Not infrequently over the last few years, I’ve criticised the Reserve Bank (and The Treasury and the Minister of Finance, both at least equally responsible) for the lack of any real sign that they were taking seriously the potentially severe limitations on the use of stabilisation policy (monetary policy in particular) in the next serious recession. The topic never featured in speeches from the Governor, there was no published research on related issues, and getting ready never featured as a priority in the Bank’s annual Statements of Intent.

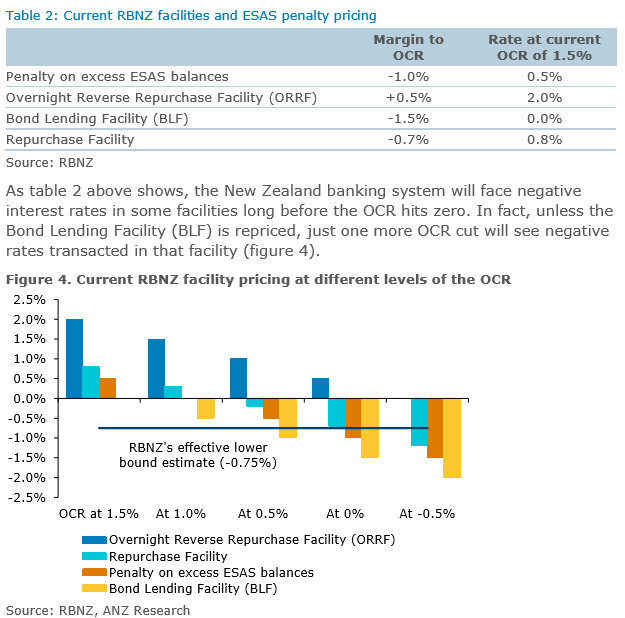

The potential problem, of course, is that – as things stand – the OCR can probably be lowered another couple of hundred basis points (to around -0.75 per cent) but for anything beyond that conventional monetary policy will quickly become quite ineffective, as large depositors (I’m thinking financial institutions and investment funds mostly) would exercise their option to switch into large holdings of (zero interest) physical cash. People will still use bank accounts (negative interest rates and all) for most day to day transactions, but most financial assets aren’t held for immediate transactions purposes.

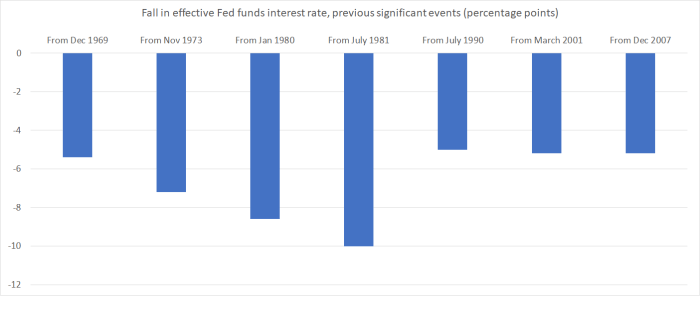

In typical past downturns OCR cuts of 500 basis points or more have been judged necesssary (the Reserve Bank cut by 575 basis points in 2008/09). Similar magnitudes of adjustment have been made in, for example, the United States.

It is now almost 10 years since the Reserve Bank first cut the OCR to 2.5 per cent. In the early years after that, the assumption was that (a) the 2008/09 recession had been unusually large, and (b) interest rates would soon need to be raised quite considerably, and so that whenever – perhaps a decade hence – the next recession happened New Zealand wasn’t likely to face a problem. That was then. As late as 2014 the then Governor was loudly talking up his plans to raise interest rates a lot, to – as he saw it – ‘normalise’ monetary policy.

