Tomorrow Graeme Wheeler will announce his second-to-last OCR decision. Assuming, as everyone seems to expect, that the Governor largely restates the policy stance he adopted six weeks ago, I expect to agree with him. Within the huge, and inevitable, bounds of uncertainty, the current OCR seems plausibly consistent with core inflation getting back to around 2 per cent, and there is no strong impetus that should be pushing the Reserve Bank to either raise or lower the OCR any time soon.

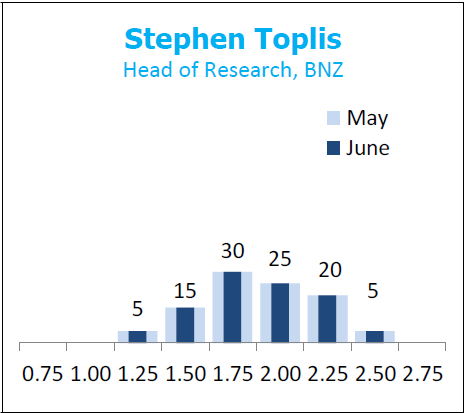

If anything, one could probably more readily argue for another cut, rather than any increase, just because core inflation has remained so low for so long and it has proved harder to get it back up than most had expected. The unemployment rate – an indicator that the Labour Party is rightly calling for the Bank to give more weight to – points in the same direction. In that respect, I disagree with the collective view of the NZIER’s Shadow Board, who have a clear upward bias. As an aside, it is interesting to note that the BNZ’s chief economist, Stephen Toplis, shares the upside bias, but is the only one of the panel to put a substantial weight on the possibility that further cuts might prove, as things stand, to be appropriate. Here is the probability distribution (percentages) of his recommendations.

But in this post, I really wanted to focus on some longer-term issues where I think there is rather more serious reason to doubt that the Governor is adequately discharging the responsibilities of his office and reason to worry that, in fact, some of his duties have been neglected. And these aren’t just issues about economic forecasting, something that no one is very good at, and where anyone who pretends otherwise is a fool.

My concern is the next recession. No one knows when it will be, but it has been seven or eight years since the last one ended. People will chip in to point out that there is nothing inevitable about another recession just because a few years have passed since the last one, and no doubt that is true. Nonetheless, downturns and recessions do happen, and discretionary monetary policy exists mostly to help cope with them. (And to anyone who wants to argue that Australia hasn’t had a recession for 26 years, the simple response is (a) check out the fluctuations in the unemployment rate, and (b) check out the fluctuations in the RBA’s policy cash rate.)

Perhaps others will want to point out that the Reserve Bank still seems to think that the neutral interest rate is perhaps 200 basis points higher than the current OCR. Perhaps they are right, and perhaps not. But even if, in some sense, they are right, it will be no comfort – and provide no buffer – if the next recession were to occur in the next couple of years (and if you think that unlikely – as probably I do too – recall that the track record of forecasting recessions, globally or domestically, is even worse than the usual economists’ dismal record of macro forecasting).

If anything, of course, these issues are even more pressing in most other advanced countries. The only upside to having, on average over very long periods of time, the highest interest rates in the advanced world is that the practical lower bound on nominal interest rates is a bit further away here. But it is quite close enough. In New Zealand recessions, cuts in short-term interest rates of 500 basis points or more haven’t been exceptional. After the last recession, the OCR has been cut by a total of 650 basis points, and (core) inflation still hasn’t got back to target. So when you are starting with an OCR of around 1.75 per cent, and the practical lower bound on nominal interest rates is probably around -0.75 per cent, the leeway that is left is much less than one would typically like. People can put on brave faces and pretend otherwise, or simply try to ignore the issue (the latter seems mostly the New Zealand approach), but burying your head under the pillow doesn’t make the problem go away.

And it is not as if this is some flaky Reddellian issue that no one else in the world cares about. In Canada, for example, there is formal process for reviewing their inflation target every five years. At the last review, they left the target unchanged, but only after doing a huge amount of work looking at some of the alternatives. That work was openly foreshadowed (eg in a speech here ), and a great deal of it was published, and is available here.

Over recent years, two former IMF chief economists – Ken Rogoff and Olivier Blanchard – have called for inflation targets to be raised to provide additional scope for discretionary monetary policy in the next downturn. [UPDATE: I had meant to include this link to a recent post from Simon Wren-Lewis, an Oxford professor of macroeconomics, which also touches on the fiscal options.]

