I was having a discussion with someone the other day about interest rates, the OCR, and how we should think about what has been going on in recent years. The person I was talking to was worried that, whatever short-term support lower interest rates might be providing to demand, activity and employment, it was at the expense of simply pulling forward consumption. And (lifetime) income which is spent today can’t be spent again tomorrow.

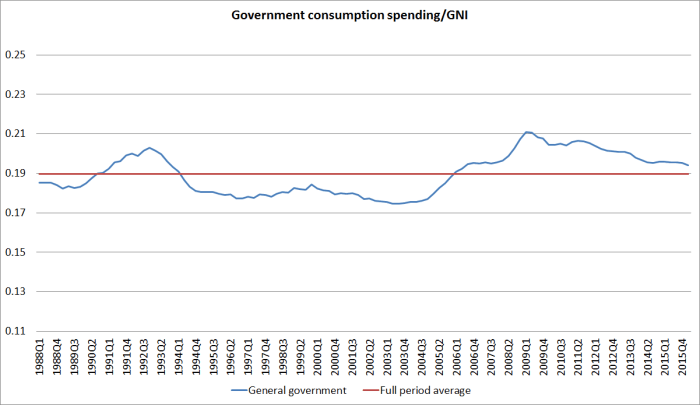

My usual starting point in such discussions is to draw attention to the little-recognized fact that consumption as a share of GDP has been largely flat in New Zealand for decades. There is some cyclical variability – consumption is a bit more stable than income, so the ratio tends to rise in recessions, and falls back as the economy recovers – but the trend has been almost dead flat. Actually, GDP isn’t the best denominator, because GDP measures what is produced here, not what accrues to New Zealanders (the difference is mostly the income earned by foreigners on the relatively large negative NIIP position New Zealand has). GNI is a measure of the aggregate incomes of New Zealanders, and here I’ve shown the various components of consumption relative to GNI since 1987, when quarterly national accounts data are available from (but using four-quarter running totals)

First, private consumption (including non-profits)

And then general government consumption

And then total consumption

I’ve shown full period averages for each. The only component of consumption where the share of GNI is a bit above the long-term average is general government consumption, the bit that is least likely to be sensitive to changes in interest rates.

Of course, if interest rates had been kept arbitrarily higher then consumption as a share of GNI might well be weaker now than it actually is, but there is really isn’t any sign of a great consumption splurge – a society desperately (over)spending now and thus increasingly likely to come a cropper later. (And as I’ve noted previously there is also nothing in any of these charts to suggest some large average wealth effect from the sharp rise in real house prices in recent decades – not surprisingly, since wealth is being transferred among New Zealanders, but no additional real wealth – future purchasing power – has been created in aggregate).

As we continued our discussion, the person I was talking to reminded me that the US picture has been somewhat different.

Here I draw on the OECD database, which has annual data for most of its members back to 1970. Here is total consumption (public + private) as a share of GDP for the United States, United Kingdom and New Zealand.

Even over the full 45 year period there is no upward trend in the consumption share in New Zealand.

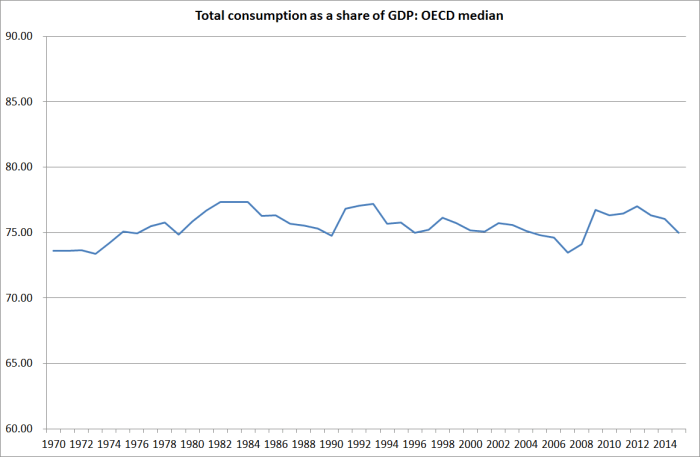

And here, on the same scale, is the consumption share of GDP for the median OECD country.

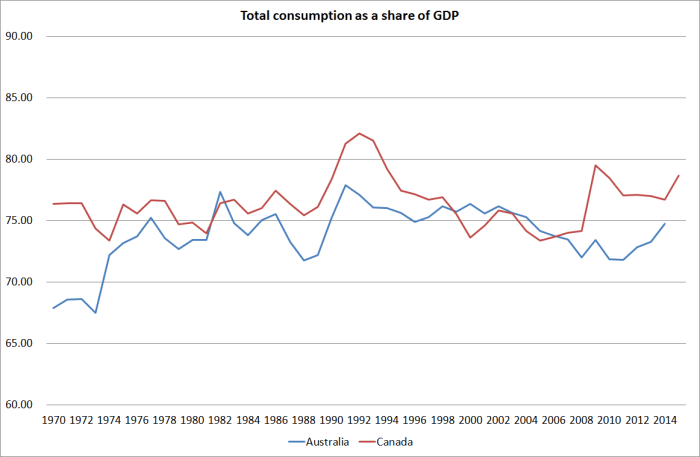

And here are Australia and Canada

Like New Zealand, no trend in either country, at least (see Australia) since the mid 1970s.

And here is Actual Individual Consumption (private consumption plus the stuff the government purchases but individuals consume directly eg healthcare and education) as a per cent of GDP for New Zealand, Australia and Canada.

I’m not quite sure what was happening to this data in New Zealand around 1985, but again for the last thirty years there has been no upward trend in consumption as a share of income.

What does all this mean? To be honest, I’m not quite sure. After all, if population growth rates have been slowing, less of GDP needs to be devoted to investment and that might mean more is available for consumption. But in the UK in particular, population growth rates have been somewhat faster in the last couple of decades than they had been previously. And things like defence spending trends can also complicate the picture – weapons system purchases are now part of investment, and we know in the US (and the UK) defence spending as a share of GDP is much lower than it was some decades ago.

I guess all I take from it is my original point. At least in New Zealand – and in most of the OECD – there is no sign that lower interest rates are resulting in a large scale bringing forward of consumption, for which at some point there must be payback. But that shouldn’t be too surprising. After all, interest rates are as low as they are for a good – if ill-understood by anyone – reason: in summary, because if they weren’t this low, consumption and investment spending would be even weaker. That, in a market economy, is really all interest rates do: they balance desired savings and investment patterns. Central banks that are too slow to adjust to changes in desired savings or investment patterns – at any given interest rate – can slow the adjustment, but in that respect a good central bank shouldn’t be trying to stand in the way of the sorts of real adjustments the private sector has underway, A century or more ago Wicksell introduced the concept of a neutral or natural interest rate. Those rates change over time, for reasons that aren’t always easy to recognize. Markets don’t need a fully convincing analytical reason – they just reflect the changing balance of demand and supply. Central banks shouldn’t let the difficulty of finding a good explanation stand in the way of allowing what would be the market processes to work

But quite why consumption shares in the US and UK have risen so much is an interesting question – to which I don’t have any good answers right now.