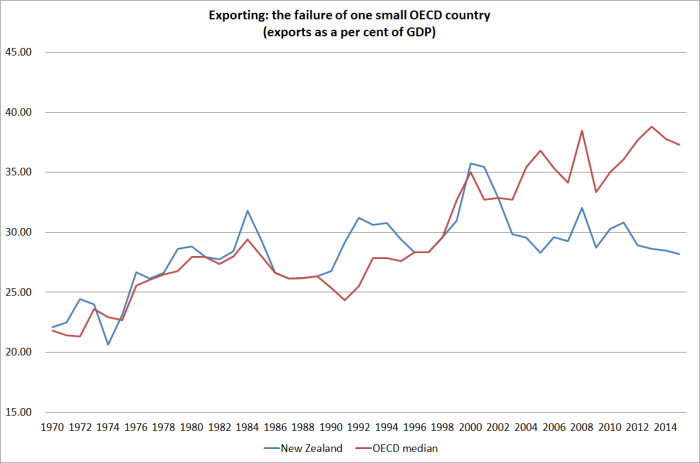

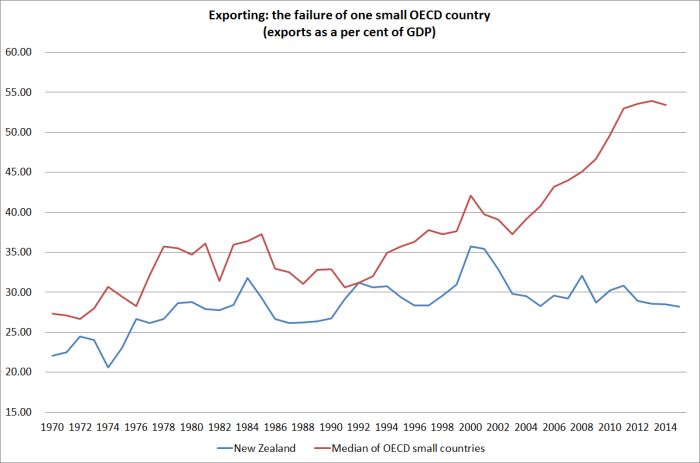

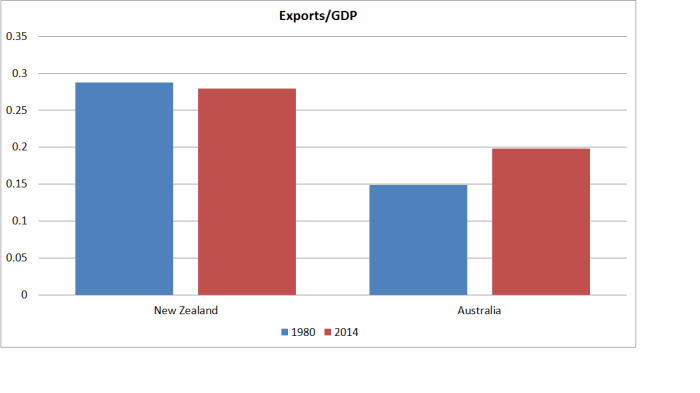

New Zealand’s export share of GDP hasn’t changed in 35 years.

New Zealand’s export share of GDP hasn’t changed in 35 years.