In the US context, I linked a couple of weeks ago to a speech by John Williams, head of the San Francisco Fed, openly exploring whether the Fed should move away from inflation targeting to price-level targeting, again with a view to increasing resilience in the next downturn. As I observed then

I’m not persuaded by Williams’ case, but what struck me is how open the system is when such a senior figure can openly make such a case. The markets didn’t melt down. The political system didn’t grind to a halt. Rather an able senior official made his case, and people individually assessed the argument on its merits.

And then a couple of weeks ago there was an open letter to the Board of Governors of the Federal Reserve from 22 economists calling for serious consideration to be given to an increase in the inflation target, and specifically that

the Fed should appoint a diverse and representative blue ribbon commission with expertise, integrity, and transparency to evaluate and expeditiously recommend a path forward on these questions.

As they noted, other senior Fed people had openly acknowledged the importance of the issues.

And was the letter – mostly from a group of fairly left-leaning economists, but including one former FOMC member, and one former member of the Bank of England’s Monetary Policy Committee – just ignored? Time will tell, but Janet Yellen was asked about it at her press conference. Her response?

Ms Yellen stressed in her news conference last week that there were both costs and benefits to a higher inflation target, but she added that the Fed would be reconsidering the issue in the future. “We very much look forward to seeing research by economists that will help inform our future decisions on this.”

There are pros and cons to making changes, whether simply to raise the inflation target, or to look at options such as levels targets for the price level, nominal GDP, or wages. Personally, I would prefer that central banks (and finance ministries) focused on options that eased or removed the effective lower bound on nominal interest rates (issues on which, again, very able people internationally have written). As I noted in an earlier post on these issues

At the extreme, central bank physical currency could be withdrawn and completely replaced with electronic central bank liabilities, on which (say) negative interest rates could be paid. But that would take legislation and considerable organisation, and would be an unnecessary over-reaction, while there is still a considerable revealed demand to transact (in the mainstream economy) in cash. Better options might be to, say, cap the total issuance of Reserve Bank physical currency and allow an auction mechanism to set a variable exchange rate between physical and electronic Reserve Bank liabilities. Banks themselves could be allowed to issue currency again – on whatever terms they chose. Or the Reserve Bank could simply put in place an administered premium price on access to new physical currency (eg a 2 per cent lump sum fee would be likely to introduce considerable additional conventional monetary policy leeway). Each of these possibilities has potential pitfalls and possible legal issues.

But now is the time to be doing the research and analysis. Now is the time to be working through the technical obstacles and logistical constraints. And now is the time to be (a) canvassing the issues in public, and drawing on the perspectives of outside experts as well as public servants, (b) to be making the informed decisions as to whether (reluctantly) inflation targets need to be raised, and (c) to be able to lay out in public a confident articulation of how the authorities envisage that they would handle the next significant recession, given the evident limitations at present.

Why does it matter now? There are at least two reasons. The first is that if a higher inflation target is part of the answer, now is the time to do it. It can’t meaningfully or usefully be done in the middle of the next recession, because by then there will very serious doubts that the authorities can get inflation up to even the current target rate. And the second reason is because when the next recession is upon us (whenever it is) commentators will very quickly realise the limitations of conventional monetary policy. We’ve been used to a world in which central banks could act decisively to lean against recessions – not prevent them, but limit the damage that is done, and prompt a rebound. If people realise that is no longer possible to anything like the usual extent, they will – entirely rational – adjust their expectations in light of that knowledge. Expectations quickly become reality in that sort of climate, deepening (perhaps quite materially) the recession. It would be almost inexcusable to simply let that happen – with all the real adverse consequences on individuals and families from unemployment – when there has been years to prepare against the possibility.

The third consideration is a bureaucratic one. There will be a new Policy Targets Agreement negotiated before the new Governor takes office next March. In the normal cycle of our law, that is the time to make any significant changes in the regime. And now is time to be doing the work on these issues, and canvassing them in public. There aren’t automatically obvious right answers to these questions, and answering them – what are the best guidelines to govern macroeconomic management – isn’t just a matter where those inside the bureaucracy are blessed with a monopoly on wisdom. (It is an unusual and undesirable feature of our law that the Policy Targets Agreement is formulated before the Governor takes office – when he or she may have little specific expertise, and little access to staff (or outside) advice – but that is just one of the many aspects of the Reserve Bank Act that is overdue for reform.)

