Some link or other took me recently to the website of the University of Chicago’s Booth School of Business and, in particular, the IGM (economic) Experts Panel that they run.

Every few months, this outfit runs surveys of US-based academics on interesting economic questions. Their panel is described this way

our panel was chosen to include distinguished experts with a keen interest in public policy from the major areas of economics, to be geographically diverse, and to include Democrats, Republicans and Independents as well as older and younger scholars. The panel members are all senior faculty at the most elite research universities in the United States. The panel includes Nobel Laureates, John Bates Clark Medalists, fellows of the Econometric society, past Presidents of both the American Economics Association and American Finance Association, past Democratic and Republican members of the President’s Council of Economics, and past and current editors of the leading journals in the profession.

You might not go to this group for “truth”. Academic economists have biases and blindspots, like everyone else (and tilt leftward politically), and sometimes the answers can look quite self-serving. But a panel like this is likely to provide a fair representation of what US-based economics academics are thinking about issues. They even provide two sets of answers: the raw responses, and a set in which respondents self-identify how confident they are of their views on the particular topic.

Flicking through the surveys from the last year or so, there were a couple of some relevance to the current review of the Policy Targets Agreement – a new PTA is required in the next few weeks – and of the Reserve Bank Act.

The new government has indicated its intention to add some sort of employment dimension to the Reserve Bank’s statutory objective for monetary policy, and they have often cited the (to me rather vague) wording in the US and Australian legislation. In the US, the Federal Reserve is required by law to manage the money supply to grow in line with production, with the aim of thus contributing to

the goals of maximum employment, stable prices, and moderate long-term interest rates.

The Fed itself has reinterpreted this mandate – without statutory authority although probably not unreasonably – as

The Congress has directed the Fed to conduct the nation’s monetary policy to support three specific goals: maximum sustainable employment, stable prices, and moderate long-term interest rates. These goals are sometimes referred to as the Fed’s “mandate.”

Maximum sustainable employment is the highest level of employment that the economy can sustain while maintaining a stable inflation rate.

One of the concerns some commentators here have expressed is whether any employment dimension added to our central banking legislation will have any real meaning or substance. My own view, articulated here previously, is that it could do, but whether or not it does depends on how the provision is written, and what sort of reporting and accountability obligations are imposed on the Reserve Bank in respect of the employment dimension of the goal. The Minister of Finance has not yet proposed any specific wording.

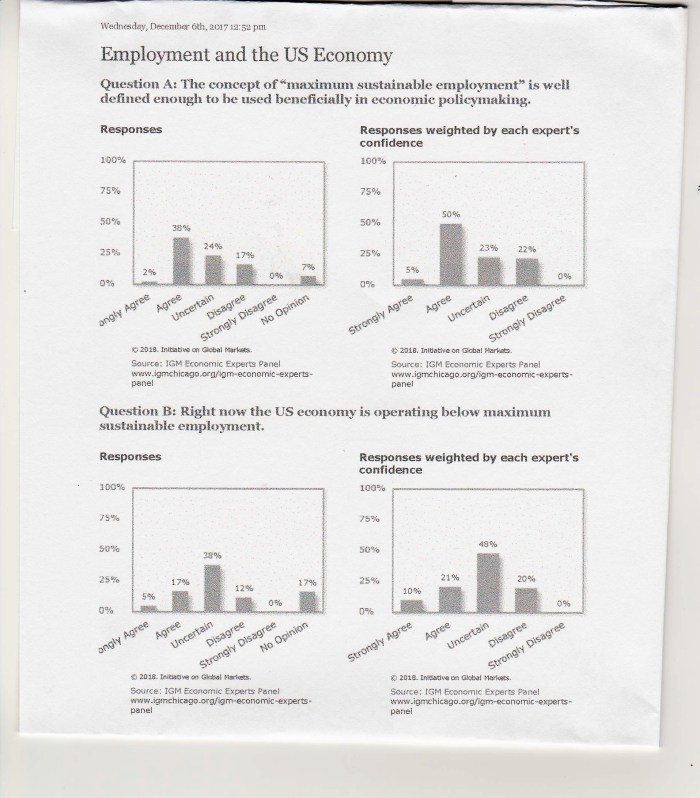

Against this background, it was interesting that the IGM Forum asked their panel members about the US wording.

Weighted by the respondents’ individual levels of confidence, 55 per cent thought “maximum sustainable employment” was well enough defined to be used beneficially in policymaking. 22 per cent disagreed, and the remainder were uncertain.

