A few weeks ago I wrote a post about an article the Herald’s Jenee Tibshraeny had written based on an interview she’d done with the Minister of Finance. Willis was reported as toying with a number of fairly questionable ideas around the Reserve Bank (none involving actually replacing the Board chair). One of those involved the interest rate paid on banks’ settlement account balances at the Reserve Bank. Those balances are currently high (something that is entirely determined by the Reserve Bank; banks themselves can influence only the distribution of the aggregate balances among them).

I wrote then

It would be an arbitrary bank tax, even if Willis amended the Reserve Bank Act to mandate such an approach

I ended the post noting that I had lodged an Official Information Act request with the Minister for all the advice etc she had received on the matter. You will note (above) that Grant Robertson had been pretty responsive to OIA requests on this issue a couple of years ago (and appropriately so, given the OIA’s presumption in favour of disclosure.

The current Minister of Finance’s response came back this morning (and yes, I just noticed that her office dated it 9 August rather than 9 September)

It is pretty remarkable that she is withholding absolutely everything (down to and including titles of papers etc, or initial briefings from many months ago). Not the approach of a Minister with any sort of interest in or commitment to open and transparent government, let alone either the letter of spirit of the OIA (perhaps this is why the annual pro-active disclosure of official papers relating to the Budget has still not happened, more than three months on).

Some weeks ago, after I wrote my post, Jenee Tibshraeny kindly offered me the opportunity to listen to the full interview she’d done with Willis. There were a number of interesting aspects that hadn’t really come out in the article (space constraints and all that), but what really caught my attention was that she mentioned almost in passing that she’d be keen to see the advice on this issue, to which the Minister’s response was that she couldn’t do that as the matter was “under active consideration”.

Section 9(2)(f)(iv) – the clause the Minister cited – is generally interpreted as providing some protection when matters are under active consideration (Ombudsman’s guidance note), in which case we are left to conclude that not only was the matter still being considered when Tibshraeny did the initial interview more than a month ago, but that it is still under active consideration now. She seems to be seriously toying with a law change to allow an arbitrary distortionary and inefficient tax on banks. It is quite extraordinary (or perhaps would be if this were not the Minister of Finance who has already increased taxes on business – removing depreciation provisions on buildings – and whose government last week imposed an arbitrary export tax (on overseas tourism), in what seems to be a pure revenue grab so flagrant that even Steven Joyce – no free market purist – was prompted to attack the move in his Herald column).

One can only hope that there is a less-bad interpretation, but the Minister herself has chosen to go public with the comment to Tibshraeny that she could consider legislative intervention, and the Minister herself is now refusing to release any material on the issue.

Any such “tax” would be a seriously retrograde step and would be a signal that the government was much more interested in populist bank-bashing (Green Party style, worse than Grant Robertson) than in serious policymaking. It would be a pure revenue grab, that might even garner a few cheers from the cheap seats, but would command not a shred of respect (for her or for New Zealand policymaking more generally) from serious observers, here or abroad.

If, for example, the high level of settlement cash balances troubles her – and it should, as a reflection of past mistakes – perhaps she should have done something about (eg) replacing the Board chair and filling the Board vacancies, with people who are serious about holding Orr to account, and getting a more rigorous approach to policymaking at the Bank. There has been quite enough bad policymaking in recent years without Willis and Luxon adding to it.

It didn’t used to be terribly controversial that powerful independent government bodies and powerful statutory officeholders should “stay in their lane” or “stick to their knitting”. Those entities/individuals typically have a pretty narrow set of official statutory responsibilities and if they are exercising power independently of the naturally-partisan governments of the day, they should focus their energies on those official responsibilities and keep quiet about, and keep out of, other stuff. Central banks are a classic example. Independent central bankers exercise enormous delegated power in some narrow and specific areas (monetary policy, banking regulation). Part of the way they build and retain trust – our willingness to delegate that power to them – is by doing the day job excellently. But one of the other ways is by staying out of other highly contentious and/or party political stuff. We need to be able to be confident that these very powerful people aren’t using their (rather limited) official position to advance personal ideological or political agendas. And, frankly, that should be so whether or not we as individuals might happen to agree with a particular cause the powerful decisionmaker happens to be advancing (I’ve written here previously (see link above) about Orr in this respect, but also the very dubious case of Don Brash – as Governor – and the Knowledge Wave speech, some of which I did agree with). As I noted in an earlier post

We should value a good independent central bank, but the legitimacy of the institution – and its ability to withstand threats to that independence – will be compromised if Governors play politicians or independent policy and economic commentators.

And that applies to statutory members of the Monetary Policy Committee too, especially ones employed fulltime in the service of the Reserve Bank.

(Here I would note that, rightly or wrongly, central bankers have tended to be given more societal leeway to weigh in on this, that or the other policy issue when the central bank itself is perceived to have been doing its day job excellently. No serious observer would accord that description of the Reserve Bank of New Zealand in the last few years,)

I opened The Post this morning to find a headline “Cutting a $20b fossil fuel bill”, and read on. It was a report on a new paper from a think tank called “Rewiring Aotearoa” championing widespread electrification and all sorts of policy levers in support of that end. Fair enough you might suppose, were it coming from the Helen Clark Foundation, or really anyone independent. They are welcome to present their arguments and make their case. But it wasn’t until I got halfway through the article that I learned that “it was co-written by Reserve Bank chief economist Paul Conway”.

The chief executive of this think tank, one Mike Casey, was at pains to assure us that

So, at least according to Casey, the Reserve Bank didn’t “endorse” the document, but had it seems done enough checking to know that it was all “economically viable”. Quite whether that is how the Reserve Bank would see it – having its imprimatur asserted by Casey – is not clear (one would hope not). Casey himself seems like a pretty entrepreneurial guy – and was featured on Country Calendar last year around his impressive central Otago cherry orchard – but……he isn’t a central bank statutory officeholder wielding considerable power/influence over the macroeconomy and not supposed to be using his office, or associations, to advance personal agendas.

I went and downloaded the report, which was apparently released yesterday at an online event in which the two speakers were an Australian entrepreneur/author and Conway. There were four authors of the paper but Conway is one of the two used to market the release.

I opened the report and the concerns grew. On the first page I found this

So Conway’s involvement in this report is explicitly linked to his rather important day job as chief economist of the Reserve Bank. Conway must have been aware of this, highly inappropriate, linkage being drawn (he is a co-author, it is on the very first page).

Then I went looking for any sort of disclaimer. Often enough, when official agencies publish their own research reports there is a standard disclaimer noting (generally not very credibly) that views expressed are those of the individual and not necessarily those of the institution they work for and which is publishing the research. Here, as illustration, is an example from a recent Reserve Bank research Discussion Paper

But there is no disclaimer at all on the Rewiring Aotearoa paper that Conway co-authored and fronted, even as he is presented by them as the chief economist of the Reserve Bank. Conway simply cannot be unaware of this lapse: even if he was authorised by the Reserve Bank to get involved in this project in whatever spare time he has, surely they and he would have been bending over backwards to ensure that there was no association between this involvement and the Bank? A disclaimer would have been the bare minimum. At least among central bankers with any regard at all for appropriate boundaries.

Perhaps you wonder if all this is just very technical and not worth bothering about. Well, here (from Rewiring Aotearoa’s LinkedIn)

This is a highly political project. And there is nothing wrong with that – it is how policy debate goes – but not the place for the central bank’s chief economist (and even less when pro-actively identified as such, with not even a hint of a disclaimer in the official report, even while the champion of the project claims that the Reserve Bank thinks it is all very robust or they wouldn’t have let their chief economist get involved.)

Or there is this from the report itself

I’m sure parts of the political spectrum will really welcome the report and be cheering on its state-led approach. But senior central bankers aren’t supposed to be championing divisive causes – at least not ones other than those Parliament has specifically assigned to them.

You’ll note earlier that the report described Conway as having given his “personal time” to working on this report. One does wonder quite how much spare time a senior manager of the Reserve Bank actually has. After all, this is an agency that has been coming off the back of the biggest policy failure, in Conway’s own area, in decades (the sustained outbreak of inflation, only just now getting back inside the target range). It was Conway himself who was on record after the May Monetary Policy Statement lamenting potential problems with either the modelling tools or the Bank’s use of them (both things the chief economist might be thought primarily responsible for). Mind you, this was the same Conway who chose to take his holidays and miss the (July) Monetary Policy Committee meeting where the MPC executed perhaps its biggest U-turn in decades in such a short space of time. Very few people looking at the conduct of monetary policy over the last six months (hawkish lurch in May, quick reversal in July, rate cut in August, all on not much new data) would think that all was well in the economics functions of the Reserve Bank, and that it was appropriate for the Bank to be signing off on its senior officeholder getting heavily involved in any other project, no matter how non-political or innocuous.

And is if all that wasn’t enough, it is worth remembering the Code of Conduct governing MPC members

Conway’s boss is the underqualified Karen Silk, but it is hard to believe that this involvement wasn’t signed off by the Governor himself. It shows remarkably poor judgement by all three of them (Silk, Conway, and Orr), around both the initial involvement and the active identification of Conway’s involvement in the Rewiring Aotearoa report and the absence of any serious disclaimer (not that the latter would have materially allayed concerns).

I’m sure work in the area of this report was after Conway’s own heart. His inclinations seem to be to the technocratic left, and his professional experience has been most strongly in these microeconomic areas and issues around productivity. But he chose to take up a role as a senior statutory officeholder, wielding huge influence over the near-term performance of our economy. That needs to be his focus, and we need to be able to trust that he – and his colleagues – are using their professional endeavours only for the narrow task Parliament has given them.

In a serious world, the Minister of Finance and the chair of the Reserve Bank’s Board would be asking hard questions about all this, including around the judgement of those involved. In latter day New Zealand (with Quigley and Willis in those offices) it seems sadly unlikely. And so standards degrade even further, and there is a bit less reason still to have any trust in or respect for our central bank.

The Minister of Finance has, over the last couple of weeks, been trailing various possible changes in the financial system. At the National Party conference there was the suggestion of trying to beef up Kiwibank, including by the injection of some additional capital from other than direct central government sources. And last Friday, there was an interview with the Herald’s Jenee Tibshraeny in which the Minister talked up the idea of overriding various bits of policy that are now squarely the legal responsibility of the Reserve Bank. Commentators suggest all this talk is to a considerable degree about preparing the ground for the release next week of the final report of the Commerce Commission’s report on elements of the banking sector, perhaps trying to ensure that there is little plausible ground for Labour or the Greens to attack the government on banking profits, access to services, or whatever.

I’m not going to respond in depth to all the Minister’s suggestions. On Kiwibank, I largely agree with VUW banking academic (and former regulator) Martien Lubberink’s column, and (rarely, and as it happens, even with John Key). If it were me, I would sell 100 per cent of Kiwibank tomorrow, simply because there is no good reason for a government to own a commercial bank, but I am even more wary of partial privatisation of a bank than of the status quo).