There are at least two countervailing arguments that I want to address briefly. The first is one that I take some comfort from myself. Foreign trade is more important to the New Zealand economy than it is, say, to the United States. Should our OCR ever have to be cut to the effective lower limit (even if it was then no lower than those of most other advanced countries) it seems highly likely that our exchange rate would fall very substantially. We’ve seen that in the past when the gap between our interest rates and those abroad has closed (most obviously in 2000). That would make some material difference in buffering our economy. Against that, however, it is important to recall that in each past New Zealand recession the exchange rate has also fallen a long way. We seem to have needed both large interest rate cuts and large falls in the exchange rate.

The second countervailing argument is the potential role of fiscal policy. But although New Zealand’s government debt position isn’t bad:

- it is not as good as it was going into the last recession,

- since then we’ve been reminded repeatedly of the potential fiscal pressures from natural disasters,

- there is no coordination framework between fiscal and monetary policy and the Reserve Bank (rightly) has no control over the use of fiscal policy,

- it isn’t clear that in any of the countries that actively used fiscal policy in the last severe recession it was done on a scale that was enough to make a decisive difference,

- while politicians in other countries were often willing to actively use fiscal policy to boost demand for a year (or perhaps two), the imperatives – political, economic or market – for tightening up again seemed to take hold pretty quickly,

- fiscal policy is simply less well-suited to the cyclical stabilisation role than monetary policy.

But if fiscal policy is to be a big part of New Zealand’s answer to the limitations on monetary policy in the next recession, again the issues need to be openly canvassed and debated now.

These are issues that should be worrying the Reserve Bank, the Treasury, and the Minister of Finance. But there is not a hint of such concern in any of their publications or public statements. This isn’t one of those issues – is a bank on the brink of failure eg – where secrecy is required. If anything, it is one that would benefit (perhaps greatly) from open discussion, and a sharing of perspectives, research insights, and other analysis.

Each year the Reserve Bank (for example) is required to publish a Statement of Intent. In many ways it is a bureaucratic hoop-jumping exercise, but it does require the Governor to set out the Bank’s priorites and areas of focus for the coming three years. I’ve written here previously about how these issues – really important medium-term considerations – have had no mention in past Statements of Intent. There will be a new SOI out in the next week or so – they have to publish before 1 July. Of course, at this stage with only three months left in office, what the Governor thinks of as the priorities for the next three years may not matter much in practice. But it will be interesting to see if he has given these “next recession” issues any space in this year’s document. I hope so, but fear not.

It is a shame that he hasn’t used the opportunity of his last year in office, when he could have acted as an honest broker and champion of opening up issues for his successors, to have openly put these issues on the agenda – in public and for the Bank’s own research. To do so would have been fully consistent with his responsibilities under the Act. It would, almost certainly, have been a more appropriate use of his energies than corralling his senior managers into efforts to censor a market economist who disagrees with him in tones the Governor finds uncomfortable. Leadership is about looking beyond the trivial, restraining your own irritations, and focusing attention on important issues that may be just beyond the horizon (and the immediate concerns of officials and market economists) right now, but are no less important for that.

One would hope that when the Board is interviewing candidates for the next Governor (recall that applications close in a couple of weeks) these are among the sorts of substantive issues they are conscious of. But you have to wonder how they would do so. The Board has no role in the formulation of the Policy Targets Agreement, and among its members there is very little expertise in the sorts of issues that need to be grappled with. As a group that has collectively defended the status quo, it isn’t obvious that it would be in the personal interests of any applicants to seriously challenge in front of the Board whether things are quite right. That would be a shame. (And again, it is reason for reforming the Reserve Bank Act – both to shift the setting of the policy target away from the appointment of a Governor, and to shift responsibility for appointing a Governor more squarely to the Minister of Finance.)

As a marker of just how untransparent the New Zealand system is, the Reserve Bank proved highly obstructive a couple of years ago when I sought papers relating to the 2012 Policy Targets Agreement. To the credit of Treasury, while I’ve been typing this post I’ve just received a 90 page release of papers relating to the negotiation of the 2012 PTA. People shouldn’t be having to dig this stuff out years after the event. Setting the rules, and institutions, for New Zealand macroeconomic management should be one of those areas where government agencies are open and pro-active, before and after decisions are made.

With NZ households having $161 billion in deposit savings and $167 billion in long term house debt. It does not matter whether interest rates are at 10% or at 1% from a overall household perspective. The net difference is very marginal. Where it does matter is the effect interest rates have to industry.

