In both The Post and the Herald this morning there are reports of interviews with executive members of the Reserve Bank’s Monetary Policy Committee: the Bank’s chief economist Paul Conway in The Post and his boss, and the deputy chief executive responsible for monetary policy and macroeconomics, Karen Silk in the Herald. In a high-performing central bank the holders of these two positions should be the people we look to for the most depth and authoritative background comment on monetary policy and economic developments. But in New Zealand we are dealing with the legacy of the Orr/Quigley years where we struggle to get straightforwardness, let alone depth and insight.

Now, to bend over backwards to be fair, interview responses will depend, at least in part, on what the journalist concerned chooses to ask. But then standard media training advice is to answer the question you wish they’d ask, not (necessarily or only just) the one they did. An interview with a powerful decisionmaker is a platform for the decisionmaker.

The Conway interview appears somewhat meandering and not very focused. I wanted to touch on three sets of comments in it.

First, asked about the transition after Adrian Orr’s sudden (and unexplained) departure, he says it is business as usual and it has been “a very smooth transition”.

“I think this institution is bigger than even Adrian Orr [it was certainly bigger – much bigger – as a result of Adrian Orr]……There’s a real sense of the ‘show must go on’ and it really has. We miss Adrian. It is a bit less fun around the place, less jokes going on – probably more appropriate jokes”, he smiles again.

So in addition to Orr being a bully, an empire builder, and someone well known for freezing out challenge and dissent, he also created an uncomfortable and inappropriate working environment? Or at least that is what Conway appears to be saying about the man who recruited him.

But you also wonder about just how straight Conway is being (and why the journalist didn’t ask more). After all, the Bank itself tells us there are big changes afoot (presumably consequent on the new Funding Agreement, prospect and actual). In the just over two months since Orr resigned, the top tier of management has been brutally slimmed down (credit to Hawkesby). At the start of March there was the Governor and an Executive Leadership Team of seven Assistant/Deputy Governors and one “Strategic Adviser”. Since then, Kate Kolich, Greg Smith, Sarah Owen, Simone Robbers and Nigel Prince have all either left already or we’ve been advised they will soon be doing so (none with an announced job to go to). Governor plus eight has been reduced to Governor plus four. And

That first group is Conway’s own level (though presumably the Bank will continue to need a chief economist). And then on down to the staff (and much of this is because Orr/Quigley massively blew the budget limit Grant Robertson had set for them and went on one last hiring spree last year). You somehow suspect that all is not exactly sweetness, light, and engagement at the Reserve Bank.

And then there was this

Conway is on record as a bigger-government sort of guy (we had his extra-curricular stuff last year, as an example) but what possessed him, interviewed as an MPC member and senior central banker, to suggest that more state interventions and bigger government might be “worth thinking about”? It simply isn’t in his bailiwick, and he shouldn’t have allowed himself to be dragged into responding to a hypothetical, especially about one outside the Bank’s responsibilities.

And finally, we got the meandering thought that “it’s possible that we get to a point where people just adjust their behaviours and ‘uncertainty’ becomes the new normal and we just get on with it. I’ve got no ’empirics’ to base that on – it’s just, I think, a very interesting thought-stream.”

Really? A “very interesting thought-stream” that people do in fact adapt to the world as it is? Startling and insightful (not).

Then, of course, there is his boss, Silk. Most serious observers regard her as fundamentally unqualified for her job, and not the sort of person who would be likely to be on an MPC anywhere else in the world, let alone as the deputy primarily responsible for monetary policy. She can be counted on to safely deliver speeches on operational topics that others have written for her, and to answer purely factual questions at MPS press conferences and FEC about what has happened to swap yields and mortgage rates. And that is about all.

She also seems to have a mindset in which rates being paid on existing mortgages are what matter rather than the rates facing marginal borrowers and purchasers. Perhaps it is what comes from a non-economics background in a bank? Thus, in the Herald interview we are told that she claimed that “the effects of the 225 basis points of OCR cuts the committee had delivered in less than a year were yet to be widely felt”. The journalist added some RB data on average actual mortgage rates which might appear to back that up. Of course, expected cash flows matter as well as actual ones – if your fixed rate mortgage is going to roll over in a couple of months onto a much lower rate that will almost certainly be affecting your comfort, confidence, and willingness to spend now. But more to the point, marginal rates for people looking at buying a property or otherwise taking on new debt have come down a long way, and were already down a long way months ago. This chart is from the Bank’s own website, showing short-term fixed mortgage rates.

As at yesterday, rates were a few basis points lower again than the end-April rates shown here. 200 basis points plus down from the peak, and that not just yesterday. And falling wholesale rates, which underpin these falls in retail rates, also affect the exchange rate, another important part of the transmission mechanism. (And, of course, with all Silk’s focus on the cash flows of existing borrowers, she never ever mentions the offsetting changes in the cash flows for existing depositors – I’m of an age to know!)

So far, so predictable (at least from Silk). But then there was this (charitably I’ll assume the word “fulsome” was not hers)

Reasonable people might differ over the inflation outlook and the required future path for the OCR, except that we were told in the MPS that there was unanimous agreement from the MPC to the forecast path for interest rates. And that is a path that is lower from here than the path published (again unanimously) in the February MPS (the deviation begins after the May MPS, not at it). In other words, not only did the February path show some further easing from (where they expected to be, and were, by) May onwards, but the May path shows even more easing from here forward.

And yet Silk talks of a “much stronger easing signal” sent in February.

Frankly, they seem all over the place. If the Committee (as it did) unanimously agrees to publish a (somewhat) steeper downward track than the one you had before then either you have an easing bias – always contingent on the data of course – or you made a mistake in adopting the track you did. And if you are comfortable with the track, it feels like a mis-step for the temporary fill-in Governor to announce that there was no bias. I guess Silk might have got stuck having to cover for her fill-in boss, but it is a pretty poor look all round. Surely (surely?) they must have rehearsed lines about biases before the press conference? Surely, if so, someone pointed out the disconnect between the proposed words and the chart above?

And finally from Silk we learn that “price stability is one of the conditions you need for growth”. It simply isn’t – and the economists on the committee are usually much more careful, with the standard central banker line being that price stability, or low and stable inflation, is the best contribution monetary policy can make (many muttering under their breath that that contribution isn’t necessarily very large). Not to labour the point but the economy was still growing, reaching its most overheated point in late 2022, when core inflation was around its worst.

All in all, not a great effort at communications from the MPC this week. As I noted in my post on Thursday, there was none of the prickly frostiness of Orr, and no sign of deliberately or conscious setting out to mislead Parliament, but it simply wasn’t a very good performance. And while Hawkesby is new to the role, chairing MPC and acting as its prime spokesperson on the day, Conway and Silk have no such excuse. Someone flippantly suggested that perhaps there is something about May and the MPC – last May was when the MPC went a bit wild talking of raising rates further (the OCR was still going to be above 5 per cent by now), and then Conway tried to blame his tools, rather than the judgements of him and his colleagues, for the associated forecasts.

If the government is at all serious about a much better, world class, Reserve Bank, they need to work with the Board to find a Governor who will lift the game and the Governor/refreshed Board will need to work with the Minister to produce a stronger MPC. It would seem unlikely that in such an improved Bank/MPC there would be a natural place for either Conway or Silk, pleasant enough people as they may be.

Procrastinating this morning, I asked Grok to write a post in my style on yesterday’s Monetary Policy Statement. Suffice to say, I think I’ll stick to thinking and writing for myself for the time being. Among the many oddities of Grok’s product was the conviction that Adrian Orr was still Governor. Mercifully that is not so, even if – despite all the questioning yesterday – we are still no closer to getting straight answers on the explanation for the sudden, no-notice, accelerated departure of the previous Governor. Perhaps responses to OIAs will eventually help, but some basic straightforwardness from all involved – but especially Quigley and Orr himself – would seem the least that the public is owed, especially after all the damage wreaked on Orr’s watch.

Yesterday’s Monetary Policy Statement certainly made for a pleasant change of tone. Stuff’s Luke Malpass captured it nicely: “A lack of journalists being upbraided at times for not reading the materials in the hour allowed, or for asking the wrong question, was a change from previous management”. I watched about half of the Bank’s appearance at FEC this morning, and it was as if it was a whole different Bank. Not necessarily any deeper or more excellent on substance, but pleasant, respectful, engaged people accounting to Parliament, as they should. And, setting the standards low here, there wasn’t any sign of attempts to actively mislead or lie to the committee (Orr, just three months ago in only the most recent example).

I don’t have any particular quibbles with yesterday’s OCR decision. It was probably the right thing to do with the hard information to hand, but we won’t know for quite some time whether it really was the call that was needed. The NZIER runs a Shadow Board exercise before each OCR decision where they ask various people (mostly, but not all, economists) where they think the OCR should be at this review and in 12 months time, and invites them to provide a probability distribution. I’m not part of that exercise but I put my rough distributions on Twitter earlier in the week (in truth the blue bars should probably have been distributed in a flatter distribution – we really do not know)

The Bank’s projection for the OCR troughs early next year at 2.85 per cent and, as the scenarios they present reinforce again, there is a great deal of uncertainty about just what will be required (and not just because of the Trump tariff madness and associated uncertainty).

