I wrote about the new – and last ever – Policy Targets Agreement when it was released by the incoming Governor and the Minister of Finance last week. Mostly the changes were pretty small, and in some cases you had to wonder why they bothered (since the PTA system itself is to be scrapped when the planned amendments to the Reserve Bank Act are passsed later this year).

I lodged Official Information Act requests with the Reserve Bank and Treasury for background papers relevant to the new PTA. I wasn’t very optimistic about what I might get from the Reserve Bank – both because of a culture of secrecy, and because the incoming Governor probably wasn’t covered by the Official Information Act when he was negotiating this major instrument of public policy. But The Treasury kindly pointed out that they had already pro-actively (if not very visibly) released several papers, including Treasury’s own advice to the Minister of Finance, and two Cabinet papers.

(I would link to those papers, but Treasury has been upgrading its website this week and the link they provided me with no longer works. If I manage to trace one that does work I will update this.) [UPDATE 9/4. Here is the new link to those papers,]

Those papers help answer the question about why they bothered with the small changes. The Treasury advice to the Minister of Finance was dated 7 February, well before Treasury had formulated its advice on Stage 1 of the Reserve Bank Act review, and before the Independent Expert Advisory Panel had reported. In other words, well before it was decided that PTAs would soon be done away with altogether. Indeed, there are suggestions in the paper that most of the relevant work had been done 18 months ago – they say they consulted “a number of economists and market participants over 2016” – when they thought the Minister would be replacing Graeme Wheeler early last year (rather than falling back on the unlawful “acting Governor” route to deal with the election period). Interestingly, the advice suggests Treasury favoured, on balance, increasing the focus on the 2 per cent target midpoint and de-emphasising the 1 to 3 per cent target range, but the Minister appears to have rejected that option.

There are two Cabinet papers among the material that was released. One was from 19 February, before the Minister had engaged with the Governor-designate on the possible wording of the PTA. In that short document the Minister outlines for his colleagues the draft PTA he would be suggesting to Adrian Orr. The other was from 19 March, advising his colleagues of the text he had agreed with Orr.

The differences in the two texts are small, but in my view the changes represent improvements relative to the Minister’s draft (for example, keeping the political waffle about climate change, inclusive economies etc, clear of the material dealing with the Reserve Bank’s own responsibilities). Presumably Orr would have consulted senior Reserve Bank staff, but on the basis of what has been released so far, we don’t know.

The documents suggest that The Treasury has played the lead (official) role in reshaping the Policy Targets Agreement (the Treasury advice to the Minister refers to them having consulted the Bank, but there is no suggestion that the Bank staff had necessarily agreed with the recommendations, or any suggestion of a separate Reserve Bank paper). In a way, the lead role for The Treasury makes sense – macroeconomic policy parameters should be set primarily by the Minister, not the Governor-designate. On the other hand, The Treasury will typically not have the degree of expertise, or depth, in issues around monetary policy that the Reserve Bank should have. I welcome the Minister’s announcement that in future, when the Minister directly sets the operational goal for monetary policy, he will be required to do so after having regard to the advice (publicly disclosed) of both the Reserve Bank and The Treasury.

My main prompt for this post, however, was one element of The Treasury advice which seriously concerned me, and represented a grossly inadequate treatment of an important issue.

In Treasury’s advice to the Minister, they have an appendix dealing with a couple of aspects of the Policy Targets Agreement where they didn’t propose change. The one I’m interested in was the question of the level of the inflation target itself.

Treasury note that “there have been a number of arguments advanced by commentators over recent years in favour of either a higher or lower inflation target”.

Treasury notes, correctly, that

The main argument in favour of increasing inflation targets is in order to ensure that central banks will have enough scope to lower interest rates in the face of a large contractionary economic shock that may result in monetary policy reaching the effective lower bound of [nominal] interest rates

Amazingly, this issue is dismissed in a mere two sentences. As they note

a higher inflation target would lead to higher costs of inflation at all times, whereas the risks of a lower bound event occur infrequently

But instead of moving on to offer some numerical analysis, or even plausible scenarios, the government’s principal economic advisers simply observe that

Given this, the costs of a higher inflation target may outweigh the benefits

Or may not. But Treasury doesn’t seem to know, and doesn’t offer the Minister (or us) any substantive analysis.

Here is one scenario. Recessions seem to come round about once a decade, and in typical recessions (admittedly a small sample) the Reserve Bank has needed to cut interest rates by around 500 basis points. If it can only cut interest rates by, say, 250 basis points, and that difference meant even just 2 per cent additional lost output (eg the unemployment rate one percentage point higher than otherwise for two years, the annual costs of a higher – but still low – inflation rate would have to be quite large, for the costs of a higher target to outweigh the benefits. Perhaps my scenario is wrong, but Treasury doesn’t offer one at all.

