Economist and commentator, Gareth Morgan, has begun releasing the policy platforms that his new party, The Opportunities Party, plans to contest next year’s election on. Fairness seems to be his watchword and – within limits – who can argue with that aspiration? But whatever “fairness” means, it doesn’t automatically translate into an obvious set of policy prescriptions.

The first policy he announced was that on tax (document here, and lots of FAQs here). The centrepiece of the tax policy is to apply a deemed rate of return to (the equity held in) all productive assets (including all houses) and tax that deemed rate of return at the owner’s marginal tax rate. Own a million dollar house freehold and if the deemed rate of return was 3 per cent, you’d have an additional $30000 added to your assessed annual taxable income and those on the top marginal tax rate would have to pay, for example, an additional $10000 per annum. The promise is that any revenue raised from this tax would be fully used to cut income tax rates, with a focus on those on below-average incomes. In their own words, they expect this policy would

a. Make the tax system fairer;

b. Make housing more affordable over time;

c. Lead to more sensible investment of capital (everyone’s savings);

d. Make capital more readily available for productive businesses that create jobs and pay wages;

e. Encourage a lot more “trickle down” from those who have stockpiled wealth courtesy of this loophole; and

f. Reduce New Zealand’s reliance on foreign investment and debt to finance our growth.

I’m sceptical.

No doubt tax accountants and lawyers will have their own detailed concerns (some interesting issues were raised in this post from former Treasury and IRD tax adviser Andrea Black).

At the heart of the policy is a concern that the returns on houses are not appropriately taxed. There are two strands to that. The first, and most important in their thinking, is that the imputed rents on living in your own home aren’t taxed. Everyone will, more or less, accept that that is something of an anomaly. After all, if you rent an equivalent house and put your equity in a bank deposit, the returns to that deposit will be taxed. The second is that capital gains typically aren’t taxed (and capital losses typically aren’t deductible). There is much more room for debate about even the theoretical merits of taxing capital gains – to say nothing of the practical problems. But over the last 15 years in most of the country there have been large capital gains associated with housing. Many rental property owners have not been declaring positive net taxable income, but have still made good overall returns through capital gains.

TOP eschew a capital gains tax – rightly in my view – but they appear to believe that their deemed rate of return policy will make future (untaxed) capital gains – house price booms – less likely.

The idea of a deemed rate of return approach to taxing asset income isn’t new in the New Zealand debate. Such an approach is already applied to holdings of foreign equities, and only a few years ago the government’s Tax Working Group reviewed the option as an approach to changing the taxation of housing.

Here are some of the reasons why I’m sceptical.

First, Gareth claims that a big part of the economic problem in New Zealand is an over-investment in housing, and that imposing a heavier tax burden on housing will reduce that. As a result, so it is argued, more resources will be attracted towards business invesment.

This is old ground, but there is simply no evidence of systematic over-investment in housing. Real investment (gross fixed capital formation) in housebuilding has,if anything, been less – over recent decades- than we might have expected given our rate of population growth. Countries with lots more people need lots more housing. Most indications are that we haven’t built enough new houses. And perhaps the best indication of that is the high price of houses and urban land. Over-investment in something is usually consistent with low prices over time, not high prices.

But perhaps TOP have in mind something other than a national accounts meaning of “investment”? They hint at a belief that houses make up more of household overall asset portfolios than is the case in other countries. First, that factoid has been substantially discredited since the Reserve Bank last year introduced new and more comprehensive household balance sheet data. Second, even to the extent it is true it partly reflects (a) overall modest rates of total household savings (people still have to live somewhere), and (b) the extent to which our tax system does not work to bias the ownership of the housing stock towards corporate or funds management entities (often tax-preferred in other countries). And third, for every housebuyer there is a seller – typically, from within the household sector.