One of the interesting aspects of yesterday was that for only the second time in the six year run of the MPC that there was a vote (5:1 for a 25 point cut rather than no change). But, of course, being the non-transparent RBNZ we do not know which member favoured no change, so cannot ask him or her to explain their position, let hold them to account or credit them when time reveals whether or not it was a good call. As it happens, despite the vote the MPC reached consensus on a forecast track for the OCR and since that track embodies a rate below 3.5 per cent as the average for the June quarter and yesterday’s was the final decision of the June quarter, I’m not sure what to make of what must really have been quite a small difference. The bigger issue remains that there is (almost always) huge uncertainty about what monetary policy will be required over the following three years (the standard RB forecast horizon) and yet never once has any MPC member dissented from the consensus track. Groupthink still appears to be very strong. And notwithstanding the Governor’s claim that there is “no bias” one way or the other for the next move or the next meeting, the track – which all the MPC agreed on – clearly implies an easing bias (even if not necessarily a large one for July rather than August).

Hawkesby, unprompted, was yesterday championing the standard approach under the agreement with the Minister which enjoins the committee to seek consensus and only vote as a last resort. He acknowledged it is now an unusual model internationally, but claims it was preferable because it means – he claims – that everyone enters the room with a completely open mind about what should be done, whereas in a voting model people tend to enter the room with a preconceived view. Perhaps it sounds good to them, but it simply doesn’t ring true (and there is no evidence their model – which, among other things, saw them lose the taxpayer $11bn – produces better results in exchange for the reduction in transparency and accountability.)

It rang about as false as yesterday’s claim from the chief economist that the uneventful (in markets) transition when Orr resigned was evidence for the desirability of the decisionmaking committee. I’m all in favour of a committee (although a better, and better designed committee) but my memory suggested (and the numbers seem to confirm) that there were also no market ructions when Don Brash resigned, in the days of the single decisionmaker model.

There were a few things worth noting in the numbers. First, the Reserve Bank expects much weaker GDP growth than the Treasury numbers released with the Budget last week (Treasury numbers finalised in early April)

and as a result, significant excess capacity persists for materially longer than in the Bank’s February forecasts

And I’m still not sure where the rebound (above trend growth reabsorbing all the excess capacity) is really supposed to come from, on their telling, given that the OCR is still above their longer-term estimate of neutral, and never drops below it in the projection period. Reasonable people can differ on where neutral is likely to be (when the OCR was last at this level, less than three years ago, the Bank thought neutral was nearer 2%, now they estimate close to 3%), but it is the internal consistency (or lack of it) that troubles me.

I had only two more points to make, one fairly trivial, but the other not.

The trivial one first. In the minutes there was this paragraph about the world economy.

I don’t have any trouble with the (“weak world”) bottom line, but two specific comments puzzled me. The first was that difference in tone in the commentary on fiscal policy in China and the US: one might use “sizeable fiscal stimulus” (with no negative connotations) and of the other (and much more negatively) “fiscal policy could place strains on the sustainability of its public debt”. It wasn’t at all clear that the MPC realises that China’s government debt is almost as large as the US’s, and as a share of GDP has been increasing (and is expect to increase) much more rapidly than that of the US.

In a similar vein, this chart from the recent IMF Fiscal Monitor suggests that on IMF estimates China is already in a deeper fiscal hole, needing more fiscal adjustment (% of GDP) than the US to stabilise government debt.

Of course, the rest of the world is much more entangled with US government debt instruments than with Chinese ones, but it was a puzzling line nonetheless.

I’m also at a loss to know quite what the MPC was getting at with the line about ‘the decline in the quality of macroeconomic institutional arrangements [was] likely to result in precautionary behaviour by firms and households’. Not only is it not clear what decline they are talking about – are the Fed and the ECB not still independent, and the PBOC still far from it, and fiscal policy seems to have been on its current track for some years (in multiple countries). Is Congress bad in the US? For sure, but it has been so for a long time. I guess it might have been the relaxation of the German debt brake they had in mind, but….probably not. I was also a bit unsure how all this was supposed to play out. If, for example, there was an increased perceived risk of government debt being inflated away, wouldn’t the rational reaction be to increase purchases of goods and services on the one hand, and real assets on the other to get in before the inflation? Private indebtedness tends to rise when interest rates are modest and inflation fears are rising. In the end, who knows what they meant. Which isn’t ideal. They should tell us.

The more important issue is the Reserve Bank’s treatment of fiscal policy, where the bad old ways of Orr were again on display yesterday, in ways that really should undermine confidence in the Bank’s analytical grasp (and, frankly, its willingness to make itself unpopular by speaking truth in the face of power).

In his press conference yesterday the temporary Governor was asked about the impact of the Budget on the projections and policy decisions. He noted that they were glad to have all the information but that really it hadn’t made much difference, noting that any stimulus from the Investment Boost policy was offset by the impact of spending cuts. This is made a little more specific in the projections section of the document (a small increase in business investment, and on the other hand “on net, lower government spending reduces inflationary pressure”).

Readers with longer memories may recall that this issue first came to light a couple of years ago. Until then, for many years, the Bank had presented the impact of fiscal policy on demand primarily through the lens of the Treasury’s fiscal impulse measure, which had originally been developed for exactly that (RB) purpose. The Treasury has made some changes to that measure a few years ago which, in my view, reduce its usefulness to some extent, but certainly doesn’t eliminate it. Treasury continues to present the numbers with each Economic and Forecast Update. The basic idea is that increased taxes reduce aggregate demand and increased spending increases demand, but (for example) some spending is primarily offshore and thus doesn’t directly affect domestic demand. It is a best approximation of the overall effects on domestic demand of changes in fiscal policy. You can have a positive impulse while running a surplus (typically, if the surplus is getting smaller) or a negative one with a deficit (typically, if the deficit is getting smaller). It is straightforward standard stuff.

And yet two years ago the Bank simply stopped talking about this approach and replaced it with an exclusive focus on government consumption and investment spending (ie excluding all transfers – a huge component of spending – and the entire revenue side). This sort of chart has appeared ever since

and, probably not coincidentally, projections of (real) government consumption and investment have been trending downwards over that entire period. (This was the same vapourware I referred to in Monday’s fiscal post, where both Grant Robertson and Nicola Willis have repeatedly told us – and Treasury – that future spending will be cut.).

Back when this started, I OIAed the Bank for any research or analysis backing this change of approach. Had there been any of course they would already have highlighted it. There was none. But the switch had allowed the Governor to wax eloquent about how helpful fiscal policy was being, even as by standard reckonings (Treasury, IMF, anyone really) that year’s Budget had been really quite expansionary, complicating the anti-inflation drive.

The temporary Governor – who is presumed to be seeking the permanent job – seems, whether consciously or not, to be engaged in the same sort of half-baked analysis that avoids saying anything that might upset the government. Yes, on the Treasury projections government consumption and investment spending are projected to fall. But what does the Treasury fiscal impulse measure show?

At the time of the HYEFU last December, the sum of the fiscal impulses for 24/25 and 25/26 fiscal years was estimated to be -0.47 per cent of GDP (with a significant negative impulse for 25/26, thus acting as a drag on demand). By the time of last week’s Budget, not only was the impulse for 25/26 forecast to be slightly positive (this is consistent with, but not the same as, the structural deficit increasing) but the sum of the impulses for the two year was now 0.7 per cent of GDP positive. Fiscal policy, in aggregate is adding to demand (and by materially more than estimated at the last update). And the incentive effect of Investment Boost on private behaviour is on top of that.

Absent some serious supporting analysis from the Bank or its temporary Governor for its chosen approach (focus on just one bit of the fiscal accounts), it looks a lot like an institution (management and MPC) that now prefers to avoid ever suggesting that the fiscal policy effects might ever be unhelpful. After all, all else equal a positive fiscal impulse reduces the need and scope for OCR cuts – and we all know (we see their press releases) how ministers love to claim credit for OCR cuts.

If there is a better explanation, they really owe it to us. If they aren’t any longer happy with Treasury’s particular impulse estimate, they have the resources to come up with their own. But there is no decent case for simply ignoring developments in the bulk of the fiscal accounts. Wanting the quiet life simply isn’t a legitimate goal for a central banker, and if Hawkesby continues with the dodgy Orr approach – and he has been part of MPC all along – it does call into question his fitness for the permanent job. It isn’t the Reserve Bank’s job, except perhaps in extremis, to be making calls on the merits or otherwise of the fiscal choices of governments, but they are supposed to be straight with us (and, by default, with governments) on the demand and activity implications of those choices. They aren’t at present.

After the discussion in my post yesterday on the Investment Boost subsidy scheme announced in the Budget I thought a bit more about who was likely to benefit the most from it.

The general answer of course is the purchasers of the longest-lived assets.