The Minister also suggested that she might change the law to force the Reserve Bank to (a) lower bank capital requirements, and b) provide carveouts for some or other favoured groups. Now, as it happens, I have long argued that prudential regulatory policy settings should be decided by the Minister of Finance, on the advice of the Reserve Bank and The Treasury. As Willis notes, she is accountable, and the Reserve Bank is not (although the Minister decided to reinforce that effective unaccountability recently by further extending the term of the chair of the Reserve Bank Board – and it is the board that now wields the prudential policysetting powers). But if you really want to make a change like that you do it after wide and serious consultation, or perhaps even as part of a well-trailed campaign promise, not simply (as it seems) to play distraction because another government agency might be about to release a briefly awkward report. I’m also inclined to think bank capital requirements are higher than is really warranted (that was my view when the policy was being set five years ago and remains so today) but if you want to be taken seriously as a Minister of Finance, you don’t just drop such a view into an interview – with, it appears, nothing in support – you outline carefully your case, or commission some reviewers to look into the matter carefully. Martien Lubberink also addressed this set of Willis comments, including this apt line.

But the item in the Minister’s grab-bag that I wanted to comment on was around the remuneration of settlement account balances held by banks at the Reserve Bank. On these balances – the aggregate level of which is determined wholly and solely by the Reserve Bank – banks are paid the OCR (currently 5.5%). The level of settlement cash balances is currently around $43 billion – off its highs, but still hugely higher than the $7bn or so that was more common pre-Covid. The reason for the difference? LSAP bond purchases by the Reserve Bank, and the subsidised direct lending (under the so-called “Funding for Lending” scheme) from the Reserve Bank to banks.

In the Herald interview the Minister is reported as saying that “she had asked officials for advice on the way the RBNZ manages banks’ settlement accounts”, and in further comments in the same interview making clear that she was referring to how interest was paid. She goes as far as to suggest that it might be appropriate to amend the Reserve Bank Act to compel any change in approach that she considered warranted.

The issue of remuneration of the high settlement cash balances has been around for a couple of years. I think I introduced it first to the New Zealand discussion with a post in late 2022 on a paper by a former Bank of England Deputy Governor in which, among other issues, he suggested a possible case for paying below market rates on some portion of the large (at present) settlement cash balances in the UK. My post was headed “A bad idea”, which remains my view. That October 2022 post prompted Tibshraeny to give the issue a bit of coverage, which in turned seemed to prompt the then Minister of Finance Grant Robertson to ask for some official advice on the matter. Tibshraeny OIAed that advice, and I wrote about it in another post in March 2023. Neither the Reserve Bank nor The Treasury were at all enthusiastic, and there even Grant Robertson – who, we later learned, had at the same time been toying with windfall profits taxes on banks – left it. It was, after all, on current legislation simply a matter for the Reserve Bank (the OCR, the rate paid on settlement cash balances, is the primary instrument of monetary policy, and the Reserve Bank has operational independence).

There is a bit of a view around in some quarters that changing remuneration practices could undermine the effectiveness of monetary policy (in fact, it was one of the lines the Reserve Bank used on Robertson). That isn’t necessarily so. Tiered approaches have been used elsewhere (including by the ECB when they had negative interest rates, as a subsidy to banks in that case), and so long as one clearly distinguishes between a first tranche that received a nil or below market rate from the marginal balances on which the full OCR would be paid, effective monetary control would not be impaired. But that doesn’t make the policy option the Minister was openly toying with a better idea. In fact, it is still a very bad idea. Bank settlement account balances don’t just arrive in a vacuum – rather they are a counterpart to a change in some or other items on bank balance sheets (eg a bank increases its settlement account balances when it wins deposits from another bank, or (in this case) when (say) a customer sells government bonds to the Reserve Bank and deposits the proceeds in a bank account, on which the customer will normally and reasonably expect a return). Running a tiered approach to remuneration of settlement cash balances, of the sort Paul Tucker first proposed a couple of years ago, is simply an arbitrary tax on banks, and financial intermediation more generally, without any analytical foundations or – if the RB simply did it – without any parliamentary scrutiny. Taxes should be imposed by those whom we elect, our MPs sitting in Parliament.

But changing the law to enable the Minister to direct the bank on policy on remuneration of settlement accounts, or simply to mandate a completely different model, would be hardly any better than the RB just arbitrarily making such a change. There would be some formal democratic legitimacy, but for a policy that has just no substantive merit. As there was no good case for a windfall profits tax for banks, so there is no decent case – not even a shred of one – for a targeted ongoing tax specifically on banks. It would be arbitrary, inefficient, largely borne by New Zealand depositors and borrowers, and would send a simply dreadful signal, at a time when international markets are already looking askance at the Reserve Bank and the conduct of policy – and the policy “debate” more generally.

I don’t suppose it is very likely that Willis and the government will end up doing any of the things she trailed in last week’ Herald interview. Doing them probably wasn’t the point – rather the pursuit of a good headline with a certain sector of the New Zealand audience, narrowing room for Labour and the Greens, seems to have been the point. Empty populist rhetoric seems a description closer to the mark than serious considered policy options and analysis (note that not a hint of any of this appeared in the election campaign, less than a year ago). Perhaps the rhetoric plays well with some focus groups, but it hardly enhances any reputation Willis aspires to to be (and be seen as) a more serious Minister of Finance (focused on things that might make a real difference) than her predecessor.

I’ve already noted that Willis could readily have changed the chair of the Reserve Bank board when his term expired (her government has been happy to replace various other chairs in agencies where dismissal at will as an option). She could have filled the vacancies on the board with people better qualified than those Robertson appointed but hasn’t done anything about that either. It remains almost beyond comprehension that she didn’t move on either front, and suggests she isn’t really serious about any of this. In the same vein, each year the Minister of Finance writes a Letter of Expectation to the Board, an opportunity to highlight her priorities or things she wants the board and Bank to have regard to etc. The 2024 letter is sitting on the Bank’s website, and has not a hint of any of the sorts of issues/concerns Willis was raising in the Herald interview. She also hasn’t revised the Financial Policy Remit (a new tool) issued by Robertson a couple of years ago. There are things around the Reserve Bank that the Minister can’t easily or quickly fix (eg she is stuck with the Governor, unless he chooses to go early, for another 3.5 years), but she has shown no sign of doing any of the things she could (eg Board chair and vacancies, unwinding new indemnities the Bank has been given) or of using any moral suasion (eg through the letter of expectation) around financial policy issues or the Bank’s budgetary excesses.

So it all just looks a lot like a search for a good headline, and political operatives managing tactical risks for a couple of weeks, rather than a Minister with any sort of serious interest in, or intent towards, a much better central bank, whether in its monetary policy or financial regulatory roles. Perhaps in that sense she and the Governor – who seemed to have such a testy relationship when National was in Opposition – deserve each other. It is just that New Zealanders deserve much better from both roles.

(I have submitted an OIA this morning for the advice etc around remuneration on settlement cash balances. It will be interesting to see if either Treasury or the Bank are giving Willis even slightly different advice now than they gave Grant Robertson last year (but it seems unlikely).

A week or so back I did a post, prompted by some tweets by @Charteddaily, about the Reserve Bank’s big-spending plans for the current (24/25) financial year – the financial year, that is, in which many Wellington bureaucracies are facing quite some considerable expenditure restraint/cuts, most particularly those that don’t really do stuff that directly faces members of the general public.

There was the 20 per cent planned increase in spending on staff salaries – with inflation coming down it must be a big increase planned in staff numbers, and the really extraordinary $35 million planned spending on “engagement with the public and other stakeholders” (this on top, apparently, of the item further down about communication of MPC decisions).

No one seems to have any clear idea what this $35 million is (nothing they’ve published gives any real sense) and although, as I noted to someone the other day who asked if I had any idea, it just can’t be quite as bad as it sounds, it sounds pretty bad indeed.

Today, @Charteddaily was at it again, having dug out from Parliament’s website the Reserve Bank’s responses to their 2022/23 financial year Annual Review undertaken by FEC. There are all sorts of gems apparently, from the $5500 spent at the Maranui cafe in Lyall Bay for offsite planning/team-building (lots more on other such events). Perhaps, and just possibly, some level of expense on those sorts of things is necessary and even warranted (it was, after all, 2022/23 a year of Labour fiscal excess), but when I scrolled through the documents what really caught my eye was the bloated spending on communications functions. Here are the permanent staff numbers

So that was eleven full-timers on “content and channels”, and six for internal communications alone (this is an organisation with only two offices and about 500 staff). @Chartedaily checked and found that The Treasury has only six communications staff in total……. Now, the Reserve Bank is a little more public facing than The Treasury, so you might expect a few more, but….more on internal comms than Treasury has in total? Really? Well, apparently so on the Orr/Quigley/Robertson watch (and Robertson gave them a second big boost to their funding agreement during this period).

Then there is some time series data

Note that on top of the 27 permanent staff there were 4 contractors (although a later table suggests they mostly work on other stuff). 27+ communications staff (and they still can’t even commuicate monetary policy competently – see last two OCR reviews). Oh, and the salary budget in 22/23 was five times what it had been in 2018/19, Orr’s first full year. (I recall doing an OIA several years ago when the comms staff were around 18, and that seemed flabbergasting enough……but 31 of them now).

What has the Board and Board chair been doing? Presumably just what Nicola Willis wanted given that (a) she just reappointed the Board chair, and (b) raised no issues around spending restraint in her letter of expectation to the Board.

One part of the communications empire is responsible for OIA requests, so you’d assume that with so many resources they’d be just superb in responding to those requests. But….whereas in 2019/20 78 per cent of their 100 OIA requests were responded to within the statutory 30 days, in 2022/23 only 54 per cent of their 94 requests were. That won’t greatly surprise anyone who has ever dealt with them, but is still striking to see it in print.

It is a great deal of money being spent by an organisation with very weak accountability, and without even the excuse/rationale that they do a lot of direct public-facing stuff. They don’t sell stuff to the general public, or grant things to the general public. They mostly deal with banks, financial institutions, other government agencies, and various vendors. Their policies affect many or most of us indirectly in various ways but – mercifully – we aren’t yet subject to massive billboards of Orr and the MPC, or full page newspaper adverts etc. Not even a mea culpa for losing taxpayers a mere…..$11 billion (which swamps even the comms budget).

And it isn’t even as if their communications is that good. It just isn’t obvious what they – and more importantly we – are getting for the money they are spending. Their main documents seem okayish, but nothing spectacular. They seem not (mercifully again) to be running a TikTok account, and although they do have an Instagram account it doesn’t seem to have very many followers (as you might expect: central banking done well is supposed to be pretty dry and boring; grey men and women operating technocratically and (supposedly) expertly). You are rather left wondering what these 27+ people actually do all day? But that is probably just a failure of imagination….always meetings to attend, coffee catch-ups to hold, and so on.