But now it is 2018, and nominal interest rates are even lower than they were in 2008/09, and no serious observer thinks the Reserve Bank will have 500 basis points of policy leeway if another recession were to strike in the next few years (many doubt that the OCR will be raised much, if it all, in the intervening period, and a few – including me – think cuts would be more appropriate). Most likely, the New Zealand economy will go into the next recession – whenever it comes – with the OCR 50 basis points either side of the current 1.75 per cent. That just isn’t enough. And the problem will be (greatly) compounded by the fact that central banks in almost all other advanced countries will be in much the same situation of worse (several already have their policy interest rates at -0.75 per cent.

If your central bank can’t cut policy rates (very much), and markets and firms/households know it, any incipient recession is likely to be worse than otherwise, and worse than we are used to (when downturns happen, central banks cut policy rates, often quite aggressively (if also often a bit belatedly), and people know/expect it). Expectations of inflation may also drop away more sharply than we are used to, compounding the problems (real interest rates could raise, with nominal rates already on the floor). Monetary policy has been the key stabilisation tool for decades, and (at best) it will be hobbled in any recession in the next few years. For those who argue that interest rates don’t affect anything much domestically (a) I think you are wrong, but (b) the connection to the exchange rate is vital. In monetary policy easing cycles in New Zealand, we also typically see big exchange rate adjustments, and that is part of how the economy stabilises and the next recovery begins.

Which is all a fairly long introduction to welcoming a new issue of the Bulletin published a few weeks ago by the Reserve Bank under the heading Aspects of implementing unconventional monetary policy in New Zealand. As the introduction puts it

This article provides an overview of the experience with unconventional monetary policies since the global financial crisis of 2007/8, and assesses the scope for unconventional monetary policy in New Zealand. While there is no need to introduce unconventional monetary policies in New Zealand at this time, it is prudent to learn from other countries’ experiences and examine how such polices might work in New Zealand if the need arises.

It is, unambiguously, good to see such an article being published by the Bank. Unfortunately, there is a degree of complacency about the content – echoing remarks the Governor made at a recent press conference suggesting there was nothing to worry about – that should be quite disconcerting. Complacency on such matters might be expected from politicians, with a tendency to live from one news cycle to the next. We should not expect it from our central bankers.

As a brief survey of what other countries have done, the article is not bad. There is some discussion of the experience with negiative policy rates, which comes to the pretty standard conclusion that policy rates probably can not usefully be taken below about -0.75 per cent. There is a fairly long discussion of large scale asset purchases (mostly the government bond purchasing programmes) and some discussion of targeted term lending programmes operated in a few countries in the wake of the 2008/09 crisis.

Of large scale asset programmes, the Reserve Bank authors cautiously conclude

A large body of evidence shows that LSAPs were successful in easing financial conditions, through lower bond yields, higher asset prices and weaker exchange rates.11 The forward looking nature of financial markets means that most of the impact occurred on announcement, rather than when purchases were executed. As highlighted by Gagnon (2016), LSAPs can be especially powerful during times of financial stress, although the signalling and portfolio balance channels should still have a significant effect in normal times. There may, however, be diminishing returns through these channels. In particular, given the lower bound on short-term interest rates, there will be a limit to how far interest rates can be reduced via the signalling channel. Similarly, there is likely to be a lower bound on long-term interest rates (as investors have the option of holding paper currency with a fixed yield of zero) meaning additional purchases might not drive yields much below zero.

What really matters for central banks is whether LSAPs helped central banks achieve their mandates, related to achieving inflation, output and employment goals. While most studies into the effect of LSAPs in the post 2007/8 global financial crisis period find positive effects, they must be treated with caution. In part this is because of measurement issues: LSAPs have been implemented over a relatively short period since the 2007/8 global financial crisis, and previous historical relationships can have been expected to have changed. Overall, early work suggests LSAPs can be a beneficial monetary policy tool in exceptional circumstances. However the nature and extent of the transmission of these polices to inflation and activity is still being established.