Treasury devotes more space to the possibility of lowering the inflation target. They aren’t keen on that – some of their arguments are fine, others flawed at best – but even then they seem determined to play down the near-zero effective lower bound on nominal interest rates, noting that (emphasis added)

a lower inflation target marginally increases the risk that the ELB [effective lower bound] may be reached, thereby providing monetary policy marginally less space to respond to shocks

Those who have sometimes called for cutting the target probably have in mind cutting the target midpoint from 2 per cent to 1 per cent (where it was in the early days of inflation targeting). When interest rates are 8 per cent, that might make only a marginal difference to the chances of the lower bound being reached – indeed, that was standard Reserve Bank advice in years gone by, when the lower bound was treated as a curiosity of little or no relevance to New Zealand. But when the OCR is at 1.75 per cent (and the central bank thinks the output gap and unemployment gaps are near zero) a 1 percentage point cut in the inflation target would hugely reduce the effective monetary policy space for dealing with serious adverse shocks. The floor would be hit with relatively minor adverse shocks.

And they conclude this way

New Zealand’s inflation target has been changed a number of times in the past and frequent changes to the level of the target could undermine the credibility of the regime.

There were two changes in the level of the target inside six years, which was unfortunate. But the most recent of those changes was 16 years ago. At that time, the idea of running out of monetary policy room in New Zealand was little more than a theoretical possibility. Now it seems quite likely whenever the next recession happens here, and has already happened to numerous other advanced countries.

As I hope readers recognise by now, I regard an increase in the inflation target as an undesirable outcome, a second-best option. I would rather the authorities (Reserve Bank, Treasury, and the Minister of Finance) treated as a matter of urgency removing directly – and with preannounced certainty and credibility – the extent to which the near-zero lower bound on nominal interest rates bites, by reducing or removing the incentives in the face of negative interest rates for people (large holders of financial assets, rather than transactions balances) to shift to holding physical cash. Even just ensuring that the Reserve Bank gets inflation up to around 2 per cent – rather than the 1.4 per cent (core) inflation has averaged for the last five years – would help.

But there is nothing about any of this in The Treasury’s advice on the main instrument of New Zealand macroeconomic policy. It seems extraordinarily inadequate. Perhaps they have provided some other, more in-depth, advice on these sorts of issues – in which case it might be good to proactively release that – but there is no hint of, or allusion to, any deeper thinking in the PTA advice. “Wellbeing” is all the (content-lite) rage at The Treasury these days. I’m not a fan, but perhaps they should reflect that one of the biggest things policymakers can do to avoid adverse hits to “wellbeing” is to avoid unnecessarily severe or protracted recessions (and spells of unemployment). Indifference on this score is all the more inexcusable when the limitations arise wholly and solely from policymaker/legislator choices – whether around the level of the inflation target or the system of physical currency issues (and the prohibitions on innovation in that sector). Ordinary New Zealanders – not Treasury officials – risk having to live with the consequences of their malign apparent indifference.

As it happens, a reader last night sent me a link to a couple of new pieces on exactly these sorts of issues. The first was the (brilliantly-titled) “Crisis, Rinse, Repeat” column by Berkeley economist and economic historian Brad Delong. He concludes

It has now been 11 years since the start of the last crisis, and it is only a matter of time before we experience another one – as has been the rule for modern capitalist economies since at least 1825. When that happens, will we have the monetary- and fiscal-policy space to address it in such a way as to prevent long-term output shortfalls? The current political environment does not inspire much hope.

And his column took me on to recent work by his colleagues David and Christina Romer, and in particular to a recently-published lecture on macroeconomic policy and the aftermath of financial crises.

The authors focus on financial crises (and I have a few questions about which events are included and which are not), rather than recessions more generally, but it isn’t obvious to me why their results wouldn’t generalise. Here is their abstract.

Analysis based on a new measure of financial distress for 24 advanced economies in the postwar period shows substantial variation in the aftermath of financial crises. This paper examines the role that macroeconomic policy plays in explaining this variation. We find that the degree of monetary and fiscal policy space prior to financial distress—that is, whether the policy interest rate is above the zero lower bound and whether the debt-to-GDP ratio is relatively low—greatly affects the aftermath of crises. The decline in output following a crisis is less than 1% when a country possesses both types of policy space, but almost 10% when it has neither. The difference is highly statistically significant and robust to the measures of policy space and the sample. We also consider the mechanisms by which policy space matters. We find that monetary and fiscal policy are used more aggressively when policy space is ample. Financial distress itself is also less persistent when there is policy space. The findings may have implications for policy during both normal times and periods of acute financial distress.

These are really huge differences. And they reflect a combination (a) a substantive lack of capacity, and (b) a reluctance to use aggressively what capacity still exists when the bottom of the barrel is getting close.