Is there reason to think that New Zealand in some sense devotes “too many” real resources to housing. The only one I can think of is that the average size of New Zealand houses – like those in Australia and the United States – is quite large (much larger than in Europe). Perhaps there is something in that, although since TOP argue that we need this policy partly because other countries (including the US and Australia) already deal with the distortions in other ways, it isn’t overly compelling. Nor is it probably great politics to suggest smaller houses – as we get richer – rather than more houses.

TOP claim that their tax policy will “reduce New Zealand’s reliance on foreign investment and debt to finance our growth”. They don’t explain what they have in mind here. Since, as I’ve pointed out, we already devote fewer real resources to building houses than one might expect given our population growth rate, it can’t really be through a channel of less housebuilding. All else equal, less investment would reduce the current account deficit but……the TOP policy document argues we would see more business investment if their policy was adopted, so it isn’t even obvious why the current account deficit would narrow.

I think they must have in mind a wealth effect from high house prices onto consumption. If high house prices encourages more overall consumption then, all else equal, that will widen the current account deficit – although, contrary, to Gareth’s speaking notes at the launch of the policy, not since 1984 have these deficits involved “our political leaders trotting round the world with the begging bowl out”. But as I have noted on various occasions previously, the evidence for a material wealth effect from higher house prices just isn’t very strong. Here is a chart from a post I ran a few months ago showing consumption as a share of GDP over the last 30 years or so.

Almost dead-flat (the red line is the full period average), and if anything edging slightly downwards, even as house prices have gone crazy. That isn’t surprising: high house prices don’t make New Zealanders as a whole richer, they just redistribute wealth from one group to another (and in most cases – since people want to stay living in the same house – even the redistribution is more apparent than real).

In principle, of course, taxing an asset more heavily will tend to reduce its value. Adopting the TOP policy could be expected to reduce house prices, to some extent. But it won’t change the fundamental imbalances in the housing and urban land market (regulatory restrictions on land use the most important, but running head on into sustained government-induced population pressures). And I wonder quite how much there is in the TOP policy proposal.

When the Tax Working Group looked at these issues a few years ago, they could talk loosely about a deemed rate of return of 6 per cent, something like the 10 year government bond rate at the time. These days, having rebounded somewhat in the last few months the 10 year government bond rate is not much above 3 per cent. And the Reserve Bank assures us that its modelling of long-term inflation expectations shows that they are firmly anchored around 2 per cent. Real interest rates – the real risk-free benchmark rate of return in New Zealand are very low. And even then, our interest rates are still materially higher than those in most countries abroad – and, as everyone accepts, that isn’t because productivity growth and real opportunities here are so much better than those abroad. In the UK for example – with a better long-term productivity record than New Zealand, much more government debt, and a similar inflation target – the 10 year bond yield is around 1.3 per cent.

One of the problems with the TOP policy document is that there are no details. They say that is all to be negotiated once they get into Parliament, but it makes a lot of difference whether they plan to use a real or nominal risk-free interest rate, or even a short or long-term rate. Much discussion has tended to assume that a nominal long-term rate should be used. I could make a strong – stronger I think – case for using a real short-term interest rate.

One of the flaws of our tax system – or at least its interaction with our monetary policy inflation target – is that all of nominal interest is taxed, and where interest is deductible all of nominal interest is deductible. That is so even though the portion of the interest that simply compensates for inflation – maintains the real value of the asset – is not (in economic terms) income at all. As a parallel, inflation raises the nominal value of your human capital to maintain the real value of that asset, but it is only the returns to that higher nominal asset value (any increase in annual wages) that is taxed. Economists tend to quite like the idea of inflation-adjusting the tax system, while tax administrators hate it (for practical reasons). It is already more of a problem in New Zealand than in most countries (because we fully tax – and thus double tax – all interest income). But it would be a major new distortion, on a much more serious scale, to impose a nominal deemed rate of return across a much much larger stock of assets (than just fixed income assets that are already over-taxed).

So to me if the TOP policy were to be adopted the logic of using a real interest rate as the deemed rate of return (or fixing the zero lower bound and lowering the inflation target) seems pretty clear.