Cautious as that is, I suspect it is not cautious enough. For example, if one takes a cross-country approach there is little sign that long-term interest rates have fallen further relative to short-term interest rates in countries that did large scale asset purchases than in those which did not (for example, New Zealand and Australia). Whatever the headline or announcement effects – and some probably real effects in the midst of the crisis itself – without those longer-term effect on real bond rates, it is difficult to believe that the asset purchase programmes really made much difference to stabilisation and recovery.

Relatedly, as the authors note, the real test is surely progress towards meeting inflation targets and getting unemployment rates back down again quickly. Against that standard, with the best unconventional tools central banks could deploy, on top of large reductions in policy rates, the experience has been very troubling – the weakest recovery in many decades. With that set of tools, the outlook the next time a serious recession hits has to be, almost by construction, worse than over the last decade.

But in many respects, the most interesting part of the article is the second half, exploring options for New Zealand. Unfortunately, they do not seem to have moved very far at all from past work. Just based on things I personally was involved in, in the late stages of the last recession I spent quite a bit of time at Treasury looking at options that might be deployed in things worsened further, and when the euro crisis was at its height in 2012 I led a Reserve Bank working group looking at some of the issues around how far we could go with conventional monetary policy, and what other instruments were then at our disposal. The sorts of options we looked at then were helpful (and even then we reckoned the OCR could be cut to perhaps -0.75 per cent) but pretty limited. The Bank seems no further ahead now and – disconcertingly – seems unbothered by that situation.

What tools do they have in mind?

The first is a negative OCR.

Overall, it appears that the Reserve Bank could implement negative interest rates, with the potential leakage into cash relatively small in value terms at modestly negative rates.

That seems right to me. It would not be expected to involve, say, negative mortgage interest rates, but there have been some examples even of those in Scandinavia.

But it is the limits to the negative OCR which are the issue.

The second possible instrument they cover in the option of large-scale asset purchases.

As they note, there are not many (liquid) bond issues in New Zealand other than government bonds, and even the stock of government bonds is (generally fortunately) smaller than in many other advanced countries (including the US, UK, Japan and the more troubled parts of the euro-area). And many passive holders of government bonds – having made long-term asset allocation choices – will not be that interested in selling.

In a New Zealand specific severe recession, these constraints might not matter very much. Many of our government bonds are held by foreign investment funds, who have no natural (benchmark) reason to be in New Zealand. Shake them loose by offering a high enough price and not only might bond yields fall quite a bit – at least initially – but the exchange rate could be expected to fall too. That latter channel would probably be much the most important one (since few New Zealand borrowers issue long-term debt, and those that do will typically swap it back into a floating rate exposure).

But if the downturn is pretty synchronised across a range of countries (as it was in 2008/09), that is a less compelling story. Everyone will be trying to cut policy rates, and pretty everyone will be coming up against practical lower bounds. Everyone can try to depreciate their currency, but in aggregate that ends up with not much expected change. I’ve argued previously that if our OCR is ever around that of other advanced countries, our exchange rate should fall quite a lot, but at present the margins between our OCR and those of other countries is already smaller than we often find going into past recessions.

The Reserve Bank authors also note that the Bank could engage in (unlimited) unsterilised exchange rate intervention, buying assets in other countries’ currencies, and selling (‘printing’) New Zealand dollars, which the Bank can do without technical limit. All else equal, that should tend to lower the exchange rate.

This might be more of an option for a small and inobtrusive country like New Zealand – among the majors ‘currency war’ rhetoric would soon be flying. But even then, it isn’t likely to be a terribly effective policy. The Reserve Bank notes some of the reasons (other countries trying to do the same thing – eg Australia our largest trade/investment partner). But the other reason involves thinking about transmissions mechanisms: printing lots more New Zealand dollars creates more interest-bearing assets in New Zealand. In normal circumstances, unsterilised intervention will drive down domestic interests rates, setting in train a mechanism that will lower the exchange rate, raise inflation etc etc. But in this scenario, by construction, short-term interest rates can’t fall any further. And there is no compelling reason to suppose that the holders of those new New Zealand dollars will want to spend more on goods and services (a channel which really might raise inflation).