Why? Because if you have an asset which IRD estimates to have a useful life of 100 years, your straight line depreciation deduction normally would be 1% per annum for each of those 100 years. But under investment boost, you get to do almost the first 21 years of deductions in the first year (the 20% Investment Boost deduction plus your 0.8% normal depreciation), and then the annual deduction each year thereafter is reduced by a little. But money today is very valuable relative to money given up (ie higher taxable income because of reduced future annual deductions) decades hence.

If on the other hand, you have an investment asset that has an estimated life of only 5 years (and there are many of them) it would normally be depreciated (straight line) at 20% per annum. Under Investment Boost, you get to deduct 36 per cent in year 1, but that additional depreciation upfront is clawed back over only the following four years. The Investment Boost additional upfront deduction has a positive present value, but it is fairly modest for such short-lived assets.

And what are the longest-lived assets? They will mostly be buildings. And, as we know, last year the government (with Labour’s support) moved to abolish tax depreciation altogether on commercial buildings (with an estimated useful life in excess of 50 years).

And that hugely magnifies the advantage of the Investment Boost policy for purchasers of new commercial buildings. Not only are they very long-lived assets but because there is no general tax depreciation on these assets, there is no depreciation clawback. The 20 per cent Investment Boost deduction is just pure gift (recall that the actual value to companies of all these deductions is 28 per cent of the value of the deduction itself – the company tax rate).

I did a little illustrative exercise in the table below, comparing the present value of the Investment Boost deduction for three different types of assets: commercial buildings, a winch (which IRD estimates has a 10 year useful life), and a printer (IRD estimates a five year useful life). Under the policy, in year 1 you get to deduct 20 per cent of the value of the asset plus normal depreciation calculated on the remaining 80 per cent. I’ve evaluated each option using a discount rate of 5 per cent (choice of discount rate won’t change the relative story across assets).

On plausible scenarios, Investment Boost is much much more beneficial to purchasers of commercial buildings than it is to most other assets (eight times as much for the same capital outlay on an asset with a life of five years[but see update at end of post]). There are, of course, other business assets with longer useful lives than 10 years (my winch example) but if you skim through the IRD schedule not that many more than 15.5 years.

And this a sector that just a year ago the government thought should get no tax depreciation at all…..

And a reminder, per yesterday’s post, that the IRD Fact Sheet on this policy says that (new or extended) rest homes will get to benefit from this (substantial) deduction, but that rental accommodation built afresh for any demographics to live in will not.

I challenge you to find the intellectual coherence in that.

Of course, you wouldn’t have got from anything announced on Budget day the sense that new commercial building purchasers were going to be by far the biggest winners. The Minister’s press release on the policy talks of how

To achieve that growth, New Zealand needs businesses to invest in productive assets – like machinery, tools, equipment, vehicles and technology.

But not a mention of commercial buildings. And perhaps more strangely, there is no discussion at all in the IRD/Treasury RIS of which sectors will benefit most, let alone the consistency with last year’s policy initiative on tax deprecation for commercial buildings, or of the rather anomalous situation where some new commercial residential accommodation (rest homes) gets the subsidy, while most of that market doesn’t. Quite extraordinary really.

It needn’t have worked out that way. Had the policy been set up to allow (say) double the normal rate of depreciation, until the asset was fully depreciated – rather than a flat 20 per cent in the first year – then there’d have been no benefit for commercial buildings at all (and whatever the merits of that at least it would have been consistent from one year to the next). Doing it in combination with restoring tax depreciation for commercial buildings might have involved initial backtracking but would at least have the merit of some consistency and coherence now.

UPDATE: A commenter notes that I really should compare scenarios with replacement at the end of the asset’s useful life. That is right. It will matter for the absolute comparison between 5 and 10 year assets (reduces the PV margin of a 10 year asset to 15% or so), and for the absolute scale of advantage of commercial buildings, but – since there is no clawback at all in respect of commercial buildings – it does not change the point that Investment Boost most strongly favours commercial building investment. Moreover, and all else equal, an investor with even a mild degree of risk aversion would favour cash in hand (20% immediate deduction on a 100 year life asset) over the uncertainty of the deduction regime at each replacement of shorter-lived assets.

On two separate themes; aggregate fiscal policy, and the Investment Boost initiative.

Aggregate fiscal policy

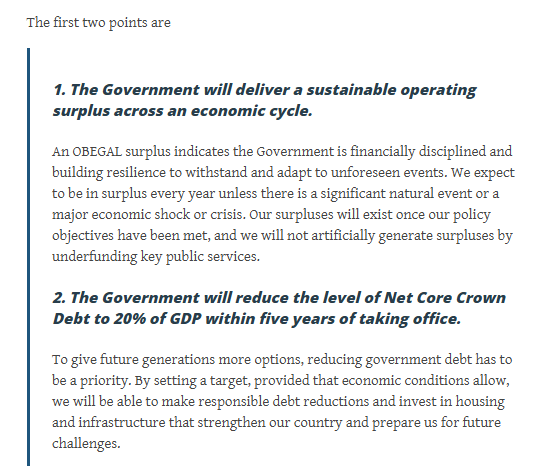

Over the weekend for some reason I was prompted to look up the Budget Responsibility Rules that Labour and the Greens committed to in early 2017 (my commentary on them here). At the time, the intention seemed to be to fix in the public mind a sense that these two parties of the left would nonetheless be responsible and prudent fiscal managers (as I recall a fair bit of the more left wing parts of the bases of the two parties lamented the agreement for giving much too much ground to what might have been thought of as orthodoxy).

And what were they promising?

The debt measure they were using at time had been 24.6 per cent of GDP in June 2016.

To which one can only say, those were the days:

the last time there was an OBEGAL surplus was the year to June 2019, and neither government nor opposition now seem bothered by the forecast of another 3.4 per cent of GDP deficit in 25/26 (just the same as the latest estimate for 24/25). Under the current government, the preferred deficit measure has been changed, against Treasury advice, to make things seem less bad. The current government’s long-term fiscal objectives (in the Fiscal Strategy Report) still include maintaining on average “over a reasonable period of time” a zero operating deficit, but there is little practical sign it means anything to them (or that Labour now would be less bad)

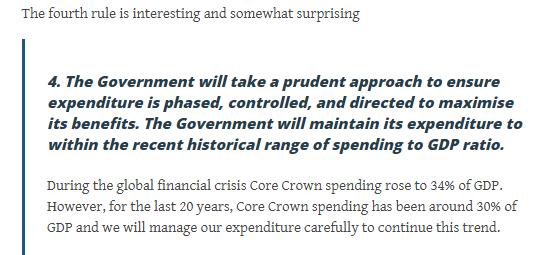

core Crown expenses are projected to be 32.9 per cent of GDP in 25/26, up slightly from 32.7 per cent in 24/25, and down only a touch on the 33 per cent actual for 23/24. Back when Labour and the Greens made those 2017 commitments core Crown expenses were a touch under 30 per cent.

debt measures have chopped and changed (and the current government was stuck with the additional debt their predecessors took on, although have not hesitated to take on much more since). These days, net core Crown debt is about 42 per cent of GDP. The government’s long-term fiscal goal is stated to be getting into, and keeping that measure in, a range of 20-40 per cent of GDP, but even on their rose-tinted fiscal forecasts that measure is projected to be 45.5 per cent of GDP by June 2029 (NB, that will be seven years on from the end of Covid as a big budgetary item). Meanwhile, Labour seems uncertain whether they’d attempt to even keep this debt measure below 50 per cent of GDP.

A political party today that seriously pledged to do what Labour and the Greens promised in 2017 to do (and by 2019, net core Crown debt was below 20 per cent, OBEGAL was in surplus, and core Crown expenses were below 30 per cent of GDP) would almost certainly be slammed as dangerous, extremist, unrealistic etc. So far have things fallen, under Labour and under National.

Meanwhile, too many journalists still seem to accord some degree of seriousness to fiscal projections for the end of the forecast horizon (four years out, so currently the year to June 2029). When the date for the crossover point from deficit to surplus keeps getting pushed out (and more recently, the Minister’s definition changes to make things easier), people should eventually realise that there is little or no substance to these numbers. They might be generated by The Treasury, but they aren’t some sort of best unconditional forecast, but rather the best forecast conditional on whatever successive ministers tell Treasury will be their policy for several years ahead (the end of the forecast period always, by construction) being well beyond the following election). The problem is that even if ministers honestly believe what they tell Treasury at any point in time (and probably they mostly do), it isn’t then anything more than a statement of good intention, perhaps even wishful thinking.