It really is quite extraordinary. Not so much that Orr and Quigley would do this if they could (bad bureaucrats will, and recall that in his day job at a university Quigley was spending $1m on a lobbyist), but that ministers enable it and now, apparently, endorse it. It was Robertson-era excess in 2022/23 – the stuff National rightly complained about – but…..the chair has just been reappointed, the budgets are expanding again.

And that is now on the new Minister of Finance who seems to have done nothing about it. (You rather hope The Treasury monitoring reports to the Minister are doing something about highlighting such excess.)

It isn’t something I’d usually recommend (or even do myself) but the useful new Twitter account @Charteddaily (basically one interesting New Zealand chart a day) posted a couple of charts drawn from the suite of Reserve Bank documents that were released last Thursday, and they piqued my interest (and, for reasons you will see below, concern).

But first, also on Thursday there was some attempt by the government to defend the extraordinary reappointment (yet again) of Neil Quigley as chair of the Reserve Bank’s board (which I’d written about, and lamented, here). The Herald’s Jenée Tibshraeny had got in touch with both the Minister of Finance and with David Seymour (both an Associate Minister of Finance, and leader of a party that had also firmly opposed Orr’s reappointment – something recommended by Quigley’s Board – and whose Finance spokesperson had only a few weeks earlier suggested that Orr (still supported by Quigley and his Board) was unfit for office). The article is headed “Nicola Willis and David Seymour confident in call to appoint…”. If you read the article carefully, Willis never actually explains why she did what she did. She says she stands by her previous criticisms of the Bank and of Orr’s reappointment – thus putting her clearly at odds with Quigley’s views – and the only new observation she makes (that Quigley played a “key role” in establishing the new RB Board) seems irrelevant (not only was that transition presumably why Grant Robertson gave him another two years in 2022, but the Reserve Bank itself shows no sign of any better performance now, whether Governor, MPC or more broadly).

I guess one should give credit to David Seymour for engaging more substantively (since he isn’t the responsible minister he could have just hidden behind Cabinet collective responsibility), but his more extended arguments simply don’t wash either. This was the bulk of his comments

None of this washes. I’m sure many people have heard the story of Orr once being pulled out of a Board meeting by Quigley to get him to calm down. That’s good, but what about the repeated active misrepresentations to FEC, or the dismissive approach Orr – Quigley’s man – routinely takes to any criticism or disagreement. And quite how losing 10 of your top 26 people in short order, several of whom had only recently been promoted by Orr, speaks to Quigley’s value I don’t know. And “chopping and changing”? Quigley has been on the Board since 2010, chair since 2016. Actually, turnover and fresh faces have value (as is widely recognised in other government appointments), especially when the institution has not itself done a good job (massive financial losses, serious inflation outbreak etc). When you can’t change the chief executive (and the government can’t until 2028) getting rid of the chair, at the end of his term, when the chair has backed the Governor all the way, was the way to signal a seriousness about wanting something different. On the evidence of the Willis/Seymour words and actions, this government – once in office – doesn’t.

And it isn’t as if the Bank – Orr or Quigley – is changing of its own accord. This was the first of the snippets that @Charteddaily had highlighted (drawn from RB Annual Reports and from the last two Statements of Performance Expectations).

That is a further 21 per cent planned increase in staff expenses in the year that began on Monday, on top of really large cumulative increases over the Orr era to date. It is just staggering, in a year when almost every other government agency is being expected to cut back, often quite materially. The Reserve Bank is funded through a five-yearly Funding Agreement, and the current one doesn’t expire until 30 June 2025, so the government couldn’t compel them to cut back immediately, but (a) there isn’t anything in the Minister’s letter of expectation (sent back in early April, only finally released last week) urging them to do so, and (b) it is in stark contrast to the voluntary savings in place by ACC, also not funded by direct parliamentary appropriations. The Orr/Quigley approach seems to be “hey, we are the Reserve Bank, we’ll just go our own way”. And there is not the slightest evidence that the Minister of Finance cares.

Then again, her government is throwing out new subsidies to fund Shortland Street.

And it is not as if they are throwing lots more money at improving their monetary policy and inflation research or analysis. Actually, comparing this year’s Statement of Performance Expectations to last year’s, in 2024/25 they plan to spend $46 million on monetary policy up just slightly from a planned $45 million in 2023/24.

So what are they spending their (well, our) money on. This was where I was really gobsmacked by a @Charteddaily tweet, trusting that the person behind that account read documents accurately but still not quite believing it.

Yes, you are reading that correctly: $35 million in 2024/25 on “engaging with the public and other stakeholders”. Since issuing physical cash (zero interest liabilities) is a highly profitable business (forecast net operating profit $483 million), this weird category of “engagement with the public and other stakeholders” is really their biggest item of spending.

I’ve been reading around their documents over the last day or so and I still find it incomprehensible, on numerous counts. First, one would normally have assumed that any costs – including communications costs – associated with the Bank’s various statutory functions (monetary policy, financial system regulation and oversight, foreign reserves etc) would have been allocated to those functions themselves. And you can see that when it comes to monetary policy there is a specific item for “Communication and implementation”. Promoting the institution itself, distinct from its specific statutory responsibilities and powers, is simply not a legitimate use of (very large amounts of) public money.

Here is a high level summary that I found on their website about this activity

But it doesn’t really help. The Reserve Bank, for example, doesn’t fund Parliament. Rather, like any public agency, it is required to front up when called, and the costs of providing information to FEC would, one would have thought, been (modest and) allocated to the respective functions (directly in the case of MPSs and FSRs, perhaps indirectly in respect of the overarching corporate documents).

Much the same goes for 6.1, with the added point that granting media interviews tends not to cost taxpayers anything. The Governor in particular seems to use his rare interviews to hand wave and distract rather than to engage with alternative perspectives or criticisms. As for speaking engagements, there is a bit of cost to them (getting out and around the country) but what has been noticeable for years is how few such engagements – at least on the record ones – they do; hardly any at all in the case of MPC members. And shouldn’t such costs be allocated to (in this case) the monetary policy function?

And so we are left with 6.2. What is proposed? Some massive advertising campaign, indirectly subsidising NZ media? Surely not, but then if not then what? A fair question for Treasury to be asking the Reserve Bank is something along the lines of what outcomes would be worse for New Zealanders if this line item was to be cut by 80 per cent?

The performance measures in the Statement of Performance Expectations are not really any more helpful

None of it tells us what they are actually spending so much money on (or why most of the costs are not allocated back to respective core functions).

There was some verbiage and effort at distraction in the Statement of Intent itself

Quite what any changes in the “media landscape” might have to do with the extent of trust people might repose in New Zealand’s central bank isn’t clear, but I guess playing distraction is better than identifying factors like:

presiding over the worst inflation outbreak in decades, and then trying to openly blame it on everyone than the central bank itself,

losing taxpayers $11.5 billion in a huge bond market punt, and then refusing to seriously engage on the extent of the loss and associated misjudgement,

everyone involved in these decisions (Governor, MPC members, Board chair) getting reappointed, only confirming that “accountability” has been emptied of all content,

the appointment of a DCE responsible for macro and monetary policy with not the slightest background in that area,

blackballing people with research expertise from the new Monetary Policy Committee, and then years later assserting openly that there never was such a ban,

a Governor who is universally known to be intolerant of debate or challenge/disagreement,

barely any (and then of no depth) serious speeches from key monetary policy figures through the worst inflation outbreak and period of greatest policy uncertainty in decades,

a central bank that shows little sign of being exclusively focused on the limited range of things Parliament instructs it to do, instead pursuing management/Board ideological causes.

and so on

But sure, try blaming the “media landscape”. Seems a bit more like an effort – at taxpayers’ expense, from public officials – at active disinformation.

And if you are inclined to doubt the point about loss of focus, I can only suggest reading the Statement of Intent itself. “Climate” gets more mentions than either “inflation” or “price stability”, and if that particular ratio is (much) less bad than it was in their previous Statement of Intent, what hasn’t changed is that while “inflation” gets five mentions, and “price stability” six, “Maori” features 52 times (pretty similar to the previous Statement of Intent). And, yes, I did check and it is not that they are publishing lists of all different ethnicities: neither Asian, Pacific, nor European get even a mention (and nor would you expect any of them to do so in a central bank actually focused on its mandate, which by its nature operates pretty pervasively across the entire economy, regardless of religion, ethnicity, sexuality or whatever).

But Orr and Quigley have a crusade.

I checked again the Reserve Bank Act. There is but one substantive reference to “Maori” in that legislation (in a “good employer” section) and none at all – again unsurprisingly – to the treaty of Waitangi.

But you wouldn’t guess it from reading the Statement of Intent. It starts – first substantive page – with the tree god nonsense Orr used to spout on about a few years ago (complete with dodgy economic history about the founding of the Reserve Bank). Their so-called Te Ao Maori strategy gets two whole pages, complete with links to their treaty of Waitangi statement, well before any serious discussion about monetary policy, the cash system, or the soundness of the financial system, none of it grounded in statute. It pervades the document.

Now, in fairness to Nicola Willis, her letter of expectations to the Bank’s Board is different than those from Robertson. There is nothing at all of the dubious ideological stuff that Robertson used to throw in. But what difference has it made? None, apparently, given that her letter is dated 3 April, all these corporate documents came out only last Thursday, and none will have been a surprise to the Minister, since she had to be consulted. And yet she and the Cabinet reappointed Quigley.

Just breathtaking.

I’m still at a loss to understand what they have included in that $35 million. Perhaps they will now stop stonewalling on OIAs, and stop trying to charge me for information they should have released 5 years ago (but then OIAs weren’t even mentioned in that “engagement” description). Pro-active openness also tends to be even cheaper than handling OIAs, but that is something the Bank seems totally averse to. Perhaps they could spend a bit on a better proofreader (the table that showed that $35m had a typo in its title).

But more seriously, we deserve to know what this total includes, and why they are spending so much of our money to try to make us like/respect them (when just doing their job well – and only their job – would do more of that, and have substantive benefits to us). I suspect – but can’t confirm – the $35 million includes a lot of spending on things that really can’t be tied at all to statutory functions: their climate advisers, their Maori advisers, their diversity and equity (so-called) people, their multi-national central bank indigenous network costs etc, although it is still really hard to see how it gets to $35m per annum (hard to tell how much of an increase it is for this year, as they have changed their presentation, athough a number from last year that looks to be similar is about $29m).

While pouring out lengthy bureaucratic documents they avoid real scrutiny, they don’t do their day jobs at all well (we are living with the aftermath of really bad misjudgements in 2020/21), never show the slightest contrition, and feel free to use large amounts of public money to pursue personal ideological agendas not even slightly grounded in their statutory responsibilities, they rarely engage substantively, publish next to no research, and so on.