The Reserve Bank briefly discusses the option of transacting the derivatives market, via interest rate swaps (larger and more liquid than the bond market). This idea has been around for years. There is no doubt it would enable the Reserve Bank to, say, cap the long-term (synthetic) interest rate, but it isn’t clear what good that would do, and there is no sign in the article of any new thinking in that regard. The Bank talks of signalling gains – communicating a commitment to keep the OCR low for a long period – but I doubt that does much good beyond the short-term announcement effect. For one, central banks can’t pre-commit, and markets and other observers will make their own judgements based on their read of the emerging economic data.

The final option they discuss is targeted term lending. What they have mind here isn’t replacing market credit when funding markets seize up (as happened in 2008/09) but direct intervention in which the government and the Reserve Bank try to target credit to particular sectors.

This type of facility would provide collateralised term lending to banks at a subsidised rate if banks met specified lending objectives. These criteria would ensure that the low policy rate was being passed on to households and businesses. Holding collateral against the loans would mitigate the risks to the Reserve Bank’s balance sheet. Since a targeted lending scheme could see banks taking on more credit risk than they might otherwise choose, it would need to be carefully managed.

That final sentence is an understatement to say the very least. Policies of this sort are really fiscal policy and, if done at all (which they should not be) should be done by the government itself, not the autonomous central bank. Government involvement in encouraging credit provision to particular sectors has a poor track record, here or abroad (see US crisis ca 2008/09). And when the Reserve Bank takes collateral to try to encourage/coerce banks into providing credit they would not otherwise provide, it is directly preferencing itself relative to other creditors (including depositors) if things later go wrong.

In an article about monetary policy, it is not surprising that the Bank gives little space to discretionary fiscal policy. But it is disconcerting that when they do touch on it, they get their basic facts wrong.

And in New Zealand, fiscal policy played an important role in the response to the 2007/08 global financial crisis.

Discretionary fiscal policy played no role at all in responding to the recession of 2008/09 (if anything, it was marginally contractionary given the cancellation of promised tax cuts in 2009). Yes, the overal fiscal position slid into deficit but that was wholly because of (a) policy choices made before the government or Treasury realised there was a recession, and (b) automatic stabilisers, which are weaker in New Zealand than in most advanced countries.

As I said earlier on, the degree of complacency – and refusal to confront options that really could make a significant difference – is disconcerting. The Bank argues

The Reserve Bank would look to communicate well in advance of any of unconventional policies being implemented, so as to enable financial markets and the government to prepare.

A nice sentiment, but as they note a few sentences later

we are rarely given the luxury of time when financial crises [or other recessions] hit

including because central banks are usually slow to recognise what is happening. When you only have 200 basis points of conventional policy leeway – and everyone knows that (a point not touched on in the article at all) – they will need to be willing to signal a credible strategy very early. And, on the evidence of this article, they do not have one (that would be likely to make any very material difference).

I suspect the authors really know that too, but prefer not (or are institutionally prevented from) saying so. After all, they each smart people, and they know how poorly the world economy coped with, and recovered from, the last downturn, even deploying all sorts of unconventional policies (fiscal and monetary) on top of the considerable conventional monetary policy leeway that existed going into that recession. Even here – where we never reached the limits of conventional policy – the output gap remained negative, and the unemployment rate above official estimates of the NAIRU for eight or nine years. Eight or nine years…….. That is just a huge amount of lost capacity, and of lives that are permanently blighted (prolonged involuntary spells of unemployment do that to people).

Perhaps the implicit argument is that we, and other countries, will do even more next time round. But that isn’t likely. Perhaps fiscal policy is, or should be, an option, at least in modestly-indebted countries like New Zealand, but any sober observer will recognise the real world political constraints other countries faced in using active fiscal policy to any great extent, for long, in the last recession. Why is New Zealand likely to be different?