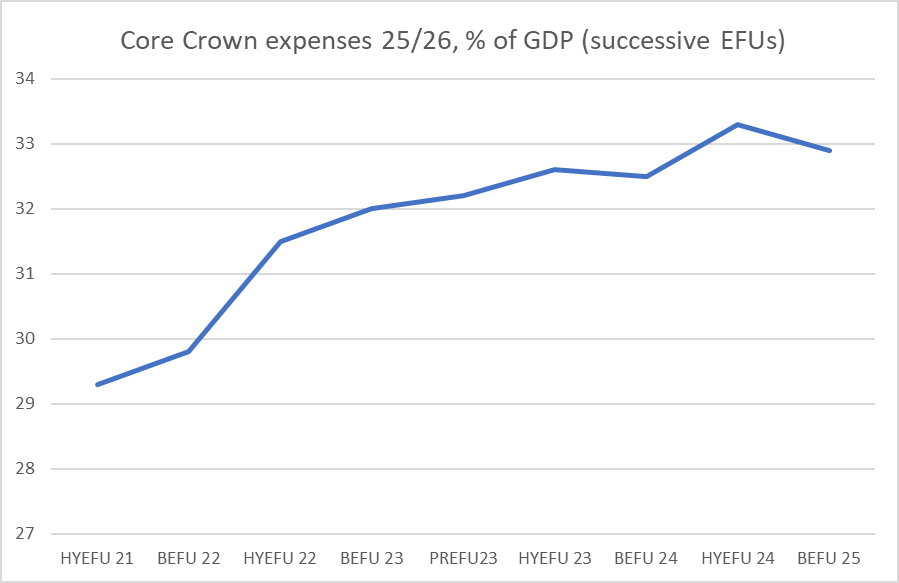

As an illustration of the point, consider this chart which shows projected core Crown expenses for 2025/26 as a share of GDP in successive Treasury economic and fiscal updates, going back to the end of 2021. The biggest further increases happened under Labour, but the line has continued to trend up under the current government.

Now, sure, further out the projections show core Crown expenses falling as a share of GDP, but that is sort of my point. Such projections are just vapourware. Exactly the same trend showed in the projections Treasury did under Labour (HYEFU21 to PREFU23 in this chart). It is easy, and perhaps appealing, to show such downward trends in future. It is quite another thing – politically rather than technically – to actually deliver. In both of the last two Budgets there has been plenty of hullabaloo (from politicians left and right) about expenditure cuts. But whatever the merits of those cuts, the bottom line remains that most of the proceeds have been used to increase other spending (some tax cuts last year)….and thus core Crown spending as a share of GDP is not actually falling.

Journalists, in particular (since politicians will politick), would be well-advised to ignore pretty much everything in the Treasury fiscal forecasts beyond the financial year to which the Budget actually relates (25/26 in this case), the year for which Parliament is actually being asked to make specific concrete appropriations. Most of the rest is vapourware.

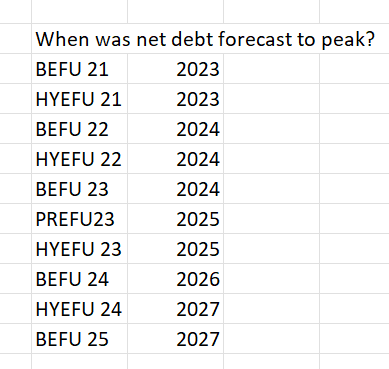

In a similar vein, here is a little table I stuck on Twitter on Saturday. The peak in net debt remains consistently two years ahead of whichever of five years’ Budgets one is looking at.

The government’s fiscal strategy seems to be not very different from that of the last couple of years of the previous government – do nothing about the long-term and in the short-term spend just as much as you possibly can without scaring the horses by blowing out the fiscal projections for net debt peaks and deficit crossovers too much in any one go.

Treasury are somewhat caught in the middle in all this. They have to forecast on the basis of fiscal policy as communicated by the Minister. That might be inescapable, but as I’ve argued previously in a PREFU context, maybe it would make sense to require Treasury to do a parallel set of forecasts showing the main fiscal variables on (a) unchanged tax rates (as at present), and b) maintaining the real per capita level of central government purchases (health, education, defence, Police etc) and the current programmes of transfers and income support. Those latter shouldn’t of course be treated as set in stone – efficiencies can be made, and different governments can have different priorities – but the expected cost if none of the expected deliverables are changed is still useful information, both for ministers (who may well already get something similar) and those seeking to hold them to account.

Investment Boost

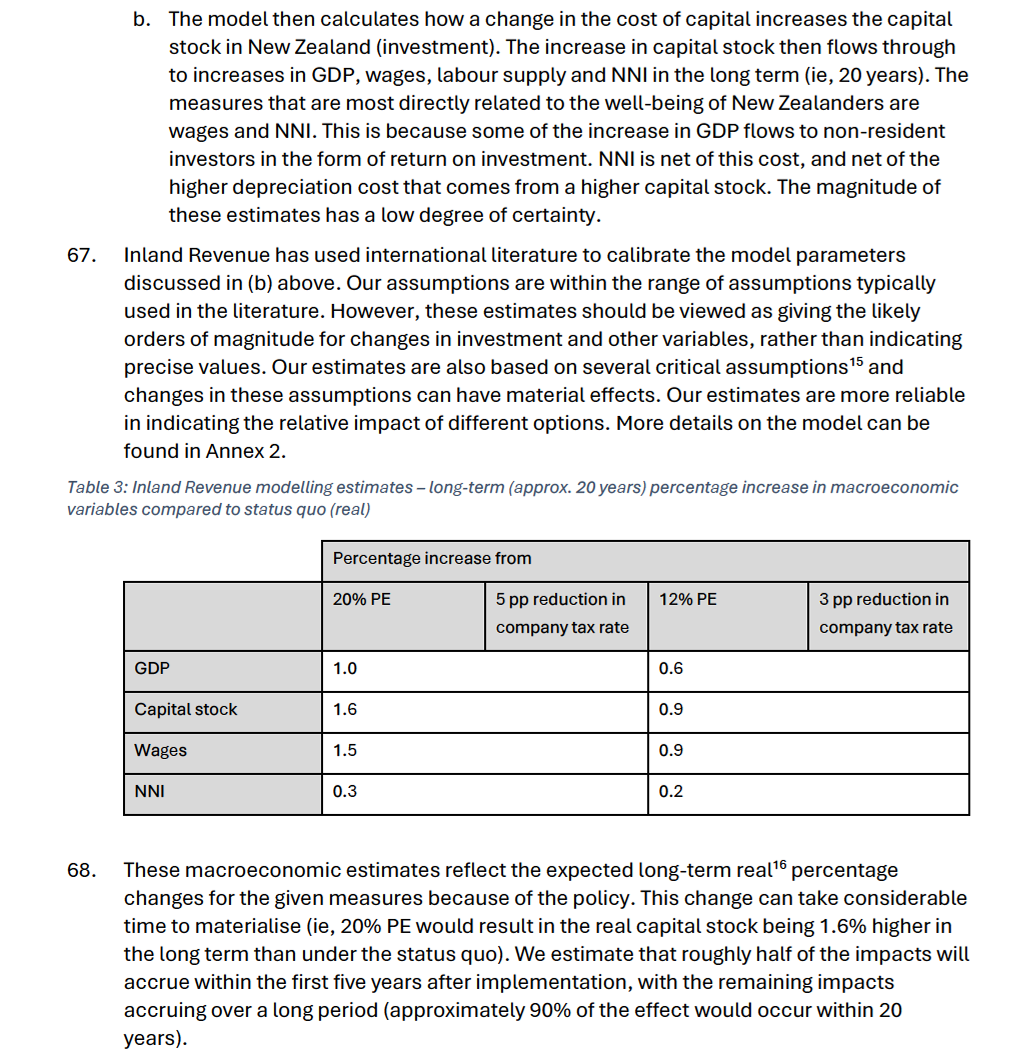

Having been promised, by the Minister of Finance herself, “bold steps” in the Budget to address economic growth and productivity underperformance, in the end it all came down to a single measure, the so-called Investment Boost. In my quick post last Thursday I was mostly focused on the fact of the single measure and the rather underwhelming forecast change to our longer-term growth prospects (the level of GDP lifts by 1 per cent, not getting there fully for more than 20 years). [Note that this is quite similar to the then-estimated long-run effect of the 2010 tax-switch reform, which involved a switch from personal income to consumption tax and a slight increase in the corporate tax burden.] Considered against the size of gap between New Zealand average productivity and that of OECD leaders (60 per cent or more), it would represent little more than rounding error, even if the case for the new policy measure itself was strong.

I don’t envy IRD and Treasury having to come up with estimates of the economywide long-term impact of an intervention like this investment incentive. Their Regulatory Impact Statement is here, and it reports that while there have been various experiments with such policy interventions in other countries in fact there doesn’t seem to be much in the way of robust evaluations (and often these investment incentives have either been time-limited and/or applying to a materially more restricted range of assets than Investment Boost).

This is the bit of the RIS where they describe the economywide results

Note that in the new steady state (many years hence) GDP is 1 per cent higher than otherwise, and the capital stock is 1.6 per cent higher. Since it is stated (and both IRD and the Minister have confirmed) that the results include an increase in jobs/hours (increase in total use of labour), it is a bit difficult to see how there is likely to be any material increase in total factor productivity at all. Among the other oddities is that if total wages are rising by more than GDP, and yet the capital stock in increasing even more, the model must be generating quite a reduction in rates of return to capital. Why that is, and how plausible it is, I’ll leave to the specialists.