Here is the chart they use for monetary policy space (and lack thereof).

(the dotted lines are confidence bands)

The Romers offer some thoughts on the policy implications, including

Very low inflation means that nominal interest rates tend to be low, so monetary policy space is inherently limited. A somewhat higher target rate of inflation might actually be the more prudent course of action if policymakers want to be able to reduce interest rates when needed.

Our finding that policy space matters substantially through the degree to which policy is used during crises also implies difficult decisions. For example, it is not enough to have ample fiscal space at the start of a crisis. For the space to be useful in combating the crisis, policymakers have to actually enact aggressive fiscal expansion. However, countercyclical fiscal policy has become so politically controversial that policymakers might refuse to use it the next time a country faces a crisis.

What of New Zealand (included in their empirical sample)? We have plenty of “fiscal space” – both gross and net debt are pretty low (around the lower quartile of OECD countries). In a technical sense that might substitute to some extent for a lack of monetary policy capacity (if a recession hit today, we start with an OCR at 1.75 per cent, while most countries were at 5 per cent or more going into the last recession). But fiscal deficits blow out quite quickly in recessions anyway – as the automatic stabilisers do their work – and can anyone honestly assure New Zealanders that governments would be willing to engage in much larger than usual, more sustained than usual, active fiscal stimulus if a new and serious recession hits at some stage? Of course they can’t. Politicians can’t precommit (and even Treasury can’t precommit what its advice would be) and the political constraints on a willingness to actively choose to take on large deficits far into the future – perhaps on projects of questionable merit – would almost certainly be quite real (as they were in so many countries after 2008). So we are better placed than some because of the fiscal capacity – itself less than it was here in 2008 – but we really should be taking steps to re-establish effective monetary policy capacity. That might involve (my preference) dealing directly with the lower bound, it might involve changing the inflation target, it might involve putting more pressure on the Bank to get inflation up to 2 per cent, or it might even involve asking questions about whether inflation targeting (as distinct from levels targeting) offers more crisis resilience (senior US monetary policymakers have openly been discussing some of those latter issues).

There is no sign, for now, that The Treasury is taking the issue at all seriously, and there has been no sign – in speeches, or Statements of Intent – that the Reserve Bank has been doing so. That needs to change. Perhaps it is a good opportunity for the new Governor. But the Minister – rightly focused on employment issues – should really be taking the lead, and insisting on getting better quality analysis and advice, engaging with the real risks and offering practical solutions, than what was on offer when the PTA was being reviewed.

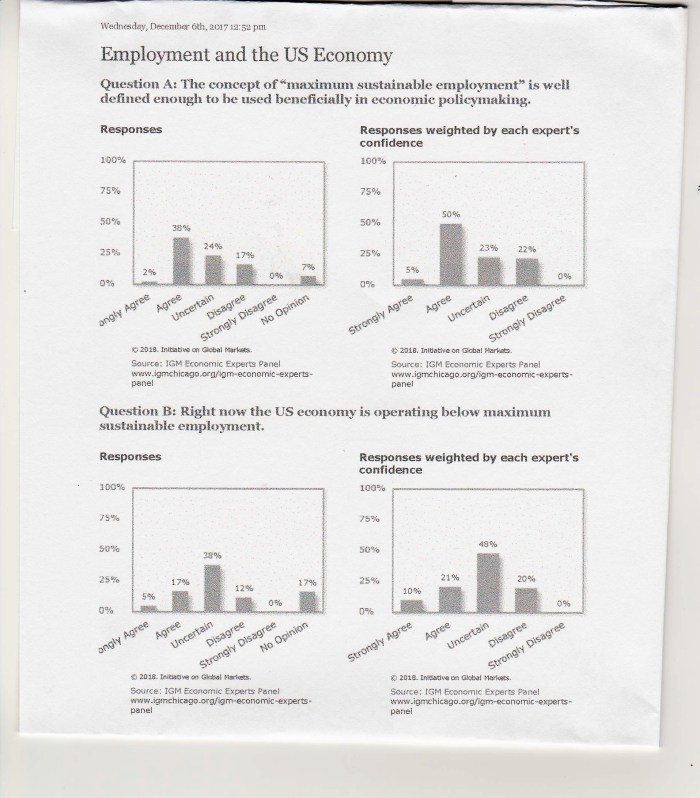

Weighted by the respondents’ individual levels of confidence, 55 per cent thought “maximum sustainable employment” was well enough defined to be used beneficially in policymaking. 22 per cent disagreed, and the remainder were uncertain.

Weighted by the respondents’ individual levels of confidence, 55 per cent thought “maximum sustainable employment” was well enough defined to be used beneficially in policymaking. 22 per cent disagreed, and the remainder were uncertain.