I’ve already written a bit about Labour proposals on monetary policy (here and here) and, for now at least, I don’t want to write anything more about the proposed changes to the decision-making process or the plan to require the Monetary Policy Committee to publish its minutes. If there are all sorts of issues around the details of how, I haven’t seen anyone objecting to the notion of moving from a single decisionmaker model to a a legislated committee, or objecting to proposals to enhance the transparency of the Bank’s monetary policy. The Bank was once a leader in some aspects of monetary policy transparency, but is now much more of a laggard.

Where there has been more sceptical comment is around Labour’s proposal to add full employment to the statutory monetary policy objective. At present, section 8 of the Reserve Bank Act reads as follows:

The primary function of the Bank is to formulate and implement monetary policy directed to the economic objective of achieving and maintaining stability in the general level of prices.

Responding to this aspect of Labour’s announcement hasn’t been made easier by the lack of any specificity: we don’t know (and they may not either) how Labour plans to phrase this statutory amendment. There are some possible formulations that could really be quite damaging. But there are others that would probably make little real difference to monetary policy decisionmaking quarter-to-quarter. Probably each of us would prefer to know in advance what, specifically, Labour plans. But this is politics, and I’m guessing that there is a range of interests Labour feels the need to manage. In that climate, specificity might not serve their pre-election ends. One could get rather precious on this point, but it is worth remembering that there are plenty of other things that may matter at least as much that we currently know little about. Under current legislation, who becomes the Governor of the Reserve Bank matters quite a lot to shorter-term economic outcomes, and we have no idea who that will be. The details of the PTA can matter too, and under the governments of both stripes the process leading up to the signing of new PTAs has been highly secretive (often even after the event). For the moment, we probably just have to be content with the “direction of travel” Labour has outlined.

In some quarters, Labour’s plans for adding a full employment objective have been described as “cosmetic”, as if to describe them thus is to dismiss them. That is probably a mistake. When I went hunting, I found that cosmetics have been around for perhaps 5000 years (rather longer than central banks). People keep spending scarce resources on them for, apparently, good reasons. Why? They can, as it were, accentuate the positive or eliminate the negative – highlighting features the wearer wants to draw attention to, or covering up the unsightly or unwanted marks of ageing. They (apparently) accomplish things for the wearer.

What is the relevance of all this to monetary policy? Well, there has been a long-running discontent with monetary policy in New Zealand, especially (but not exclusively) on the left. In the 28 years since the Act was passed there has not yet been an election in which some reasonably significant party was not campaigning to change either the Act or the PTA. We haven’t seen anything like it in other advanced countries. Personally, I think much of the discontent has been wrongheaded or misplaced – the real medium-term economic performance problems of New Zealand have little or nothing to do with the Reserve Bank – and many of the solutions haven’t been much better (in the 1990s, eg, Labour was campaigning to change the target to a range of -1 to 3 per cent and NZ First wanted to target the inflation rates of our trading partners, whatever they were). But that doesn’t change the fact that there has been discontent – and more than is really desirable.

I’m quite clear that there is no long-run trade-off adverse trade-off between achieving and maintaining a moderate inflation rate (the sorts of inflation rates we’ve targeted since 1990) and unemployment. And since something akin to general price stability generally helps the economy function better (clearer signals, fewer tax distortions etc) there is at least the possibility that maintaining stable price might help keep unemployment a little lower than otherwise. Milton Friedman argued for that possibility.

But I don’t think that is really the issue here.

Because it is not as if there are no other possible connections between monetary policy and unemployment. Pretty much every analyst and policymaker recognises that there can be short-term trade-offs between inflation and unemployment (or excesss capacity more generally – but here I’m focusing on unemployment). Those trade-offs aren’t always stable, even in the short-term, or predictable, but they are there. Thus, getting inflation down in the 1980s and early 1990s involved a sharp, but temporary, increase in the unemployment rate. That was all but inescapable. And when the unemployment rate was extremely low in the years just prior to 2008, that went hand in hand with core inflation rising quite a bit. Monetary policy decisions will typically have unemployment consequences. Unelected technocrats are messing, pretty seriously, with the lives of ordinary people. It is all in a good cause (and I mean that totally seriously with not a hint of irony intended) but the costs, and disruptions, are real – and typically don’t fall on the policymaker (or his/her advisers).

And it isn’t as if monetary policymakers are typically oblivious to the pain. There was plenty of gallows humour around the Reserve Bank in the disinflation years, a reflection of that unease. And yet often the official rhetoric is all about inflation – as if, in some sense, what look like relatively small fluctuations around a relatively low rate of inflation, matter more than lives disrupted by the scourge of unemployment.

