In the interview with Richard Harman I noted that one of my main interests and (rather more importantly) one of the bigger challenges for New Zealand was its disappointing economic performance over the last 25 years. The liberalisation of the economy in the 1980s and early 1990s was generally expected to have reversed the earlier decades of relative decline. Not everyone shared that optimism, but among the advocates of reform within government and the public service, and among most international observers (for example, the IMF and OECD, and financial markets), that sort of re-convergence was generally expected.

But it didn’t happen. For a while there was a “the cheque is in the mail” hypothesis doing the rounds – it hadn’t happened yet, but it surely wasn’t far away. But 25 years is a long time, and it just has not happened. Around 1990, the former eastern-bloc countries started serious liberalisation. Their economies had been much more heavily distorted than New Zealand’s (notwithstanding the Bob Jones crack in 1984 about the New Zealand economy resembling a Polish shipyard), but they have subsequently seen considerable convergence.

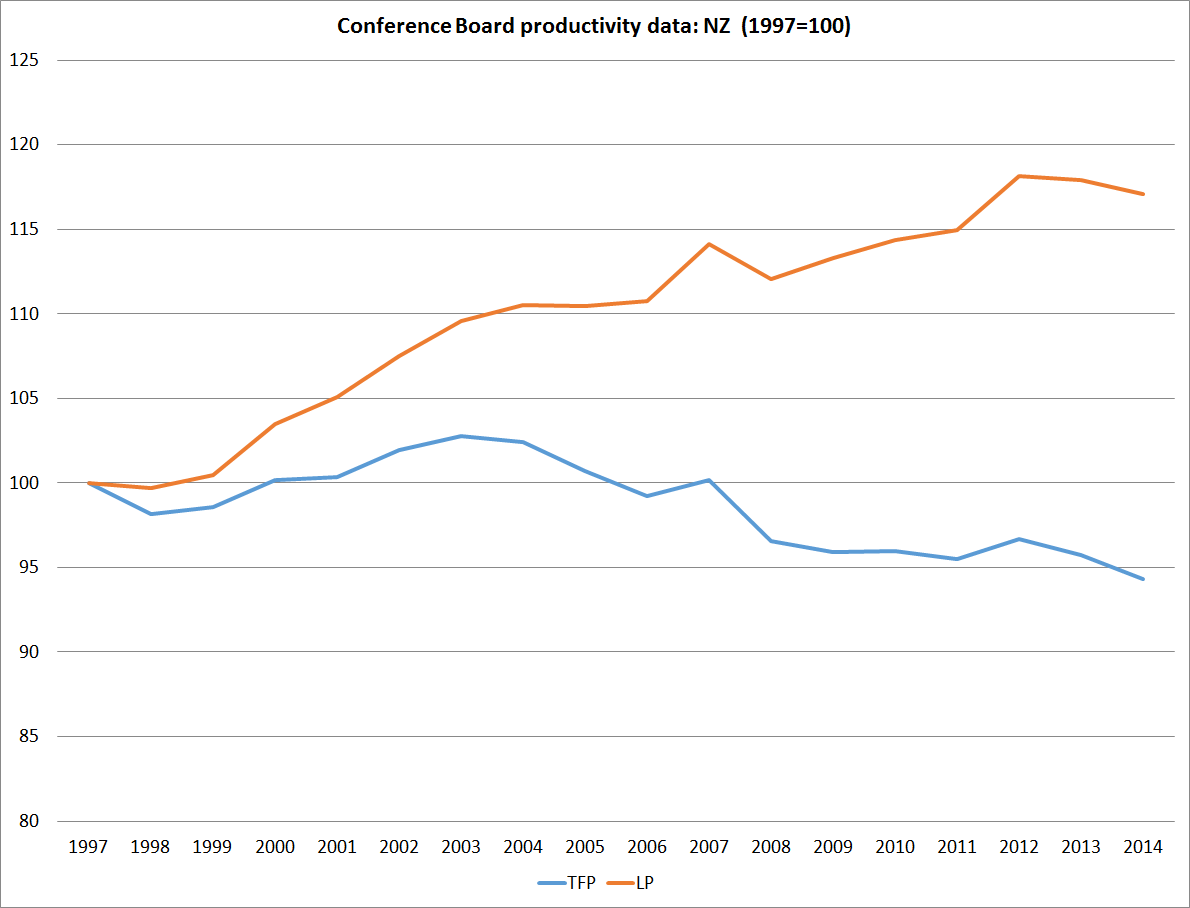

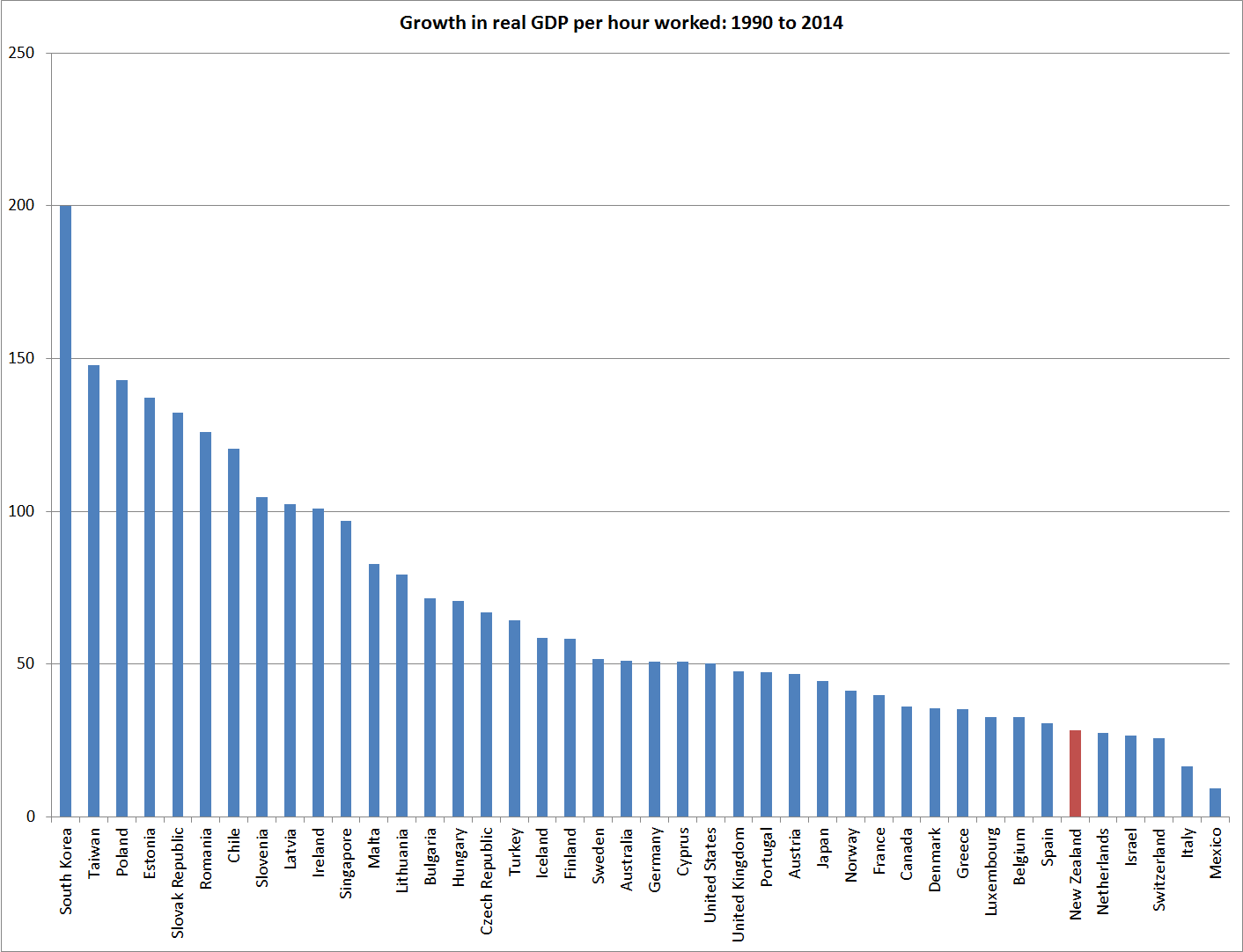

Here is my favourite summary chart of our underperformance over that period. Using the Conference Board data, it is total growth in real GDP per hour worked for 42 advanced countries (OECD, EU, and Singapore and Taiwan) since 1990. Only five countries had had slower growth over that period than New Zealand – and two of them (Switzerland and the Netherlands) had had among the highest levels of labour productivity in any of these countries in 1990 (so one might have expected unspectacular growth subsequently). No cross-country comparative measure is perfect, but I don’t this one is particularly unrepresentative of New Zealand’s relative performance On this measure, Greece and Portugal have done less badly than us (but recall that this is GDP per hour worked, and in the current Greek Depression total hours worked have dropped away precipitously).

I’ve been running a story about the role of immigration policy in explaining that failure to converge – total GDP has grown a lot, even if GDP per hour worked hasn’t. In this wider sample of countries, New Zealand has had among the faster rates of population growth, despite the huge outflow of New Zealanders (around 525,000) over that period. Singapore (86%) and Israel (77%) have had much faster rates of population growth than New Zealand (30%) over this period.

My argument has been that in a country with a low savings rate, rapid population growth has put considerable sustained upward pressure on real interest rates and the real exchange rate, squeezing the share of GDP devoted to business investment and preventing the emergence of new tradables sector firms/products at the rate that (a) convergence would have required, and (b) the rest of NZ’s microeconomic policy framework might have suggested/warranted. A few weeks ago, I showed how our real exchange rate against Australia had failed to decline despite the deterioration in our relative economic performance over decades.