And yet Nicola Willis (and her leader and Cabinet) seem quite unbothered and just went ahead and reappointed the chair yet again.

Then again, this is the government – that campaigned up hill and down dale on fiscal excess and waste – which yesterday announced big new subsidies for……keeping an old local soap opera going.

although it was followed with more comments trying to reframe what the Bank had published in the MPSonly a couple of days ago.

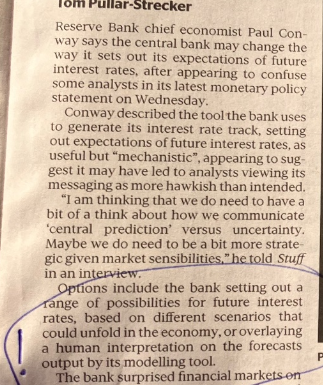

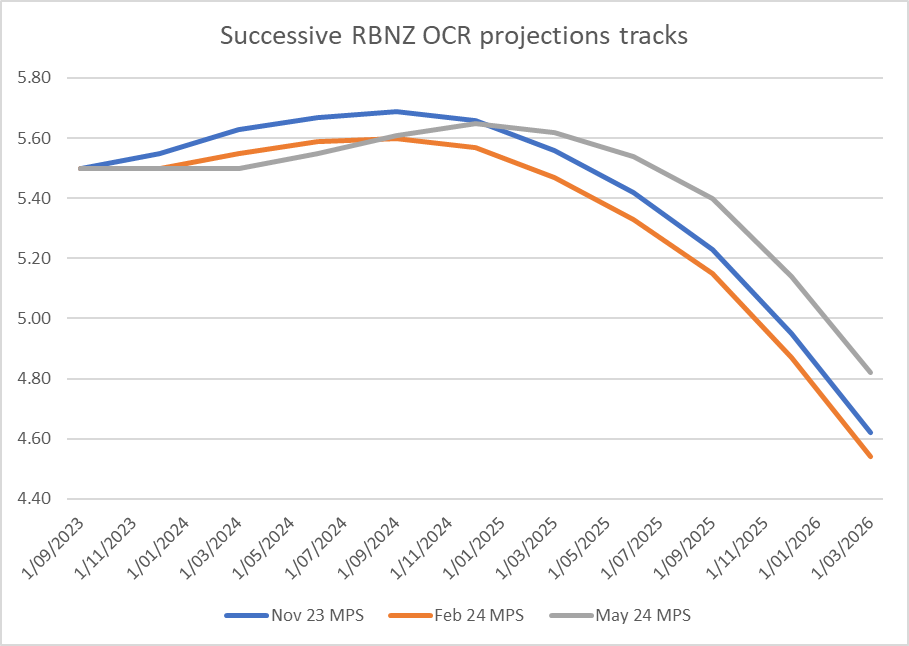

The Bank has been publishing a so-called endogenous track for short-term interest rates, as a central indication of what it believes to be required to deliver inflation at or near target 1 to 2 years ahead, for more than 25 years now. If the current crop of MPC members doesn’t yet understand how their numbers will be interpreted, that is more of a reflection on the MPC, and their chief economics adviser, than on the tool. (I’m not a big fan of publishing medium-term interest rate projections – never have been – but it is hardly a new or unfamiliar tool).

So when you published an OCR track that is revised up and out

you know the likely reaction, likely questions etc. And when you complement that numerical track by explicitly stating that the MPC actively considered raising the OCR at this very meeting, you shouldn’t be surprised you are going to be challenged. On a central track, where the OCR is averaging 5.65 per cent in the December quarter, that is consistent with a high probability of an OCR increase later this year.

If the Bank didn’t want people to take that interpretation (and both Conway’s comments in this article, and his and Orr’s comments at the press conference suggest they didn’t), they should have published different numbers. The comments from Conway in the Post article suggest that somehow the OCR projection track was outside their control – product of “its modelling tool” – when it has always been clear that the projections are the MPC’s, not some staff model (which itself has considerable human interventions pretty routinely). Perhaps it is different now, but in the many many years when I sat on the equivalent of the MPC, we used to spending huge amounts of time (arguably at times inordinate) on those last tweaks to the interest rate track, bearing in mind how any numbers would be read by outsiders. There was never a time when any published forecasts – and particularly for the interest rate track – were just some sort of machine-generated product.

Listening to the press conference for the first time in a while just confirmed a sense of how inadequate the MPC, and its chair, are for the job they’ve been charged with. They didn’t have a straight story to tell, and they were trying to back away from the clear implication of numbers they’d chosen to publish. To which one could add yet another appearance saying nothing of substance from the deputy chief executive responsible for macroeconomics and monetary policy at the Bank, or a Governor who chose to opine on productivity growth or the lack of it, suggesting that things were different (better) in Australia, even though recent productivity growth there has been just as weak as in New Zealand. Why are these people – having delivered us the inflationary mess in the first place – still in office? New Zealanders deserve better from officials – supposedly expert ones – delegated so much power. Apart from anything else they deserve real expertise and real accountability.

But then there was also a sense of how weak the media scrutiny was. Was it really the case that no journalist had wondered quite how economic growth was supposed to rebound, on these projections, with real interest rates already restrictive and set to rise further, fiscal policy restrictive, no help from the world economy, and with an expected further downturn in the net immigration impulse? In any case, none asked. None asked why if the OCR had helped lower the output gap by almost 5 percentage points so far, a continuing high OCR, rising further in real terms (as inflation and expectations fall but the OCR doesn’t), was only going to lower the output gap by a little more than 1 percentage point.

And remarkably no journalist asked, and no central banker mentioned, the very real lags in monetary policy. If the real OCR keeps rising to at least the middle of next year, won’t that be acting as a material drag on economic activity and inflation for a couple of years after that? And yet, on the Bank’s projections – the ones the Governor was presenting and journalists were supposedly questioning – quarterly inflation is back at target midpoint by the middle of next year, and – on the Bank’s telling – goes no lower from there.

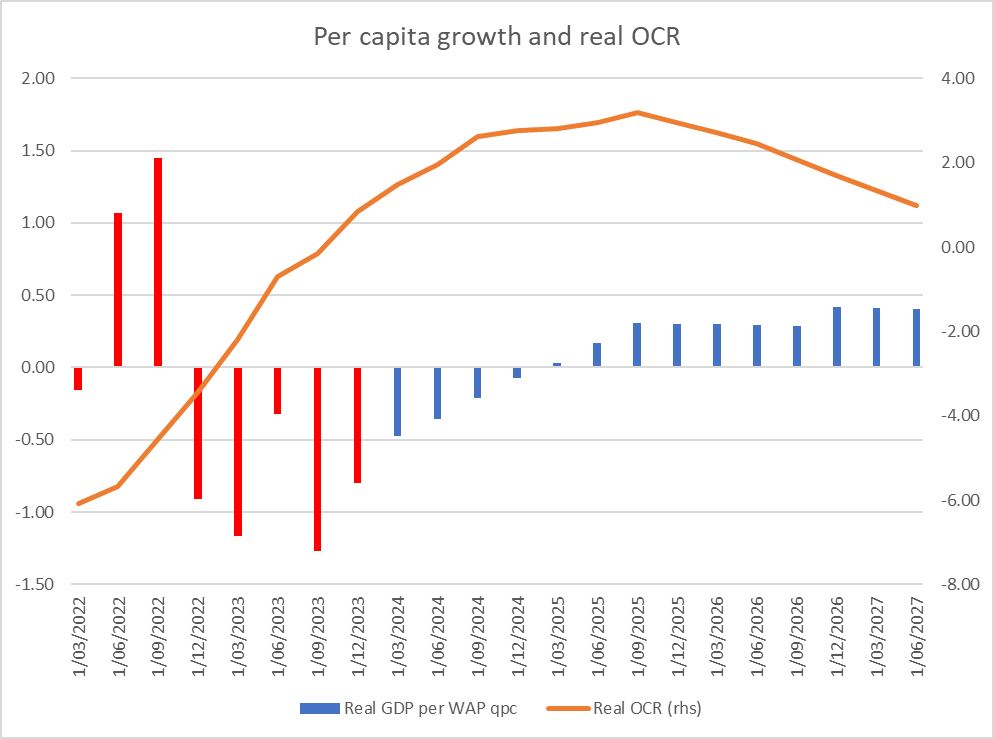

After my post yesterday I had a few people get in touch, spanning the positions from what one might call extremely dovish to extremely hawkish. My key chart in that post was this one.

Pretty much any way one looked at real interest rates they (a) had been rising, and (b) on the Bank’s forecasts were set to continue to rise for another year or more, and yet – on those same forecasts – growth was set to return. It might not look like spectacular per capita growth next year, but on these numbers we are set to get back to slightly above average (for the pre-Covid decade) per capita growth before there have been any OCR cuts at all (in a period when fiscal policy is likely to be contractionary and the migration boost to demand and activity is expected to shrink). It was, and is, a puzzle.

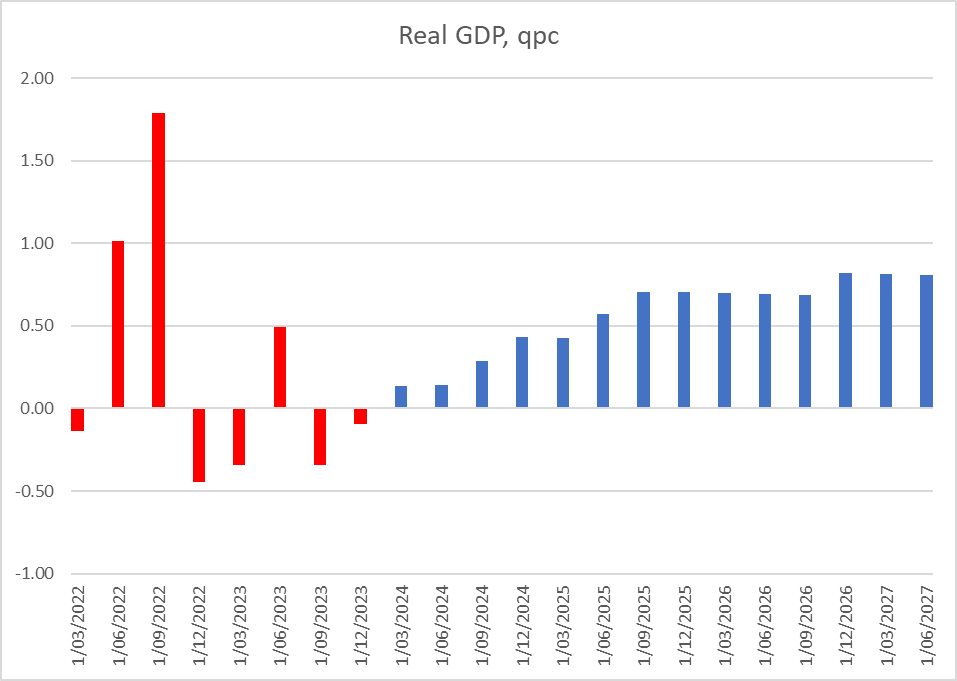

One person objected to the use of per capita measures of GDP. As it happens, the pattern looks much the same, just a bit less marked, if one uses headline changes in real GDP. We go from an average quarterly contraction over the last five published quarters of -0.15% to quarterly growth of about 0.7% even as real interest rates rise and before the first OCR cut occurs in August next year.