So perhaps that is why cosmetics can matter, and serve useful ends even in areas like monetary policy. There isn’t that much difference, on average over time, in how the Reserve Bank of New Zealand, the Reserve Bank of Australia, or the Federal Reserve (or various other inflation targeting advanced country central banks) conduct monetary policy. They each tend to react to incoming data in much the same way (again, on average over time). In the financial markets, they probably each have much the same degree of “credibility” (people think the respective central banks are serious about their stated inflation targets). And yet my impression is that the Federal Reserve, for example, talks much more about unemployment than the Reserve Bank of New Zealand does. The Fed gives the impression that (a) it is aware, and (b) that it cares. In the last decade or so at least, that has been much less so here.

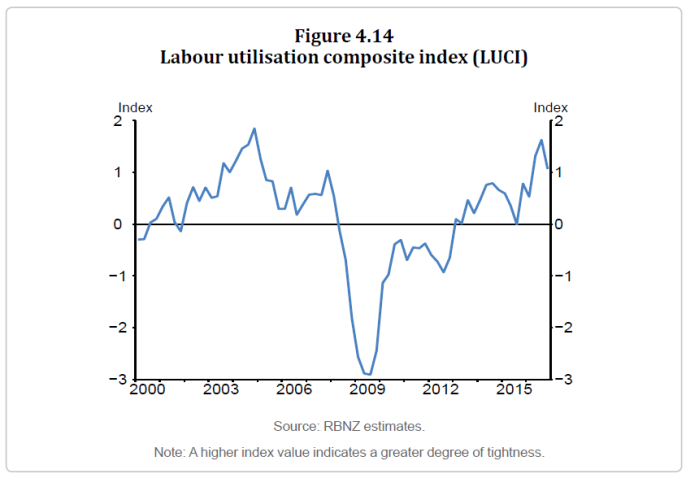

In New Zealand, the problem has been compounded by a sustained period when the Reserve Bank turned out to have run monetary policy too tightly (including two tightening phases that had to be quickly reversed). Over that period – and today – the unemployment rate (the number of people unemployed – the phrase I always used to encourage staff to prefer when we replied to correspondence) has been persistently above estimates of the NAIRU (non-accelerating inflation rate of unemployment).

The Reserve Bank is entrusted with a great deal of discretion, in an area riddled with uncertainty and imprecision. We don’t know exactly what the NAIRU is (nor does the Bank). We don’t even know what “true” core inflation is, let alone what it will be over the 12-24 months ahead, the sort of period today’s monetary policy decisions affect. That makes signalling and symbols perhaps more important than otherwise.

It is also why lines like

“It is mathematically impossible to target two variables with one instrument.”

while formally true, aren’t really the point here. Voters – or some subsets of them – simply want to know that those other things matter – and matter quite a lot – to the people wielding the power. And as there is quite a connection between monetary policy choices and fluctuations in the numbers of people unemployed, they aren’t irrational to do so. After all, they might well note that the old argument – “well if unemployment is too high, inflation will undershoot the target and the Bank will quickly correct that” doesn’t sound so compelling after years of an undershoot, and years when unemployment has lingered quite high.

There is a whole variety of ways to send the signals:

- one can tinker with the PTA again (most of the changes of 28 years have had this quality about them – including for example the current references to unnecessary variability in output, interest and exchange rates),

- one can choose a Governor who is known to care (although typically technocrats won’t be much known at all),

- one could require the Bank to publish estimates of the NAIRU and report regularly on how monetary policy was affecting the gap between actual unemployment and the NAIRU,

- the Bank could regularly write about, or give speeches, highlighting the importance of unemployment (gaps) in its thinking, and expressing discomfort whenever unemployment has to be temporarily high.

Or one could tinker with section 8 of the Act and add a full employment reference.

Perhaps Labour actually has a combination of these sorts of approaches in mind. Amending the Act is isolation might not do much (even in signalling and symbolism) in isolation, but it might encourage the appointment of a Governor who took seriously the concern (after all the Bank’s Board has to operate under the Act), and it might encourage the Governor, the Bank, and any future Monetary Policy Committee to address these issues more directly in their own communications.

And at a political level, if they are serious about prioritising full employment as one over-arching goal of economic policy (which seems a worthy goal to me, even if there are good and bad ways of pursuing it), a change to the Reserve Bank Act might also signal – what the monetary policy analysts already know – that in the medium to longer-term monetary policy and the Reserve Bank are no obstacle to full employment.

As I noted last week, in 1950 the incoming National government amended the Reserve Bank Act to specify an objective for monetary policy as follows

[The Bank] shall do all such things within the limits of its powers as it deems necessary or desirable to promote and safeguard a stable internal price level and the highest degree of production, trade, and employment that can be achieved by monetary action.