Each time our trigger happy RB governors start to raise interest rates, they have a death wish for NZ industry. They tend to push rates up 4 to 5 times in very rapid succession which pushes up the NZD and encourages imports, increases costs and erodes margins. Industry reliant of debt like the building industry is completely decimated and job losses start.

In other words you raise interest rates high enough and fast enough to critically damage the economy and industry in order to damage savers employment which then stops them from spending. Because small incremental increases in interest rates would not slow down consumption in NZ. Savers make more interest income, they have more disposable income and they can spend. Borrowers stop spending. Savers start spending. One offsets the other.

LikeLike

Borrowers have had a pretty good suck on the sauce bottle at the expense of savers

These borrowers have been sucking on the sauce bottle for a very long time now and if they havent used the holiday times to may hay while the sun shone then tough luck

It’s time for savers to have a turn on the end of the sauce bottle

LikeLike

interest rates are supposed to balance supply and demand pressures. While demand remains weakish relative to supply (eg core inflation and U), there isn’t much whole economy case for higher rates (and more than there was a case for lower rates when borrowers were complaining thru the long boom).

LikeLike

NZ private sector debt is $405.9 Billion (RBNZ figures) with Household debt making up 242.5 Billion of that and business/farming the rest. Household debt at 168% of disposable income is among the(2nd or 3rd) highest in the world and probably at it’s realistic upper limit. I believe that it is these high levels and associated extreme asset valuations (rather than an immediate issue with general inflation) that are a concern for the RBNZ as they make us highly vulnerable to catastrophic collapse or Minsky moment.

The fact that we have become reliant for our prosperity on an unsustainable injection of newly created credit money (28 Billion last year) is the real concern. When she blows this next time it will be truly epic (and global?) pretty much regardless of what the RBNZ does.

LikeLike

I disagree almost entirely. the overall indebtedness of NZ vis-a-vis the rest of the world has been broadly unchanged (share of GDP) for 25 years now, even household debt isn’t much higher than it was in 2007, and (compared to the pre-07 period) there is little sign of the systematic speculative excess, across multiple markets, and deterioriating lending standards, that was apparent then.

I’ll elaborate in a post at some stage (incl one why I think stories that keep popping up about comparisons between Aus banks and the Irish ones are just totally barking up the wrong tree).

LikeLike

According to RBNZ figures, NZ household debt is $167 billion. The $242.50 includes Residential investment property debt which is really business related debt.

LikeLike

I know you don’t agree Michael, we touched on this (excessive debt growth) previously, looking forward to your more in depth look at it. I have to say though that the IMF and others are pretty concerned and have described the situation (record debt to disposable income and Auckland houses at 10x income) as a very real threat to our financial security.

You may be interested in this by Steve Keen – mostly regarding Australia but some stats from NZ as well. Just a note for those reading it he uses the term “credit” for annual percentage change and “debt” for the total.

https://www.macrobusiness.com.au/2017/06/steve-keen-on-the-secret-source-of-eternal-australian-growth/

LikeLike

Thanks for the link. There is quite a tension in the IMF material. They struggle – as RB stress tests do – to find a scenario that poses a systemic threat to our banking system, but anguish nonetheless. In my view, they are anguishing about the wrong thing: the high house prices and high debt are genuinely scandalous, and risky, but the risk is probably more social than economic (no less important for that), and the problems arise not from bad banking, or even bad RB supervision, but from that savage interaction of rapid population growth and tight land use restrictions.

LikeLike

George, you have to factor in also that NZ household Net Wealth is $1.3 trillion which makes the net assets around $1.5 trillion. The $242.5 billion household debt is actually very miniscule when compared with the assets of $1.5 trillion. Our fear of taking on debt has resulted in very little investment in infrastructure.

Our banks are very good at risk management and very good at turning in record profits. I would argue that they are too good which points to a monopoly. They have tightened up lending risk management quite extensively. In the current period of falling and flat interest rates the banks can manage their risk easily.

The problem in bank stability arises when interest rates start climbing aggressively. The RBNZ become so focused on rising inflation and as a result raising interest rates they actually become negligent in managing the bank stability risk. This is because banks do not manage the inflow of savings deposits. Most of us do not think of savings deposits as a problem and therefore work hard to encourage savings. The problem with savings to a bank it is a liability on the banks books and the interest paid on savings is a cost, therefore as our trigger happy RBNZ governors raise interest rates too quickly, the level of savings in banks start to rise too quickly as savers start to pressure the banks to offer them a higher interest rate as opposed to other savings vehicles. The inflow of savings start to erode profitability which then puts pressure on banks to lend out. Don’t forget that lending is an asset and the interest received from borrowers is Revenue to a bank.