But perhaps more worthy of attention is that last line in the table. NNI is net national income (ie net of depreciation, and national= benefits to New Zealand residents, as distinct from “domestic” which is things generated in New Zealand, whether by New Zealand residents or foreign investors), and by far the best measure of the economic gains (or otherwise) to New Zealand. Note that NNI in New Zealand is currently about 80 per cent GDP, so – on this particular model – only 25 per cent of the lift in GDP flows through to economic benefits to New Zealand residents ((0.3/1)*0.8). Most of the GDP gains accrue to foreign investors (something IRD is certainly not hiding, but obviously wasn’t being advertised by the government). Now, to be clear, I am all in favour of facilating foreign investment, but as with almost any policy intervention the test is whether whatever benefits foreigners may pick up result in sufficient gains to New Zealanders. For interventions that cost NZ taxpayers’ lots of money (as this one does), gains to foreigners are not themselves a benefit. The question is whether they enable greater benefits for New Zealanders.

(Note that IRD makes the point that “the magnitude of these [absolute] estimates has a low degree of certainty”. But their best estimates are, presumably, what ministers had available to them.)

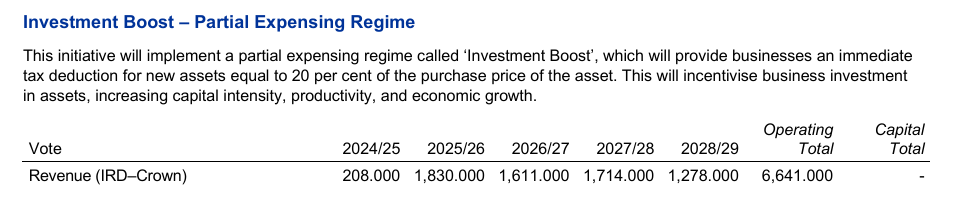

How large is the direct fiscal cost?

This is from the Summary of Initiatives document

Note that the cost in the early years is considerably higher than that by 2028/29. I presume that is reflecting the fact that for most investment the Investment Boost deduction is “just” changing the timing of the deduction (you get to write off 20 per cent of the cost in the first year, but then subsequent depreciation deductions over the remaining life of the asset are correspondingly reduced: for shorter-lived assets those reduced future deductions is significant once you are beyond the purchase year). In the RIS it is stated that that 2028/29 number is also the one they assume for the out-years (although presumably adjusting for inflation, and with a trend increase in the level of business investment – population growth etc).

And how much is $1278m per annum relative to net national income? Net national income, based on Treasury’s GDP forecasts, for 2028/29 is likely to be around $420 billion (80% of forecast GDP of $524bn), so the direct annual fiscal cost to New Zealand residents of this policy, once we get through the more expensive introductory phase, looks to be about 0.3 per cent of NNI. And that cost is being incurred every year, even though the NNI income gains don’t get up to 0.3 per cent for 20 years or more. Apply a discount rate of 8 per cent (as surely Treasury should insist on for what is a commercially-focused policy) and things could quickly look not overly attractive if a proper cost-benefit analysis had been done (it wasn’t). I guess there will be additional tax revenue on the additional GDP (tax/GDP is about 28 per cent), but again you don’t earn the tax until the real GDP benefits gradually flow through, while the fiscal cost is frontloaded. Time costs.

So perhaps the policy is net beneficial to New Zealanders (even if the scale is small). But is it an appropriate policy?

Reflecting on it further over the weekend, I’m not sure it is really either appropriate or particularly intellectually coherent. (I could add that I’m not greatly bothered by it being uncapped – so, for example, is the unemployment benefit which costs what it costs depending how many people end up unemployed, or interest deductibility etc. Government champions will no doubt add that since the point is to increase investment, if there is even more new investment than IRD/Treasury forecasts that is likely to be a good thing, not a bad thing. In some commentary I wondered if people realised that it is not a 20% grant, but rather a reduction in first year tax of 5.6 per cent of the purchase price (0.28*20).)

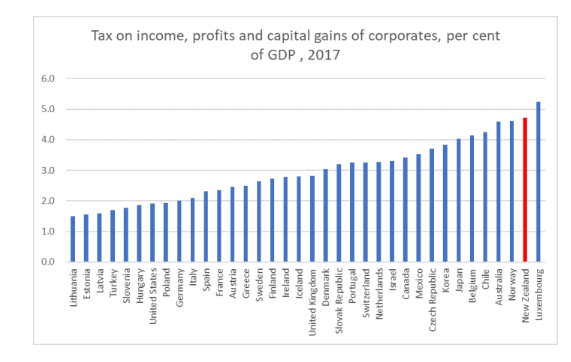

To me, there is little serious doubt that New Zealand has overtaxed business income. IRD show some of the cross-country comparisons, and they could have added this one (which is a few years old but was in the background documents for the Tax Working Group).

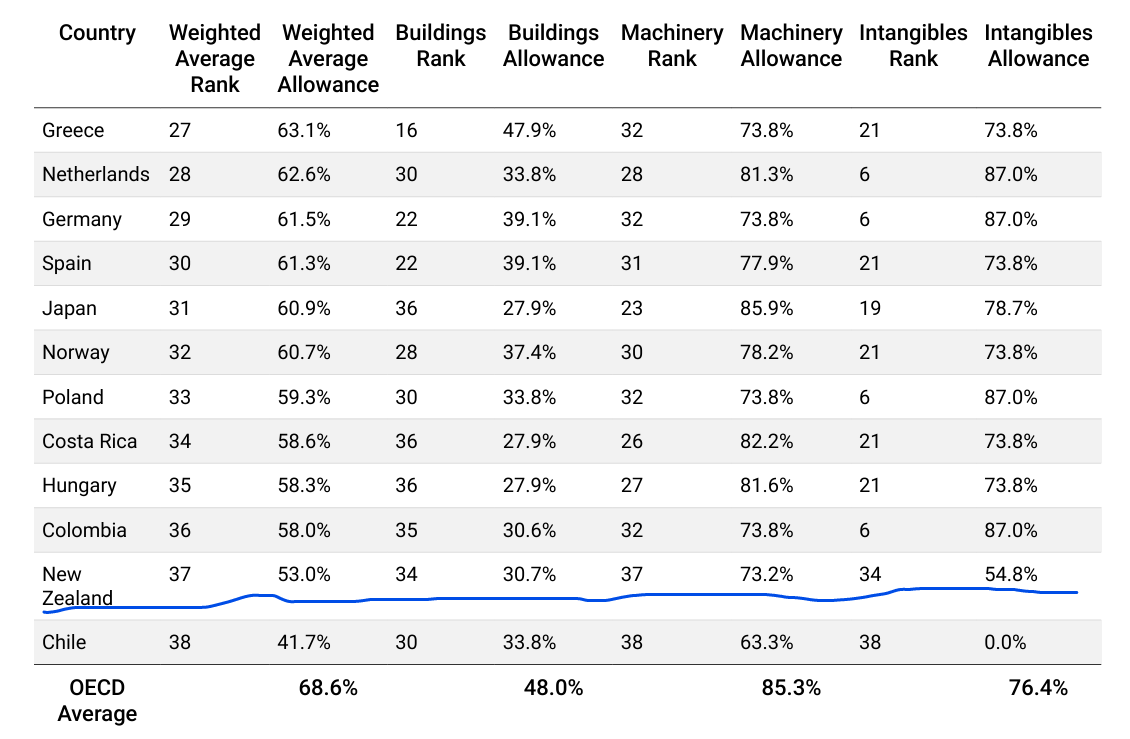

They could also have cited the Tax Foundation’s recent piece on capital cost recovery, depreciation etc. This was the bottom (worst) bit of their table for OECD countries showing the net present value of total write-offs over the life of an asset

Very few countries, for example, do as they should and inflation-adjust the value of assets to allow full real economic depreciation over the life of an asset.

But I’m still left uneasy about this particular Investment Boost initiative.

You hear a lot these days about “capital intensity” (lack thereof). For years, Treasury has talked up this rather mechanical growth accounting decomposition – business investment has been quite modest for decades, and so capital stock per worker has tended to lag – and this year ministers have taken to championing the line. And sure enough, from the RIS

There aren’t (in the views of ministers) enough capital assets, so we’ll offer an incentive (quite an expensive one) to encourage firms to have more capital assets.

The problem with this mentality – whether it is officials or ministers talking – is that it too easily fixates on symptoms rather than underlying economic causes. It never asks the question as to what is is about the New Zealand economy or its policy settings that means either New Zealand firms or foreign ones don’t seem to find that many profitable (after tax) opportunities available here (let alone look at what might be the best, or most cost-effective ways of addressing any issues thus identified.)

[Perhaps I should add here I’m old enough – as is Nicola Willis – to have been around when, a mere 15 years ago, New Zealand’s accelerated depreciation regime was scrapped – something signed off by the government (for which Willis worked at the time) and enthusiastically welcomed by Treasury (where I was working).]