The objection to using per capita numbers reflected a view – that some international agencies seem to like (the then chief economist of the OECD tried it out here a few years ago) – that it was almost inevitable that immigration surges would initially dampen GDP per capita, which would then recover over time as the migrants were absorbed. Perhaps there is something to this sort of model where many migrants are irregular or refugees, but this is New Zealand, where most migrants arrive on pre-approved work visas. Refugee numbers here are small, and illegal arrivals (as distinct from people overstaying visas) smaller still.

The New Zealand experience, over many decades, has tended to be that immigration shocks add more to demand (including derived demand for labour) than to supply in the short-run. And the experience of the last couple of years doesn’t seem inconsistent with that. There was a big unexpected influx, and yet there was no temporary dip in the ratio of employment to working age population: as it happened the absolute peak in the employment rate was in the same quarter as the estimated net migration peak (note that the Reserve Bank’s output gap estimate in fact peaked a few quarters earlier).

So I’m sticking with there being a puzzle. Where is this growth rebound supposed to be coming from, as monetary conditions tighten, fiscal policy tightens, net migration falls (further) and the world economy is assumed to jog along much as it has been?

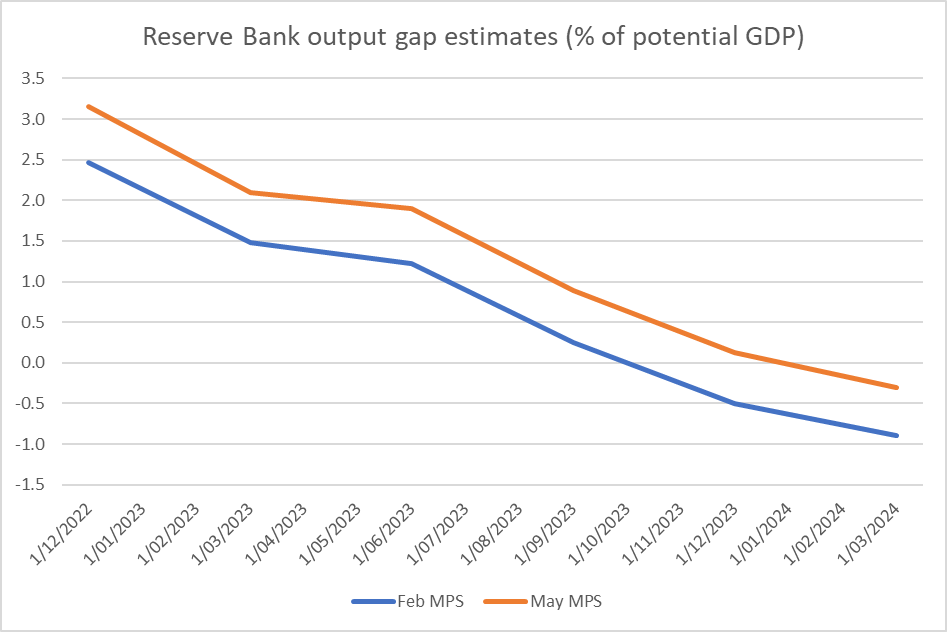

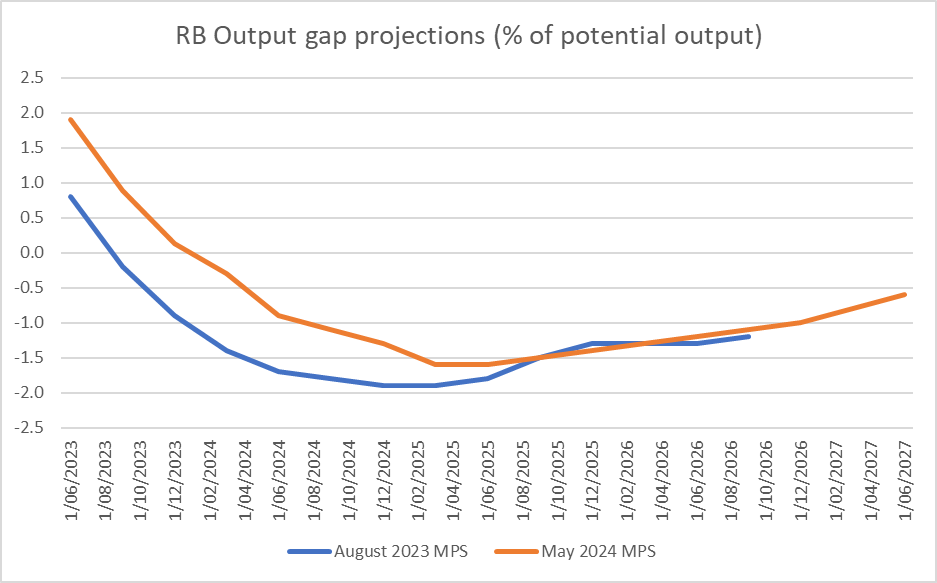

But the real prompt for another post was looking at the output gap estimates themselves. In this week’s MPS there has been quite a big revision to the Bank’s estimates of the output gap (for the most recent estimated quarter, March 2024) and through all last year. On these numbers, only in the March quarter does the Reserve Bank think the economy crossed over to having (very slightly) excess capacity.

One could argue that it is consistent with their (prior) view that inflation has become more problematic than they realised, and harder to get down. One might also argue that perhaps the latest estimate lines up with the latest unemployment rate which, at 4.3 per cent, is probably around economists’ estimates of the NAIRU. Correct or not, a few more deeply negative GDP per capita quarters would quickly take the output gap deeply negative (monetary policy – and any other influences – has already taken the output gap down by 3 full percentage points of GDP in just 18 months.

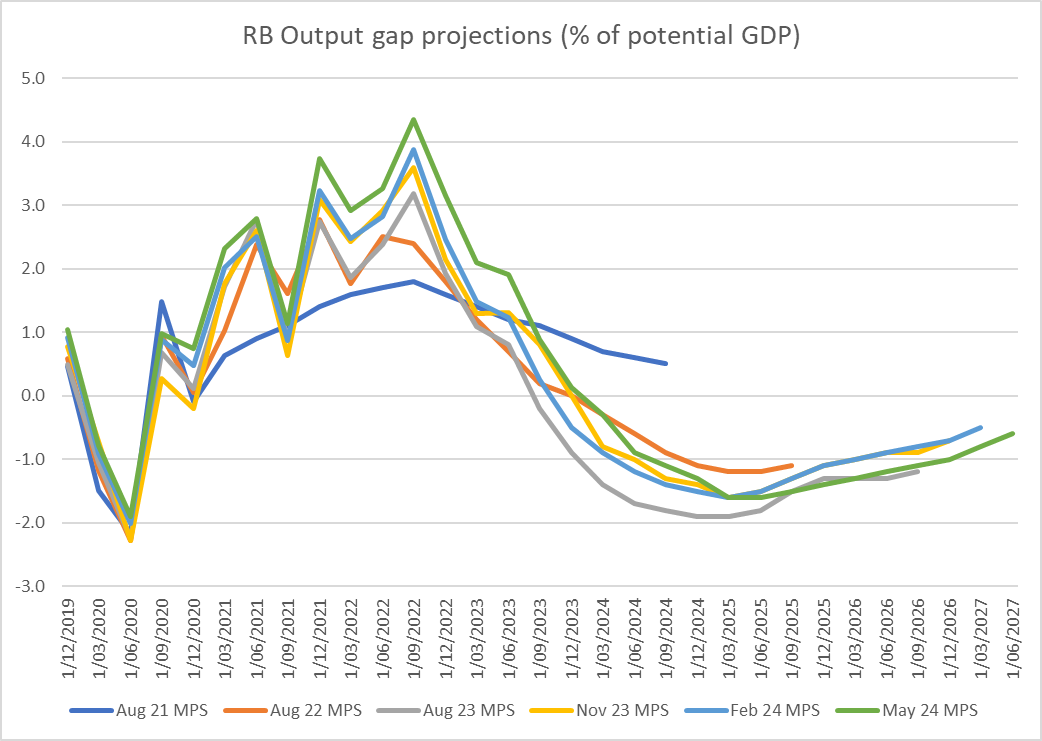

But my interest is more in what the Reserve Bank’s revisions are now saying about just how overheated the New Zealand economy actually got in 2022. Here is a chart of the Bank’s output gap estimates over time.

As late as (say) August 2022 they thought the excess demand had peaked in late 2021 at under 3 per cent of GDP (large enough by any historical standards). Now, after successive revisions, not only is the (estimated) peak much later (September quarter of 2022) but it is much larger (4.3 per cent of GDP). All the quarters either side of that peak have also been revised up quite materially.