Lending does not actually slow down as interest rates rise until considerable damage is done to the economy and to jobs and it does erode a banks profit margins and therefore increasing bank stability risks.

LikeLike

Thanks Michael, the RBNZ etc. may be looking in the wrong place for a catalyst. In the posted article by Steve Keen he believes that it is declining credit growth (exacerbated by declining asset values) that will lead to recession and unemployment not the other way round.

LikeLike

Perhaps Central Banks should raise the inflation target as Simon Wren-Lewis explains. I also note the FRBSF put pout a paper explaining how interest rates may well have a lower new normal which I found quite interesting.

LikeLike

Thanks. I had meant to incl Wren-Lewis in the post. Will add a link

LikeLike

I assume the public knows the RBNZ controls the price and quantity of central bank reserves so even if the former falls to zero, the latter has no upper limit (in theory). Given the country’s reliance on offshore investors, tend to agree the NZD would be the safety valve that would allow the CPI index to hit the magical 2.0% marker. Seems very odd to argue for a higher inflation target – history doesn’t seem to suggest higher inflation is a path to riches (unless we are talking house price inflation…)

LikeLike

A higher inflation target wouldn’t be a path to riches, but is an insurance policy about limiting the negative output/employment effects of severe adverse shocks. If we fixed the tax system, the welfare effects of even higher target inflation would be very small. that said, i still favour trying to take steps to make the effective lower bound on nominal interest rates less binding. I’m pretty sure it can be done, but in a sense answering that question, with confidence, is the question that needs exploring – and now, not in the middle of the next deep recession.

LikeLike

…..yes but it is the effective lower bound on one interest rate which indirectly influences market rates that incorporate credit, liquidity, term and other ‘premiums’ which can be erratic; tend to think history suggests the zero lower bound goes hand in hand with a banking crisis – at that point, a nudge here or there on the official cash rate when it is at zero is probably not the major policy worry; that said, agree there should be research on these topics – wouldn’t mind knowing if adverse shocks are really about allocating loss, cleaning up and moving on rather than inflating away past decisions (or putting $2.0bn into failed finance companies..)

LikeLike

Of course, the limitations of a single policy rate are an issue even when the OCR (or equivalent) is at say 7%

Also agree that what causes the recession may well matter in thinking about how quickly things can rebound, but there are plenty of countries sitting now with official interest rates at or very near zero (in some cases below) which didn’t have a domestic banking crisis at all. Switzerland and the UK are just two prominent examples (some of their banks were in great distress, but not on the basis of domestic economy loan losses).

LikeLike

We used to be the laboratory of the world, and many of those experiments turned out pretty well. Now we don’t even want to do the basic research. Sigh…

I don’t really like the higher inflation target for NZ, worry it would lead to even more carry trade (I know that’s irrational for the holders, but still). Prefer incomes level targeting and removing barriers to negative interest rates.

LikeLike

A higher inflation target does not necessarily affect the carry trade because to maintain the higher target there is downward pressure on interest rates. Carry trades in the NZD becomes popular and usually arises when interest rates have risen too high when compared to global interest rates but is still rising but on a long term negative yield track with the NZD rising.

Bond values increase as interest rates fall and thats when you are timing to sell. Bond values fall as interest rate rises, thats when you are buying in, which is the carry trade. All about timing rather than inflation targets.

LikeLike

The last recession in 2007 to 2010 was engineered by the Reserve Bank. But they got way too heavy handed and instead of a slow down we got a long deep recession decimating an entire building industry which dominoed into the bankruptcy and liquidation of 61 Finance companies and the loss of $6 billion in risk capital provided by mum and dad investors.

LikeLike

Steve keen is an interesting thinker but I see him more as experimenting with alternative models that give a bigger role to the banking system. I don’t think any of his models have developed enough to be able to make reliable predictions (even compared to the low bar set by DSGE). Even Minksy was wrong for 40 years before he was right. I think putting a greater weight on market forecasts is more productive, as they act as a kind of summation of all available models.

LikeLike

I haven’t paid much attention to Keen in recent years. I was keen follower for some years, and then The Treasury got him over to NZ for a visit, and I think even those of us who had initially been quite sympathetic came away quite disillusioned. I still keep an eye on his stuff from time to time, but otherwise largely agree withyou.

LikeLike