Instead, there seems to have been a lurch to subsidise (one group of) inputs, even though outputs and outcomes are the things we should care about (much) more. Are more and more- highly-successful companies likely to also be engaging in more capital investment? Of course, but that is a different framing than one of “if we subsidise more capital goods will we see more highly successful companies?”

There are reasons to be ambivalent at best. For example, the goal of the policy appears to be more new investment (rather than higher GDP or NNI themselves), and thus you can get the subsidy for buying a new asset (or a used one from abroad), but not for buying an existing asset which some other might no longer need, or not be using as efficiently as your firm perhaps might. A whole new wedge is inserted, actively discouraging more efficient use of existing resources (TFP) in favour of subsidising more resources. Is that effect likely to be small enough not to worry about? Hard to tell, but (for example) very long-lived assets like factories and office buildings are caught in the net, and it is quite likely that a building won’t have the same best owner for its entire life. And what about vehicles? Some tradesman’s business fails and there is a vehicle to be sold – there is less likely to be a good recovery when a new or expanding business can get a subsidy on a new asset, but not on picking up an under-utilised existing one. And if, for small businesses in particular, there is an element of personal consumption in some business assets (be it the fancy ute or the higher-end-than-strictly-necessary laptop), lower rates of tax on business income would seem more likely to generate efficient outcomes than subsidising the purchase of capital assets. Again, perhaps small in the scheme of things, but not self-evidently an efficient approach.

Then, of course, there is the question of the intellectual coherence of the government’s approach to the taxation of business.

Last year, it was important (or so both government and Opposition believed) to remove tax depreciation from commercial buildings (otherwise the 2024 Budget numbers wouldn’t have added up), but this year new commercial buildings (including, according to the fact sheet, work already underway last Thursday) gets a 20 per cent deduction in the first year of purchase (absolutely huge upfront compared to the usual depreciation rates for buildings) – and since there is no clawback in reduced depreciation in later years, by far the biggest winners from this policy will be those adding new commercial buildings. So was tax policy last year correct – when it went one way on commercial buildings – or is correct this year, when it went quite the opposite direction? (And what was the net NNI effect of those two contradictory policy changes?)

Last year, the government also moved to reinstate interest deductibility in respect of residential rental property. The argument – which I supported totally – was that interest was and is a normal cost of doing business and as it was deductible for every other sort of company there were no good grounds for disallowing interest deductions on residential rentals. Firms need office, people need places to live, and in both cases owner-occupation will suit some but not others. So last year, residential rentals were a business like others, but this year……”residential buildings and most buildings used to provide accommodation are not eligible for Investment Boost – though there are explicit exceptions for some buildings such as hotels, hospitals, and rest homes”. Rest homes – you mean places where people live and are not owner-occupiers? I guess Rymans and the others will be happy, but where is the intellectual coherence? (And it is not as if the fact that depreciation is not allowed on residential rentals – itself a flawed policy- is a decent justification; after all, see above in respect of commercial buildings.)

Here is the main IRD/Treasury justification for excluding residential investment

As if the ultimate point was not improved household wellbeing, whether that arose via higher wages or lower real rental prices. And not a mention of last year’s policy stance, just officials and ministers again picking preferred types of capital assets.

I’m left rather ambivalent at best. There have been, and no doubt will be again (from whoever is in government) worse policies but this is simply a not very good one (despite the Minister touting apparent Treasury advice that there was something “optimal” about the 20 per cent). Had the government wanted to do something economically rational and rigorous around depreciation – see table above – it might have been better to have reinstated depreciation on buildings (residential and non) and inflation-indexed the depreciable values. But if it was coherent, it would have been a lot less catchy, since lots of machinery and software etc depreciates quickly and things like the inflation distortion matters less.

Finally, from a purely cyclical perspective, it isn’t impossible that there could be a larger short-term boost to demand and activity than implied by those long-term numbers.

Working back from the IRD cost estimate for 2025/26 ($1830m) and a company tax rate of 28 per cent suggests a base level of (covered) business investment of about $33bn. GDP is estimated at just over $450bn in 2025/26. Whatever the longer-term effects, perhaps there is reason to think the short-term lift to investment might exceed the long-term one: on the one hand, the enthusiasm effect among small businesses in particular (the policy seems to have gotten good headline reaction where it was presumably supposed to do so), and on the other, the risk/possibility that if there were to be a change of government after next year’s election this incentive could be wound back or abolished (the left would need money to fund their preferred initiatives, just as this government has – and the Greens, notably, have promised to increase company tax rates). If one were thinking of doing some capex in the next few years, the next 18 months or so might seem a particularly propitious time all else equal. A 10 per cent lift in business investment in a year would itself represent about a 0.7% lift to aggregate demand. At very least, and like all tweaky tool incentives, it will make for an interesting case study.

There were good things in the Budget. There may be few/no votes in better macroeconomic statistics and, specifically, a monthly CPI but – years late (for which the current government can’t really be blamed) – it is finally going to happen.

I went along to the Budget lock-up today (first time ever), mostly to help out the Taxpayers’ Union with their analysis and commentary.

At least from my (macroeconomist’s) perspective there were two areas to focus on when we were handed the documents at 10:30 this morning:

productivity and growth-oriented policy measures,

fiscal deficit etc adjustment

On the former, the government chose to title its effort today “The Growth Budget”. The Minister spoke today against a backdrop emblazoned repeatedly with that label.

You might remember that back in January the Prime Minister made a big thing of the need to accelerate growth in productivity and real incomes, not just on a cyclical basis. The Minister of Finance in announcing the Budget date in late January went further

They did not deliver.

There was a single growth-oriented initiative in the Budget; a provision under which firms will be able to write off 20 per cent of the cost of new investments in the first year, on top of the regular tax depreciation allowances. Whatever the substantive merits of the policy, the best Treasury estimate is that it will lift GDP by 1 per cent, but take 20 years to do so (the forecast gains are frontloaded, but even in five years time they reckon the level of GDP will have risen by only 0.5 per cent relative to the counterfactual). If that looks small, bear in mind that Treasury’s number seem to assume that this measure may actually worsen overall productivity as the Minister’s press release says they estimate the capital stock will rise by 1.6 per cent and wages will rise by 1.5 per cent (at her press conference she said this was because more people would be employed).

And that’s it. This in an economy where there has been no multi-factor productivity growth now for almost a decade (chart from Twitter this morning)

and, where as regular readers know, to catch up to the labour productivity levels of the leading OECD bunch (US and various countries in northern Europe), we’d need something like a 60 per cent increase in productivity.

It is simply unserious.

Things were no better on the fiscal side. Here, for today, I’m largely just going to rerun the notes I wrote for the Taxpayers’ Union and which are already in their newsletter

“This year’s Budget represents another lost opportunity, and probably the last one before next year’s election when there might have been a chance for some serious fiscal consolidation. The government should have been focused on securing progress back towards a balanced budget. Instead, the focus seems to have been on doing just as much spending as they could get away with without markedly further worsening our decade of government deficits.

“OBEGAL – the traditional measure of the operating deficit, and the one preferred by The Treasury – is a bit further away from balance by the end of the forecast period (28/29) than it was the last time we saw numbers in the HYEFU. There will be at least a decade of operating deficits, and even the reduction in the projected deficits over the next few years relies on little more than “lines on a graph” – statements about how small future operating allowances will be – that are quite at odds with this government’s record on overall total spending. Core Crown spending as a share of GDP is projected to be 32.9 per cent of GDP in 25/26, up from 32.7 per cent in 24/25 (and compared with the 31.8 per cent in the last full year Grant Robertson was responsible for). The government has proved quite effective in finding savings in places, but all and more of those savings have been used to fund other initiatives. Neither total spending nor deficits (as a share of GDP) are coming down.

“Fiscal deficits fluctuate with the state of the economic cycle, and one-offs can muddy the waters too. However, Treasury produces regular estimates of what economists call the structural deficit – the bit that won’t go away by itself. For 25/26, Treasury estimates that this structural deficit will be around 2.6 per cent of GDP, worse than the deficit of 1.9 per cent in 24/25 (and also worse than the last full year Grant Robertson was responsible for). There is no evidence at all that deficits are being closed, and the ageing population pressures get closer by the year.

“Some things aren’t under the government’s direct control. The BEFU documents today highlight the extent to which Treasury has revised down again forecasts of the ratio of tax to GDP (which reflects very poorly on Treasury who rashly assumed that far too much of the temporary Covid boost would prove to be permanent). But, on the other hand, the forecasts published today also assume a materially high terms of trade (export prices relative to import prices), which provides a windfall lift in tax revenue. Forecast fluctuations will happen, but the overall stance of fiscal policy is simply a series of government choices. Unfortunate ones on this occasion.