What about the short-term vs long-term rate issue? No doubt, defenders of using a long-term rate would note that these are typically long-term assets. But…..one has to assume that the deemed rate of return will change over time (even long-term bond rates do). And it seems unlikely that if I buy a house today, Gareth’s policy would offer me tax certainty – say, using today’s 10 year bond rate for the next 10 years. If not, and if the deemed rate of return is subject to, say, annual review at each Budget, then using something like a one year government bond rate would seem a reasonable approach. But the one year government bond rate is around 1.9 per cent at present, and year-ahead inflation expectations aren’t much lower than that. A real risk-free government bond yield in New Zealand at present is around 0.5 per cent. And it is even lower in other, generally more successful, economies.

Now a reasonable rejoinder might be that the times are exceptional, and that these rates can’t last for ever. If I were a betting man, I would probably agree. But……our interest rates are higher than those in the rest of the world, and one of the goals of the Business Growth Agenda is to see that gap close. And we aren’t in the depths of a recession: best estimates are that the output gap might be somewhere near zero, and yet our Reserve Bank expects no change in the short-term policy rate for the next few years. If one is taking a policy to the electorate over the next 12 months, one surely has to work on the basis that the interest rates we have now might be around for some time.

If real short-term interest rates are the conceptually and practically appropriate rate to use in a deemed rate of return model, the tax on that million dollar housing equity would be around $1666 per annum, even for those on the top marginal tax rate. That would be an annoyance to homeowners but – especially with some income tax relief on the other side – hardly likely to materially transform the housing market. From Gareth’s perspective, that could have an upside – an unthreatening introduction, and then when/if real interest rates return to “normal” it begins to bite much harder semi-automatically. But it is a hard sell to make big changes in the tax system for such small potential payoffs at anything like current interest rates.

What else makes me uneasy (more briefly):

- one of my objections to a practical CGT is that it tends to make government revenue even more highly pro-cyclical, encouraging unsustainable spend-ups as asset booms go on. The deemed rate of return approach seems to face very similar problems. Because a lot of housing assets are leveraged, the equity in housing changes more than proportionally with changes in houses prices. A 20 per cent annual increase in house prices – perhaps at a time when interest rates were rising anyway – might induce a 25 per cent rise in annual revenue from this tax. While it is all very well to talk of full offsets in income tax reductions, it is very unlikely that would happen year by year – or else, there will be material increases in income tax rates in the middle of asset busts, which again seems highly unlikely. So, it looks like a policy that will tend to undermine spending discipline just at points of cycles when it is most needed, and undermine government revenue just at the point of the cycle when it is most valuable.

- it is a systematic tax on Aucklanders (most of the asset-based revenue will be raised in Auckland, but income tax rates are national and low income people aren’t concentrated in Auckland). As a Wellingtonian that might not unduly bother me, and as an economist there might be a plausible argument for it, but there are awfully large number of voters in Auckland.

- Valuation issues seem more substantial than TOP allow for. In their FAQs there are blithe descriptions of how house values might be triangulated, but if I am facing a large annual tax on the imputed rent on my house I will likely care much more about the assessed value being used than I will in respect of local body rates. The compliance costs seem non-trivial – and that is before getting into business assets.

- There is a reasonable economic case for a pure land tax. The quantity of unimproved land is fixed, and so taxing that value doesn’t change the supply of land. But this isn’t a land tax. It would apply to business assets as well, as – in effect – an underpinning minimum tax (if existing income tax liability is lower than the deemed rate of return). But many businesses fail – they never succeed in making much taxable income. And while we want a strong stream of highly profitable businesses, one of the ways one gets there is to have plenty of entrepreneurs take risks, and often enough fail. The TOP document talks about the ability of firms to “allow those businesses facing a temporary or cyclical earnings downturn to defer their minimum income tax for a period of up this to 3 years (use of money interest to be charged)”. But that doesn’t seem to deal with businesses that never succeed at all. Imposing a fixed minimum tax, even if it can be deferred for a few years, is an increased tax on entrepreneurship. What you tax, you get less of. And yet TOP talk of encouraging more “productive” business investment and more entrepreneurship.