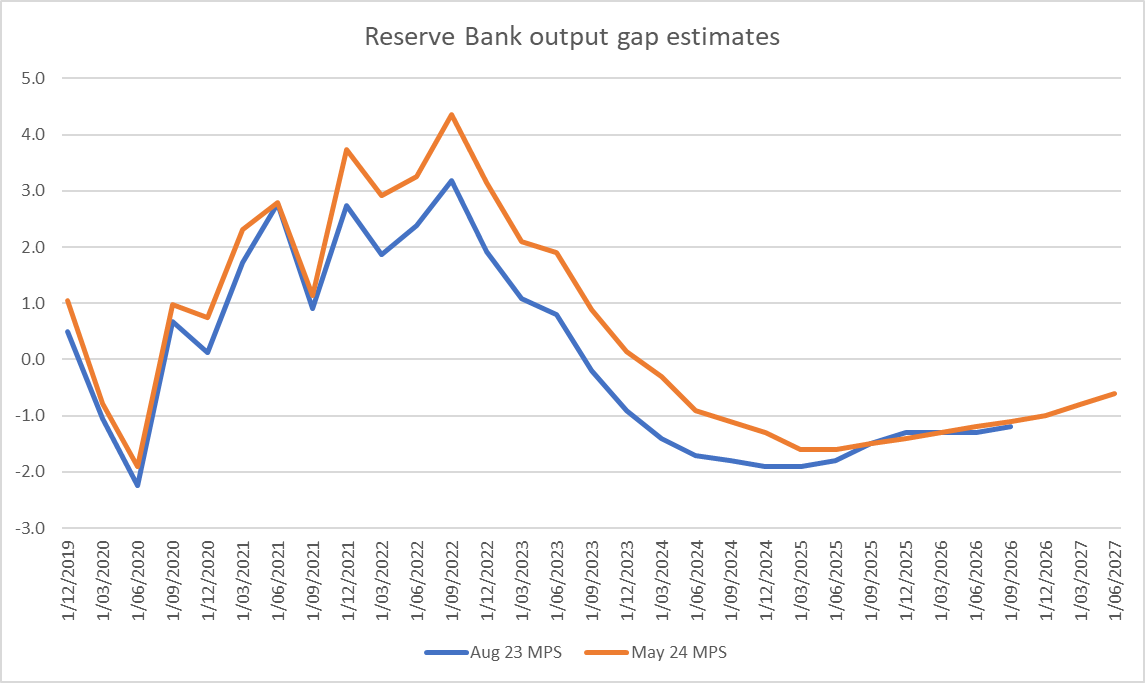

So big revisions upwards. But how do those estimates now compare with history? This is a chart of the Bank’s current output gap estimates this century

The economy was overheating in the mid 00s, and core inflation got a bit above 3 per cent. But it was nothing like as serious as the (now) estimated overheating in 2021 and 2022. And this was what the Bank simply totally failed to recognise for far too long (recall it was not until February 2022 that the OCR had even been raised back to the level it was just prior to Covid). Even now it is revising up its view of the extent of its own misjudgement and resulting policy mistakes. It was by far the biggest monetary policy mistake in the 34 years of Reserve Bank operational autonomy…..and no one seems to have paid any price at all (Governor and MPC members were all reappointed).

18 months or so ago the Bank came out with a review of its own performance, which unsurprisingly wasn’t very critical at all. Yes, we were told, it was clear with the benefit of hindsight they should have started tightening earlier, but it might only have been by a quarter and wouldn’t really have made much difference to outcomes. It was implausible even at the time – failing to grapple with the severity of the misread of the economy and associated capacity pressures. It has become literally incredible as time has gone on. Did others make similar misjudgements? Of course. But others weren’t delegated the power to run monetary policy, and the responsibility to get it right. No one forced them to take the job, purportedly delegated to people of real expertise.

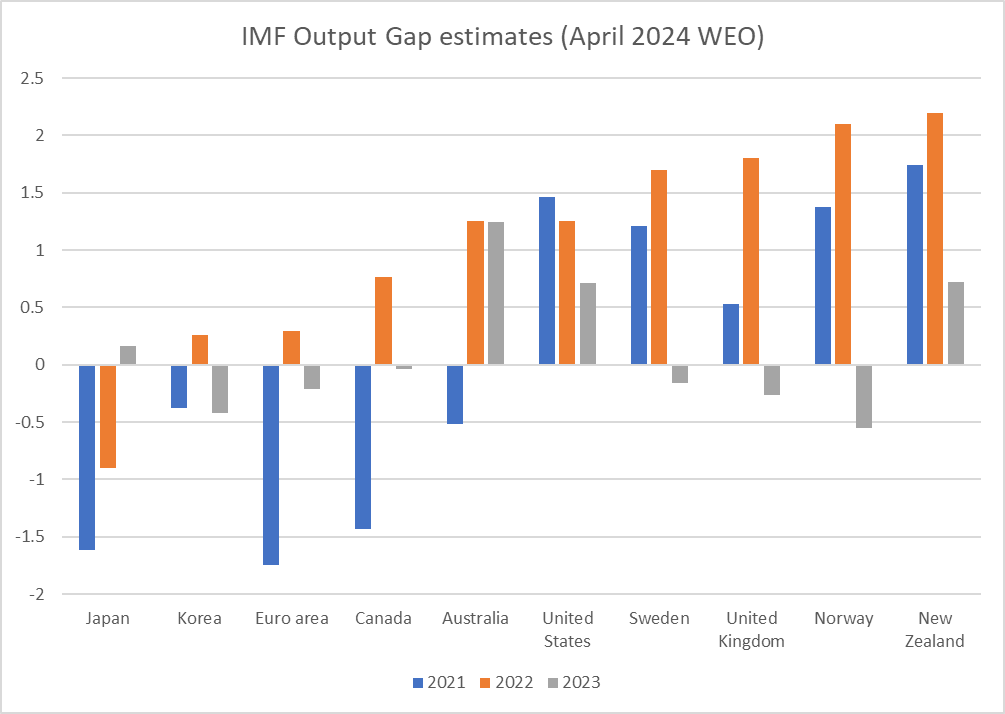

A common response is some mix of claims that (a) other central banks were just as bad, and b) the Reserve Bank of New Zealand was relatively early in starting tightening. Even if the first claim were correct, it is no excuse: central bankers abroad also voluntarily accepted a mandate and failed to deliver. But it also isn’t really true. It is hard to get consistent output gap estimates across time and across countries, but the IMF is one source

On their current estimates – presumably different techniques to the RBNZ’s estimates – in both 2021 and 2022 New Zealand had the largest positive output gap of any of the advanced economies for which the IMF produces numbers. Imbalances of that extent occur because our Reserve Bank got it (rather badly) wrong, acting late and (for too long) sluggishly relative to the inflation pressures in our own economy (and even among this group of countries, the RBNZ was only the 3rd to start tightening; among OECD central banks it was 7th).

But accountability doesn’t appear to be something that mattered either to the previous government (concerned perhaps that suggesting the Bank had done poorly would reflect poorly on them who appointed the MPC) or to the current one (which tends to play down any role for the Bank, presumably to tar Labour with the blame for the high inflation, while claiming the credit for themselves when inflation settles down again).

And just one final (puzzling) chart. I noticed a few quarters ago (last August) that the Bank’s then output gap projections had about as much space above the zero line as below (probably a bit more below as it still hadn’t got back to zero by the end of the projection period). But this time – and it has been transitioning towards this over the last couple of MPSs – and focusing on the orange line (this week’s estimates), there is far more space above the zero line than there is below. In other words, on these numbers, we got to enjoy the excess output but don’t pay any sort of equivalent or commensurate price in lost output.

It doesn’t make a lot of sense (and would be something very different than we saw in the previous cycle, after 2008). Perhaps there really wasn’t quite as much excess demand at peak as they now think? Perhaps more pain (lost output relative to potential) will be required than they are saying (which might well come about quite easily if the implausible growth rebound they are projecting just doesn’t occur over the next few quarters).

I’m really not sure what is going on. But it doesn’t leave one with any more confidence that the Bank knows what it is doing than we can have now about how they handled the period from mid 2020 to mid 2022, which delivered us this persistently high inflation – and attendant arbitrary wealth redistributions – in the first place.

The Reserve Bank doesn’t do independent fiscal forecasts so there is no news in the fiscal numbers in today’s Monetary Policy Statement themselves. The last official Treasury forecasts don’t take account of whatever the government is planning in next week’s Budget, and as the Bank notes they will need to update their assessment in light of whatever the spending and tax plans prove to be.

So I was more interested in the Bank’s numbers for the things they do forecast independently, and which in turn have implications for both the tax revenue the government could expect to collect on any given set of tax rates and for the likely expenditure pressures (from things like population growth and inflation).

One of the lines the Minister of Finance has repeatedly sought to use over her time in office is something about how much worse the economy was than they had appreciated (or had been clear) pre-election, to soften us up (it appeared) for yet more delay in getting back to fiscal surplus (see, we can’t really help it, it was done to us, and no one told us). It has always been an unsatisfactory argument (to say the least) since the previous projections (say, those in the PREFU and those in National’s fiscal plan) weren’t for a return to surplus for a couple more years anyway (2026/27) and by then whatever the forecast fiscal outcome, it is purely a matter of policy choice.

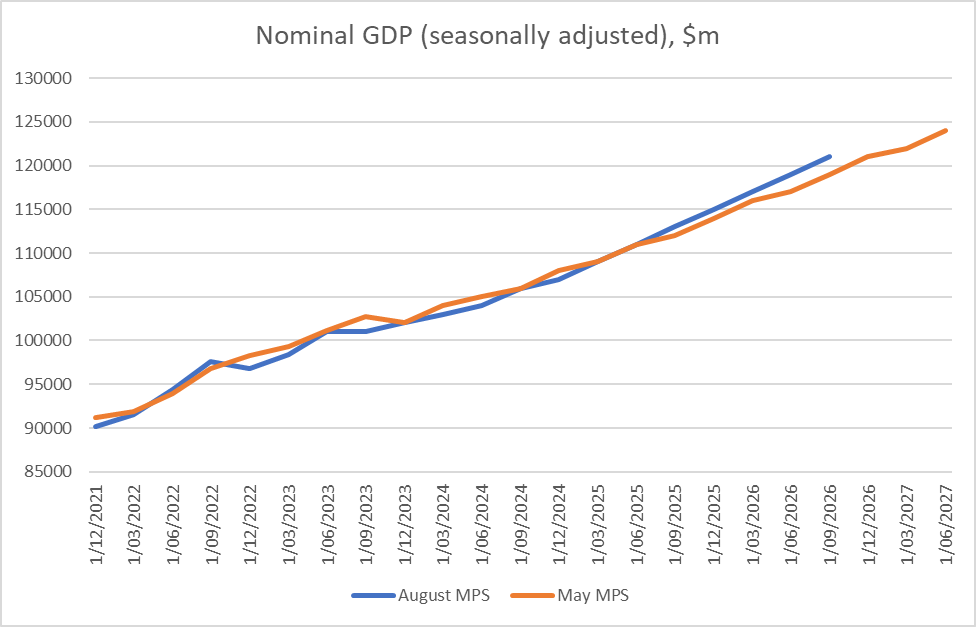

Now, the Budget numbers out next week will use The Treasury’s forecasts as their base. But here are the nominal GDP projections the Reserve Bank was making (a) at the August 2023 Monetary Policy Statement (ie the last set of forecasts pre-election), and b) today. Nominal activity is what gets taxed.

There is a slightly larger gap opening up a couple of years out (when, of course, who knows; both sets of numbers are just anyone’s guess out there) but as late as the June quarter next year the two observations are exactly the same, as they are (a 0.1% difference) for the last pre-PREFU quarter, 2023Q2.