“A few weeks ago the IMF produced its latest set of fiscal forecasts. I highlighted then that on their numbers New Zealand had one the very largest structural fiscal deficits of any advanced economy (and that we were worse on that ranking than we’d been just 18 months ago when the IMF did the numbers just before our election). The IMF methodology will be a bit different from Treasury’s but there is nothing in this Budget suggesting New Zealand’s relative position will have improved. We used to have some of the best fiscal numbers anywhere in the advanced world, but as things have been going – under both governments – in the last few years we are on the sort of path that will, before long, turn us into a fairly highly indebted advanced economy, one unusually vulnerable to things like expensive natural disasters.”

With just a few elaborations/illustrations

First, here is the chart of tax/GDP

Even allowing for fiscal drag, quite how Treasury thought so much of the lift in tax/GDP was going to be more or less permanent is lost on me. They don’t really say.

Second, here is Treasury’s estimate of the structural (OBEGAL) balance as a per cent of GDP, showing recent years, and the forthcoming (25/26) financial year on the Budget announced today

The government seems to have become quite adept at rearranging the deckchairs (cutting spending that they consider low priority and increasing other spending) but they are choosing to make no progress at all in reducing the structural deficit. There were big savings found in this Budget, but none were applied to deficit reduction. Sure, the forward forecasts showing the structural deficit shrinking – never closing, even by 28/29 – but that is based on wishful “lines on a graph”, suggesting that the government intends to cut core crown expenses by a full 2 percentage points of GDP over the following three financial years, when on today’s forecasts expenditure as a share of GDP in 25/26 (32.9 per cent), will be a bit higher than in 24/25, and very slightly lower than in 23/24. The Ardern/Robertson government got by on 31.8 per cent in 22/23.

Finally, a reminder from Monday’s post

Depending on your measure we were (based on HYEFU/BPS numbers) worst or close to worst in the advanced world. Today’s Budget will have done nothing to improve that ranking. It should have.

The Budget is a lost opportunity, both on the fiscal and the productivity front. A couple of journalists at the lock-up asked for a summary label for the Budget. Some people had snappier versions, but mine was simply the “Deeply underwhelming Budget”.

Take a scenario, just as a thought experiment for now.

A new government gets elected, amid a lot of rhetoric about excessive increases in government spending and public service numbers. They pretty quickly move to require government departments – typically funded by Parliament through annual appropriations – to cut their spending. Typically these agencies were being expected to make cuts of 6.5 per cent or 7.5 per cent.

You are part of the governance structure – Board member, CEO, perhaps other top tier managers – of a powerful public agency, one that doesn’t really do “frontline services” types of stuff, but also one that isn’t directly funded by Parliament. Instead, by law every few years your agency agrees with the Minister of Finance how much you can spend for each of the following few years. When the government changes there is still a little more than 18 months to run on your latest agreement – itself in fact a variation agreement made just a few months earlier, just before the election, that had substantially increased how much your agency could spend over the remainder of the agreement period.

How would you react in such a situation? (How do you like to think you would have reacted?)

One other big agency in New Zealand, not directly funded by Parliament either and not directly subject to the new government’s savings target, early on decided that they really needed to move with the spirit of the new environment. They (Board and CE presumably) adopted a 6.5 per cent cut themselves, telling the media that while they weren’t within the formal government plans “there’s a very clear expectation that we’ll make material cost saving”.

It is the sort of way I hope I’d have behaved had I been in their shoes.

Of course, there is another approach. After all, under the law governing this agency, they get to set their own annual budget. Remember that there is an agreement with the Minister, but actually there is nothing in law that forces them to actually spend in line with that agreement, and no direct consequences if they fail to do so.

So, another possibility, knowing that your agreement has 18 months or so to run, is simply to ramp up your organisation’s budget for the final year of that old agreement – perhaps to levels well above what is approved in the agreement – and then when it comes time to negotiate with the Minister of Finance on spending levels for the following five years, you simply offer up a 7.5 per cent saving from the hugely increased budget you yourself had set just a couple of months previously (all while shuffling a few more costs into the out-of-scope category to reduce even further the extent of the proposed “savings”).

And that, readers, is the story of what Adrian Orr, Neil Quigley, and the Reserve Bank’s Board did. It was simply extraordinary. Quite shameless really. Longstanding readers will know I have not been a fan of the Orr/Quigley stewardship of the Bank but…..I wouldn’t have guessed, without seeing it in writing, that their approach would be quite so openly shameless.

I wrote about the Bank’s new Funding Agreement quite a bit last month. The final and most comprehensive post was here. There are still lots of unanswered questions, but in early May – just before I headed off to PNG – the Bank released on its website a redacted version of the initial bid they had put in to Treasury, as adviser to the Minister of Finance, in September 2024 (NB: Thanks to the RB comms person who got in touch to draw my attention to this document.) This was the bid for $1 billion or so ($981 million opex and $50 million capex, both over five years), for things that would be covered by the Funding Agreement (quite a lot wouldn’t). I only got back to reading it this week.

To recap, in September 2023 Grant Robertson had agreed to a (further) increase in the Bank’s Funding Agreement spending for the last two years of the 2020-2025 agreement. For the year to 30 June 2025, the amount of core operational spending Robertson had approved was $149.44 million. In that previous funding agreement there was also a separate line item for direct currency issue expenses and Robertson agreed that if they underspent that they could use the balance for general operating expenses. That gave them perhaps another $5 million.

So as the Bank’s Board and management approached the setting of the 2024/25 Budget those were the parameters they were supposed to be working within. But they also had information from the Minister of Finance about future intentions. On 3 April she had sent the Board her annual Letter of Expectation, which contained these points

In the general

And the specific

A responsible Board member would surely then have read the times and concluded that (a) they really needed to ensure that the 2024/25 Budget was, at worst, no higher than what Grant Robertson had allowed (bearing in mind that most agencies were getting those 6.5 to 7.5 per cuts even in 2024/25) and b) that any bids for the new 2025-30 Funding Agreement should be kept no higher (whether in real or nominal terms) than the 2024/25 approved level of spending. The focus was clearly intended to be reprioritisation, not further increases (in an organisation whose operating spending and staff numbers had already increased massively in recent years).

That is what a responsible Board member, looking to the public interest etc, would have done.

It wasn’t what the actual Board and senior management did. Instead, they adopted and published a budget for operating spending (captured by the Funding Agreement) of $191 million for 2024/25. Recall the spending that Grant Robertson – Mr Big Spender himself as Minister of Finance – had allowed the Bank for 24/25: $149.44m plus (on their budget) $5.5m from the underspend of their direct currency expenses allowance. The approved budget for 24/25, on items covered by the Funding Agreement, was 23 per cent in excess of what Robertson had allowed them, having already had those counsels of restraint from the Minister of Finance in her April letter. (As I noted in earlier post, there are mysteries around whether the Minister raised any objection at the time – she had to be consulted – which maybe an outstanding OIA will shed some light on, but that isn’t the focus of this post.)

That Budget was approved in June 2024 and in late August the Board approved the Funding Agreement bid (note that the current “temporary Governor” while not then a full Board member himself was in attendance throughout the relevant Board meeting). It was sent off to the acting Secretary to the Treasury, signed by both Orr and Quigley, on 13 September. And here from the second page of the covering letter (with a 40+ page document) was how their bid was sold, in blaring headline

In the body of the document it is repeated: “this approach would achieve savings of 7.5 per cent from our baseline operating expenditure, as requested by the Minister of Finance” [a footnote here refers the reader to the 3 April Letter of Expectation].

Ramp up the budget to 23 per cent above (previous Minister’s) authorised levels…..and then graciously offer a 7.5 per cent “cut” from that level. Really quite breathtaking… In fact in the previous paragraph they carefully noted that they had “had regard” to the Minister’s stance in her Letter of Expectation. Read, thought about, and then ignored would seem a more accurate description, all while attempting to spin Treasury and the Minister of Finance (nowhere in the document do they claim, for example, that the previous Funding Agreement levels were inadequate and needed to be increased. They simply take their own budget as the starting point, claim to have heeded the Minister, and end up “offering” a level of spending well above (in real and nominal terms) what even Grant Robertson had approved.

There is more sleight of hand when it comes to staff numbers. The government had seemed to be looking for agencies to be slimming staff numbers. In the year to June 2024 the Bank had increased staff numbers by 18 per cent (another 90 people), and in their Funding Agreement bid you get the sense that the “current headcount” was, in their view, roughly adequate for the things they had to do. And in fact later in the document they suggest that their preferred option would involve a net headcount reduction of 19 people. But what they didn’t point out to Treasury (or thus to the Minister) is that at the very same time they were handwaving about potential savings, they were going hell-for-leather to further increase staff numbers. We know this because the paper the Minister of Finance finally took to Cabinet in March tells us that the Bank increased staff numbers from the 601 at the end of June 2024 to 660 (FTE) by the end of January 2025. So they had no intention of actually cutting staff numbers, just of slightly slowing the rapid further increase they were already recruiting for. Now, sure, acute readers must have realised that such a huge operating budget increase in 2024/25 must have involved further increases in staff numbers, but….they were left to work it out for themselves. In a political and public spending climate in which Orr and Quigley and all the rest of them were only too well aware of sensitivities around rising staff numbers.