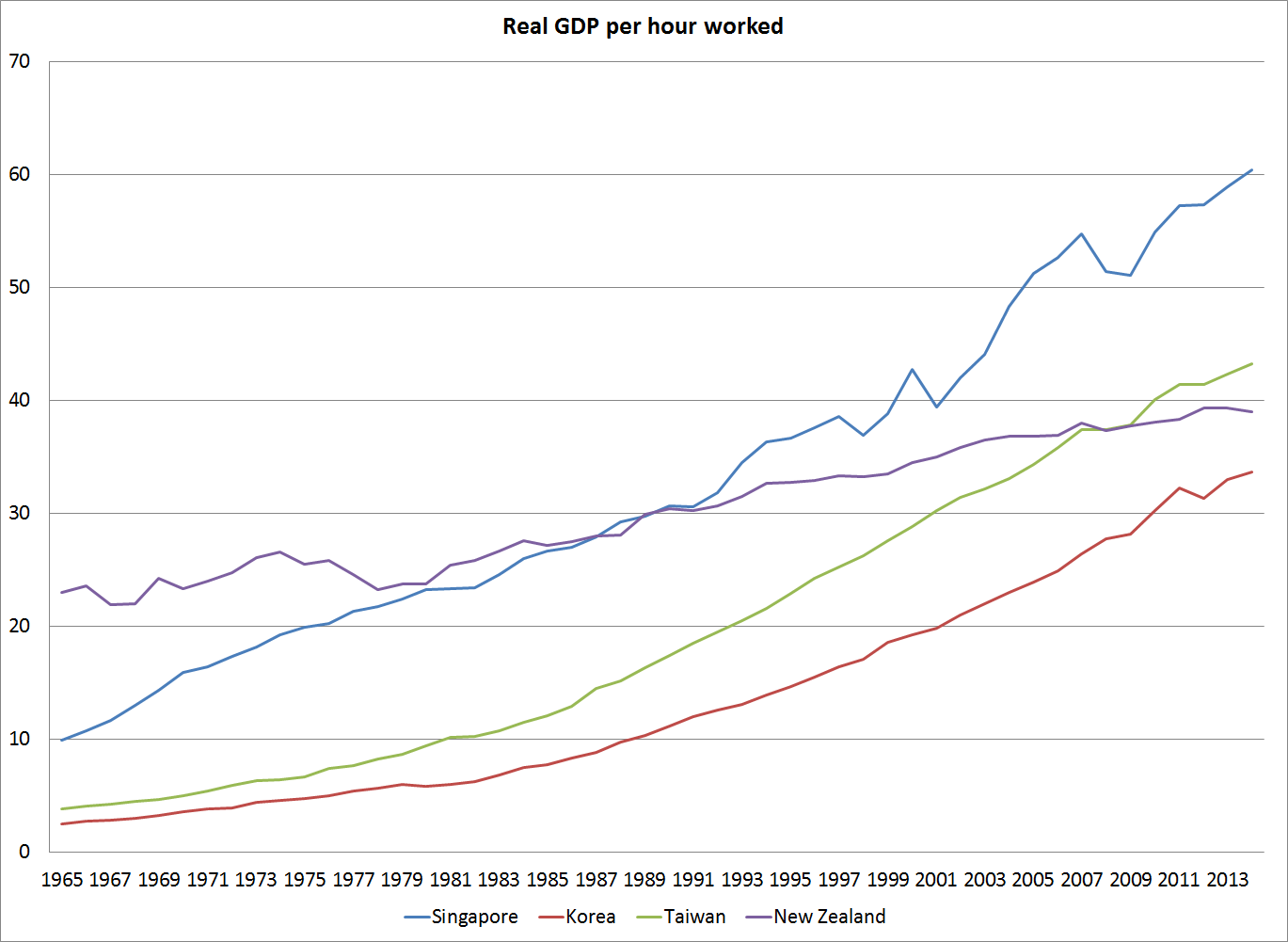

Here is another way of looking at the same point. The two countries with the fastest growth in the chart above were Taiwan and Korea. Singapore has also done impressively well. In 1990, Taiwan and Korea were well behind New Zealand, and Singapore had about the same level of real GDP per hour worked as New Zealand (precise comparisons depend on which set of relative prices are used, but on any measure all three countries have had growth outstripping that of New Zealand).

And here is the picture over 50 years, again using the Conference Board data

All three Asian countries have had some of the more dramatic catch-ups in productivity levels seen anywhere. New Zealand, by contrast, in 1965 was among the advanced countries with the highest levels of labour productivity, and has been in relative decline since.