In the end, I think my assessment of the TOP policy is that a very high level it isn’t necessarily inappropriate, but would be hard to make work well, doesn’t offer very much in a low (real) interest rate world, and is misconceived as a structural answer to either our housing price problems or our sustained economic underperformance.

Next week I will write about TOP’s new immigration policy, which I strongly agree with parts of, while being quite sceptical of other parts. To their credit, it is a more serious engagement with the issues than we’ve seen from other parties to date.

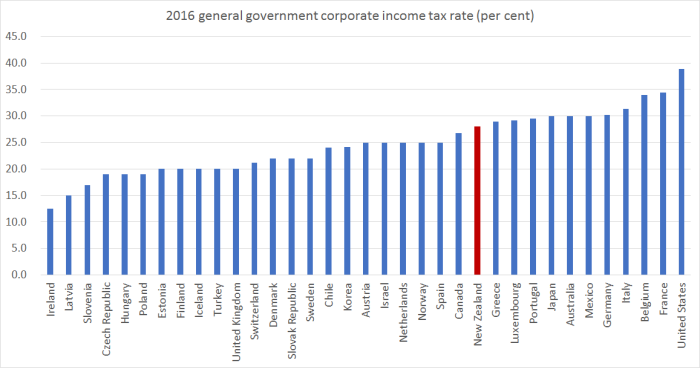

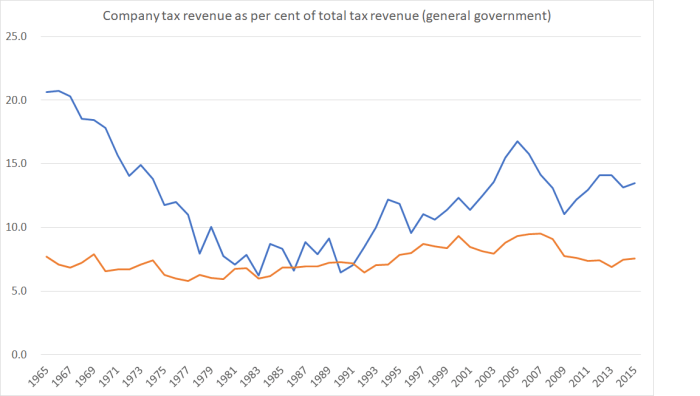

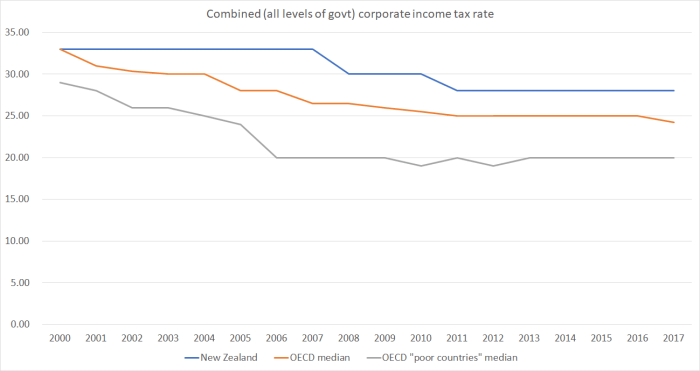

Of the “poor” OECD countries, only Mexico and Portugal now have higher company tax rates than we do. Whereas most of the “poor” countries are closing the income/productivity gaps to the richer OECD countries, Mexico and Portugal (and New Zealand) aren’t. I’m not suggesting it is the only factor by any means, just highlighting the choice that the more successful converging countries have been making.

Of the “poor” OECD countries, only Mexico and Portugal now have higher company tax rates than we do. Whereas most of the “poor” countries are closing the income/productivity gaps to the richer OECD countries, Mexico and Portugal (and New Zealand) aren’t. I’m not suggesting it is the only factor by any means, just highlighting the choice that the more successful converging countries have been making.