It is all pretty disreputable, shabby, and borderline dishonest (I didn’t spot an actual verifiable lie in the document; it was all in the self-serving misleading framing). Among the ongoing mysteries is why, when Treasury received this bid, they didn’t take a quick look and send it straight back with a demand that the Board revise the starting point back to (say) the previously approved (by Robertson) level of opex, not the Board’s own inflated budget which bore no relation to what the previous Minister of Finance had approved them spending. It wasn’t until March this year, after Orr’s departure, that there was finally a revised (much lower) submission.

And although the Orr/Quigley initial submission had strongly suggested that the Bank needed every one of the proposed billion dollars to function, reality seems to disagree. Just a couple of weeks ago the “temporary Governor” completed a restructuring of his top tier, in which the number of (very expensive) roles was reduced from about nine to four. Not hard to economise when you try (when the Minister’s choices finally compelled it). The Governor has gone of course (he’ll eventually be replaced), as have Assistant Governors Smith (finance), Kolich (data), Robbers (strategy, governance, and sustainability), Strategic Adviser Prince, and the grapevine reports that another of the Orr hires, Assistant Governor Owen (risk and legal) has also resigned. It is really only a start, since Board chair Neil Quigley and all the board members who approved and endorsed this egregious funding bid are still there (although the terms of two expire next month). And are we really to believe that all along the Deputy Governor, Hawkesby, hadn’t been endorsing the approach?

And then, of course, there is the lack of transparency. In that Funding Agreement bid they explicitly told Treasury that once a new agreement was reached “our intent is to publish the final version of our Funding Proposal on our website”. Which sounds quite good, but…. the new Funding Agreement was published on 16 April. It is now 20 May, and although they have published a redacted version of the first proposal (which is a start) there is no sign of the final revised March bid. In fact, I have an OIA request in for it

Just yesterday I heard back from the Bank

Of these:

the first relates to the question of whether the Minister ever pushed back on the proposed 24/25 budget

the second covers two specific and easily identified documents (the first now released – see above), and

the third is to shed light on whether the Board pushed back at all on what management was proposing (is the final version different in any material extent to what went to Treasury.

None of these documents will take any particular effort to find, and at least one they promised Treasury nine months ago they’d publish. But…..in the way of public sector obstructionism, they’ve just taken another six weeks to respond to a fairly straightforward request. Isn’t that convenient for them.

It really is staggering that a government-appointed Board chair could try it on quite as egregiously as Quigley did (in league with Orr) and still hold his very well-paid role ($200000 for a part-time role), including leading the process of selecting a nominee to be the next Governor.

Not that long ago, New Zealand’s fiscal balances looked pretty good by advanced country standards. Sure, the fiscal pressures from longer life expectancies were beginning to build – as they were in most of the advanced world – but in absolute and relative terms New Zealand still looked in pretty good shape.

Just a few months before Covid, in October 2019, the IMF published its half-yearly Fiscal Monitor, with the helpful cross-country comparative tables (whatever the merits of New Zealand’s own approach to measuring and reporting fiscal balances it doesn’t facilitate international comparisons).

This was how we’d compared with the median advanced country that year and the previous few.

Notes for this and several later charts:

“general government” (not central), the only meaningful basis for international comparisons

“primary” = ex interest (so reflecting current spending choices not legacy debt)

“cyclically-adjusted”, so looking through the state of the economic cycle. For Norway the data are not cyclically-adjusted (IMF only publishes cyclically-adjusted numbers for ex-oil Norway)

“advanced countries” = IMF classification for sovereign states (so ex Hong Kong), with Poland and Hungary added.

So under both National and Labour-led governments we were mostly running structural primary surpluses, and surpluses a bit larger than the median advanced country. Since our starting level of net public debt was lower than that of the median OECD country, using cyclically-adjusted overall balances our relative position was a bit stronger still.

Covid, of course, intervened, and in 2020 and 2021 most countries (including New Zealand) had really big fiscal outlays associated with supporting the Covid disruption to economic activity.

So fast forward to 2023. The Covid spending itself was by then a thing of the past.

The IMF released another Fiscal Monitor set of forecasts/estimates in October 2023 just a few days before our election (I wrote about the numbers here at the time). I’ve averaged the numbers for 2023 and 2024, but choosing either year individually wouldn’t make much difference. We now had among the larger structural primary deficits of any advanced country (again, the picture was a little less bad using the cyclically-adjusted total balance).

So that, as estimated by the IMF (who use national numbers for each country but do their own cyclical adjustment), was pretty much the situation the incoming government inherited at the end of 2023. They knew that New Zealand was estimated to have among the largest primary structural deficits advanced world – a choice (and it was pure choice) made by the outgoing government.

So what stance was taken by the incoming government in its first Budget this time last year? This chart is from the Budget Economic and Fiscal Update. Treasury’s own estimate of the structural deficit was that policy choices would widen the structural deficit for 24/25 slightly relative to the estimate for 23/24.

That wasn’t particularly surprising. There were expenditure cuts (and a tax increase) but there were also a number of tax cuts (much as had been promised by National in the election campaign).

Treasury estimates of the adjustments required to get to structural and cyclically-adjusted balance estimates can change with incoming data, but this chart was from last December’s HYEFU

There was still no sign of any improvement in the structural position, based on decisions already made (ie last year’s actual Budget as distinct from lines on a graph about possible future Budgets).

Which brings us to the most recent IMF Fiscal Monitor released a few weeks ago. This is how our cyclically-adjusted primary deficit now compares (for NZ, the IMF uses HYEFU/BPS information – they don’t impose their own guesses about fiscal policy itself): largest structural primary deficit among the advanced countries (and a far cry from the modest structural primary surpluses New Zealand governments ran – chose to run – last decade)

and here is the chart for the structural overall balance (ie including finance costs)

Not quite as bad, but still 4th largest deficits among advanced countries.

As I’ve shown previously, the net debt position is not yet particularly bad. Government debt as a share of GDP is still below that of the median advanced country, but that gap has been closing rapidly.

And one could add to the mix the repeated extension – by both governments – of the horizon for getting back to operating balance (currently, on the standard OBEGAL definition, both National and Labour seem agreed that 2029 is fine, at least until some other shock or pressure comes along).

It isn’t as if the financial markets are going to compel adjustment. If the net debt rises materially further a credit rating downgrade can’t be ruled out, but on its own that wouldn’t matter very much. It is more a question of our own choices and our own sense of fiscal responsibility and accountability.

Of course, there will be plenty of people – perhaps currently mostly on the political left – inclined to the view that if anything our governments should take on more debt. I’d largely agree with them that a somewhat higher level of debt is not likely to either raise interest rates very much or dampen potential GDP growth very much. My aversion to higher public debt is more about the demonstrated weakness of the political process in too many countries – not so much in New Zealand for a couple of decades, but again apparently now. It is easy to promise nice-to-haves (and both main parties have been guilty of this in recent years) when you don’t have to go to the voters and ask them for higher taxes now to pay for the handouts. Much more honest that if you want to increase (structural) spending – new or more expensive programmes – to raise taxes to pay for it. Failing to do that risks taking our country the way of places like France, the UK or the US – even before the demographic pressures really up the ante.

What will we see in the Budget? We’ll see I guess, but the Minister of Finance has announced a cut in the operating allowance for 24/25. That is no doubt fine and good, but relative to the scale of the structural imbalances – see charts above – it is pretty small beer, enough only to improve our ranking in those IMF charts by one place. Perhaps the Treasury’s estimation of cyclically-adjustment will have changed – for better or for worse – but we seem a long way from where we should be. And having chosen not to adjust last year, and with the three-party coalition chasing re-election next year, this year’s Budget was perhaps the only real hope left this term for getting back on fiscal track. To be sure, economic activity at present appears pretty weak, but a well-signalled tougher fiscal adjustment would normally be expected to be met by a looser-than-otherwise monetary policy (rather than further weakening economic activity). That, it seems, is not to be.

(The Opposition, of course, seems to differ only on the mix, not the extent of the fiscal imbalance they created and bequeathed, or the speed – sluggish at very best – with which it should be dealt with.)

But no doubt we will all be looking forward to the “bold” steps to lift economic growth etc

I saw this morning this chart in a tweet from a Canadian economics professor (prompted by the new ministerial appointments in Canada).

I was digging around in the list of former New Zealand Ministers of Finance anyway, and thought it might be interesting to try a New Zealand version. Responsible government here goes back to 1856 and so I dug out the previous occupations of those who have held the office of Minister of Finance (or Colonial Treasurer or Treasurer) since then. The list has 42 names (although several held the office on several separate occasions – Ward being the most recent to have been Minister of Finance four separate times, the last ending in 1930). Canada, reading from the chart above, appears to have had 43 federal Ministers of Finance since 1867.

Of our 43, 7 held office for less than six months (some of those early governments lasted for days or mere weeks). I could have excluded them from the chart below, but it doesn’t look as though doing so would materially alter the picture (although it would mean dropping our one engineer – Charles Brown (1856) – and the one builder (William Hall-Jones (1906)).