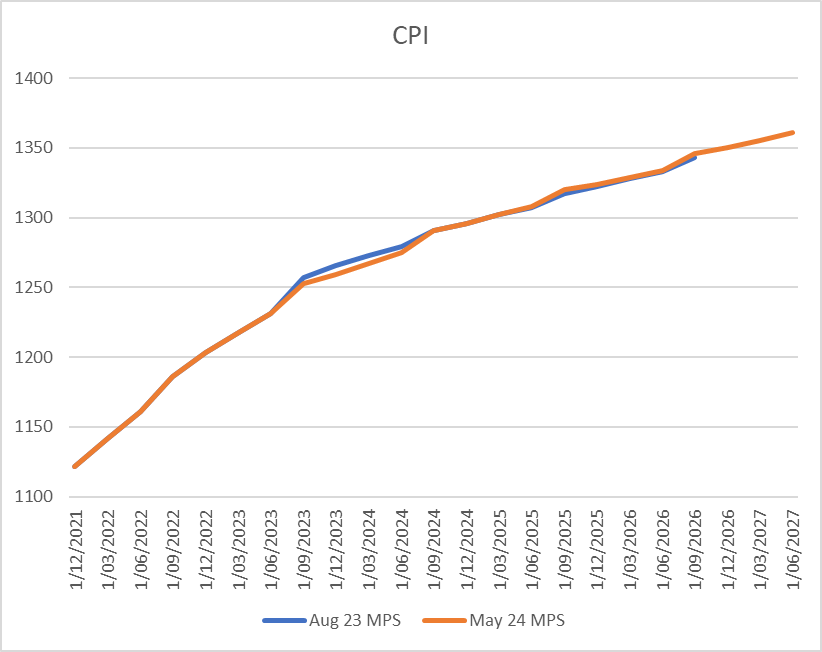

Ah, perhaps you are thinking, but what about inflation. If there is more inflation than was previously forecast the revenue just won’t go as far.

But there isn’t anything much in that sort of story either.

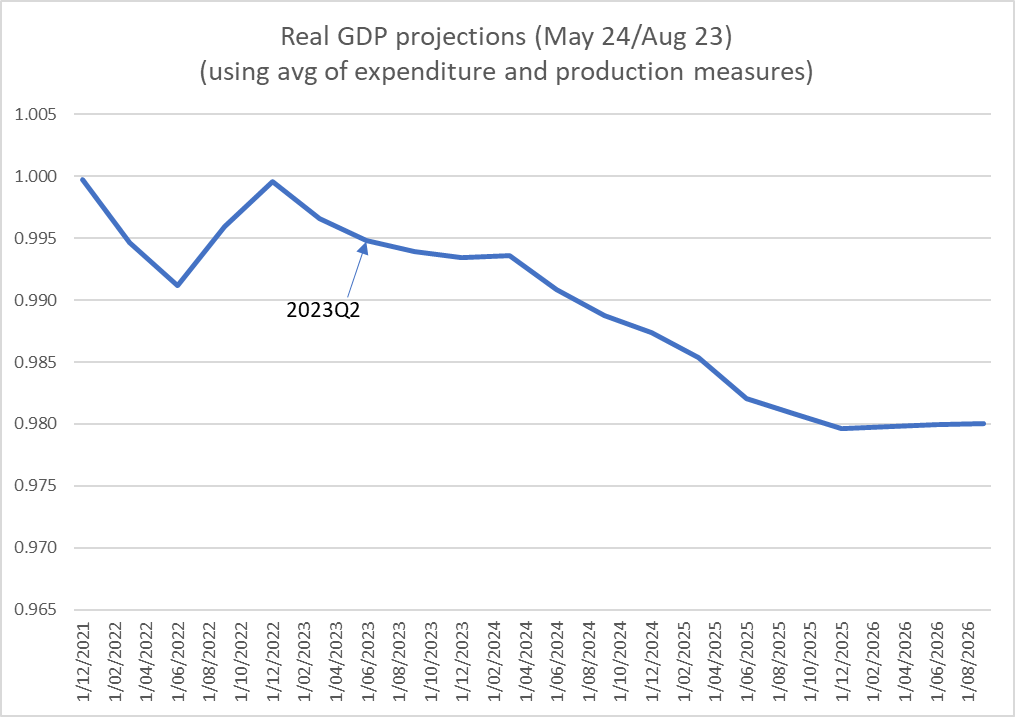

There were some historical revisions late last year to the estimated level of real GDP. Those revisions don’t have any material implications for anything much, since life had already been lived through that period, and (in any case) it is nominal GDP that more closely approximates the tax base.

But in this chart I’ve shown the ratio of the RB’s latest forecasts for real GDP to those it did last August, and it is certainly true that over the full forecast period the latest forecasts are a couple of per cent weaker than last August’s forecasts.

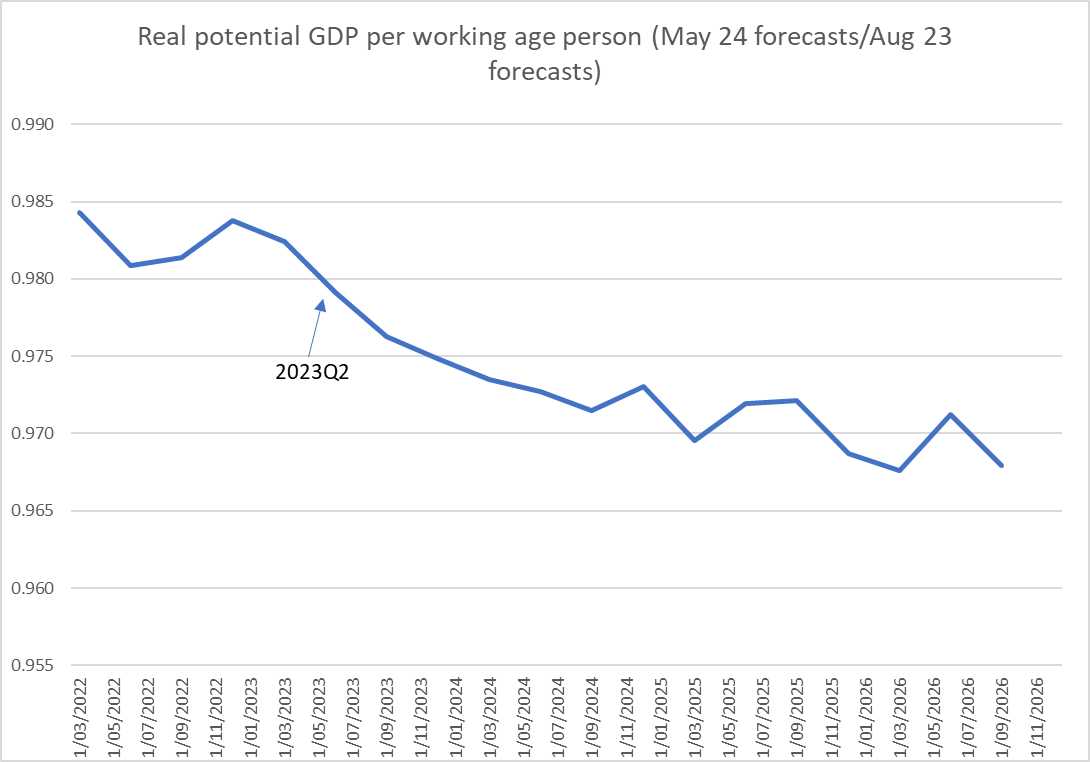

Here is a slightly more obscure chart: the same sort of ratio but this time for the Bank’s estimates of real potential GDP per working age population. Things worsen there by about 1 per cent relative to the position thought to have prevailed just prior to the election.

And if weaker GDP per person implies some loss of productivity (some things the government might be purchasing won’t be getting relatively cheaper), it also suggests that (eg) public service wage pressures and NZS adjustments should be less than they might otherwise be.

The key point? At least on the Reserve Bank’s telling – and they could of course have a very different view than the Treasury – there just isn’t that much there. We are set to be less well-off per person than the Bank thought just prior to the election, but nominal GDP and the CPI forecasts have barely changed, and even the real output changes aren’t particularly large in the scheme of things (nothing at all like the extent of the revisions that followed in the wake of the 2008 recession). What we have, on the Bank’s numbers, is a recession and a protracted period of excess capacity (slack) that is not quite as deep, but quite as protracted, as the Bank suggested to any and all readers (Opposition politicians included) just prior to the election.

Almost all government agencies are in cost-cutting mode at present, under instructions from the incoming government. All sorts of things they, or the previous government, thought were nice to have and some things perhaps they thought were really rather useful indeed seem to be going by the wayside.

But at the Reserve Bank they are planning a new nice-to-have.

The Bank has a consultation process open at present on a proposal to “invest in” (that is public sector for “spend”) a new survey of business people, asking about their specific numerical expectations for a subset of macroeconomic variables. What is striking, in this climate of general public sector austerity, is the utter absence of any analysis of what gaps this survey is designed to fill and how material they might be for monetary policymakers. That was one thing in the era of bloat and lavish increases in public spending – in which the Bank fully participated over the last few years – but it really shouldn’t be acceptable at present.

On the substance, I’m sceptical of asking specific numerical questions to a wide range of businesses about specific macroeconomic variables (up, down, or the same questions just might be useful) and of whether there are really information gaps at all. I put in a fairly short submission, as follows:

Submission to the Reserve Bank on proposed Business Expectations Survey

Michael Reddell

23 March 2024

This is my personal submission in response to the Reserve Bank’s consultation document on the proposed Business Expectations Survey. I have been a long-term user of business and household surveys, was involved in various refinement to the existing (and now) expert survey of expectations the Bank runs, and was a user of such material for several decades as a senior monetary policy adviser in the (former) OCR Advisory Group. I am now also a monetary policymaker in another country, so am very much attuned to the perspectives and interests of policymakers.

There appears to be no prior background document referred to, so I am working on the assumption that the current document is all the information/analysis that the Bank is choosing to provide.

On that basis, it is quite astonishing that there is no analysis of the case for (or against) a survey of the sort the Reserve Bank proposes to spend additional public money on. As you will be well aware, there is a plethora of surveys in existence (which wasn’t the case several decades ago), including the monthly ANZBO, the monthly BNZ PMI and PSI, the quarterly QSBO, and of course the Bank’s own survey of (now) expert expectations – to name just the more-prominent of the business surveys. The Bank used to be a large funder of the QSBO, and I assume that that is still the case (and I used to, and would still, champion the case for some slight extensions to the QSBO, notably around wages).

The survey you propose is of a subset of macroeconomic variables. You will no doubt be aware that the existing Survey of Expectations began with a much larger range of respondents, including business and union people, and was eventually slimmed down towards its current form in part as it was realised that many of the business respondents had no particular reason to have formed specific expectations for many macroeconomic variables, or even in some case to be aware of the specific measures being asked about. I am aware, of course, that your current proposal is for a more-limited subset of questions, and in the case of near-term inflation it is a fairly commonly asked question even of households. But do you really believe that many business respondents are likely to have well-developed thoughts on what the inflation rate might be in 10 years’ time (or even that they have risen or need to have even implicit views given that very few nominal contracts exist)? Similarly, how many of your respondents will be familiar with the details of the specific wage series you ask about, or will recognise a difference between annual GDP growth and annual average GDP growth (let alone know the numbers).