For much of the last decade, one has had the feeling – in gubernatorial speeches and other commentary – that, when it comes to it, the Reserve Bank really isn’t that bothered by lingering unemployment, excess capacity, or undershooting inflation. One would like to think – given his new mandate – that the new Governor is different. But this article isn’t really evidence for the defence on that score.

It is striking that the article does not engage at all with either of the two more radical options debated in other places and other countries:

- reconfiguring the target for monetary policy. This could take the form of a higher inflation target or, for example, the use of a price level or nominal GDP level target. Each approach has its weaknesses, but either – done in advance of the next serious downturn, not in midst when much of the opportunity is lost – could help raise, and hold up, expectations about the path of the nominal economy, including inflation.

- taking steps to material reduce the extent of the effective lower bound on nominal interest rates.

The latter remains my preference, for a number of reasons (including that the existing problem arises largely because central banks have – by law – monopolised note issue, and then not proved responsive to changing circumstances and technologies. Problems are usually best fixed at source.

If there is still a useful role for physical currency (I discussed some of these issues here), the ability to convert huge amounts of financial assets into physical currency, on demand, without pushing the price against you, is now a material obstacle to monetary policy doing its job in the next recession. There is a good case for looking seriously at a variety of reform options, such as:

- phasing out large denomination Reserve Bank notes (while perhaps again allowing private banks to offer them, on their own terms, conditions and technologies),

- capping the physical Reserve Bank note issue, scaled to growth in, say, nominal GDP (perhaps with provision for overrides in the case of financial crisis runs),

- putting a spread (between buy and sell prices) on Reserve Bank dealing in bank notes, or

- auctioning a fixed quota of bank notes, and thus allowing the price to adjust semi-automatically (when currency demand rises, as when the OCR goes materially negative) the cost of conversion rises.

These sorts of ideas are not new. They do not get rid of the entire issue – at an OCR of, say, -10 per cent, even transaction demand for bank deposits might dry up – but they would go an awfully long way to ensuring that the next recession can be dealt with more effectively than the last.

If, for example, you thought the OCR was going to be set at -3 per cent for two years, then once storage and insurance costs are taken into account (the things that allow the OCR to be cut to around -0.75 per cent now), even a lump sum conversion cost (deposits into physical cash) of 5 per cent would be enough to keep almost everyone in deposits and bonds (even at negative yields) rather than physical cash. That is a great deal leeway than the Reserve Bank has now. Having that leeway – and being willing to use it – helps ensure nominal rates don’t need to stay extremely low for too long.

In principle, many of these sorts of initiatives probably could be done in short order in the midst of the next serious downturn. But we shouldn’t have to count on unknown crisis responses, the tenor of which have not been consulted on, socialised, and tested in advance. It may even be that some legislative amendments might be required.

In summary, I welcome the fact that the Reserve Bank has begun to talk more openly about the potential limitations in its response to the next recession, but it is disconcerting that they still seem to be trying to minimise the potential severity of the issue. In that, they aren’t alone. I’m not aware of any central bank that has yet laid out credible plans to minimise the damage (although senior officials of the Federal Reserve have been more willing to talk about the issues openly). In that, they are doing the public a serious dis-service, and risking worse outcomes than we need to face – repeating the sort of reluctance to address issues that saw the world drift into crisis in the early 1930s. Fortunately for the central bankers perhaps, it won’t be central bankers personally who pay the price. That won’t be much consolation for the many ordinary people who do.

Since politicians, and not central bankers, are accountable to the voters, the Minister of Finance should be taking the lead in requiring a more pro-active (and open) set of preparations to be undertaken by the Reserve Bank and The Treasury.

UPDATE (6 July): I have only just discovered that one of the authors of this article, whom I had known – although not been close to – for 35 years, had died shortly before publication. Rereading this post, I don’t particularly resile from any of the content, but had I known I’d have written differently.