Something similar, in today’s language, seems at worst unobjectionable to me. At best, it might strengthen public confidence in the Bank and encourage the Bank and its incoming Governor and Deputy Governor to convey with more conviction how seriously they take the overall economic environment – real firms, real people – within which the Bank exercises its considerable discretionary power.

Reflecting on all this over the weekend, another parallel struck me. In wartime, the priority is to win the war. In many ways it is as simple as that. A single objective. And yet combat generals, delegated power by political leaders, who become known as reckless with the lives of their men eventually forfeit trust, corroding the loyalty of those who serve them (and those who appoint them). Wars involve losses of life, often heavy losses. No general can take on the role without being ready to see young men lose their lives, perhaps in very large numbers. And yet – at least in a free society – we don’t want generals who are indifferent to the cost. We want them to spend lives as if each one were precious. Soldiers who believe that of their generals probably fight with more conviction and determination. And societies give leeway and respect to those generals, allowing them to lead the battles that, in time, win the war. It isn’t a dual objective – in the end societies do what they need to to survive and prevail – but it isn’t irrelevant either.

In both countries the current unemployment rate is around 1.5 to 1.7 percentage points higher than it was in the year or so prior to the global downturn. And neither country was troubled by a domestic financial crisis, nor did they run out of room to use conventional monetary policy. The monetary policy authorities should have been able to do better. If I look across the monetary areas in the OECD (again replacing individual euro area countries with the region as a whole), the only places with a worse record on this score – unemployment rates now compared to the pre-recession levels – are:

In both countries the current unemployment rate is around 1.5 to 1.7 percentage points higher than it was in the year or so prior to the global downturn. And neither country was troubled by a domestic financial crisis, nor did they run out of room to use conventional monetary policy. The monetary policy authorities should have been able to do better. If I look across the monetary areas in the OECD (again replacing individual euro area countries with the region as a whole), the only places with a worse record on this score – unemployment rates now compared to the pre-recession levels – are:

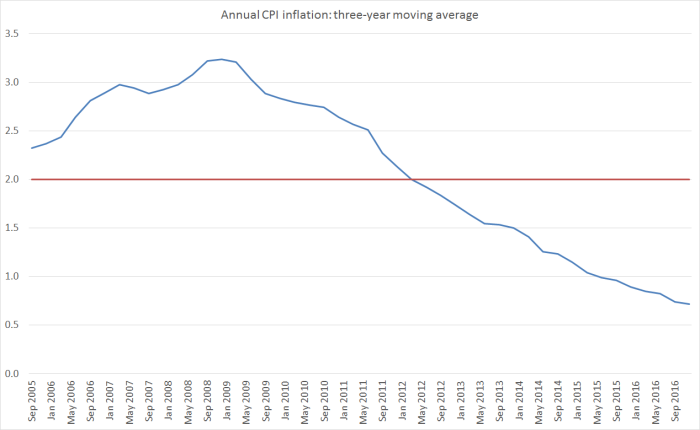

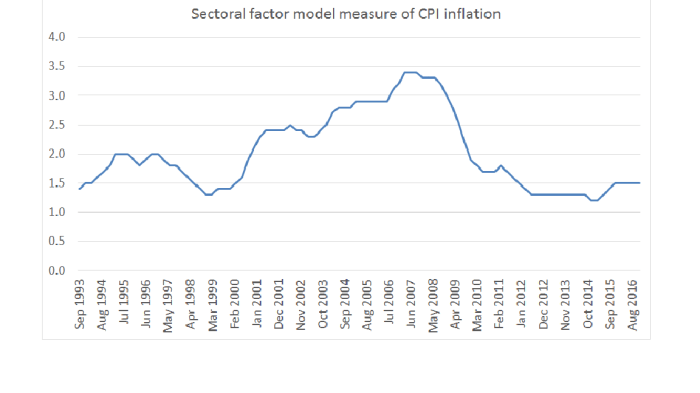

The fact that this measure is not very volatile tends to mean more weight should be put on deviations from the target – they aren’t likely to be simply “noise”. Perhaps the latest estimates will eventually be revised up a little in time, but as it happens the sectoral factor model estimate is now around the median of the whole suite of core measures. The medium-term trend in inflation was probably around 1.5-1.6 per cent late last year.

The fact that this measure is not very volatile tends to mean more weight should be put on deviations from the target – they aren’t likely to be simply “noise”. Perhaps the latest estimates will eventually be revised up a little in time, but as it happens the sectoral factor model estimate is now around the median of the whole suite of core measures. The medium-term trend in inflation was probably around 1.5-1.6 per cent late last year.