Weighted by the respondents’ individual levels of confidence, 55 per cent thought “maximum sustainable employment” was well enough defined to be used beneficially in policymaking. 22 per cent disagreed, and the remainder were uncertain.

This survey was done only a couple of months ago. In that light, it is also interesting – although not directly relevant to New Zealand – that more respondents thought the US was still operating below “maximum sustainable employment” than disagreed.

At very least, these sorts of survey responses suggest that the government can come up with a formulation that might pass muster, as useful, among academic economists. As a practical matter – and most of these respondents haven’t spent much time around policy – I’m sure they can. As I’ve noted previously, Lars Svensson – the leading Swedish economist who did a review of New Zealand monetary policy for the previous Labour government – certainly believes some such framing is desirable and practically useful.

It isn’t yet clear whether the government wants a formulation that is practically beneficial and makes some difference to the conduct of short-term monetary policy, or simply wants something that looks different. With Treasury, and the Independent Expert Advisory Panel (of questionable independence if the report on the back page of Friday’s NBR is anything to go by), due to report very soon, we should have some stronger indications before too long.

There was another recent IGM survey question of some relevance to New Zealand and other countries. Last July, panellists were asked their view of the following proposition

Raising the inflation target to 4% would make it possible for the Fed to lower rates by a greater amount in a future recession.

Weighted by the confidence of the individual respondents 86 per cent agreed.

The panel was also asked their view of this proposition

If the Fed changed its inflation target from 2% to 4%, the long-run costs of inflation for households would be essentially unchanged.

A majority (51 per cent vs 29 per cent) disagreed, presumably thinking the costs of inflation would rise.

I’d agree with the majorities in both cases, and would answer the same way if the questions were posed for New Zealand. I’d prefer not to have the target raised to 4 per cent – actually meeting (or perhaps slightly overshooting) the 2 per cent target would do for now – because there are (modest) welfare costs from a higher inflation target in normal circumstances. But limitations on macro policy in the next serious recession is a real challenge, and there is little sign that the Treasury or the Reserve Bank have really engaged with them (eg it never appeared in the work programmes in Reserve Bank statements of intent). And if there isn’t a willingness to address the practical constraint on taking interest rates much below zero, the Minister needs to be taking much more seriously the option of a higher inflation target. Better to address the problem at source, but there is no sign our government – or officials – have been doing so.

For those of a technical bent, in a Brookings newsletter the other day I noted a description of an interesting looking new paper tackling this issue from another angle.

Decline in long-run interest rates increases optimal inflation, but not one-for-one

If the decline in long-run real interest rates in advanced economies persists, nominal interest rates may be constrained by the zero lower bound more frequently. To counteract this, some economists have supported increasing the inflation target. Using a new Keynesian DSGE model, Philippe Andrade of the Bank of France and co-authors find that a 1 percentage point decline in the long-run natural rate of interest should be accommodated by an increase in the optimal inflation rate of about 0.9 percentage point—an estimate that is robust to various specifications that allow for uncertainty about key parameters in the model.

I’m completely against the Reserve Bank doing anything other than controlling the money supply. It is the job of Cabinet and its various ministries to deal with employment levels. There is growing trend towards “technocratic creep” where elected officials transfer more of their responsibilities to unelected bureaucrats, which I believe is being done to reduce their own culpability for the policies they support.

Also, the inflation target should be 0%, erring on the side of positive if necessary.

And the Reserve Bank should open up its ledger to everyone, not just commercial banks and other big operators; we should have full reserve banking.

LikeLike

As a long-run proposition I totally agree with you. But we only have dsicretionary monetary policy at all because of the potential adverse impacts (output and employment) if we’d didn’t.

Re the inflation target, as a first-best I’d agree (and always regretted the move away from something centred on 1% (as the target was from 90 to 96). But it is only viable, in a world of much lower neutral interest rates, if authorities address the self-imposed (by various legal restrictions and regulatory practices) the near-zero lower bound on nominal interest rates. Doing so should be a priority.

I agree that Reserve Bank accounts should be open to anyone, but do not favour mandating 100% reserve banking. In practice, without that, market demand for central banks accounts – outside crises – would be quite small.

LikeLike

Jobs are paramount. 2 World Wars have followed job losses and depressions. Therefore jobs must be at the topmost of any mandate.

LikeLike