It is much more common for surveys of the wider business community to use tendency questions and focus reporting on net balance results. Absent any compelling analysis or evidence from abroad, I’d have thought that was likely to be a much better way to go, if you really believe there is value to the MPC in yet another business survey (typical targeted respondents seem much more likely to have some sense as to whether growth or wage inflation might speed up or slow down over the period ahead than to have meaningful numerical expectations. In respect of labour market slack existing questions in other survey (“difficulty of finding labour”) seem to cover the ground these sorts of respondents could typically generally offer (few will, by contrast, have particular to care what the specific HLFS definition of unemployment is).

But, more generally, where is the evidence of gaps in the (survey) data that the MPC needs to make good monetary policy? This is posed as a serious question. I’m not aware of such gaps, but perhaps you are and could have elaborated on this point for submitters. Material monetary policy mistakes have (and no doubt will again, in the nature of imperfect individuals and institutions) be made, but is there really any evidence that it is (a subset of) business expectations of macroeconomic variables that is lacking, or which led the MPC astray in the last few year? I’d be surprised, but am certainly open to evidence.

It was perhaps surprising that there was no indication in the consultation document of the cost of (a) developing and (b) administering the proposed survey, which makes it even more difficult to assess whether it is plausible that there will be net benefit for taxpayers (as ultimate funders of the Bank).

On a couple of specific items in your document:

It was rather surprising to see several references to “respondent burden”, including to justify leaving out very small businesses from the possible sample base. It is a highly relevant consideration when the state uses the coercive powers SNZ in particular has to insist on private firms and citizens completing surveys, but as you note this proposed survey will be quite as voluntary as any of the other business surveys, and it isn’t obvious that – to the extent you are likely to get any useful data from this survey – businesses with 5 employees will have anything less to offer than those with (say) 15, again bearing in mind that it is macroeconomic variables you are asking about. Moreover, since you propose to revolve the panel, no one potential respondent would be asked for response all that often or for that long. More generally, I note the very low response rate you expect (“10-20%”) and given the severe selection bias that probably introduces one is again left wondering about the strength of the case for the survey at all.

I’m also unpersuaded by the (very sketchy) case made for the exclusion of primary industry firms. It might be common to exclude such firms, but (as you recognise) this is an economy in which the primary sector is of some considerable importance, and (again) these are macroeconomic questions you are proposing to ask, and it isn’t obvious why primary industry respondents would be any less equipped to answer such questions than other firms their size. I note that you say that primary industry firms are not generally price-setters, but it is a galaxy of macro questions you are proposing to ask, not ones about price-setting intentions (and primary sector firms employ, borrow, fx hedge (or not), and so on).

Finally, and while I recognise that the Reserve Bank’s current funding agreement does not run out until next year, in the current climate in which government agencies pretty much across the board are being expected to exercise considerable spending restraint, often cutting established functions and activities, it seems extraordinary (but consistent with a longstanding culture of Reserve Bank exceptionalism – and yes, I used to share and even champion it) for the Bank to be proposing a new ongoing spending commitment on what is, at best, a nice-to-have, supported by no serious underlying analysis of the need for this new survey, or even of the Bank’s ability to continue to fund it (against other priority claims) if and when the Minister of Finance finally catches up with the Bank and adjusts its authorised spending levels.

A while ago I stumbled on the report of Kristy McDonald QC, dated 22 February 2022, which had been commissioned by Hon David Clark, then Minister of Commerce, into aspects of the appointment of the default Kiwisaver providers, and specifically around the handling of conflicts of interest involving the then chief executive of the Financial Markets Authority (FMA) whose brother-in-law was the chief executive of one of the providers. The FMA provided a strictly limited bit of advice to the Minister.

I was less interested in the specifics of the case - which didn’t reflect very well on the FMA or its board/chair, but was (from the report) hardly the worst thing in the world - than in Ms McDonald’s observations on conflicts of interest. This is probably the most useful excerpt from her report (the document mentioned in italics is from the Public Service Commission).

There is a heavy emphasis on three things really. First, avoiding actual conflicts of interest. Second, ensuring that outside (“fair minded”) observers can be confident that decisions have not been improperly influenced. And, third, documentation, documentation, documentation (which helps demonstrate, at the time and if necessary later, that actual and apparent conflicts have been recognised and dealt with appropriately). As McDonald notes in 6.22 you’d think considerations like these should be particularly important in a regulatory agency, especially one - such as the FMA - with regulatory responsibilities in the financial sector. This is from the very top of the front page of the FMA’s website

You’d really have hoped that the Financial Markets Authority would have gone above and beyond in setting and applying standards for its own people, But…..no. You might remember them banging on a few years ago about “culture and conduct” in the private financial sector. I guess those were aspirations for other people. One hopes that, in the light of the McDonald report, the FMA has now lifted its game in handling such issues in its own organisation. One might hope…..

One of the classes of financial product/entity that the FMA has regulatory responsibility for is superannuation schemes. It has particular responsibility now for a class of so-called “restricted” schemes, closed off to new members and generally in multi-decade run-off. One of the FMA’s predecessor entities was the office of the Government Actuary which had in times past been required to consent to any changes in superannuation scheme rules. In old-style defined benefit superannuation schemes - a form of deferred remuneration where the effects (contributions/entitlements), even for an individual, stretch over decades – those sorts of protection and oversights, whether embedded in statute law or in the deeds of schemes are vitally important. Such schemes are typically established as trust structures in which all trustees are required to undertake their duties with the best interests of members in mind. Being a trustee is, or should be, no small thing, not a duty entered upon lightly.

Conflicts of interest can, at times, be a significant issue. In a typical employer-sponsored superannuation scheme some of the trustees will be elected by members and some will be appointed by the employer. These days - in what is mostly regulatory impost (thank you Key government) – schemes are also required to have a Licensed Independent Trustee. (There were hazy warm thoughts at the time that these might be courageous independent thinkers who’d be a force for good, but the model really seems built more to encourage box-ticking – there are lots of boxes to tick – establishment figures earning a bit of pre-retirement income: you aren’t likely to be appointed to such roles if there is any fear you might rock the boat.)

In a scheme that defers for decades employee remuneration there can be material tensions between the interests of the employer and the members. But much of the time there aren’t such conflicts. The day-to-day responsibility is to ensure that the pensions are calculated correctly and paid reliably, that member queries are dealt with in an appropriate and timely way, that statutory reporting and compliance requirements are met, and that money is collected properly and invested prudently. I’ve been a trustee of the Reserve Bank scheme for 15 years and those issues go by pretty harmoniously, with any differences of view rarely falling along Bank-appointed vs member-elected trustee lines. And if the rules are clear and discretion strictly limited the room for seriously conflicting interests is minimised.

But the differences come to the fore when there is any consideration of material changes to the rules or the status of the scheme. Things are especially problematic if employer-appointed trustees form a majority. That is why, for example, it is common to require regulator consent to change rules and to include protections such that member consent is required from any members who might be made worse off by a rule change (to which they might still consent if, for example, one adverse rule change was balanced by other changes the member considered was to their benefit).

And here the situation is supposed to be pretty clear. A member-elected trustee is not generally regarded as intrinsically conflicted simply by virtue of being a member (since the entire purpose of the trust is to benefit members, whose interests all trustees are supposed to advance). A member-elected trustee can, of course, be specifically conflicted and should then recuse themselves (as an example, it turned out some years after I left the Bank that my retirement benefits from the pension scheme had been materially miscalculated. I stood aside for any deliberations on that matter). But the situation of employer-appointed trustees is generally regarded as different: often they will be senior managers or Board members of the sponsoring employer and the potential conflicts between the interest of the employing firm and that of the trust (and its beneficiaries) can be all too evident.

There is very little regulator guidance on these issues in New Zealand - perhaps not surprising when the FMA hadn’t really handled its own well - but shortly after I became a trustee I found a lengthy guidance note from the UK Pensions Regulator, which I have since regarded as something of a guidepost (it is still current). It is a different country to be sure, but with broadly similar culture, a large DB pension sector, and much of the case law that gets cited here comes from the UK. In any case, the question here is not what is lawful, but what is proper (substantively and in terms of perceptions and appearances).

You might remember that the whole “culture and conduct” tub-thumping exercise a few years back was done jointly with the Reserve Bank. You’d have thought that the Reserve Bank might be some sort of exemplar of good conduct, and concerned to be seen as such. I guess you might have thought that of the FMA too. More fool us.

For the last decade the trustees of the Reserve Bank pension scheme have been grappling with arguments and evidence around claims that several significant deed amendments done in the white heat of the reform era (late 80s, early 90s) were not lawfully made and are thus invalid. No one really quite knows what the implications would be if these changes were to be held to be invalid, but it would be unlikely to be good for the Reserve Bank (either reputationally or financially). It would, I think, generally be conceded now that the rule changes were, to say the very least, not handled well by former trustees and management (eminent figures such as Sir Spencer Russell, Don Brash, Suzanne Snively, but also able members’ trustees). In fact, Don Brash himself has raised specific concerns with trustees regarding events on his watch - and trustees simply refused to ever meet him.

Three of the six trustees are appointed by the Board of the Reserve Bank from among directors or staff members (a fourth – the LIT – is chosen by other trustees but long ago declared he never wanted to come between member and employer interests). Those Bank-appointed members can be replaced at will for any reason or none. Over the decade they have included a Governor, a Deputy Governor, a deputy chief executive, a couple of Board members, and a long-serving relatively junior staffer. As we have dealt with the issues over ten years there has never been any sign of these appointees putting member interests first. It is not that nothing has happened - some serious mistakes have been acknowledged and or fixed – but only things that are not awkward or potentially costly for the Bank. It is, of course, impossible to know whether these trustees have actually prioritised Bank interests, but it is impossible to tell apart their actual approach from the sort of approach that would be predicted were Bank interests to be prioritised. Nothing has ever been done to acknowledge the serious conflicts of interest or to document how those conflicts are being managed or dealt with (and the Bank trustees have consistently refused suggestions of either using an arbitrator or approaching the courts for (definitive) guidance and resolution).

Tomorrow morning in Wellington there is a meeting of the members of the Reserve Bank scheme, called by a group of members (including two former senior Reserve Bank managers) under the provisions of the Financial Markets Conduct Act. The members say that they want to seek explanations for the thinking behind various decisions the trustees have made (usually by majority). Rather than engage, it appears that the intention of the Bank-appointed majority is to stonewall. The current chair – one of Adrian Orr’s many deputies - appears more interested in pursuing me for openly articulating my dissent and criticisms of trustee processes and advice than in engaging with members or getting to grips with the substance of the issues. And - par for the course – never seems to recognise any sort of conflict.

I’ve put as much emphasis on atrociously poor processes (in one part of the decade I was moved to describe what was going on as a “corrupt process”, words today’s trustee wanted excised from the version of minutes provided to members for tomorrow’s meeting). But the process problems go back to the start.