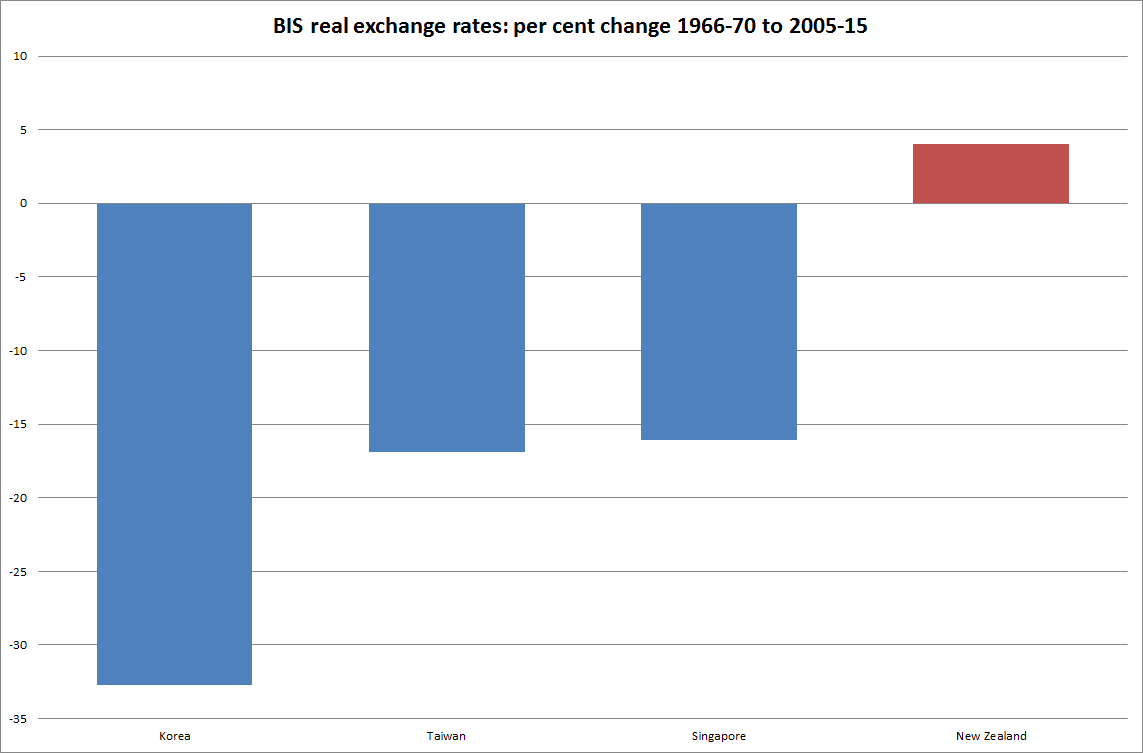

But what has happened to the countries’ real exchange rates since? As ever, there is no unambiguous way to measure that, but the BIS have real exchange rate indexes for each of the four countries going back to the 1960s. Of course, real exchange rates can move around a lot from year to year, so in this chart I’ve shown the percentage change in the real exchange rate from the average for 1966-70[1] to the average for the 10 years to May 2015.

The countries that have had such dramatic productivity improvements have all recorded modest falls in their real exchange rates, and by contrast New Zealand has had an increase in its real exchange rate. That is opposite of what one might initially have expected. One might have expected a strong real appreciation in the Asian currencies (as has happened in Japan), as much higher incomes supported more and cheaper consumption in these countries. Fewer resources now needed to be devoted to the tradables sectors in those countries. And in New Zealand one might have expected the deteriorating productivity performance, and hence declining (relative) future consumption opportunities, to have been met by a declining real exchange rate. That would have increased the returns to productive investment in New Zealand – helping to reverse the decline – and raised the relative price of consumption.

How does my story explain what went on?

In last 25 years, Korea and Taiwan have had materially slower population growth rates than New Zealand has, and much higher savings rates. That meant both less pressure on resources simply to maintain the capital stock per person, and more domestic resources available to meet investment demand. The net result: little upward pressure on real interest rates and the real exchange rate, despite the continuing productivity gains.

Singapore is at the extreme. The national savings rate has averaged 46 per cent in Singapore over the last 25 years, roughly double the rate for advanced countries as a whole. With so many resources available (earned but not consumed) even the investment needs of an average population growth rate of 2.5 per cent puts no pressure on domestic resources, or hence on real interest rates and the real exchange rate, despite the continuing productivity gains.

And that is my story in a nutshell: with very high saving rates your country might need lots more people to make the most of the savings. But in a country with only a rather modest savings rate (for whatever reason) then having lots more people – and especially bringing them in as a matter of policy – simply looks wrongheaded. It undermines what policy is setting out to achieve.

It isn’t that migrants somehow “take away jobs”, but rather that rapid population growth (whether migrants or high birth rates) tends to divert resources (jobs) away from growing the bits of the economy that sell to the rest of world (a huge and diverse market, and probably where our future prosperity is to be found) to ensuring that the physical infrastructure (houses, roads, shops, factories, schools) keeps pace with the needs of the growing population. It makes it very hard to catch up with the richer countries. Israel has found something much the same.

No comparison of any pairs of countries, in any particular period, is ever going to be conclusive. I use the examples in this post simply to illustrate the story.

[1] Starting the comparison from the start of the BIS series in 1964 would result in an even larger fall for Korea